Quick Navigation

- Report Overview

- Key Takeaways

- By Product Type Analysis

- By Ingredients Analysis

- By Packaging Type Analysis

- By End-use Analysis

- By Distribution Channels Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

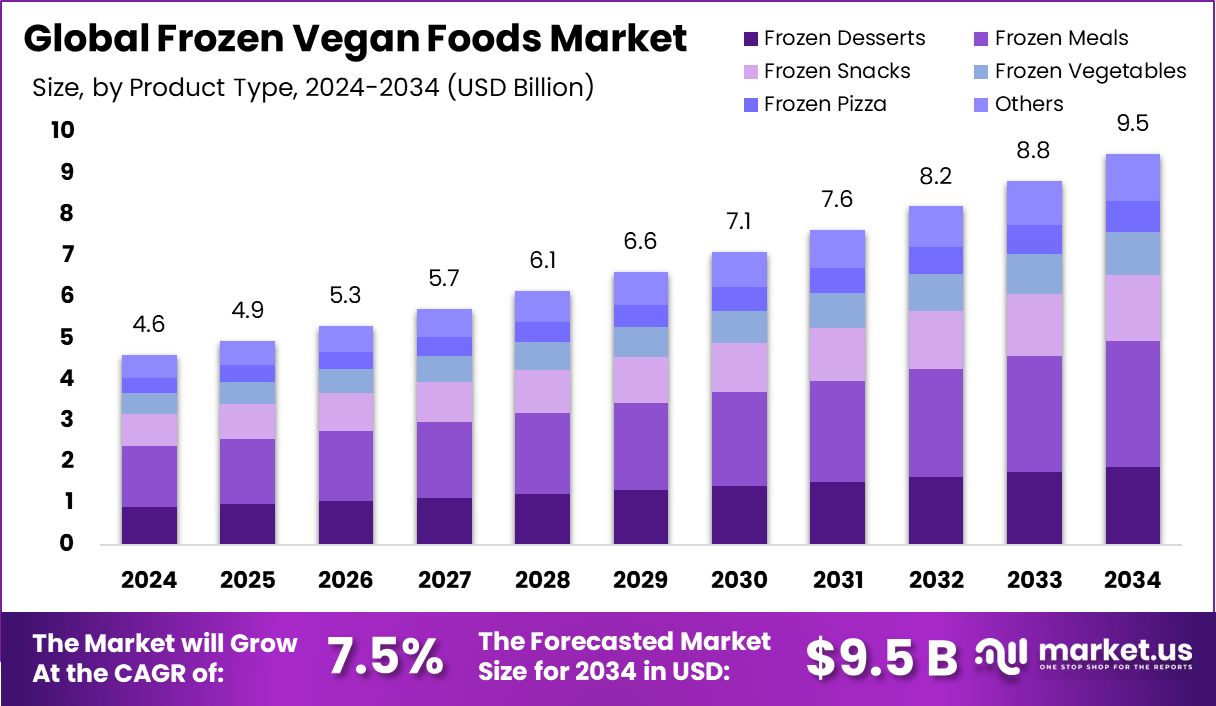

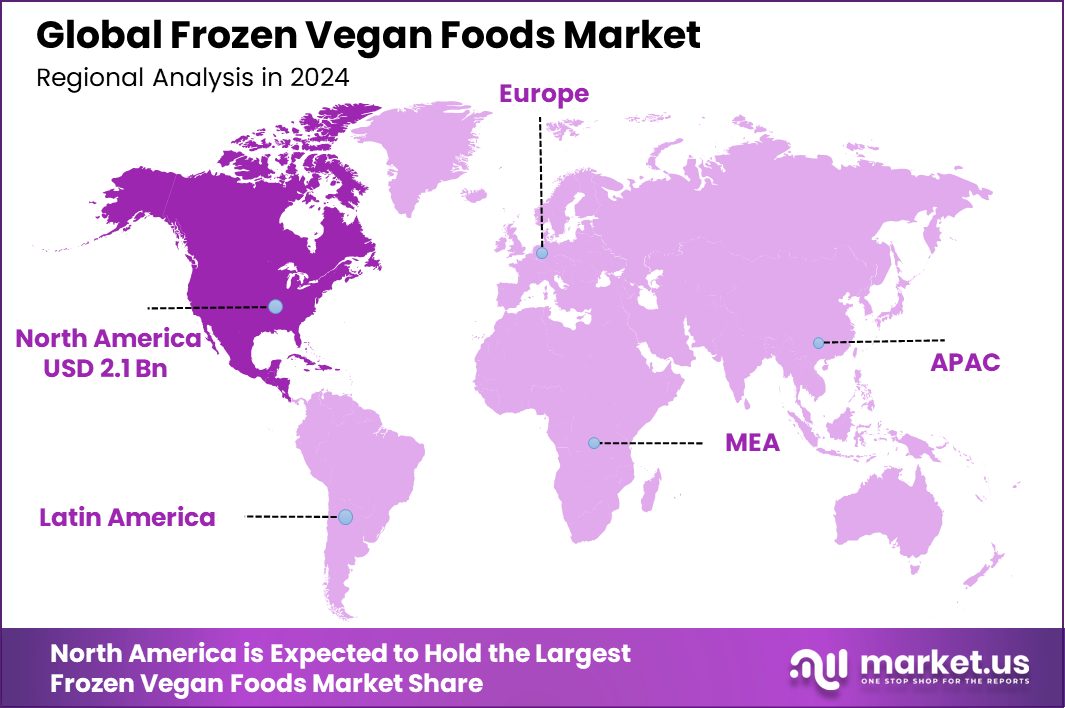

Global Frozen Vegan Foods Market is expected to be worth around USD 9.5 billion by 2034, up from USD 4.6 billion in 2024, and grow at a CAGR of 7.5% from 2025 to 2034. With a 46.20% share, North America leads frozen vegan foods industry expansion.

Frozen vegan foods are meals or ingredients that have been prepared without any animal products and are preserved through freezing. This category includes a wide variety of products such as vegetables, fruits, meat substitutes, dairy-free ice creams, ready-to-eat meals, and more. They cater specifically to the dietary needs of vegans and others looking to reduce their consumption of animal products.

The growth of the frozen vegan foods market is driven by several factors. Increasing awareness of animal welfare issues and the environmental impact of animal farming motivates many consumers to choose plant-based options. Additionally, the health benefits associated with a vegan diet, such as lower risks of heart disease, obesity, and hypertension, further propel the demand for these products.

Demand for frozen vegan foods is also bolstered by the convenience they offer. In today’s fast-paced world, consumers are looking for quick and easy meal solutions that align with their ethical and dietary preferences. Frozen vegan foods meet this need by providing nutritious and easy-to-prepare options that fit seamlessly into busy lifestyles.

Frozen vegan foods are growing rapidly, with vegan ice creams leading demand. Ben & Jerry’s now offers 19 vegan flavors, comprising 25% of its portfolio. With 75% of global consumers lactose intolerant, plant-based frozen desserts are becoming a mainstream choice.

Opportunities within the frozen vegan foods market are vast. Innovations in food technology have led to improvements in taste and texture, making plant-based alternatives more appealing to a broader audience. There is also significant potential for expansion in global markets where veganism is becoming more mainstream, coupled with growing consumer interest in health and sustainability.

Key Takeaways

- Global Frozen Vegan Foods Market is expected to be worth around USD 9.5 billion by 2034, up from USD 4.6 billion in 2024, and grow at a CAGR of 7.5% from 2025 to 2034.

- Frozen meals hold a 32.10% share in the frozen vegan foods market by product type.

- Grains dominate the ingredients segment, comprising 64.20% of the frozen vegan foods market.

- Multi-serve packaging types represent 47.30% of the market, highlighting consumer preference for convenience.

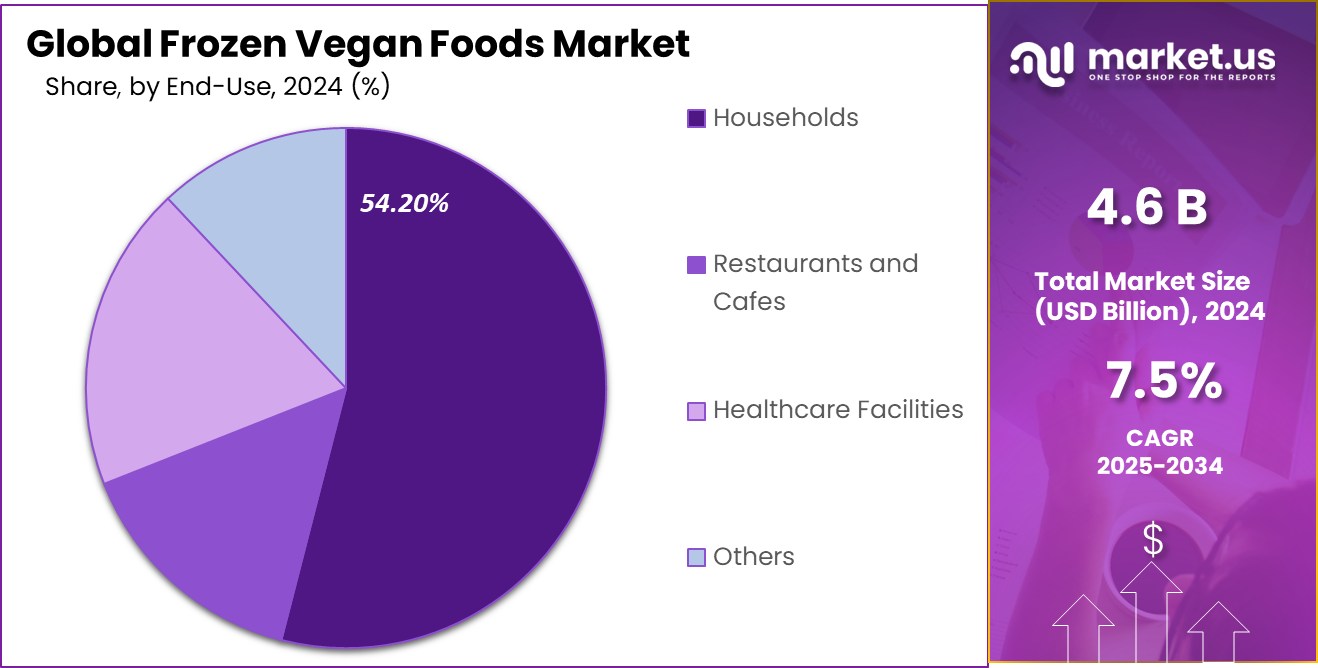

- Households are the primary end-users of frozen vegan foods, accounting for 54.20% of the market.

- Supermarkets and hypermarkets are key distribution channels, making up 38.20% of the market’s sales.

- Increasing plant-based diet adoption in North America drives USD 2.1 billion market growth.

By Product Type Analysis

Frozen meals hold a 32.10% share in the frozen vegan foods market.

In 2024, Frozen Meals held a dominant market position in the By Product Type segment of the Frozen Vegan Foods Market, capturing a 32.10% share. This segment’s prominence is primarily attributed to the increasing consumer demand for convenient, quick-to-prepare vegan options that do not compromise on nutritional value or taste. Frozen vegan meals, ranging from entrees such as vegan pizzas and pasta to ethnic cuisines like Indian and Thai, cater to a diverse palate while supporting a busy, health-conscious lifestyle.

The substantial share of frozen meals within the market underscores the significant shift in consumer eating habits, where time constraints often influence meal choices. The versatility and variety offered in the frozen vegan meals category have effectively addressed this need, making it a preferred choice among consumers who wish to adhere to a vegan diet without spending extensive time preparing meals from scratch.

This segment’s success is indicative of a broader trend towards plant-based diets, driven by factors including sustainability concerns, health awareness, and ethical considerations related to animal welfare. As such, frozen vegan meals continue to be a pivotal area of focus for producers looking to capitalize on the expanding market for plant-based foods.

By Ingredients Analysis

Grains dominate the market, comprising 64.20% of frozen vegan food ingredients.

In 2024, Grains held a dominant market position in the Ingredients segment of the Frozen Vegan Foods Market, with a 64.20% share. This substantial segmental dominance is primarily due to grains’ pivotal role in vegan diets as a source of essential nutrients, including fiber, proteins, and vitamins. Products such as frozen quinoa, rice dishes, and other grain-based meals cater to a growing consumer base seeking healthful, plant-based meal options that are both satisfying and nutritious.

The high proportion of grains in frozen vegan foods highlights their versatility and fundamental appeal among consumers aiming to balance dietary needs with convenience. Grains are easily adaptable to various cuisines and flavors, making them an ideal base for innovation in the vegan food industry. Their ability to blend with a range of seasonings and ingredients allows for a diverse array of products that can appeal to both vegan consumers and those looking to reduce meat consumption.

This segment’s growth is also a reflection of the increasing awareness and popularity of whole grains among health-conscious consumers, driving demand for more wholesome, easily accessible food choices. The ongoing development and marketing of grain-based frozen vegan foods are likely to continue as consumers increasingly prioritize health, wellness, and environmental sustainability in their dietary choices.

By Packaging Type Analysis

Multi-serve packaging is preferred, making up 47.30% of the market.

In 2024, Multi-serve held a dominant market position in the Packaging Type segment of the Frozen Vegan Foods Market, with a 47.30% share. This leadership is largely driven by the increasing consumer preference for bulk buying and family-sized food options that offer both convenience and value. Multi-serve packaging appeals especially to households looking for cost-effective solutions that minimize food waste and reduce the frequency of shopping trips.

The strong performance of multi-serve packaging in the frozen vegan food sector also reflects broader social changes, including a rise in family and group dining occasions at home. As consumers continue to seek meal options that are easy to prepare yet healthy and sustainable, multi-serve frozen vegan products meet these needs by providing larger portions that can be easily stored and reheated, offering a practical solution for busy families and shared living arrangements.

Moreover, the environmental aspect of multi-serve products, which typically use less packaging per serving compared to their single-serve counterparts, resonates well with the eco-conscious values of many vegan consumers. This segment’s prominence within the market underscores the alignment of consumer packaging preferences with broader lifestyle trends focusing on sustainability, health, and convenience.

By End-use Analysis

Households are the primary end-users, accounting for 54.20% of consumption.

In 2024, Households held a dominant market position in the By End-use segment of the Frozen Vegan Foods Market, with a 54.20% share. This significant market share highlights the strong preference among individual consumers and families for incorporating vegan options into their home cooking routines. The shift towards plant-based diets has been largely influenced by health considerations, ethical concerns, and environmental factors, making frozen vegan foods an appealing choice for home consumption.

The dominance of households in this market segment is further supported by the growing availability and variety of frozen vegan products tailored to home use. These products offer convenience without compromising on the nutritional integrity and taste expected by health-conscious consumers. The ease of preparation and storage of frozen vegan foods aligns well with the fast-paced lifestyles of modern consumers, who are increasingly looking for quicker meal solutions that fit their dietary preferences.

Additionally, the economic aspect of purchasing frozen foods for home use allows households to enjoy diverse vegan meals without the added expense of frequent dining out. This trend is likely to continue as more consumers become aware of the benefits of vegan diets and seek practical, family-friendly ways to integrate these foods into their daily lives.

By Distribution Channels Analysis

Supermarkets and hypermarkets distribute 38.20% of these products.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channels segment of the Frozen Vegan Foods Market, with a 38.20% share. This leadership is indicative of the significant role these retail giants play in making vegan products accessible to a broad consumer base.

Supermarkets and hypermarkets have been pivotal in introducing a diverse array of frozen vegan food options to shoppers, ranging from specialty items to mainstream vegan staples, thereby catering to an expanding demographic of health-conscious and ethically motivated consumers.

The prominence of supermarkets and hypermarkets in this market segment stems from their strategic placement, extensive reach, and ability to stock a wide variety of products under one roof. This convenience is a key factor driving consumer preference for purchasing frozen vegan foods from these outlets. Moreover, the visual appeal and organized layout of these stores make them an attractive shopping destination for consumers looking to explore and experiment with new vegan products.

Additionally, the aggressive marketing and promotional strategies employed by supermarkets and hypermarkets have significantly contributed to the visibility and availability of frozen vegan foods. These retailers often feature vegan products in prime in-store locations and offer promotional discounts, which help attract and retain customers looking for plant-based food options.

Key Market Segments

By Product Type

- Frozen Desserts

- Cakes

- Ice Creams

- Puddings

- Others

- Frozen Meals

- Breakfast

- Dinner

- Meals Kits

- Ready-To-Eat Meals

- Others

- Frozen Snacks

- Bites

- Patties

- Rolls

- Others

- Frozen Vegetables

- Green Peas

- Fire-Roasted Corn

- Edamame

- Butternut Squash

- Green Garbanzo Beans

- Zucchini

- Others

- Frozen Pizza

- Blackbird Pizza

- Vegan Margherita Pizza

- American Flatbread’s Vegan Harvest

- Daiya’s Meatless Meat

- Banza

- Sweet Earth Veggie Pizza

- Others

- Others

By Ingredients

- Grains

- Oats

- Quinoa

- Rice

- Others

- Plant-Based Proteins

- Pea Protein

- Soy

- Wheat Gluten

- Others

By Packaging Type

- Bulk packaging

- Multi-serve

- Single-serve

By End-use

- Households

- Restaurants and Cafes

- Healthcare Facilities

- Others

By Distribution Channels

- Supermarkets/Hypermarkets

- Health Food Stores

- Online Retailers

- Convenience Stores

- Club Stores

- Others

Driving Factors

Growing Awareness of Health and Environmental Benefits

The primary driving factor for the growth of the Frozen Vegan Foods Market is the increasing awareness of the health and environmental benefits associated with vegan diets. More consumers are becoming conscious of the impacts their food choices have on their health, with plant-based diets linked to lower risks of heart disease, diabetes, and obesity.

Additionally, environmental concerns play a significant role, as vegan diets are viewed as more sustainable compared to traditional diets reliant on animal agriculture, which is a major contributor to greenhouse gas emissions and deforestation.

This dual focus on personal health and ecological sustainability is compelling more people to choose frozen vegan foods, which offer the added convenience of easy preparation and long shelf life, fitting seamlessly into the eco-conscious consumer’s lifestyle.

Restraining Factors

Perception of Higher Cost Limits Market Growth

A significant restraining factor for the Frozen Vegan Foods Market is the perception of higher costs associated with vegan products. Many consumers view vegan foods, particularly specialty frozen items, as more expensive than their non-vegan counterparts. This price differential can deter budget-conscious shoppers, who might otherwise be interested in trying vegan options.

The higher prices are often due to the complex processing, sourcing of alternative ingredients, and smaller-scale production, which do not benefit from the economies of scale seen in more mainstream food products.

While the market is growing as manufacturers streamline production and achieve better economies of scale, the perceived premium pricing remains a barrier, potentially slowing down the adoption rate among a broader consumer base.

Growth Opportunity

Expansion into Emerging Markets Offers Significant Potential

A major growth opportunity for the Frozen Vegan Foods Market lies in expanding into emerging markets. As global awareness of veganism increases, countries that traditionally have lower consumption of vegan products are showing a rising interest in plant-based diets. This shift is driven by the growing middle class, increased access to information about health and sustainability, and urbanization.

By introducing frozen vegan foods to these new markets, companies can tap into a burgeoning consumer segment eager for diverse and convenient dietary options. Establishing a presence in these regions can be highly lucrative, especially if companies adapt flavors and products to local tastes and dietary habits, further encouraging the adoption of vegan food choices among new demographics.

Latest Trends

Innovative Plant-Based Alternatives Reshape Consumer Choices

One of the latest trends in the Frozen Vegan food market is the development of innovative plant-based alternatives that closely mimic the taste and texture of animal products. This trend is revolutionizing consumer choices, attracting not only vegans but also flexitarians and meat-eaters looking to diversify their diets.

Advances in food technology have enabled manufacturers to create highly palatable and satisfying options such as vegan meats, cheeses, and seafood, which are now widely available as frozen products.

These innovations are making it easier and more enjoyable for consumers to transition to or incorporate vegan foods into their diets. As these alternatives become more mainstream, they drive the market by meeting consumer demands for variety, convenience, and ethical eating.

Regional Analysis

North America dominates the Frozen Vegan Foods Market with a 46.20% share, reaching USD 2.1 billion.

The Frozen Vegan Foods Market is witnessing varied growth dynamics across different regions. North America dominates the market, holding a 46.20% share with a valuation of USD 2.1 billion, driven by a strong consumer shift towards plant-based diets, high awareness about health and sustainability, and well-established distribution channels in supermarkets and hypermarkets.

In Europe, the market is propelled by increasing consumer preference for eco-friendly and animal-free products, alongside supportive government policies promoting health and environmental sustainability. The region shows robust growth due to high demand in countries like Germany, the UK, and France, where veganism is becoming part of mainstream culture.

The Asia Pacific region presents significant growth opportunities with rising health consciousness and changing dietary habits, particularly in countries such as China and India. The region’s fast-growing middle class is increasingly adopting vegan diets, driven by both health considerations and ethical factors.

Meanwhile, Latin America and the Middle East & Africa are emerging as potential growth areas due to increasing urbanization and the influence of Western eating habits. Although these regions currently have smaller market shares, they exhibit potential for rapid growth as awareness and availability of vegan products increase.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key players in the global Frozen Vegan Foods Market are leveraging innovation, expanding product portfolios, and strengthening distribution networks to capture a growing consumer base.

Kellanova continues to dominate with its well-established brands, capitalizing on strong retail partnerships and consumer trust in frozen plant-based products. The company’s focus on health-conscious and convenience-driven offerings aligns well with the increasing demand for ready-to-eat vegan meals, reinforcing its market presence.

Conagra Brands remains a major player, benefiting from its diverse plant-based product range and deep penetration into retail channels. The company’s strategic efforts in reformulating frozen vegan products with improved taste, texture, and nutritional value cater to both vegans and flexitarians. By expanding its plant-based segment, Conagra is tapping into a growing preference for frozen meat alternatives and dairy-free products.

Beyond Meat continues to reshape the market with its plant-based meat alternatives, strengthening its footprint in the frozen segment. The company’s focus on clean-label ingredients and sustainable production processes enhances consumer appeal, particularly among environmentally conscious buyers.

Impossible Foods remains a significant market disruptor, bringing innovation to frozen vegan food offerings. With a strong research-driven approach, the company has successfully replicated the taste and texture of animal-based products, gaining traction in retail and food service channels.

Top Key Players in the Market

- Kellanova

- Conagra Brands

- Beyond Meat

- Impossible Foods

- Roncadin

- Unilever

- Wells Enterprises

- Amy’s Kitchen

- Maple Leaf Foods

- Nestle

- Yves Veggie Cuisine

- Daiya Foods

- Quorn

- Raised & Rooted (Tyson Foods)

- Chicago Town

- Turtle Island Foods

- Qishan Foods

- Cargill

- Gathered Foods

Recent Developments

- In 2024, Impossible Foods made significant strides in the frozen vegan foods sector. Notably, in May, the company expanded its product line by introducing Impossible™ Chicken Nuggets and Chicken Patties to select Whole Foods Market locations across the United States. These products offer high-quality protein and fiber, with no cholesterol, up to 35% less total fat, and up to 60% less saturated fat compared to traditional chicken products.

- In 2024, Chicago Town, a prominent frozen pizza brand, launched a £4.5 million marketing campaign to promote its new vegan offerings. The campaign, titled ‘Feed Your Urge; Go To Town,’ aimed to challenge the perception that frozen pizza is only for emergencies, positioning it as a convenient and indulgent meal option. The brand introduced four new products to supermarket freezers, including vegan options, to cater to the growing demand for plant-based foods.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.6 Billion |

| Forecast Revenue (2034) | USD 9.5 Billion |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Frozen Desserts (Cakes, Ice Creams, Puddings, Others), Frozen Meals (Breakfast, Dinner, Meals Kits, Ready-To-Eat Meals, Others), Frozen Snacks (Bites, Patties, Rolls, Others), Frozen Vegetables (Green Peas, Fire-Roasted Corn, Edamame, Butternut Squash, Green Garbanzo Beans, Zucchini, Others), Frozen Pizza (Blackbird Pizza, Vegan Margherita Pizza, American Flatbread’s Vegan Harvest, Daiya’s Meatless Meat, Banza, Sweet Earth Veggie Pizza, Others), Others), By Ingredients (Grains (Oats, Quinoa, Rice, Others), Plant-Based Proteins (Pea Protein, Soy, Wheat Gluten, Others)), By Packaging Type (Bulk packaging, Multi-serve, Single-serve), By End-use (Households, Restaurants and Cafes, Healthcare Facilities, Others), By Distribution Channels (Supermarkets/Hypermarkets, Health Food Stores, Online Retailers, Convenience Stores, Club Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Kellanova, Conagra Brands, Beyond Meat, Impossible Foods, Roncadin, Unilever, Wells Enterprises, Amy’s Kitchen, Maple Leaf Foods, Nestle, Yves Veggie Cuisine, Daiya Foods, Quorn, Raised & Rooted (Tyson Foods), Chicago Town, Turtle Island Foods, Qishan Foods, Cargill, Gathered Foods |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |