Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of the Coal Power Generation Market

- By Fuel Type Analysis

- By Capacity Analysis

- By Technology Analysis

- By End User Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

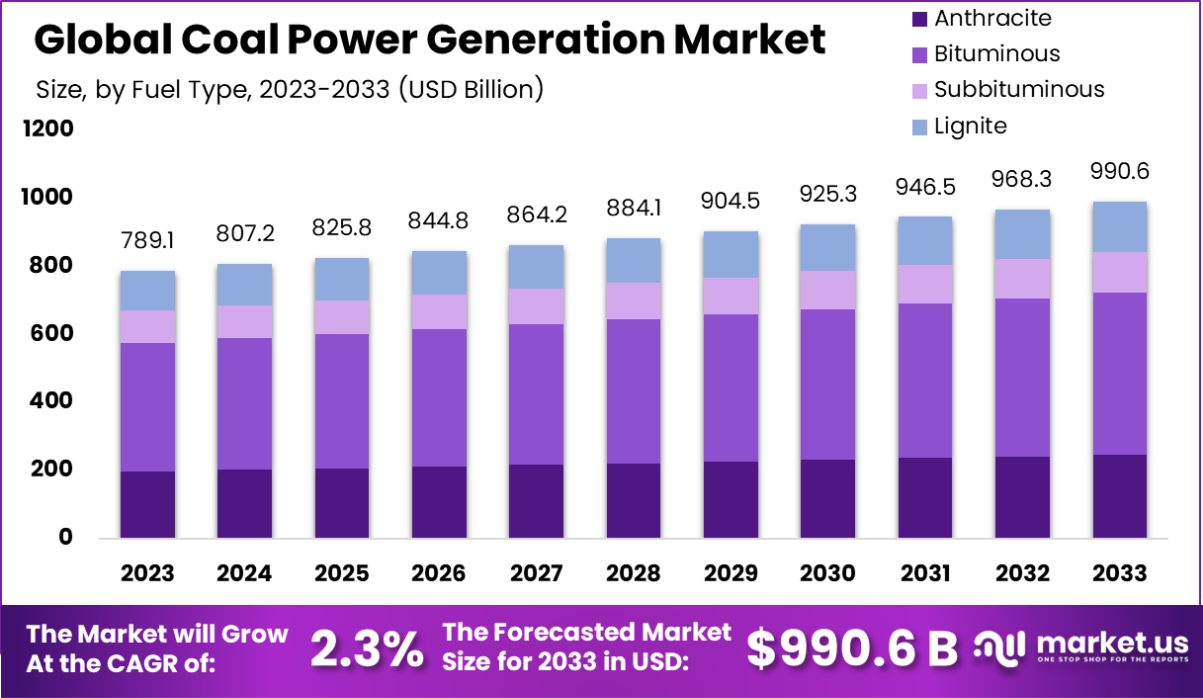

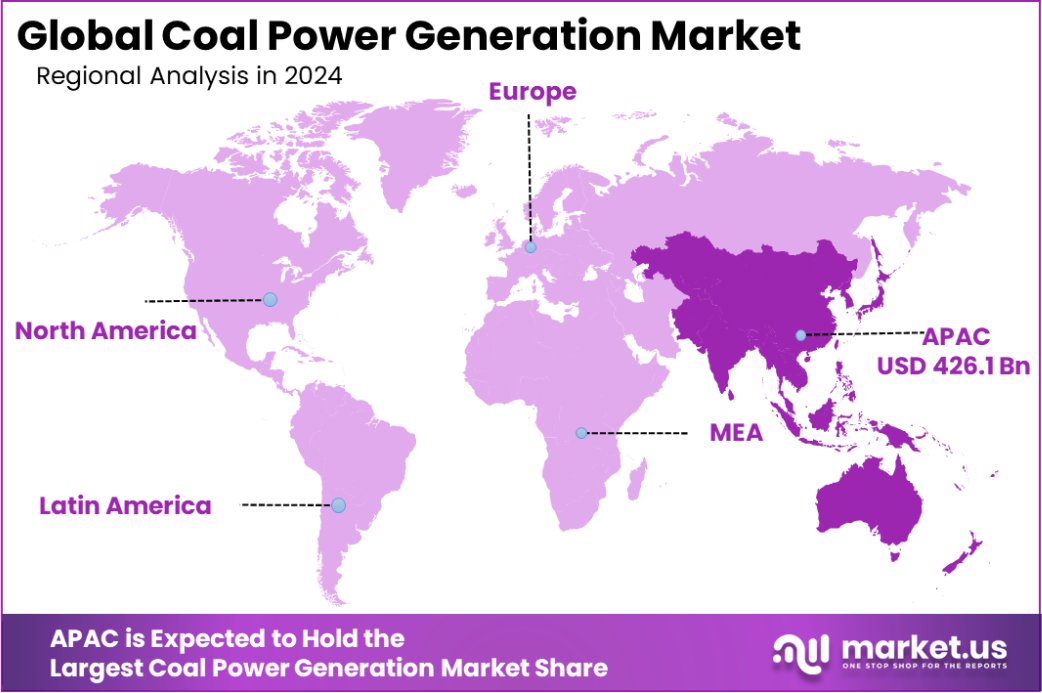

The Global Coal Power Generation Market is expected to be worth around USD 990.6 Billion by 2033, up from USD 789.1 Billion in 2023, and grow at a CAGR of 2.3% from 2024 to 2033. In Asia-Pacific, the coal power generation market holds 53.6%, valued at USD 426.1 billion.

Coal power generation involves the burning of coal to produce electricity. The process includes pulverizing coal, burning it in a furnace, and using the heat to produce steam that drives a turbine connected to an electricity generator. It is one of the oldest and most widely used energy sources globally.

The coal power generation market refers to the industry encompassing the production and distribution of electricity using coal as a primary energy source. This market is influenced by factors like energy demand, industrialization, and regulatory policies around emissions. Technological advancements and cleaner coal technologies are shaping its growth dynamics.

The coal power generation market remains a pivotal component of India’s energy infrastructure, supplying over 70% of the nation’s electricity needs. In the fiscal year 2023-24, India achieved a record coal production of 997.25 million tonnes (MT), marking an 11.65% increase from the previous year. This surge underscores the sector’s critical role in meeting the country’s escalating energy demands.

Several factors are propelling the expansion of coal-based power generation. Rapid industrialization and urbanization have led to a consistent rise in electricity consumption, necessitating a dependable and cost-effective energy source. Coal’s abundance and established supply chains render it a practical solution to fulfill this demand.

Additionally, the government’s commitment to energy security has resulted in policies to enhance domestic coal production and reduce reliance on imports. Notably, from April to September 2024, coal imports for blending purposes declined by 8.5% to 9.79 MT, reflecting efforts toward self-sufficiency.

Current trends indicate a nuanced trajectory for the coal power sector. While there is a global shift toward renewable energy sources, India’s energy strategy continues incorporating coal to ensure grid stability and support economic growth.

The Ministry of Coal has outlined plans to increase production to 1,404 MT by 2027, with a significant portion allocated to domestic coal-based power plants. Concurrently, there is an emphasis on adopting cleaner coal technologies and improving plant efficiencies to mitigate environmental impacts.

Looking ahead, India’s coal power generation market presents challenges and opportunities. The anticipated peak in coal demand between 2030 and 2035 suggests a window for strategic investments in technology upgrades and emissions control measures.

Furthermore, the integration of renewable energy sources alongside coal-fired plants offers prospects for a diversified and resilient energy mix. The government’s initiatives to bolster domestic production, coupled with a cautious approach to environmental sustainability, are poised to shape the future landscape of coal power generation in the country.

Key Takeaways

- The Global Coal Power Generation Market is expected to be worth around USD 990.6 Billion by 2033, up from USD 789.1 Billion in 2023, and grow at a CAGR of 2.3% from 2024 to 2033.

- The Coal Power Generation Market reveals bituminous fuel type holds a share of 48.1%.

- Capacity analysis shows that the 500-1000 MW segment commands a 39.1% share in the market.

- Pulverized Coal (P.C.) technology dominates the market, accounting for 53.2% of the technology segment.

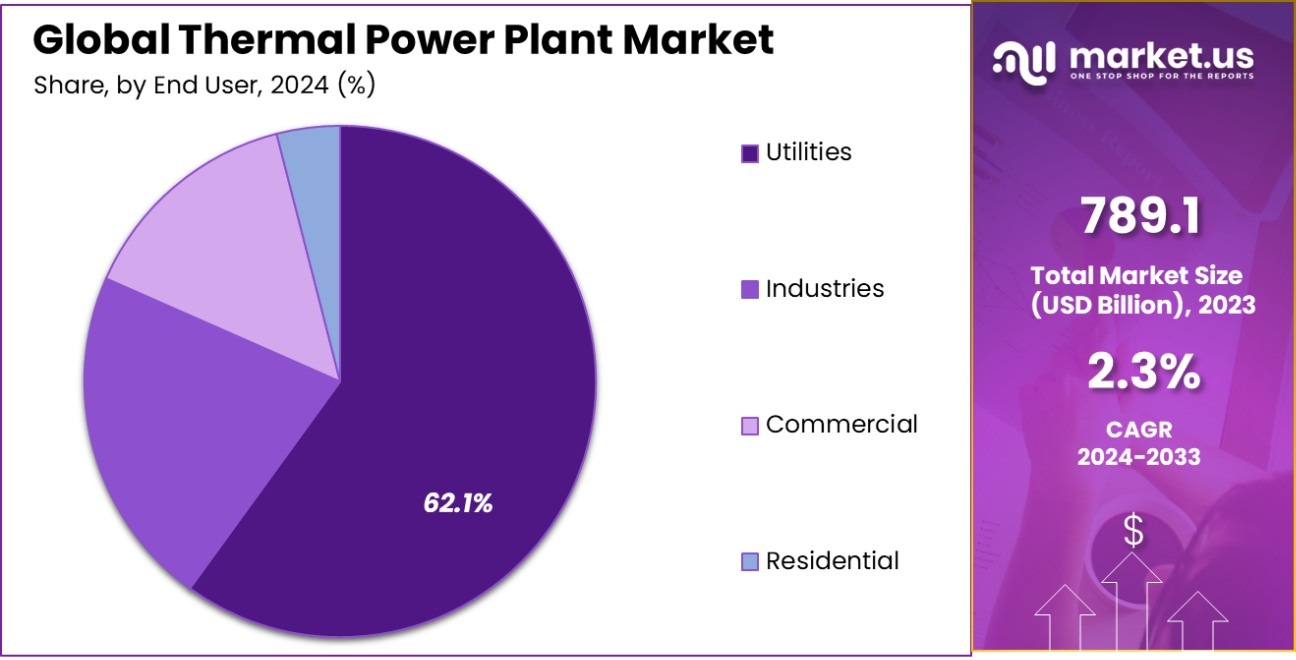

- Utilities emerge as the primary end users in the Coal Power Generation Market with 62.1%.

- The Asia-Pacific coal power generation market holds 53.6%, valued at USD 426.1 billion.

Business Benefits of the Coal Power Generation Market

Coal power generation continues to be a pivotal part of the U.S. energy mix, contributing 16.2% of the nation’s utility-scale electricity in 2023. This represents a slight decrease from 19.5% in 2022, reflecting a broader trend of decline in coal dependency.

Despite a 12% reduction in coal production from 578 million short tons in 2023 to an estimated 512 million in 2024, coal remains a critical source of electricity, especially during peak demand periods or grid instability.

In 2022, the U.S. electric power sector consumed 469.9 million short tons of coal, which constituted 91.7% of the total U.S. coal consumption. This high percentage underscores coal’s role in ensuring energy security and providing a reliable power supply.

Coal-fired power plants, while decreasing by about 23% in their electricity generation capacity between 2021 and 2023 in the Lower 48 states, still support base load generation. They offer a stable energy output that can balance intermittent sources like wind and smart solar.

The business benefits of coal power include its ability to support a diversified energy strategy and its cost-effectiveness in regions with abundant coal reserves. Additionally, coal power plants are capable of scaling production up or down to meet fluctuating demands, a critical factor in maintaining grid stability and managing energy prices.

By Fuel Type Analysis

Bituminous fuel dominates the Coal Power Generation Market with a 48.1% market share.

In 2023, Anthracite contributed 22.3% to the Coal Power Generation Market. Its superior carbon content and cleaner burning properties make it a preferred option in industries requiring efficient energy output, such as metallurgy and chemical processing.

Bituminous held a dominant market position in the By Fuel Type segment of the Coal Power Generation Market, with a 48.1% share. Its high availability and energy efficiency make it a primary choice for electricity generation across industrialized regions.

Subbituminous accounted for 18.5% of the Coal Power Generation Market. Its lower sulfur emissions compared to other types have made it a favorable alternative for countries emphasizing cleaner coal energy solutions.

Lignite contributed 11.1% to the Coal Power Generation Market. Its abundant reserves and affordability have positioned it as a viable option for cost-effective energy production in developing economies.

By Capacity Analysis

Medium capacity, 500-1000 MW, holds 39.1% of the Coal Power Generation Market.

In 2023, Less than 300 MW contributed 15.7% to the Coal Power Generation Market. This segment is driven by its suitability for small-scale energy needs and decentralized power generation in remote and rural regions.

300-500 MW accounted for 28.4% of the Coal Power Generation Market. Its balanced efficiency and ability to support medium-scale industrial and residential energy requirements have made it a prominent choice globally.

500-1000 MW held a dominant market position in the By Capacity segment of the Coal Power Generation Market, with a 39.1% share. Its scalability and efficiency in large-scale power plants cater to regions with high energy demands.

Over 1000 MW contributed 16.8% to the Coal Power Generation Market. This segment’s capability to generate substantial energy output makes it ideal for meeting the requirements of densely populated and industrialized areas.

By Technology Analysis

Pulverized Coal (P.C.) technology leads with 53.2% in the market.

In 2023, Bubbling Fluidized Bed (B.F.B.) accounted for 10.8% of the Coal Power Generation Market. Its ability to handle varied fuel types and reduce emissions has contributed to its adoption in smaller-scale power plants.

Circulating Fluidized Bed (C.F.B.) represented 14.7% of the Coal Power Generation Market. This technology is preferred for its flexibility in burning low-quality coals and its efficient emission control capabilities.

Pulverized Coal (P.C.) held a dominant market position in the By Technology segment of the Coal Power Generation Market, with a 53.2% share. Its high efficiency and widespread availability have established it as a leading technology for large-scale power generation.

Integrated Gasification Combined Cycle (IGCC) contributed 12.3% to the Coal Power Generation Market. Its advanced design enables better fuel efficiency and reduced environmental impact, making it attractive for cleaner energy initiatives.

Ultra-supercritical (U.S.C.) technology accounted for 9.0% of the Coal Power Generation Market. Its ability to operate at higher temperatures and pressures supports greater efficiency and lower emissions in modern power plants.

By End User Analysis

Utilities are the largest end users, comprising 62.1% of the market.

In 2023, Utilities held a dominant market position in the By End User segment of the Coal Power Generation Market, with a 62.1% share. Large-scale power generation and grid distribution requirements drive this segment’s growth across various regions.

Industries accounted for 21.4% of the Coal Power Generation Market. The segment’s growth stems from heavy manufacturing and processing sectors requiring stable and cost-effective energy sources.

Commercial end-users represented 10.3% of the Coal Power Generation Market. The segment benefits from consistent demand in retail complexes, business parks, and service sectors needing uninterrupted electricity supply.

Residential end users contributed 6.2% to the Coal Power Generation Market. The segment is supported by growing electricity access in developing economies and the affordability of coal-based energy solutions for households.

Key Market Segments

By Fuel Type

- Anthracite

- Bituminous

- Subbituminous

- Lignite

By Capacity

- Less than 300 MW

- 300-500 MW

- 500-1000 MW

- Over 1000 MW

By Technology

- Bubbling Fluidized Bed (B.F.B.)

- Circulating Fluidized Bed (C.F.B.)

- Pulverized Coal (P.C.)

- Integrated Gasification Combined Cycle (IGCC)

- Ultra-Supercritical (U.S.C.)

By End User

- Utilities

- Industries

- Commercial

- Residential

Driving Factors

Abundant Coal Reserves Lower Energy Production Costs

Coal remains one of the most abundant energy resources globally, particularly in the United States. This abundance directly translates to reduced costs for energy production when using coal. Coal’s extensive availability ensures that power plants can operate at higher capacities without the risk of depleting resources, making coal a cost-effective choice for energy generation.

This economic advantage positions coal as a viable option for energy producers looking to maintain affordable electricity rates amidst fluctuating fuel markets.

Coal Plants Provide Reliable Base Load Electricity

Coal power stations are capable of continuous operation, providing a stable, reliable base load supply of electricity. This reliability is crucial for balancing power grids, especially as renewable energy sources like wind and solar, which are variable by nature, become more prevalent.

The ability to produce a consistent energy output means that coal-fired plants are often pivotal in supporting grid stability, which is essential for both residential and industrial energy consumers.

Flexibility in Meeting Peak Electricity Demands

Coal-fired power plants offer exceptional flexibility in scaling their output to meet peak electricity demands, a critical feature during extreme weather conditions or other high-demand scenarios. This flexibility helps in managing grid stability and prevents potential blackouts.

By adjusting output quickly, coal plants play a vital role in ensuring that the energy supply meets the demand efficiently, thus safeguarding continuous and reliable power supply during critical times.

Restraining Factors

Environmental Regulations Tighten on Coal Emissions

Environmental concerns about air quality and climate change have led to stringent regulations on emissions from coal-fired power plants. These regulations require significant investment in technology to reduce pollutants, which can elevate operational costs and challenge profitability.

As governments globally aim to reduce carbon footprints, coal plants face increasing pressure to adhere to these environmental standards, impacting their long-term viability and prompting a shift towards cleaner energy alternatives.

Competitive Renewable Energy Technologies Gain Ground

The rapid advancement and decreasing costs of renewable energy technologies, such as solar and wind, are making these alternatives more competitive against traditional coal power. As renewables become more economically viable, the shift away from coal accelerates, driven by both policy support and consumer preference for cleaner energy sources.

This shift is reshaping the energy market, pushing coal further to the sidelines as utilities and investors prioritize green, sustainable energy options.

Public and Political Pressure for Cleaner Energy

There is a growing public and political advocacy for cleaner energy sources, which influences both market dynamics and regulatory frameworks. This pressure is partly due to increased awareness of the environmental and health impacts of coal power, such as air pollution and smart greenhouse gas emissions.

As the community’s push for sustainable and environmentally friendly energy solutions strengthens, coal’s role in the energy mix diminishes, leading to a decline in new coal power investments and a focus on phasing out existing coal-fired facilities.

Growth Opportunity

Expansion into Emerging Markets with High Energy Demands

Emerging economies with rapidly growing energy needs present significant opportunities for coal power generation. These regions often face energy deficits and may lack the infrastructure for large-scale renewable energy projects.

Coal, with its robust supply chain and established technology, can provide a quick and economical solution to meet these increasing energy demands. As these markets develop, coal power can play a transitional role, offering reliable electricity to support economic growth and societal advancement.

Technological Innovations in Emission Control

Advancements in emission control technologies offer coal power plants the opportunity to reduce environmental impact while maintaining their operational feasibility. Technologies such as carbon capture and storage (CCS) and scrubbers that reduce sulfur dioxide and particulate emissions can help coal plants meet stringent environmental regulations.

By investing in these technologies, coal power generation can sustain its market position and continue to operate under new environmental standards, thereby extending the life of existing facilities and maintaining energy security.

Hybrid Energy Systems Integration

The integration of coal-fired power with renewable energy sources offers a growth pathway by creating hybrid energy systems. These systems can leverage the reliability of coal power to stabilize the grid while incorporating intermittent renewable energies like wind and solar.

This approach allows for a smoother transition to a low-carbon future by optimizing the mix of energy sources, enhancing grid stability, and reducing overall emissions. The potential for hybrid systems is increasingly recognized as a practical solution to balance energy sustainability with reliability.

Latest Trends

Increased Investment in High-Efficiency Coal Technologies

There is a growing trend towards investing in high-efficiency, low-emission (HELE) coal technologies. These technologies significantly enhance the efficiency of coal power plants while minimizing their environmental footprint by reducing emissions per unit of power generated.

As countries balance energy needs with environmental impacts, HELE technologies are becoming increasingly popular, offering a way to keep coal as a part of the energy mix while addressing climate change concerns.

Co-Firing with Biomass to Reduce Emissions

Co-firing coal with biomass is an emerging trend in the coal power generation sector. This process involves burning a mix of coal and biomass (such as wood chips or agricultural waste) to generate electricity.

Co-firing can significantly reduce greenhouse gas emissions from coal-fired power plants and is becoming a compelling option for power producers looking to meet stricter emission regulations without completely overhauling existing infrastructure.

Development of Carbon Capture and Storage Projects

The development and implementation of carbon capture and storage (CCS) projects represent a key trend in the coal power sector. This technology captures carbon dioxide emissions from power plants and stores them underground to prevent them from entering the atmosphere.

With an increasing global focus on reducing carbon footprints, CCS projects are gaining traction as a critical component in the strategy to lower emissions from existing coal power plants, thereby extending their viability in a carbon-constrained world.

Regional Analysis

The Asia-Pacific coal power generation market commands a 53.6% share, valued at USD 426.1 billion.

The coal power generation market varies significantly across regions, reflecting diverse energy policies and economic conditions. Asia-Pacific is the dominant region, accounting for 53.6% of the market, and valued at USD 426.1 billion.

This region’s substantial share is driven by high energy demands from rapidly industrializing economies and significant investments in coal power to ensure energy security and support economic development.

In North America, the market is experiencing a shift as investments in cleaner energy sources grow, though coal remains integral in ensuring grid stability and meeting peak demands. Europe is similarly transitioning, with a strong focus on reducing emissions through advancements in technology and increased regulatory pressures, which influence a gradual move away from coal power.

The Middle East & Africa, with abundant fossil fuel reserves, continue to rely on coal power for energy security and to support its industrial sectors, despite global trends. Latin America shows a mixed pattern, with some countries exploring coal as a stopgap solution to energy shortages, while others invest in renewable energies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global coal power generation market will be shaped by the strategic maneuvers of key players, each adapting uniquely to market demands and regulatory environments. Companies like Alstom and General Electric are at the forefront, focusing on technological innovations to enhance the efficiency and environmental compliance of coal-fired plants. These improvements are critical as industries and governments seek to balance energy security with environmental sustainability.

American Electric Power Company, Inc., Duke Energy Corporation, and Dominion Energy Solutions are pivotal in the North American market. They leverage their extensive infrastructure to ensure a reliable energy supply while progressively integrating cleaner technology and carbon capture solutions to align with stricter emissions standards. Their efforts are crucial in maintaining coal’s role in a diversified energy strategy.

In Asia, firms like China Huadian Corporation Ltd., Bharat Heavy Electricals, and National Thermal Power Corporation Limited are key drivers. These companies capitalize on regional growth in energy demand by expanding coal power capacities, yet they also invest in high-efficiency technologies to reduce the environmental impact. Mitsubishi Heavy Industries and Doosan Heavy Industries Construction continue to innovate in coal technology, often exporting their advanced systems globally.

European players such as RWE and Uniper SE focus on transitioning their portfolios towards more sustainable practices, incorporating renewable energies while maintaining coal power for grid stability. Their strategies include modernizing older plants and exploring co-firing techniques, which blend coal with biomass or other renewables.

Top Key Players in the Market

- Alstom

- American Electric Power Company, Inc.

- Bharat Heavy Electricals.

- China Huadian Corporation Ltd. (CHD)

- Dominion Energy Solutions

- Doosan Heavy Industries Construction.

- Duke Energy Corporation

- E.S. Corporation

- Eskom Holdings SOC Ltd.

- General Electric.

- Harbin Electric Corporation.

- Jindal India Thermal Power Ltd.

- KEPCO Engineering & Construction Company, Inc.

- Mitsubishi Heavy Industries.

- National Thermal Power Corporation Limited (NTPC)

- RWE

- Shanghai Electric Group.

- STEAG GMBH

- Sumitomo Corporation.

- Uniper SE

Recent Developments

- In 2023, Alstom expanded its involvement in the coal power generation sector by delivering Block 9 of the Grosskraftwerk Mannheim (GKM) coal-fired power plant in Germany. This project underscored Alstom’s capabilities in managing complex infrastructure projects, particularly in the conventional power generation field.

- In 2023, American Electric Power (AEP) progressed in transitioning from coal by planning to retire the 580 MW Pirkey Plant and end coal usage at the Welsh Plant by 2028, aligning with environmental standards and their sustainability goals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 789.1 Billion |

| Forecast Revenue (2033) | USD 990.6 Billion |

| CAGR (2024-2033) | 2.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fuel Type (Anthracite, Bituminous, Subbituminous, Lignite), By Capacity (Less than 300 MW, 300-500 MW, 500-1000 MW, Over 1000 MW), By Technology (Bubbling Fluidized Bed (B.F.B.), Circulating Fluidized Bed (C.F.B.), Pulverized Coal (P.C.), Integrated Gasification Combined Cycle (IGCC), Ultra-Supercritical (U.S.C.)), By End User (Utilities, Industries, Commercial, Residential) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alstom, American Electric Power Company, Inc., Bharat Heavy Electricals., China Huadian Corporation Ltd. (CHD), Dominion Energy Solutions, Doosan Heavy Industries Construction., Duke Energy Corporation, E.S. Corporation, Eskom Holdings SOC Ltd., General Electric., Harbin Electric Corporation., Jindal India Thermal Power Ltd., KEPCO Engineering & Construction Company, Inc., Mitsubishi Heavy Industries., National Thermal Power Corporation Limited (NTPC), RWE, Shanghai Electric Group., STEAG GMBH, Sumitomo Corporation., Uniper SE |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |