Quick Navigation

Report Overview

The Global Nickel Hydrogen Batteries Market size is expected to be worth around USD 7.7 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 8.8% during the forecast period from 2024 to 2033.

The Nickel Hydrogen Batteries Market is a specialized segment within the energy storage industry, known for its reliability, longevity, and robust performance in demanding applications. These batteries use a nickel hydroxide cathode and hydrogen gas anode with potassium hydroxide as the electrolyte. They are primarily used in aerospace, telecommunications, and high-endurance applications due to their ability to endure extreme temperatures, high energy densities, and prolonged operational lifespans.

The aerospace industry accounts for a substantial portion of the market, as NiH2 batteries are ideal for powering satellites, space probes, and other orbital devices. These batteries can withstand thousands of charge-discharge cycles with minimal degradation, making them essential for space missions. The telecommunications sector also relies on these batteries for backup power in remote and critical operations. Despite lower production volumes compared to other battery technologies, the market benefits from high unit values due to the batteries’ specialized applications.

Key drivers for the market include increased investments in space exploration and satellite deployments. Global satellite launches are expected to exceed 1,800 annually by 2030, fueling demand for NiH2 batteries. The expansion of 5G networks and telecommunications infrastructure also drives the need for reliable backup power solutions, further supporting market growth. Additionally, the long lifespan of these batteries reduces replacement costs and ensures uninterrupted performance in critical systems.

Emerging trends in the market include the development of hybrid battery systems that combine nickel hydrogen with other chemistries to optimize performance. Advances in materials science are enhancing energy density and reducing weight, making NiH2 batteries more competitive. There is also a growing focus on sustainability and recycling, as these batteries are highly recyclable, aligning with global efforts to minimize electronic waste and promote a circular economy.

Key Takeaways

- Nickel Hydrogen Batteries Market size is expected to be worth around USD 7.7 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 8.8%.

- Small-Size Nickel Hydrogen Batteries held a dominant position in the market, capturing more than a 57.2% share.

- Electrode component of the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 41.2% share.

- AA Batteries in the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 31.1% share.

- Batteries with capacities Below 100 AH held a dominant market position in the Nickel Hydrogen Batteries sector, capturing more than a 34.6% share.

- Cylindrical batteries held a dominant market position in the Nickel Hydrogen Batteries sector, capturing more than a 41.2% share.

- 5V batteries in the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 37.4% share.

- Automotive sector held a dominant market position in the Nickel Hydrogen Batteries market, capturing more than a 42.1% share.

- OEM (Original Equipment Manufacturer) sales channel for Nickel Hydrogen Batteries held a dominant market position, capturing more than a 63.2% share.

- Asia Pacific region dominated the market with a 41.1% share, amounting to USD 1.3 billion in revenue.

Business Environment Analysis

The business environment for nickel hydrogen batteries is significantly shaped by technological innovations, regulatory policies, competitive dynamics, and economic factors. These batteries are recognized for their high reliability and extensive lifecycle, making them essential in critical sectors like aerospace and electric vehicles.

Technological Advancements Nickel hydrogen batteries stand out for their durability and high energy density. With the capability to withstand over 20,000 charge cycles, they are ideal for applications demanding high reliability. Notably used in space missions by organizations such as NASA, these batteries are also gaining traction in the hybrid vehicle market due to their efficiency and longevity.

Globally, there’s a shift towards sustainable technologies, positively impacting the nickel hydrogen battery sector. European regulations focused on lowering CO2 emissions are propelling automakers to adopt hybrid technologies, thereby increasing the demand for these batteries. Asian countries like Japan and South Korea are advancing battery recycling and energy-efficient practices, contributing to market expansion.

Leading manufacturers like Panasonic and Duracell are key players, continually innovating to enhance battery performance and reduce costs. Their efforts in R&D are geared towards increasing energy density and reducing weight, catering to the demands of consumer electronics and the burgeoning electric vehicle sector.

The volatility in nickel prices, essential for these batteries, poses a challenge. As per the London Metal Exchange, nickel prices have varied from $12,000 to $18,000 per ton recently, influenced by its demand across various industries including stainless steel and battery production. This variability impacts the production costs and financial strategies of battery producers.

By Type

In 2023, Small-Size Nickel Hydrogen Batteries held a dominant position in the market, capturing more than a 57.2% share. These batteries are preferred for their compact size and reliability, making them ideal for a wide range of portable electronic devices such as cameras, medical instruments, and personal care products. The demand for small-size nickel hydrogen batteries has been steadily increasing due to the growing consumer electronics market and advancements in battery technology that improve charge density and durability.

Large-Sized Nickel Hydrogen Batteries also play a critical role in the market, particularly in sectors that require high energy density and long lifecycle batteries, such as aerospace, automotive, and backup power systems. These batteries are valued for their ability to withstand harsh environments and provide stable performance over an extended period.

In 2023, they accounted for a significant portion of the market, driven by the expanding electric vehicle industry and increasing investments in renewable energy storage solutions. As we move into 2024, both segments are expected to experience growth, influenced by technological advancements and shifting consumer preferences towards more sustainable energy sources.

By Component

In 2023, the Electrode component of the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 41.2% share. The electrode is crucial in battery performance, influencing both capacity and efficiency. This component’s significant market share is driven by continuous improvements in electrode materials that enhance the overall performance and lifespan of batteries. Researchers and manufacturers are focusing on developing more conductive and durable electrode materials to meet the growing demand for efficient energy storage solutions.

The Cathode segment also plays a vital role in the market, as it directly impacts the battery’s voltage and capacity. Innovations in cathode materials have led to higher energy densities and longer battery lifespans, which are essential for applications in electric vehicles and renewable energy systems. Meanwhile, the Anode segment is advancing through the development of materials that can reduce charging times and extend battery life, crucial for consumer electronics and automotive applications.

The Electrolyte component is essential for the operation of Nickel Hydrogen batteries, as it facilitates the flow of ions between the cathode and anode. Developments in electrolyte solutions in 2023 have focused on improving safety and thermal stability, which is particularly important for high-performance applications. Looking into 2024, advancements in each of these components are expected to drive further growth in the Nickel Hydrogen Batteries market, with a strong focus on enhancing efficiency, safety, and sustainability.

By Battery Type

In 2023, AA Batteries in the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 31.1% share. Their widespread use in a variety of household and commercial devices, such as remote controls, toys, and digital cameras, drives their significant market share. These batteries are favored for their balance between size and power capacity, making them a versatile choice for many applications.

Following AA batteries, AAA batteries also hold a substantial segment of the market. These batteries are commonly used in smaller devices that require less power, like wall clocks and portable audio players. Their small size and long life make them ideal for consumers looking for convenience and reliability.

The C and D battery types are typically used in high-drain applications such as emergency equipment and portable lighting. These larger batteries are valued for their longer lifespan and higher energy output, which are essential during prolonged use.

The 9V battery, often used in smoke detectors and other safety equipment, plays a crucial role due to its reliability and longevity. Although it holds a smaller share of the market compared to AA and AAA batteries, its importance in safety-related applications cannot be overstated.

By Capacity

In 2023, batteries with capacities Below 100 AH held a dominant market position in the Nickel Hydrogen Batteries sector, capturing more than a 34.6% share. This category primarily includes batteries used in everyday devices such as handheld electronics, emergency lighting systems, and some medical equipment. Their popularity stems from their compact size, making them ideal for portable applications where space and weight are critical factors.

The 100-300 AH capacity segment also plays a significant role in the market, particularly in medium-duty applications like backup power systems and smaller-scale renewable energy storage. These batteries offer a balance between size and energy storage, catering to needs that require longer durations of power supply or higher energy demands than what the smallest capacity batteries can provide.

For applications requiring even more robust energy solutions, the 300-500 AH and 500-1000 AH segments cater to high-demand systems such as larger renewable energy installations, industrial equipment, and electric vehicles. These batteries are designed to deliver sustained power over prolonged periods, essential for ensuring reliability in critical systems and operations.

Above 1000 AH batteries represent the highest capacity segment, primarily used in heavy industrial applications and grid-scale energy storage. Although this segment captures a smaller market share, its impact on sectors that demand high durability and extended performance is profound. These batteries are crucial for stabilizing power supplies in large-scale operations and contributing significantly to energy management strategies.

By Form Factor

In 2023, Cylindrical batteries held a dominant market position in the Nickel Hydrogen Batteries sector, capturing more than a 41.2% share. This form factor is favored for its robust design and ease of manufacturing, which makes it highly suitable for a wide range of applications, from consumer electronics to industrial power tools. The cylindrical shape efficiently handles internal pressure and is versatile for various packing configurations in devices.

Prismatic batteries also form a significant part of the market. These are preferred in applications where space optimization is crucial, such as in mobile phones and various portable electronic devices. Prismatic batteries offer a compact footprint and allow for more flexible design options in terms of battery layout and space utilization.

Button and coin batteries, while smaller in market share, are essential in very specific applications such as watches, calculators, and medical implants. These batteries are valued for their small size and reliability in devices that require minimal power over extended periods. Their unique form factor is specifically designed for compact, flat battery compartments.

As we move into 2024, each of these segments is poised for further growth. Cylindrical batteries are expected to continue leading due to their adaptability and reliability in both consumer and industrial markets.

Meanwhile, advances in battery technology might boost the demand for prismatic batteries, especially in the rapidly growing sectors of mobile technology and electric vehicles, where efficient space usage is progressively more crucial. Button and coin batteries will remain indispensable in small-scale electronics, maintaining steady growth driven by the ongoing miniaturization of electronic devices.

By Voltage

In 2023, 5V batteries in the Nickel Hydrogen Batteries market held a dominant position, capturing more than a 37.4% share. This voltage is particularly favored for its versatility in powering a broad range of consumer electronics, including smartphones, portable gaming devices, and other handheld gadgets. The popularity of 5V batteries stems from their ability to efficiently meet the power demands of devices that are integral to daily life, combining convenience with high performance.

The 2V and 4V segments also play crucial roles, primarily in applications requiring lower power densities such as emergency lighting systems and some types of backup power supplies. These batteries are chosen for their reliability and cost-effectiveness in systems where high voltage is not a necessity but stability under load is critical.

On the higher end, .6V and 8V batteries cater to specialized needs. .6V batteries, often used in specific industrial and medical equipment, provide essential power in compact forms. Meanwhile, 8V batteries are typically utilized in more robust applications that require a higher voltage, including larger emergency power systems and certain industrial tools.

Nickel Hydrogen Batteries across these voltage segments is expected to expand. Technological advancements and increasing demands for portable and reliable energy sources in various industries will drive growth. The 5V segment is anticipated to continue its dominance due to the ongoing expansion of consumer electronics that require medium-range voltage batteries. Meanwhile, the demand for both lower and higher voltage batteries will likely increase as industries continue to innovate and expand their use of battery-powered solutions.

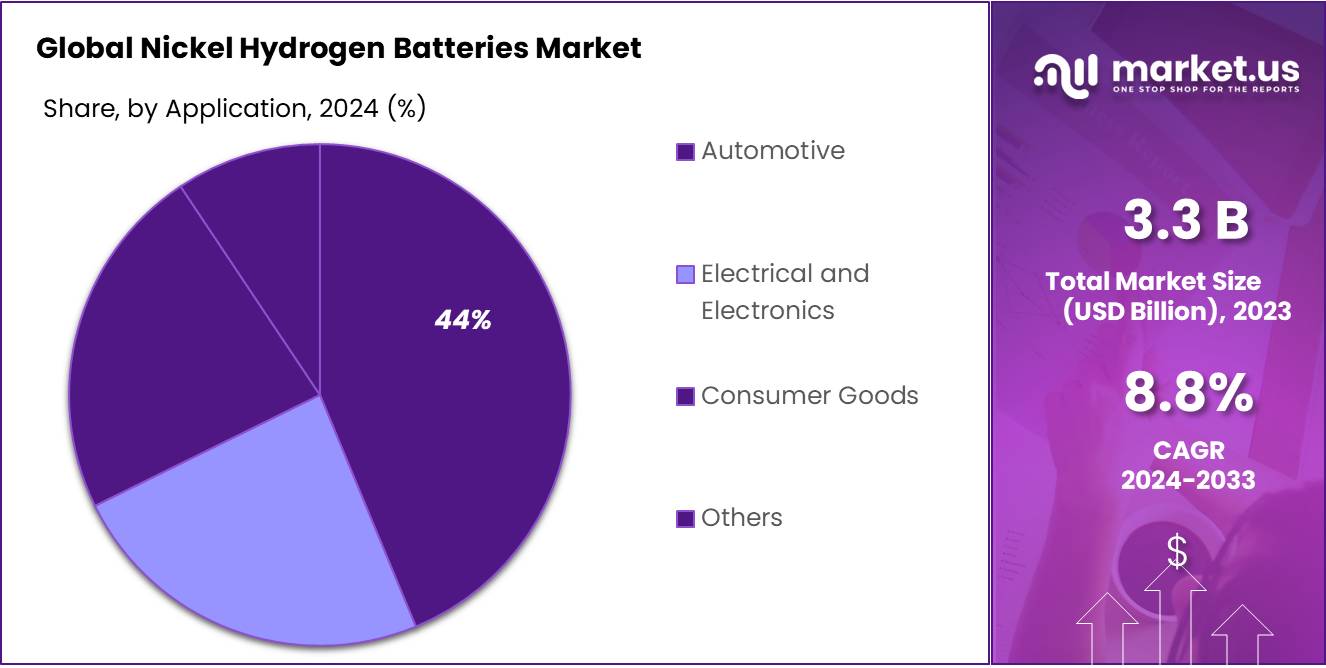

By Application

In 2023, the Automotive sector held a dominant market position in the Nickel Hydrogen Batteries market, capturing more than a 42.1% share. This significant portion is largely due to the growing adoption of hybrid and electric vehicles that rely on advanced battery technologies for improved efficiency and longer range. Nickel Hydrogen batteries are especially favored in this sector for their high energy density and reliability under varying operational conditions, making them suitable for automotive applications.

The Electrical and Electronics segment also represents a substantial share of the market. Nickel Hydrogen batteries in this segment are primarily used in portable electronic devices, emergency power backups, and renewable energy storage solutions. Their ability to provide stable power outputs and withstand frequent charge cycles makes them ideal for high-use electronics.

In the Consumer Goods category, these batteries are integral to a variety of products, from handheld appliances to power tools and personal care items. The demand in this segment is driven by the consumer’s need for durable and reliable power sources that enhance the convenience and functionality of everyday products.

By Sales Channel

In 2023, the OEM (Original Equipment Manufacturer) sales channel for Nickel Hydrogen Batteries held a dominant market position, capturing more than a 63.2% share. This substantial market share is largely attributable to the integration of these batteries into the initial manufacturing of products across various industries, including automotive, consumer electronics, and industrial equipment. OEMs prefer Nickel Hydrogen batteries for their reliability and efficiency, ensuring that the final products meet the high standards demanded by both regulatory bodies and consumers.

The Aftermarket segment, although smaller in comparison, plays a crucial role in the Nickel Hydrogen Batteries market. This channel provides replacement batteries for a wide range of applications that require periodic battery replacement due to wear and tear, such as in automotive hybrids and consumer electronics. The aftermarket is also a critical component for extending the life of existing equipment and reducing electronic waste by allowing consumers to replace batteries rather than disposing of entire devices.

Key Market Segments

By Type

- Small-Size

- Large Sized

By Component

- Electrode

- Cathode

- Anode

- Electrolyte

By Battery Type

- A

- AA

- ААА

- C

- D

- 9V

- Others

By Capacity

- Below 100 AH

- 100-300 AH

- 300-500 AH

- 500-1000 AH

- Above 1000 AH

By Form Factor

- Cylindrical

- Prismatic

- Button

- Coin

By Voltage

- 2V

- 5V

- 4V

- .6V

- 8V

By Application

- Automotive

- Electrical and Electronics

- Consumer Goods

- Others

By Sales Channel

- OEM

- Aftermarket

Drivers

Increased Demand from the Automotive Industry

One of the most significant driving factors for the growth of the Nickel Hydrogen Batteries market is the increasing demand from the automotive industry, particularly for hybrid and electric vehicles (EVs). As governments worldwide push for lower emissions and greener technologies, the automotive sector is rapidly shifting towards more sustainable energy sources. Nickel Hydrogen batteries, known for their high energy density and longer lifecycle compared to traditional batteries, are becoming an integral part of this transition.

In recent years, several government initiatives have been implemented to encourage the adoption of electric vehicles. For instance, the European Union has set ambitious targets to reduce greenhouse gas emissions by 55% by 2030, compared to 1990 levels, under the European Green Deal. This policy framework supports the development of low-emission mobility solutions, including financial incentives for consumers and manufacturers to adopt and produce electric vehicles. These incentives have significantly driven the demand for advanced battery technologies, such as Nickel Hydrogen batteries, which are crucial for enhancing the range and efficiency of EVs.

The automotive industry’s demand for Nickel Hydrogen batteries is not only limited to passenger vehicles but also extends to public transportation systems. Cities around the world are investing in electrifying their public transport fleets as part of their sustainability strategies. For example, according to the International Energy Agency (IEA), global sales of electric buses reached 600,000 units in 2021, with China leading the market, followed by Europe and the United States. This trend is expected to continue as more regions commit to reducing urban pollution and improving air quality.

Furthermore, major automotive manufacturers are incorporating Nickel Hydrogen batteries into their designs to meet the increasing consumer demand for environmentally friendly vehicles. Toyota, for instance, has been a pioneer in using Nickel Hydrogen batteries, particularly in their Prius models, which have set the standard for hybrid technology worldwide. The company reported that by the end of 2020, it had sold over 15 million hybrid vehicles globally, a testament to the growing consumer acceptance and demand for vehicles that use advanced battery technologies.

Restraints

High Production Costs and Competition from Alternative Technologies

A major restraining factor for the growth of the Nickel Hydrogen Batteries market is the high cost associated with their production, coupled with intense competition from alternative battery technologies such as lithium-ion batteries. The high cost is largely due to the complex manufacturing process and the expensive raw materials required for Nickel Hydrogen batteries. These costs often make it difficult for manufacturers to compete on price with more cost-effective alternatives.

The production of Nickel Hydrogen batteries involves sophisticated technology and materials that are more expensive than those used in other types of batteries. For instance, the nickel used in these batteries is a significant cost factor. According to the London Metal Exchange, nickel prices have been highly volatile, with significant price increases observed in recent years due to global demand for nickel in various industries, including batteries. This volatility adds an element of financial risk for manufacturers of Nickel Hydrogen batteries.

Furthermore, in the realm of electric vehicles (EVs) and consumer electronics, lithium-ion batteries have become the dominant technology due to their lower cost, higher energy density, and longer life cycle. Major tech companies and automotive manufacturers have invested heavily in lithium-ion technology, which has led to rapid advancements and cost reductions. For example, Tesla, Inc., a leader in electric vehicles, has continuously improved its battery technology to reduce costs and increase the range of its vehicles. Tesla’s commitment to lithium-ion technology has significantly influenced market trends and consumer expectations, putting additional pressure on the adoption of Nickel Hydrogen batteries.

Governmental policies and subsidies have also favored lithium-ion technologies in many regions. For instance, the U.S. Department of Energy has funded numerous projects to advance lithium-ion battery technology, aiming to reduce dependency on imported oil and improve the country’s energy independence. These initiatives have not only improved the technology but have also made it more accessible and affordable to the general public, further restraining the growth of the Nickel Hydrogen market.

Additionally, consumer preference plays a critical role in this dynamic. With the increasing awareness of the benefits of lithium-ion batteries, such as longer lifespans and quicker charging times, consumers are often more inclined to choose products powered by lithium-ion over those with Nickel Hydrogen batteries. This shift in consumer preference is gradually shaping the market landscape, making it challenging for Nickel Hydrogen batteries to compete.

Opportunity

Expansion in Renewable Energy Storage

A significant growth opportunity for the Nickel Hydrogen Batteries market lies in the renewable energy sector, particularly in energy storage systems. As the world increasingly shifts towards sustainable energy sources like solar and wind, the need for reliable energy storage solutions becomes crucial. Nickel Hydrogen batteries, known for their durability and ability to withstand deep discharge cycles, are well-suited for storing intermittent renewable energy.

The global push for cleaner energy has led to substantial government investments in renewable energy infrastructure. For example, the European Union’s Green Deal aims to make Europe climate-neutral by 2050, which includes significant funding for renewable energy projects. This initiative supports the development of energy storage technologies as a key component of renewable energy systems, creating a substantial market for batteries that can efficiently store and release energy as needed.

Nickel Hydrogen batteries are particularly advantageous for renewable energy storage due to their long life span and stability. Unlike other battery types, they do not suffer from rapid degradation when cycled deeply, making them ideal for applications where batteries are regularly charged and discharged, such as in solar power systems. This capability is critical for maintaining a consistent power supply from inherently unstable renewable sources.

Moreover, the integration of renewable energy sources into national grids requires sophisticated energy management systems. Nickel Hydrogen batteries can play a crucial role here, providing a buffer to balance supply and demand. Their high energy density and quick response times are essential for managing the fluctuations in power generation associated with renewable sources.

In addition to governmental support, consumer demand for sustainable and environmentally friendly technologies is also driving the market. Public awareness of climate change and its impacts has led to increased consumer interest in renewable energy solutions for personal and community use. Home energy storage systems, which allow individuals to store excess energy generated from home solar panels, are becoming increasingly popular. Nickel Hydrogen batteries could serve as a safer and more environmentally friendly alternative to other batteries used in these systems.

The ongoing advancements in Nickel Hydrogen battery technology could further enhance their appeal in the renewable energy sector. Research focused on improving their efficiency and reducing costs can make them more competitive with other technologies like lithium-ion batteries. Innovations that extend their lifespan or enhance their capacity could make Nickel Hydrogen batteries the preferred choice for energy storage in both residential and industrial applications.

Trends

Integration of IoT and Smart Technology in Battery Management

A major trend in the Nickel Hydrogen Batteries market is the integration of Internet of Things (IoT) technologies and smart management systems into battery applications. As industries and consumers alike seek more efficient, reliable, and sustainable energy solutions, the role of advanced technology in managing battery systems has become increasingly important. This trend is particularly evident in sectors such as automotive, renewable energy storage, and smart electronics, where optimizing battery performance can significantly enhance overall system efficiency and longevity.

The use of IoT in battery management involves embedding sensors and connectivity technology within battery systems to monitor various parameters such as temperature, voltage, and current in real time. This data is then used to optimize battery charging and discharging processes, improve safety, and extend the battery’s life by preventing conditions that lead to premature degradation. For instance, smart battery management can precisely control the charge state of Nickel Hydrogen batteries in hybrid vehicles or energy storage systems, ensuring they operate within optimal parameters to maximize energy retention and minimize wear.

Governments and regulatory bodies are also recognizing the potential of smart battery technologies in contributing to environmental sustainability and energy efficiency. For example, the U.S. Department of Energy has funded projects that explore the integration of IoT technologies into battery systems to enhance performance and safety in electric vehicles and grid storage solutions. These initiatives not only support technological innovation but also foster the adoption of smarter energy systems that can interact seamlessly with the broader energy infrastructure.

Consumer electronics manufacturers are incorporating smart management features into portable devices as well. As devices become more energy-intensive and users demand longer battery life, the efficiency of power management becomes crucial. Nickel Hydrogen batteries equipped with smart technology can adapt their behavior based on usage patterns to optimize energy consumption, thereby extending the device’s operational life and reducing the frequency of charge cycles needed.

In the renewable energy sector, the integration of smart technology with Nickel Hydrogen batteries is transforming how solar and wind power are harnessed and stored. Smart energy storage systems can dynamically adjust charging rates or switch between energy sourcing and storage based on real-time energy production and demand data. This capability not only improves the efficiency of renewable energy systems but also enhances grid stability and reliability, which is critical as the proportion of renewable energy in the power mix grows.

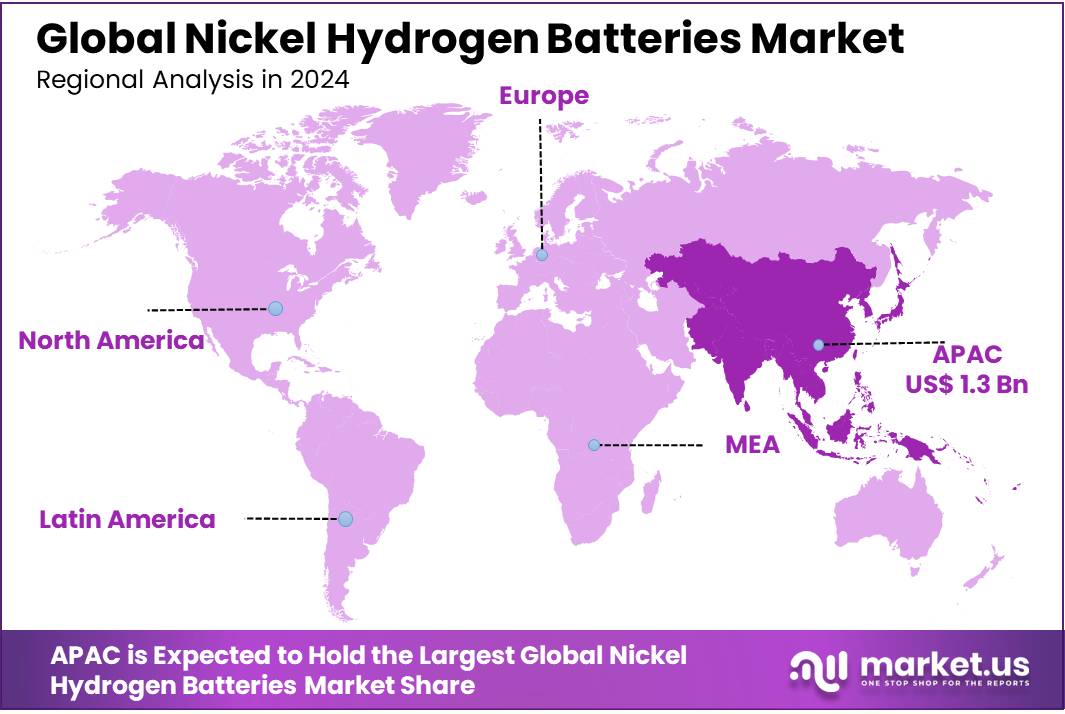

Regional Analysis

The Nickel Hydrogen Batteries market exhibits diverse dynamics across different regions, reflecting varying levels of technology adoption, industrial activity, and government policies. In 2023, the Asia Pacific region dominated the market with a 41.1% share, amounting to USD 1.3 billion in revenue. This substantial market presence is driven by the region’s robust manufacturing sector, particularly in countries like China, Japan, and South Korea, which are major players in electronics, automotive, and renewable energy industries. These countries’ strong focus on advancing battery technology and substantial government investments in clean energy projects further bolster the demand for Nickel Hydrogen batteries.

In North America, the market is propelled by the increasing adoption of electric vehicles (EVs) and a growing emphasis on renewable energy storage solutions. The United States leads in the region, with initiatives to enhance energy storage capabilities and reduce carbon emissions, supporting the uptake of Nickel Hydrogen batteries.

Europe also shows significant growth potential, driven by stringent environmental regulations and high consumer awareness regarding sustainable energy practices. The European Green Deal and similar policies encourage the adoption of green technologies, including advanced battery systems for automotive and energy storage applications.

The markets in the Middle East & Africa and Latin America are smaller but growing. In these regions, the development is spurred by increasing infrastructural projects and the gradual shift towards renewable energy sources. Countries in these regions are beginning to invest in energy infrastructure that integrates battery storage to improve energy security and manage the growing renewable installations effectively.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global Nickel Hydrogen Batteries market, several key players are driving innovation and shaping the industry. Panasonic Holdings Corporation is a prominent player, known for its advanced battery technologies and significant investments in research and development. Panasonic’s Nickel Hydrogen batteries are recognized for their reliability and are widely used in consumer electronics, automotive, and industrial applications.

BYD Company Limited is another major player, leveraging its strong presence in the electric vehicle sector to enhance its battery solutions. These batteries are integral to BYD’s automotive and renewable energy storage systems, contributing to the company’s growth in the energy storage sector.

Top Key Players

- BYD Company Limited

- Corun

- Duracell

- Energizer Holdings

- EPT Battery Co., Ltd

- FDK Corporation

- GP Batteries International Limited

- Great Power Energy

- GS Yuasa

- Highpower International Inc

- Huanyu battery

- Lexel Battery (Coslight)

- Panasonic Holdings Corporation

- Primearth EV Energy Co., Ltd.

- Spectrum Brands (Rayovac)

- VARTA AG

Recent Developments

In 2024, BYD captured a 16.1% share of the global power battery market, with an installed capacity of 69.9 GWh, making it the second-largest battery manufacturer globally.

In 2024, Corun continued to expand its operations and technological capabilities, marking significant growth in the consumer electronics battery market. Their shared charging orders saw an approximate 38% increase compared to 2023, demonstrating a robust expansion in their battery-related services.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.3 Bn |

| Forecast Revenue (2033) | USD 7.7 Bn |

| CAGR (2024-2033) | 8.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Small-Size, Large Sized), By Component (Electrode, Cathode, Anode, Electrolyte), By Battery Type (A, AA, ААА, C, D, 9V, Others), By Capacity (Below 100 AH, 100-300 AH, 300-500 AH, 500-1000 AH, Above 1000 AH), By Form Factor (Cylindrical, Prismatic, Button, Coin), By Voltage (2V, 5V, 4V, .6V, 8V), By Application (Automotive, Electrical and Electronics, Consumer Goods, Others), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | BYD Company Limited, Corun, Duracell, Energizer Holdings, EPT Battery Co., Ltd, FDK Corporation, GP Batteries International Limited, Great Power Energy, GS Yuasa, Highpower International Inc, Huanyu battery, Lexel Battery (Coslight), Panasonic Holdings Corporation, Primearth EV Energy Co., Ltd., Spectrum Brands (Rayovac), VARTA AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |