Quick Navigation

Report Overview

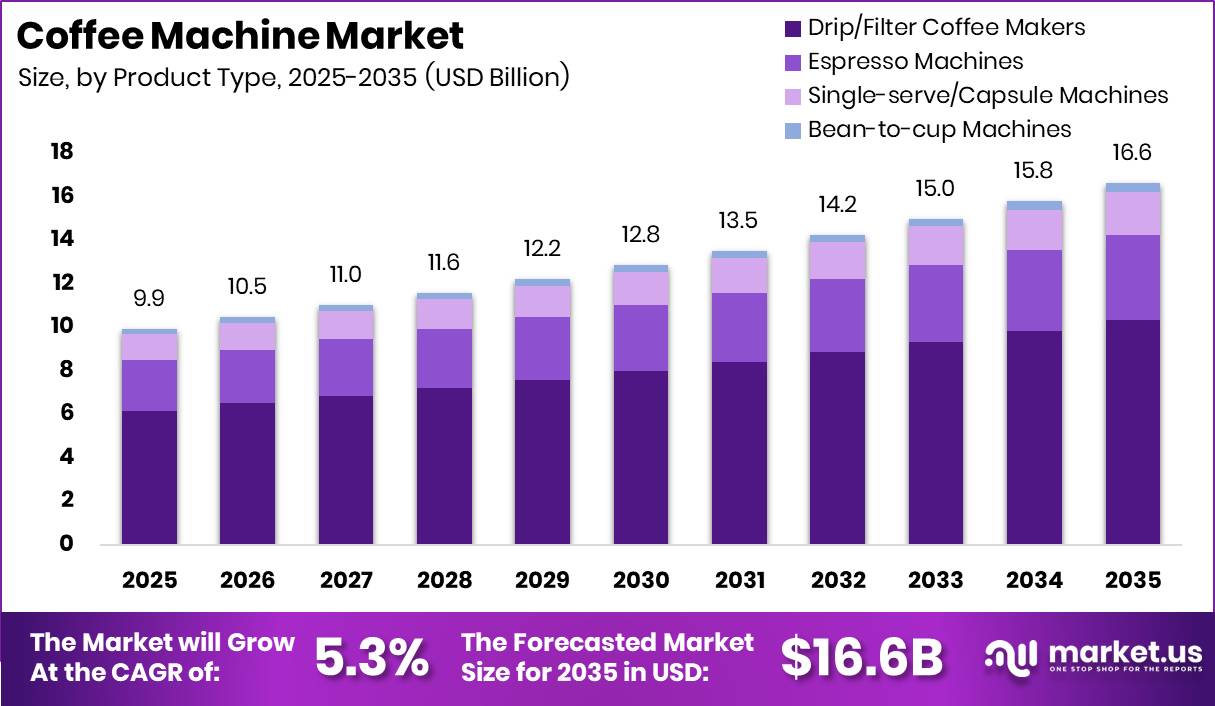

Global Coffee Machine Market size is expected to be worth around USD 16.6 Billion by 2035 from USD 9.9 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The coffee machine market encompasses a broad range of brewing equipment designed for residential and commercial use. Product categories include espresso machines, drip and filter coffee makers, single-serve capsule machines, and bean-to-cup systems. These products are sold through both offline retail channels and online platforms, serving individual consumers, foodservice operators, and workplace environments worldwide.

Key Takeaways

- Market size in 2025: USD 9.9 Billion

- Market forecast for 2035: USD 16.6 Billion

- CAGR (2026 to 2035): 5.3%

- Dominant product type: Drip/Filter Coffee Makers with 62.11% share

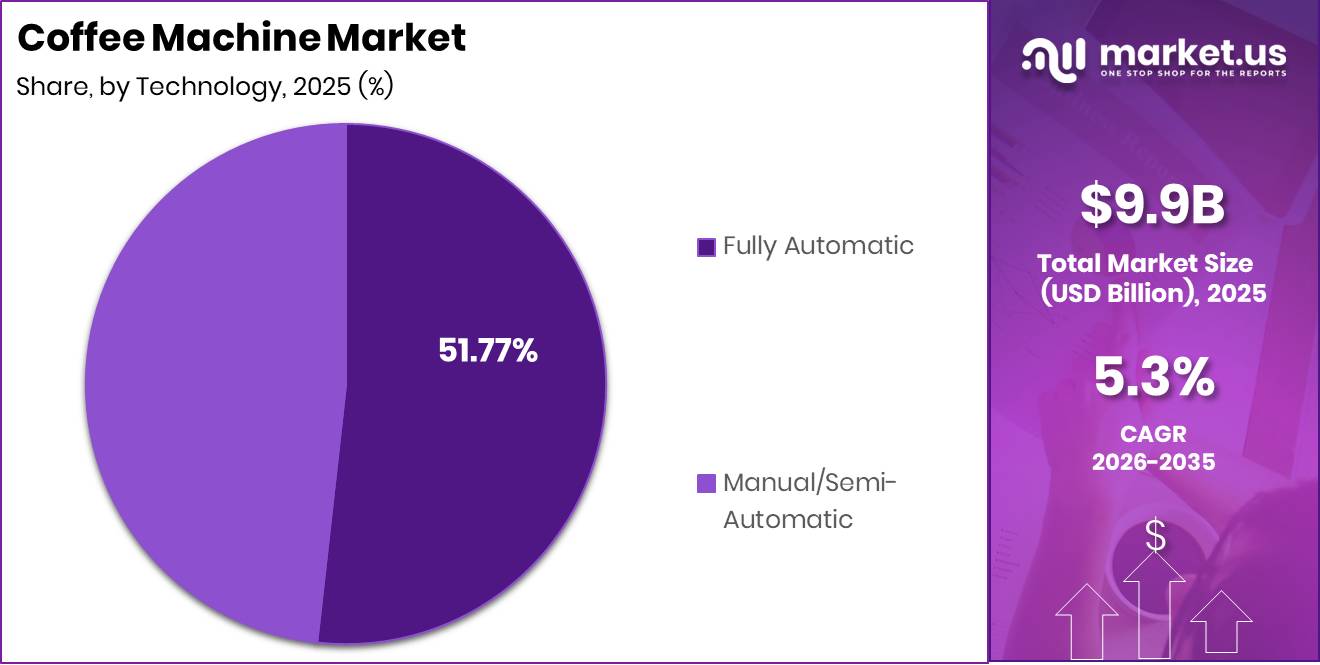

- Dominant technology: Manual/Semi-Automatic with 48.23% share

- Dominant application: Commercial with 57.66% share

- Dominant distribution channel: Offline with 64.34% share

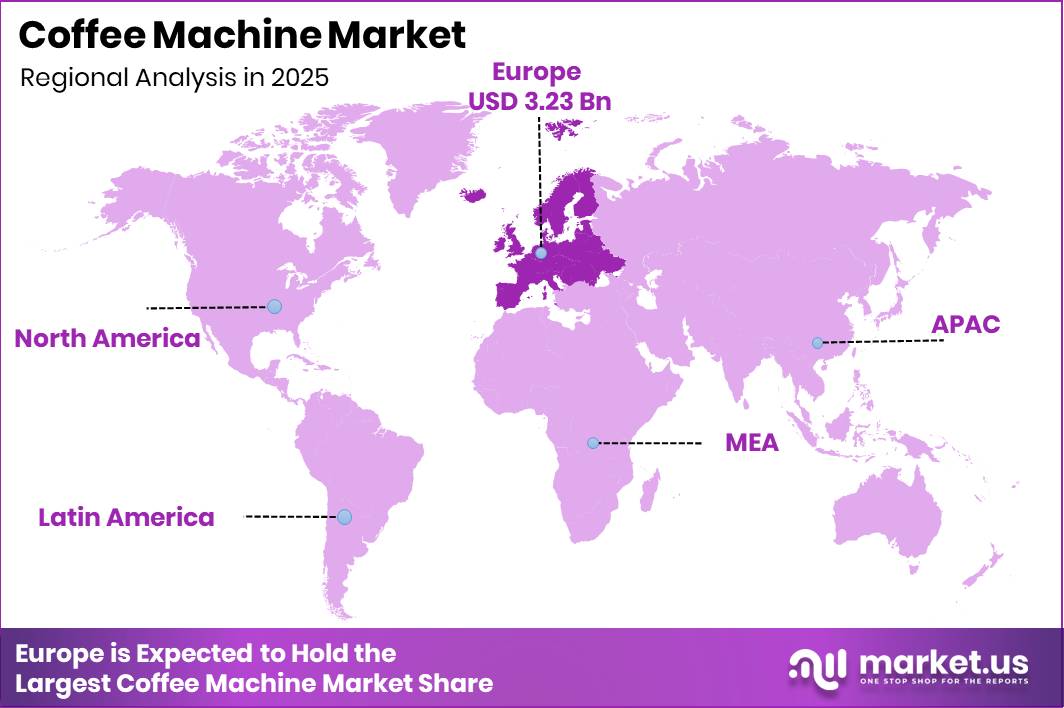

- Leading region: Europe with 32.56% share, valued at USD 3.23 Billion

According to Reuters, 85% of U.S. coffee drinkers consumed coffee at home in 2026, the highest level recorded since 2012. This behavioral shift expands the addressable market for home brewing equipment and supports sustained appliance replacement demand. Manufacturers targeting the residential segment hold a structural advantage as at-home consumption consolidates.

Reuters also found that 66% of U.S. adults reported drinking coffee in the previous day in 2026, making coffee the most-consumed beverage ahead of bottled water. As reported by Verena Street, 68% of consumers brewed coffee at home daily in 2025. This consumption frequency drives repeat machine purchases and accelerates the upgrade cycle across household income brackets.

Product Type Analysis

Drip/Filter Coffee Makers dominate with 62.11% due to broad household penetration and low entry cost.

In 2025, Drip/Filter Coffee Makers held a dominant market position in the By Product Type segment of the Coffee Machine Market, with a 62.11% share. Data from Verena Street shows 38% of consumers identified drip coffee makers as their primary home brewing equipment in 2025. Based on National Coffee Association data referenced via Reddit, 62% of U.S. consumers owned a drip coffee maker that year, confirming category saturation and steady replacement demand.

Espresso Machines occupy a premium tier within the product type segment. In June 2026, Philips unveiled the Baristina Latte, featuring an integrated Smart Wand steam system for automated milk frothing. This launch signals intensifying competition in the premium espresso segment as manufacturers embed automation features to justify higher price points and attract consumers upgrading from entry-level equipment.

Single-serve/Capsule Machines address demand for speed and portion control in both home and small-office environments. National Coffee Association figures referenced via Reddit show 42% of U.S. consumers owned a single-cup coffee machine in 2025. This ownership rate confirms that capsule systems hold a structurally significant share of the installed base alongside drip machines.

Bean-to-cup Machines represent a smaller but expanding sub-segment within the product type category. Reddit-sourced National Coffee Association data indicates 15% of consumers owned bean-to-cup machines in 2025, with ownership up 15% versus 2020 levels. This trajectory indicates a consumer shift toward fresh-grind quality at home, creating upgrade revenue for manufacturers in the premium appliance tier.

Technology Analysis

Manual/Semi-Automatic dominates with 48.23% due to barista-control preference among enthusiast buyers.

In 2025, Manual/Semi-Automatic technology held a dominant market position in the By Technology segment of the Coffee Machine Market, with a 48.23% share. This segment reflects a buyer base that prioritizes extraction control and tactile involvement over automation. The high share indicates that a significant portion of coffee machine buyers, particularly in the prosumer and specialty segments, have not yet transitioned to fully automated systems.

Fully Automatic technology is the fastest-growing sub-segment within the technology category. Consumer preference for one-touch brewing cycles drives adoption among time-constrained households and small-office users. Manufacturers offering fully automatic machines with customizable brew profiles are positioned to capture buyers moving away from manual operation as convenience becomes the primary purchase criterion.

Application Analysis

Commercial dominates with 57.66% due to high-volume daily usage across foodservice and hospitality.

In 2025, Commercial held a dominant market position in the By Application segment of the Coffee Machine Market, with a 57.66% share. Foodservice operators, hotels, and office environments require machines capable of sustained daily output at consistent quality. This operational demand sustains commercial equipment replacement cycles independent of consumer sentiment shifts.

Residential is the fastest-growing application sub-segment. According to Reuters, U.S. coffee drinkers consumed an average of 2.8 cups of coffee per day in 2026, equivalent to more than 500 million cups served daily nationwide. This consumption intensity creates recurring machine usage that accelerates wear cycles and drives replacement purchases. As per our research, at-home consumption patterns directly expand the installed base of residential coffee machines.

Distribution Channel Analysis

Offline dominates with 64.34% due to in-store trial preference for high-consideration appliances.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Coffee Machine Market, with a 64.34% share. Supermarkets, hypermarkets, and specialty stores benefit from the consumer preference to physically evaluate coffee machines before purchase. This tactile buying behavior sustains offline dominance especially in mid-price and premium product tiers.

Online is the fastest-growing distribution channel. E-commerce platforms reduce geographic barriers and allow manufacturers to reach buyers in markets with limited specialty retail infrastructure. This channel growth is most pronounced in urban markets where digital purchasing is embedded in daily consumer behavior. Brands that invest in online search presence and direct-to-consumer platforms will outpace competitors relying on traditional retail shelf space.

Key Market Segments

By Product Type

- Espresso Machines

- Drip/Filter Coffee Makers

- Single-serve/Capsule Machines

- Bean-to-cup Machines

By Technology

- Manual/Semi-Automatic

- Fully Automatic

By Application

- Residential

- Commercial

By Distribution Channel

- Online

- Offline

- Supermarkets/Hypermarkets

- Specialty Stores

Regional Analysis

Europe Dominates the Coffee Machine Market with a Market Share of 32.56%, Valued at USD 3.23 Billion

Europe leads the global coffee machine market with a 32.56% share valued at USD 3.23 Billion. Deep-rooted coffee culture across Germany, Italy, France, and the Nordic countries sustains high per-household machine ownership. In September 2025, Smeg launched the ECF03, a premium 2-in-1 espresso machine capable of producing both hot and cold-extracted espresso in approximately 2 minutes, underscoring how European manufacturers are targeting specialty demand.

North America represents a structurally strong market supported by consistently high daily coffee consumption rates. Single-serve and capsule systems maintain high household penetration, and residential demand continues to strengthen as hybrid work patterns sustain at-home brewing occasions. The region’s large mass-retail infrastructure supports both offline and online channel growth simultaneously.

Asia Pacific is an expanding market where urbanization and rising disposable incomes are broadening the buyer base for coffee appliances. Coffee consumption is shifting from a niche category to a mainstream daily habit in key markets including China, Japan, and South Korea. Manufacturers entering this region with compact premium machines are positioned to capture first-mover advantage in household penetration.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Solo households, cold-drink expansion, and office micro-kitchens offer underpenetrated entry points

The residential segment is the fastest-growing application but remains underpenetrated in Asia Pacific markets outside Japan and South Korea. Urban middle-class households in China and India are shifting toward daily at-home coffee habits without proportional machine ownership. Brands that enter these markets with affordable compact systems will capture first-mover share before premium European and North American players establish retail presence.

Solo-household compact premium systems represent an underexploited product tier in North America and Western Europe. Current product lines are designed for multi-person household output, leaving single-occupant buyers to either overpay for unnecessary capacity or accept lower-quality machines. A purpose-built compact premium segment directly addresses this mismatch and commands pricing above entry-level without requiring full super-automatic specifications.

The offline distribution channel holds a 64.34% share, yet specialty store penetration in Latin America and the Middle East and Africa remains limited. These regions hold large coffee-consuming populations but lack the retail infrastructure that drives machine conversion in Europe and North America. Manufacturers or distributors that build specialty store partnerships in these geographies will unlock machine sales in markets where café-quality expectations already exist but home equipment access does not.

Bean-to-cup machine ownership stood at 15% in 2025, up 15% versus 2020, yet the segment still trails drip and single-serve systems by a wide margin. This gap represents a conversion opportunity for manufacturers with strong grinder-quality messaging and subscription bean programs. Pairing hardware with curated bean sourcing creates a bundled value proposition that is harder for commodity competitors to replicate on price alone.

Technology and Innovation Landscape - Sustainability materials, renewable energy, and rapid-brew engineering are redefining product competitiveness

Nestlé Professional introduced self-serve coffee machine units in 2025 constructed from a material containing 70% recycled plastic waste and 30% used coffee grounds. This material innovation reduces reliance on virgin plastics while creating a product story aligned with commercial buyer sustainability procurement criteria. Manufacturers that adopt circular-material strategies in machine housings gain a compliance advantage as corporate clients impose stricter environmental purchasing standards.

Nescafé reported that 98.6% of its electricity consumption across coffee manufacturing operations came from renewable sources in 2025. This commitment to renewable energy within the coffee value chain sets a benchmark that machine manufacturers and branded beverage suppliers will face pressure to match. Buyers and procurement managers increasingly evaluate the full supply chain footprint, not just the end product.

Nescafé also recorded an 18.3% reduction in greenhouse-gas emissions from green coffee compared with its 2018 baseline during 2025. This reduction demonstrates measurable progress toward lower-carbon coffee production. Machine manufacturers that position their products within sustainable coffee ecosystems, referencing verified supply chain improvements, can command premium pricing from environmentally motivated buyers in Europe and North America.

The Keurig K-Mini Mate, released in 2025, brewed a 12-oz cup in approximately 1 minute 40 seconds including water-heating time. This brew speed benchmark sets a performance floor that mid-range single-serve manufacturers must meet or exceed to remain competitive on convenience. Speed-to-cup has become a primary specification metric as consumers evaluate whether home machines can match the immediacy of out-of-home alternatives.

Drivers

Expanding in-home coffee occasions and workplace coffee decentralization are reshaping demand for coffee machines. Hybrid work models have reduced reliance on centralized corporate breakrooms and created new need for compact machines in home offices and small commercial spaces. This distributes demand across residential and micro-commercial segments, broadening the addressable market beyond traditional categories.

Manufacturers targeting prosumer and small-office buyers gain access to a segment that requires frequent machine replacement and values premium performance over basic output capacity. Distributed work environments also elevate demand for premium at-home experiences, pulling buyers toward higher-margin products. This means equipment suppliers who extend their portfolios into the micro-commercial and home-office range will outperform those locked into conventional residential or large-commercial positioning.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding in-home coffee occasions | +2.5% | North America, Western Europe, Japan, South Korea | Short term (≤ 2 years) |

| Rising solo-household brewing demand | +2.1% | North America, EU, urban APAC | Medium term (2-4 years) |

| Coffee supply recovery supports appliance demand | +1.8% | Global coffee-consuming markets | Short term (≤ 2 years) |

| Premium bean quality pulls machine upgrades | +2.0% | North America, EU, affluent APAC | Medium term (2-4 years) |

| Workplace coffee decentralization | +1.7% | North America, EU, GCC, advanced APAC | Medium term (2-4 years) |

| Repair-aware premium ownership behavior | +1.5% | EU core, UK adjacency, mature APAC | Long term (≥ 4 years) |

Restraints

Café substitution in dense urban markets limits the conversion of coffee consumers into home machine buyers. In cities across Western Europe and East Asia, cafés function as social and work environments, not simply beverage outlets. Consumers who depend on these spaces for daily routines have lower motivation to invest in home equipment, which raises customer-acquisition costs for appliance manufacturers operating in high-density urban markets.

Entry-level commoditization and long replacement cycles compound this pressure. Premium machine manufacturers face slower unit turnover in mature markets where durable products extend ownership periods. Consequently, revenue growth depends more on upgrading existing owners than on converting new buyers, which is a more expensive and less scalable acquisition path.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-price shock to ownership economics | -2.1% | Global coffee-consuming markets | Short term (≤ 2 years) |

| Long replacement cycles in durable segments | -1.7% | EU, North America, Japan | Medium term (2-4 years) |

| Repair-right compliance cost pass-through | -1.4% | EU core, UK adjacency | Medium term (2-4 years) |

| Entry-level commoditization and price wars | -1.6% | Global mass retail channels | Short term (≤ 2 years) |

| Counter-space and housing constraints | -1.3% | Urban Europe, Japan, South Korea, tier-1 cities | Long term (≥ 4 years) |

| Café substitution in dense urban markets | -1.2% | Western Europe, East Asia, affluent urban North America | Medium term (2-4 years) |

Challenges

Supply-chain complexity creates operational vulnerability for premium coffee machine manufacturers. These products require globally sourced components including pumps, boilers, grinders, sensors, electronics, and specialty plastics. Managing this multi-region supplier base increases logistics exposure and compliance obligations. Regulatory requirements for repairability further expand SKU counts, raising inventory costs and documentation burdens across product lines.

Even minor disruptions in critical components can result in 8 to 12 weeks of production slippage for premium models. Manufacturers must therefore hold higher safety-stock levels, which ties up working capital and reduces financial flexibility. This constraint creates a competitive opening for suppliers that invest in dual-sourcing strategies and regional component redundancy before their peers do.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Coffee input price volatility | -1.3% | Global coffee-consuming markets | Medium term (2-4 years) |

| Uneven repair-readiness and obligations | -1.1% | EU core, UK, repair-adopting APAC | Long term (≥ 4 years) |

| Fragmented after-sales service networks | -1.0% | North America, EU, Latin America | Medium term (2-4 years) |

| Product reliability perception gaps | -0.9% | Global mid- and low-end segments | Short term (≤ 2 years) |

| Supply-chain complexity for premium machines | -1.0% | Europe, North America, high-end APAC | Medium term (2-4 years) |

| Demand forecasting under consumption swings | -0.8% | Global | Long term (≥ 4 years) |

Opportunities

Cold and specialty drink modules represent a product-expansion opportunity that addresses a broader range of daily consumption occasions. Manufacturers that add cold-brew preparation, rapid chilling, foam-texture customization, and software-driven recipe management can extend machine usage beyond traditional hot-coffee routines. Systems capable of preparing specialty drinks in under 90 seconds directly compete with out-of-home beverage purchases and reduce café dependency among younger buyers.

Bean-subscription machine bundles and solo-household compact systems offer two additional revenue paths with short execution windows. Subscription bundles create recurring consumable revenue streams alongside hardware sales, improving lifetime customer value. Compact premium systems targeting single-person households in North America, Western Europe, Japan, and South Korea address counter-space constraints while maintaining margin. Early movers in both models will establish ecosystem loyalty before the category attracts broader competitive attention.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Solo-household compact premium systems | +2.4% | North America, Western Europe, Japan, South Korea | Short term (≤ 2 years) |

| Repair-first lifecycle monetization | +2.1% | EU core, UK adjacency, affluent APAC | Medium term (2-4 years) |

| Bean-subscription machine bundles | +2.5% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Office micro-kitchen coffee platforms | +1.9% | North America, EU, GCC, advanced APAC | Medium term (2-4 years) |

| Cold and specialty drink modules | +2.2% | North America, East Asia, Western Europe | Medium term (2-4 years) |

| Usage-data service ecosystems | +1.7% | Global connected-machine markets | Long term (≥ 4 years) |

Key Company Insights

De’Longhi Group holds a structural advantage in the super-automatic espresso segment through its premium product positioning and global retail network. In April 2026, De’Longhi launched the PrimaDonna Aromatic, its most advanced bean-to-cup machine featuring intelligent brewing adaptation. This launch strengthens De’Longhi’s hold on buyers willing to invest in premium at-home espresso systems as residential demand consolidates.

Keurig Dr Pepper dominates the North American single-serve segment through its K-Cup ecosystem, which locks in consumable revenue alongside hardware sales. In October 2025, Keurig secured USD 7 Billion in financing from Apollo and KKR to support its acquisition of JDE Peet’s. Consumer Reports’ 2026 reliability study analyzed data from 81,568 coffee makers purchased between 2017 and 2025, including 47,003 single-serve pod machines, underscoring the category scale Keurig commands.

Key Players

- De’Longhi Group

- Keurig Dr Pepper

- Nestlé Nespresso S.A.

- Koninklijke Philips N.V.

- Robert Bosch GmbH

- Groupe SEB

- Panasonic Corporation

- La Cimbali (Gruppo Cimbali S.p.A.)

- Nuova Simonelli

- Rancilio Group

- JURA Elektroapparate AG

- WMF Group

- Hamilton Beach Brands, Inc.

- BUNN

- Other Key Players

Recent Developments

- August 2025 – Keurig Dr Pepper announced a definitive agreement to acquire JDE Peet’s for approximately EUR 15.7 Billion (USD 18.4 Billion), creating a global coffee powerhouse and strengthening its position in single-serve and coffee machine markets.

- August 2025 – Keurig Dr Pepper announced plans to separate the combined business into 2 independent companies following the JDE Peet’s acquisition, including a dedicated global coffee company focused on coffee systems, brewing technologies, and coffee equipment innovation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.9 Billion |

| Forecast Revenue (2035) | USD 16.6 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Espresso Machines, Drip/Filter Coffee Makers, Single-serve/Capsule Machines, Bean-to-cup Machines); By Technology (Manual/Semi-Automatic, Fully Automatic); By Application (Residential, Commercial); By Distribution Channel (Online, Offline including Supermarkets/Hypermarkets and Specialty Stores) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | De’Longhi Group, Keurig Dr Pepper, Nestlé Nespresso S.A., Koninklijke Philips N.V., Robert Bosch GmbH, Groupe SEB, Panasonic Corporation, La Cimbali (Gruppo Cimbali S.p.A.), Nuova Simonelli, Rancilio Group, JURA Elektroapparate AG, WMF Group, Hamilton Beach Brands, Inc., BUNN, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |