Quick Navigation

Report Overview

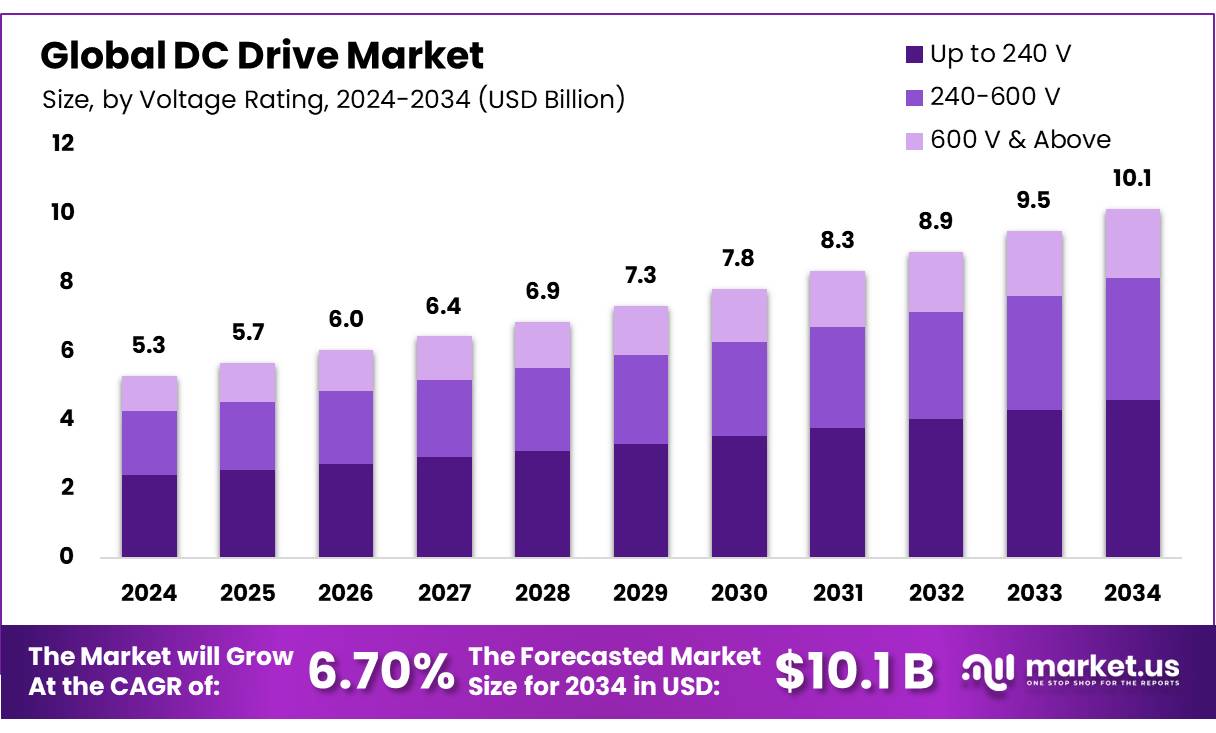

The Global DC Drive Market size is expected to be worth around USD 10.1 Billion by 2034, from USD 5.3 Billion in 2024, growing at a CAGR of 6.7% during the forecast period from 2025 to 2034.

DC drives are systems designed to control the speed of DC motors by regulating the voltage supplied to the motor. These drives are important for applications that require precise speed, torque, and direction control. The major advantages of DC drives include precise speed control, ease of speed reversal, and efficient torque management, especially at low speeds. DC drives also offer regenerative braking, which recovers energy during braking, enhancing overall energy efficiency.

Furthermore, their simpler and less expensive control methods, compared to AC drives, make DC drives the preferred choice in various industrial automation systems, such as controlling cranes, hoists, elevators, spindle drives, and paper production machines, where high accuracy and reliability are essential. Their ability to provide smooth and precise control makes them ideal for applications with varying speed requirements. The global market for DC drives continues to expand, driven by the increasing demand for efficient and reliable motor control solutions across sectors such as manufacturing, automation, and transportation.

Key Takeaways

- The global DC drive market was valued at USD 5.3 billion in 2024.

- The global DC drive market is projected to grow at a CAGR of 6.70% and is estimated to reach USD 10.1 billion by 2034.

- By voltage rating, 240-600 V accounted for the largest market share of 3%. Due to versatility in industrial applications.

- By power rating, Up to 250 kW accounted for the largest market share of 6%. Due to widespread use in medium-sized equipment.

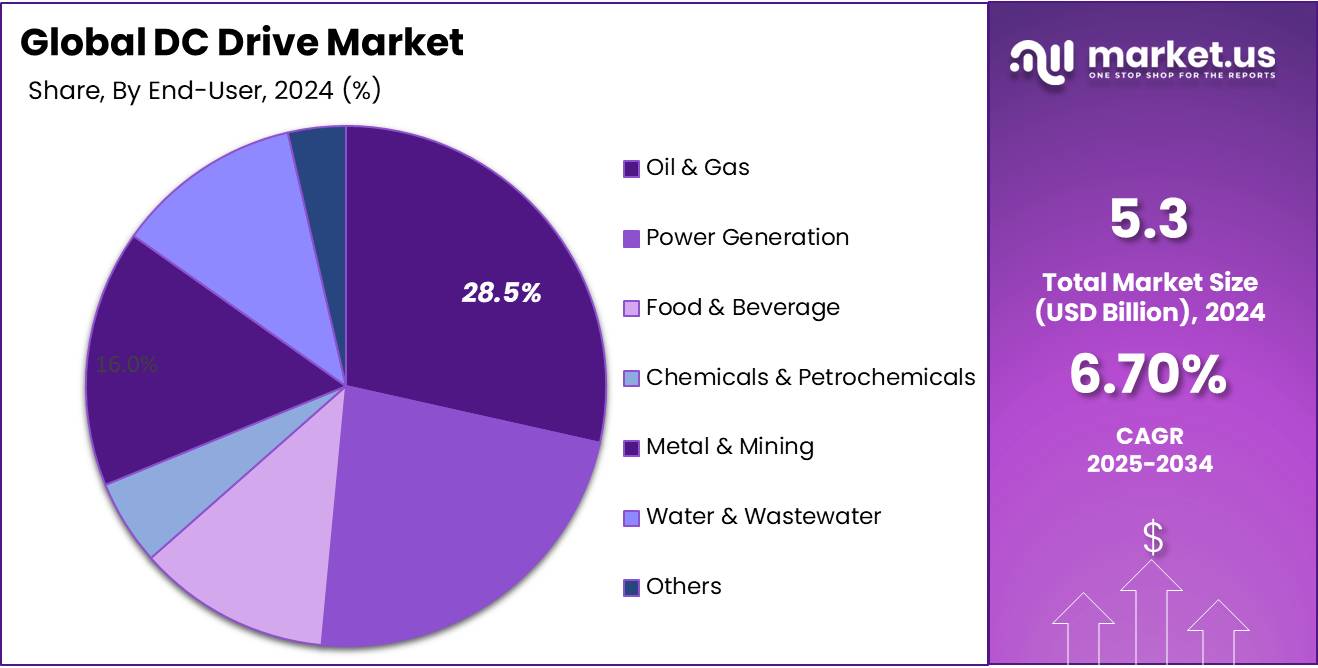

- By end-user, oil & gas accounted for the majority of the market share at 4%. Due to the high demand for energy solutions

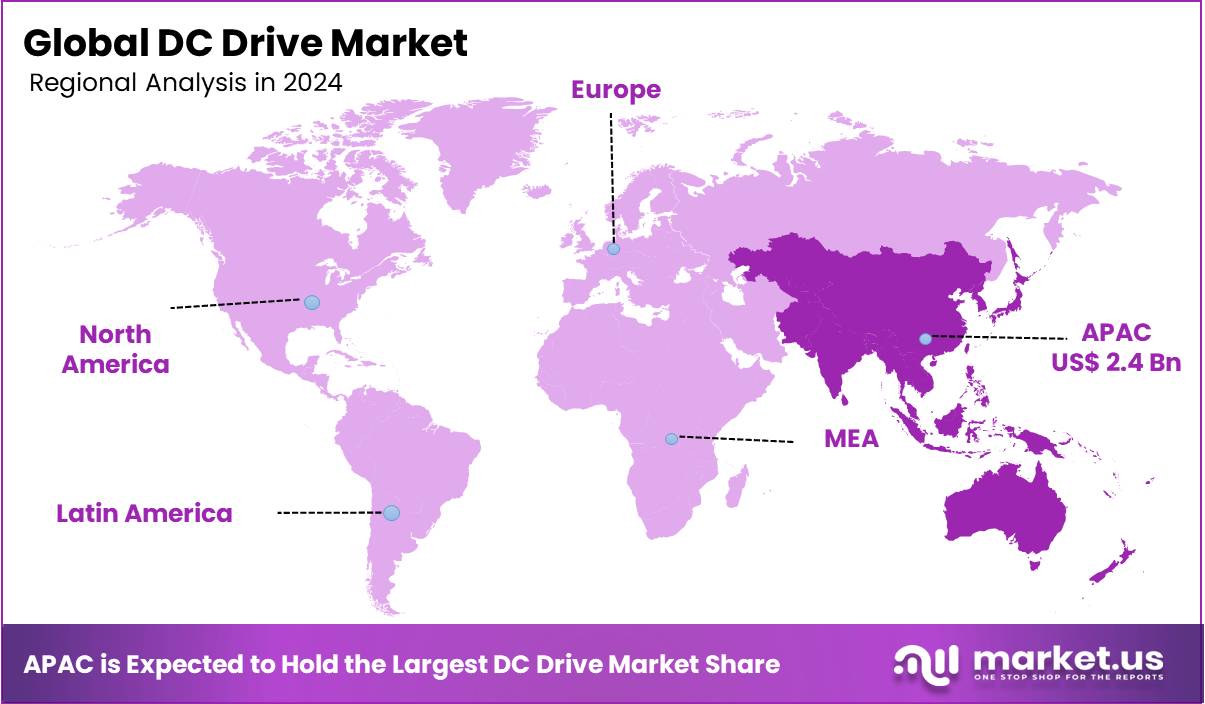

- Asia Pacific is estimated as the largest market for DC drive with a share of 5% of the market share.

Voltage Rating Analysis

The 240-600 V Dominates the Voltage Rating Segments in 2024 Due to Versatility in Industrial Applications.

The DC drive market is segmented based on voltage rating into Up to 240 V, 240-600 V, and 600 V & Above. In 2024, the 240-600 V segment held a significant revenue share of 45.3%. Due to its broad applicability in medium-power industrial sectors such as manufacturing, HVAC, material handling, and pumps, offering a balance of performance, energy efficiency, and cost-effectiveness.

Advancements in semiconductor technology and increasing energy efficiency regulations further drive demand, with these drives being versatile and scalable for both small and large systems. Their easy integration with existing infrastructure and compliance with global energy standards contribute to their continued market dominance.

Power Rating Analysis

The Up to 250 kW Dominates the Market in 2024 Due to Widespread Use in Medium-Sized Equipment.

Based on power rating, the market is further divided into Up to 250 kW,251-500 kW, and 500 kW & above. The predominance of the Up to 250 kW, commanding a substantial 47.6% market share in 2024. Due to its widespread use in small to medium-sized equipment like conveyors, fans, pumps, and compressors in industries such as manufacturing, HVAC, and water treatment.

These drives offer reliable performance, energy efficiency, and lower operational costs, making them ideal for both retrofits and new installations. Their scalability, affordability, and compatibility with various motors and automation systems make them an attractive solution for businesses seeking to optimize operations and reduce energy consumption.

End-User Analysis

Oil & Gas Dominate the DC Drive Market in 2024 Due to the High Demand for Energy Solutions

Based on end-user, the market is further divided into oil & gas, power generation, food & beverage, chemicals & petrochemicals, metal & mining, water & wastewater, building automation, and others. The predominance of the oil & gas, commanding a substantial 28.5% market share in 2024. Due to their precise control and energy-efficient operations in pumps, motors, and compressors.

These applications require high reliability, especially in remote or offshore areas where maintenance and energy savings are critical. As the industry focuses on reducing energy consumption and improving efficiency to meet environmental and cost goals, DC drives offer precise speed control and energy savings that optimize processes like drilling, refining, and transportation. Consequently, the oil and gas sector remains a major end-user, driving a significant share of the DC drive market.

Key Market Segments

By Voltage Rating

- Up to 240 V

- 240-600 V

- 600 V & Above

By Power Rating

- Up to 250 kW

- 251-500 kW

- 500 kW & Above

By End User

- Oil & Gas

- Power Generation

- Food & Beverage

- Chemicals & Petrochemicals

- Metal & Mining

- Water & Wastewater

- Building Automation

- Others

Drivers

Growth of Industrial Automation

The growth of industrial automation across key industries is a major driver for the global DC drive market. DC drives are essential in sectors like Oil & Gas, Power Generation, Food & Beverage, and Metal & Mining, providing precise control over motors in processes such as pumps, compressors, conveyors, and mixers.

These drives optimize efficiency, reduce energy consumption, and ensure reliable, smooth operations in automation systems. Their applications extend to building automation, water treatment, robotics, and more, enhancing productivity and energy savings globally. As industries increasingly adopt automation in their manufacturing and processes, there is a rising demand for more efficient and reliable systems. DC drives have emerged as a critical component in meeting these demands.

- The latest International Federation of Robotics reports report shows a 10% increase in industrial robots, with over 4.28 million units globally. Asia leads with 70% of new deployments. This growth drives the rising demand for DC drives, essential for efficient and precise robot automation.

- In 2022, North America’s automotive robotics installations surpassed 4,000 units, with electrical/electronic up 28%, metal and machinery down 9%, and plastics and chemicals down 4%, each holding a 9% market share. These developments in industrial automation highlight the growing need for efficient energy management, driving the demand for DC drives.

Moreover, another important factor driving growth is their superior control capabilities, further fueling the expansion of the global DC drive market. The increasing demand for energy efficiency, particularly through regenerative DC drives that recover energy during reduced speed, helps reduce operational costs and enhance sustainability. Their versatility, simplicity, and cost-effectiveness are driving adoption across sectors like heavy machinery, elevators, and electric vehicles, as industries increasingly embrace automation and energy-efficient solutions.

Additionally, automation becoming an important factor in reshaping industries, and the global DC drive market is poised for continued expansion. Governments worldwide are actively supporting this growth by implementing policies, offering incentives, and developing infrastructure to attract investment and foster the development of industrial automation manufacturing. This government support, combined with technological advancements and increasing demand for energy-efficient solutions, will further boost the adoption of DC drives across industries.

- The U.S. Department of Energy’s $33 million funding opportunity supports the development of smart manufacturing technologies, which directly benefits the growth of DC drives by fostering innovations in energy-efficient automation. This investment promotes the adoption of advanced technologies, including regenerative DC drives, which play a crucial role in the clean energy transition.

Restraints

Competition from AC Drives

The global DC drive market is facing considerable challenges due to the widespread adoption of AC drives, which offer several key advantages. AC drives are more cost-effective in terms of both installation and maintenance, making them a preferred choice in industries such as HVAC, water treatment, and manufacturing, where cost-efficiency, scalability, and ease of integration with standard AC motors are essential.

In contrast, DC drives require more complex installation, higher initial investments, and ongoing maintenance, making them less attractive to industries seeking simpler, scalable solutions. As AC drives dominate the market with lower operational costs and greater versatility across various applications, the growth potential of the DC drive market remains constrained.

Opportunity

Rising adoption of electric vehicles.

The rapid adoption of electric vehicles (EVs) is a key factor driving growth in the global DC drive market. DC motor controllers are critical for managing the performance and reliability of electric motors, playing a pivotal role in the automotive sector’s transition toward sustainability and reduced carbon emissions.

Governments worldwide are enacting policies and providing incentives, such as tax credits charging infrastructure incentives and rebates, to increase EV adoption. These initiatives, along with the growing shift toward electric mobility across cars, buses, railways, and two-wheelers, are significantly accelerating the demand for DC motor controllers, further fueling market expansion in the DC drive sector.

- The U.S. has 3,299,502 registered EVs, with states like California, Washington, and Oregon leading adoption through policies, and incentives for installing home charging stations. These initiatives boost the demand for DC motor drives as EV adoption and the need for supporting infrastructure continues to grow.

- Under the Bipartisan Infrastructure Law, the U.S. Department of Transportation allocated $635 million to expand electric vehicle (EV) charging infrastructure, adding over 11,500 charging ports across 27 states. This initiative boosts the demand for reliable DC motor controllers, further driving growth in the global DC drive market, in rural and complex areas.

Additionally, the growing demand for electric vehicles (EVs) can increase the need for effective voltage regulation, making DC motor drives essential for EV propulsion. With their simple speed control, optimal torque-speed characteristics, and technological maturity, DC drives are the preferred choice for EVs. Government initiatives also supporting charging infrastructure and EV adoption further boost the demand for DC motor controllers. These drives play a key role in efficient charging management by providing a steady, reliable supply for fast charging, making them a crucial element in the electric motor controller system.

Trends

Hybrid AC Drive and DC Drive System

The integration of hybrid AC/DC motor assemblies is a growing trend in the global DC drive market, driven by the need to combine the high power of DC motors with the efficiency of AC motors. These hybrid systems, commonly used in applications such as electric vehicles (EVs) and industrial machinery, offer enhanced performance and energy efficiency by using a microprocessor-based control system to ensure optimal energy delivery to both motors.

Additionally, in the energy sector, the adoption of hybrid AC/DC overhead lines (OHL) is gaining traction as a solution to increase transmission capacity without requiring new infrastructure. This approach allows utilities to convert existing HVAC lines to HVDC, improving long-distance power transmission while minimizing the need for new construction. As both the automotive and energy sectors embrace hybrid technologies, the global DC drive market is poised for growth, fueled by advancements in efficiency, sustainability, and performance.

Geopolitical Impact Analysis

Geopolitical Tensions And Trade Protectionism Increase Costs And Disrupt Supply Chains, Slowing Global DC Drive Market Growth.

The geopolitical landscape, including the uncertainties surrounding the Inflation Reduction Act (IRA) in the US and evolving trade protectionism, presents significant risks for industries reliant on the supply of raw materials, including those within the global DC drive market. As the US focuses on protectionist policies, such as tariffs on foreign steel and minerals, battery metals producers and companies involved in the production of DC drives may face higher input costs, supply chain disruptions, and limited access to critical materials. These shifts, especially in light of the US’s political volatility and the growing emphasis on green steel and carbon border adjustments, can result in increased manufacturing costs for DC drive producers, affecting market growth, particularly in regions dependent on raw materials from countries like Brazil, Russia, and Australia.

Regional Analysis

Industrial Automation And Energy Efficiency Drive Asia Pacific’s dominance in the DC Drive market.

In 2024, Asia Pacific dominated the global DC Drive market, accounting for 38.5% of the total market share, driven by the region’s rapid industrialization and expanding manufacturing sector. Industries such as automotive, HVAC, water treatment, and manufacturing are increasingly adopting DC drives for their precise control, energy efficiency, and reliability. In addition, the growing demand for energy-efficient solutions and automation in various sectors is further accelerating the market expansion.

Countries like China, Japan, and India are leading the adoption, with increasing investments in infrastructure and technology. Government initiatives aimed at reducing carbon footprints and promoting sustainable energy practices also contribute to the rising demand for DC drives. This combination of industrial growth, regulatory support, and technological advancements is shaping the future of the DC drive market in the Asia Pacific region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Key Players in the DC Drive Market Focus On Offering Premium, Sustainable Products To Cater To High-End Consumers.

Key players in DC drive development, including ABB, Rockwell Automation, Siemens, and Schneider Electric, focus on Integrating advanced features, enhancing energy efficiency, and expanding their global presence through strategic partnerships and acquisitions. Emerson Electric offers DC drive solutions that are known for their reliability and durability, often used in harsh industrial environments.

Parker Hannifin focuses on providing DC drive solutions for a wide range of applications, including industrial automation, material handling, and more. Known for its DCS550 DC drive model, ABB integrates advanced features like programmability, built-in control programs, communication, and I/O options to meet diverse application needs, emphasizing efficiency and reliability.

Major Players in the Industry

- ABB Ltd.

- American Electric Technologies Inc.

- Crompton Greaves Limited

- Danfoss Group

- Emerson Electric Co.

- GE Power Conversion

- Mitsubishi Electric Corporation

- Nidec Motor Corporation

- Parker Hannifin Co.

- Renown Electric Motors

- Rockwell Automation

- Schneider Electric Se

- Sprint Electric Limited

- Toshiba International Corporation Ltd.

- Others

Recent Development

- In December 2024 – ePropulsion expanded its electric motors and systems offerings for the OEM boatbuilding market for small electric and hybrid vessels with the launch of three new products at the METSTRADE trade show in Amsterdam. The modular design means the system can be configured to offer different functions including automatic power management, hybrid control, and supplying the vessel with different AC or DC power needs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 5.3 Bn |

| Forecast Revenue (2034) | USD 10.1 Bn |

| CAGR (2025-2034) | 6.70 % |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Voltage Rating (Up to 240 V, 240-600 V, 600 V & Above), By Power Rating (Up to 250 kW, 251-500 kW, 500 kW & Above), By End User(Oil & Gas, Power Generation, Food & Beverage, Chemicals & Petrochemicals, Metal & Mining, Water & Wastewater, Building Automation, Others), |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ABB Ltd., American Electric Technologies Inc., Crompton Greaves Limited, Danfoss Group, Emerson Electric Co., GE Power Conversion, Mitsubishi Electric Corporation, Nidec Motor Corporation, Parker Hannifin Co., Renown Electric Motors, Rockwell Automation, Schneider Electric Se, Sprint Electric Limited, Toshiba International Corporation Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |