Quick Navigation

Report Overview

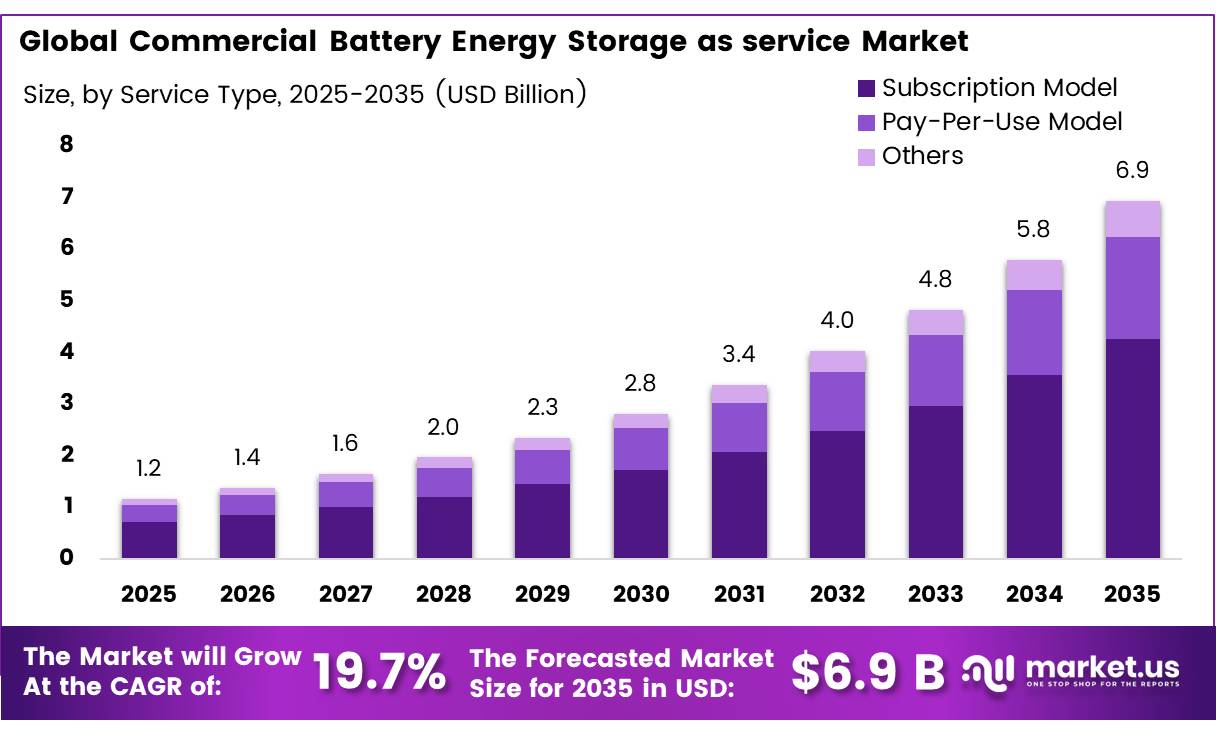

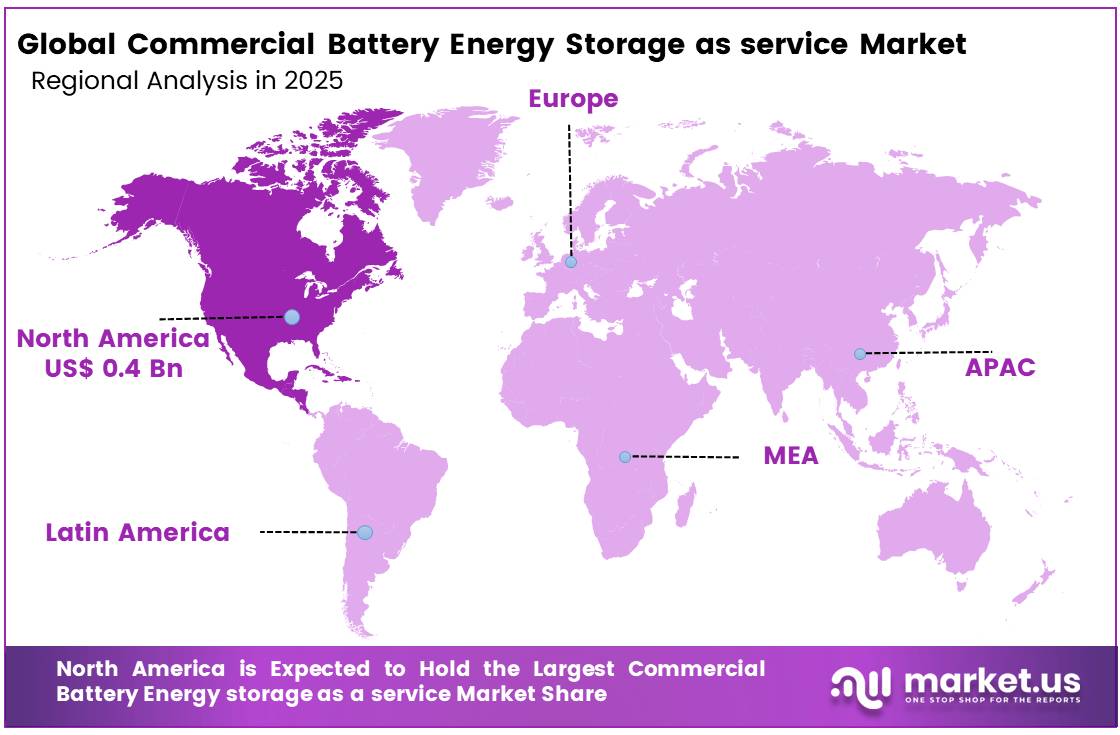

The global Commercial Battery Energy Storage as a service market was valued at USD 1.2 billion in 2025 and is expected to grow to USD 6.9 Billion in 2035. Between 2025 and 2035, this market is estimated to register a CAGR of 19.7%. In 2025, North America market, achieving over 37.0% share with a revenue of USD 0.4 Billion.

Commercial Battery Energy Storage as a Service (BESSaaS) represents a subscription- or contract-based model through which commercial and industrial end-users access battery energy storage infrastructure encompassing hardware, software, and ongoing operations without direct capital ownership. This model has gained considerable traction as grid-scale energy storage deployments surge globally.

- In April 2026, according to the IEA’s Global Energy Review, battery storage recorded 108 GW of new capacity deployed worldwide in 2025, a 40% increase over 2024, with installed capacity now eleven times higher than in 2021. The commercial sector’s pivot toward as-a-service arrangements is driven by the capital intensity of battery installations and the need for managed operational expertise, making BESSaaS a financially pragmatic alternative to direct ownership.

Key Takeaways

- The global Commercial Battery Energy Storage as a Service market was valued at USD 1.2 billion in 2025.

- The global market is projected to grow at a CAGR of 19.7% and is estimated to reach USD 6.9 billion by 2035.

- On the basis of By Service Type, Subscription Model dominated the market, constituting 61.4% of the total market share.

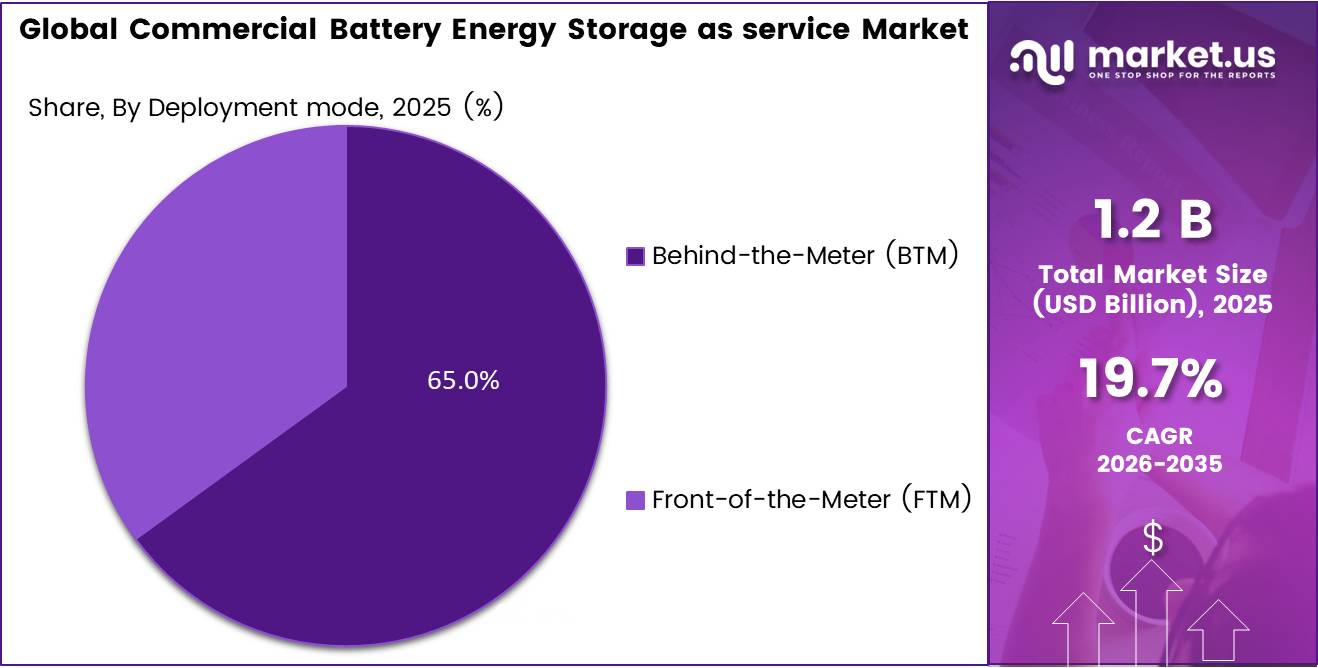

- Based on the Deployment Mode, the Behind-the-Meter (BTM) dominated the Commercial Battery Energy Storage as a Service market, with a substantial market share of around 65.0%.

- Based on the By Enterprise Size, Large Enterprises led the market, comprising 68.5% of the total market.

- Among the By Industry Vertical, the Data Centers held a major share in the Commercial Battery Energy Storage as a Service market,35. 6% of the market share.

- In 2025, the North America was the most dominant region in the Commercial Battery Energy Storage as a Service market, accounting for 34.0% of the total global consumption.

The industrial scenario is shaped by an accelerating confluence of renewable integration needs, grid reliability pressures, and steadily declining battery costs. In 2024, according to the IEA’s Batteries and Secure Energy Transitions report, lithium-ion battery prices declined from USD 1,400 per kilowatt-hour in 2010 to less than USD 140 per kilowatt-hour in 2023, representing one of the fastest cost reductions of any energy technology on record.

- In March 2025, according to the U.S. Energy Information Administration, cumulative utility-scale battery storage capacity in the United States exceeded 26 GW in 2024, with operators reporting plans to add 19.6 GW of additional capacity in 2025.

Key driving factors include supportive public policy frameworks and mandated decarbonization targets. In 2024, according to the IEA’s Batteries and Secure Energy Transitions report, global energy storage capacity must increase sixfold to 1,500 GW by 2030 to facilitate the tripling of renewable energy capacity, with batteries accounting for 90% of that incremental growth, rising 14-fold to 1,200 GW under the Net Zero Emissions by 2050 Scenario.

- In 2024, according to the European Commission, the EU’s Net-Zero Industry Act entered into force, designating batteries as a net-zero technology and streamlining permitting procedures for large-scale storage projects across member states.

- In 2024, according to the U.S. Department of Energy’s Loan Programs Office, the U.S. grid is estimated to require between 225 and 460 GW of long-duration energy storage by 2050, necessitating approximately USD 330 billion in capital investmen.

Service Type Analysis

Subscription Model represents dominant Segment in the Market.

The Subscription Model leading the market at 61.4% share. Its dominance is driven by commercial and industrial users’ preference for predictable operational expenses, efficient energy management, and minimal upfront capital investment. Subscription-based offerings provide ongoing monitoring, maintenance, software updates, and performance enhancements, making them an attractive choice for businesses seeking cost-effective and reliable energy solutions.

Deployment Mode Analysis

Behind-the-Meter (BTM) a significant deployment mode

The Behind-the-Meter (BTM) segment has taken its place as the clear frontrunner, taking 65.0% market share of the market. The popularity of this deployment model can be traced back to the growing implementation of on-site energy storage systems by the commercial and industrial end-users who wish to cut down their electricity bills and reduce peak demand charges while improving energy efficiency. BTM deployment model allows users full control over energy usage, which makes them a good choice for companies looking to optimize operations.

Enterprise size Analysis

Large Enterprises Are the Most Widely Used Enterprise size

The Large Enterprises segment emerging as the leading player with the market capturing 68.5% market share. The supremacy of the said enterprise size segment is explained by the superior financial capability of large enterprises to invest in innovative energy storage technologies and sustainable development. Furthermore, large enterprises including those in the data center, manufacturing, retail, and commercial real estate industries are increasingly relying on energy storage as a service to save money through optimized energy storage and consumption, as well as enhancing grid stability.

On the other hand, the Small and Medium-sized Enterprises (SMEs) segment constitutes an emerging part of the market thanks to rising flexibility offered by energy storage services via subscription or pay-per-use energy storage.

Industry Vertical Analysis

Data Centers Held a Major Share of the Market

The Data Centers segment leading by securing 35.6% of the market share. The dominance of the industry verticals can be attributed to the rising global demand for reliable energy sources and low-latency back up solutions for cloud computing, AI workloads, and hyperscale data infrastructure. Battery energy storage solutions enable the data centers to maximize their savings on energy consumption and provide reliable power to support consistent operation of business activities.

The Retail and Hospitality segment constitutes a major share in the commercial battery energy storage market due to the rising adoption of energy storage systems as a solution for energy cost optimization, peak load management, and power backup systems for shopping malls, hotels, and commercial buildings.

Key Market Segments

By Service Type

- Subscription Model

- Pay-Per-Use Model

- Others

By Deployment Mode

- Behind-the-Meter (BTM)

- Front-of-the-Meter (FTM)

By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Industry Vertical

- Data Centers

- Retail and Hospitality

- Healthcare Facilities

- Others

Drivers

Renewable Integration Mandates Driving Co-Location Storage Obligations

The structural compulsion to pair renewable capacity with dispatchable storage has transitioned from voluntary best practice to regulatory mandate across the three largest energy economies. China’s National Energy Administration requires new solar and wind farms to co-locate storage equal to 10–20% of their nameplate capacity generating an estimated 35 GWh of annual incremental storage demand by 2027.

India’s Solar Energy Corporation of India (SECI) has executed reverse-auction tenders bundling 4 GWh of storage with 12 GW of solar, targeting blended tariffs below INR 4.5/kWh, while the National Electricity Plan (2023) projects national BESS requirements scaling from 82 GWh in 2026–27 to 411 GWh by 2031–32. Australia’s Capacity Investment Scheme (CIS) is progressively delivering contracted storage projects from 2026, supported by a AUD 7.2 billion residential subsidy programme and accelerated coal plant retirements that are hardening grid structural demand.

In the commercial BESSaaS context, these mandates shift the customer acquisition model: rather than individual site-by-site ROI justification, large C&I buyers are entering 10–15 year service agreements that piggyback on co-location mandates for regulatory compliance, effectively converting BESSaaS providers into compliance infrastructure vendors. Global BESS installations the hardware proxy for service contract value leaped 61.3% to 275.3 GWh of new capacity in 2025, and 2026 is projected to add a further 353.4 GWh, creating a visible pipeline of service contract origination opportunities and justifying the +2.8% incremental CAGR contribution.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable Integration Mandates | +2.8% | North America (core), APAC (India, China, Australia), EU | Medium term (2–4 years) |

| Battery Cost Deflation | +2.4% | Global — China supply chain epicentre; North America, EU benefit | Short term (≤ 2 years) |

| Supportive Policy & Tax Incentive Stack | +2.1% | North America (primary), South Asia, EU secondary | Short–Medium term |

| Revenue Stacking via Multi-Service Optimization | +1.8% | North America (CAISO, ERCOT, PJM), EU (FCR/aFRR markets), Australia (NEM) | Medium term (2–4 years) |

| AI Data Centre & Hyperscale Load Growth | +1.5% | North America (core), APAC corridors, EU spill-over | Short–Medium term |

| Regulatory & Market Structure Reform | +1.2% | India (CERC reforms), EU (Clean Energy Package), Australia (CIS), LATAM emerging | Long term (≥ 4 years) |

Restraints

Grid Interconnection Queue Backlogs

As of 2025, approximately 890 GW of storage capacity was sitting in U.S. interconnection queues alone representing the single most consequential execution bottleneck in the sector and a broader LBNL analysis confirmed that the total U.S. interconnection queue had grown to over 2.6 terawatts of generation and storage capacity, more than double the entire installed capacity of the U.S. power fleet, with the average time from interconnection request to commercial operation stretching to nearly five years in 2023 versus under two years in 2008.

At Tamarindo’s March 2026 Investing in Battery Energy Storage conference in London, an overwhelming 98% of industry delegates identified grid connection delays as the single largest execution bottleneck for deployable capital, with 78% citing grid connection queues as the regulatory barrier most responsible for delayed projects across Europe dwarfing market access restrictions (11%) and permitting timelines (4%) as friction sources.

For BESSaaS providers specifically, this restraint compounds into a structural commercial problem: service contracts are typically structured with fixed commissioning dates tied to customer operational timelines, and interconnection delays of 24–48 months force providers to either absorb liquidated damages clauses, renegotiate pricing schedules, or forfeit anchor customers entirely directly compressing project IRRs from a target 12–18% to sub-10% in affected pipelines.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Interconnection Queue Backlogs | −2.6% | North America (core), EU (UK, Germany, Italy), APAC emerging | Medium term (2–4 years) |

| US–China Trade Tariff Escalation | −2.2% | North America (primary), LATAM spill-over, EU secondary | Short term (≤ 2 years) |

| Battery Degradation & Lifecycle Risk | −1.9% | Global — APAC and North America highest exposure | Long term (≥ 4 years) |

| Fire Safety & Thermal Runaway Compliance Burden | −1.6% | North America, EU, South Korea, Australia | Medium term (2–4 years) |

| Critical Mineral Supply Concentration | −1.4% | North America, EU (non-China aligned markets) | Medium–Long term |

| Skilled Workforce Deficit | −1.1% | India (acute), North America, EU, Sub-Saharan Africa | Medium term (2–4 years) |

Opportunity

Second-Life EV Battery Integration into BESSaaS Fleets

The integration of second-life EV batteries repurposed after falling below ~80% State of Health for automotive use into BESSaaS asset fleets at a BoM cost estimated at USD 45–70/kWh versus USD 100–130/kWh for equivalent new LFP packs, representing a structural 40–60% hardware cost reduction. Industry projections indicate that second-life EV battery capacity will scale from approximately 25–30 GWh in 2025 to 330–350 GWh by 2030 at a near-65% CAGR, driven by the retirement of early EV cohorts from Tesla, BYD, Nissan, and GM at volumes sufficient to underpin commercial stationary storage deployment at scale.

The key commercial model enabled by second-life integration is a two-tier BESSaaS pricing architecture: Tier 1 contracts are served by new-cell assets with guaranteed performance, while Tier 2 contracts are served by second-life packs acquired at USD 50–65/kWh a price point that drops the total installed cost of a commercial BESS system below USD 180/kWh fully installed, potentially reducing payback periods to 4–5 years versus the current 7–8 years and opening an entirely new customer segment of mid-market retailers, logistics hubs, and educational institutions that previously could not justify storage investment.

The EU Battery Regulation’s Battery Passport requirement accelerates this opportunity by creating a standardised data layer State of Health certification, cycle history, chemistry identification that reduces the due diligence cost of second-life asset screening from an estimated USD 15–25/kWh today to below USD 3–5/kWh, dramatically improving the scalability of second-life sourcing programmes and giving BESSaaS providers that establish OEM partnerships with major automotive manufacturers in 2026–2027 a first-mover cost advantage estimated at 15–20 margin points versus peers continuing to rely exclusively on new-cell procurement.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| VPP-as-a-Service Aggregation Layer | +3.2% | North America (CAISO, ERCOT, PJM), EU (FCR/aFRR markets), Australia | Short term (≤ 2 years) |

| Second-Life EV Battery Integration | +2.6% | EU (Battery Passport mandate), China, North America | Medium term (2–4 years) |

| SME & Tier-2 Commercial Market Penetration | +2.3% | India (primary), Southeast Asia, LATAM, Sub-Saharan Africa | Short–Medium term |

| Long-Duration Energy Storage (LDES) as a Service | +2.0% | EU (Spain, Portugal, Germany), Australia, North America (CAISO) | Medium term (2–4 years) |

| Carbon Credit & ESG Compliance Monetization | +1.6% | North America, EU (EU ETS), India (CCTS), South Korea | Medium–Long term |

| M&A Roll-Up of Fragmented Asset Operators | +1.4% | North America, UK, Australia | Short term (≤ 2 years) |

Challenges

Ancillary Market Revenue Cannibalisation from Fleet Scaling

Modo Energy’s 2026 dataset quantifies this most sharply in the UK: frequency services fell from approximately 80% of the average BESS revenue stack in 2022 to just 20% by 2024, as installed capacity grew from sub-1 GWh to over 6 GWh during that period a near-linear inverse relationship between fleet size and ancillary yield that is structurally irreversible once markets saturate.

Germany exhibits an analogous trajectory: ancillary service revenue was projected to decline from 55% of German BESS revenue in 2023 to approximately 5% by 2030 as FCR and aFRR markets absorb more capacity than their structural volume requirements permit, while ERCOT ancillary markets which dominated U.S. BESS revenue in 2023 had already diminished to a fraction of their prior contribution by 2025 as Texas-deployed capacity crossed the 12 GW threshold.

For BESSaaS providers with deployed fleets whose 10-year P50 revenue models were constructed at 2022–2023 ancillary price levels, per-MW annual revenues in Germany fell by approximately EUR 9,000/MW between summer 2024 and summer 2025, creating a revenue shortfall that may require contract renegotiation, augmentation deferral, or equity cash-injection to maintain DSCR compliance — each of which imposes a structural drag on provider capital efficiency and new project origination capacity.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ancillary Market Revenue Cannibalisation | −2.4% | EU (UK, Germany, France), North America (ERCOT, CAISO), Australia (NEM) | Long term (≥ 4 years) |

| Merchant Revenue Bankability Gap | −2.1% | EU (cross-market), North America, India (emerging BESS pipeline) | Medium term (2–4 years) |

| OEM Supplier Concentration Risk | −1.8% | North America, EU, India (non-China aligned markets) | Long term (≥ 4 years) |

| Cybersecurity & EMS Vulnerability Exposure | −1.5% | North America, EU (CRA compliance from Sept 2026), APAC | Medium term (2–4 years) |

| Technology Obsolescence & Upgrade Cycle Risk | −1.3% | Global — all BESSaaS contract markets | Long term (≥ 4 years) |

| Multi-Jurisdiction Regulatory & Standards Fragmentation | −1.1% | EU (cross-border), India vs. SEA, North America (state-level variation) | Medium term (2–4 years) |

Geopolitical Impact Analysis

The current political situation around the world is greatly affecting the Commercial Battery Energy Storage as a Service Market. Factors like supply chain issues, changes in trade policies, reliance on certain raw materials, and worries about energy security are playing a big role. The market heavily depends on important minerals such as lithium, nickel, cobalt, and graphite, which are mostly found in a few countries. This makes the supply chain more vulnerable to political conflicts and export limits.

The geopolitics of international tension and conflict have begun influencing the growth of the CBESS market. As pointed out by the U.S. Department of Energy, China is central to the production of lithium-ion batteries and the provision of raw materials worldwide. Shifts in policy on China’s side regarding exportation or manufacturing could have an effect on the global availability of battery systems and their pricing. With the increasing tension between China and the U.S., governments have started projects that encourage domestic battery manufacturing and energy infrastructure in both the U.S. and Europe.

Conversely, events such as the conflict between Russia and Ukraine have proven to emphasize the importance of energy security. The authorities, including even the European Commission, are advocating for energy storage and renewable energy projects that reduce reliance on foreign energy technologies. Transportation disruptions and increased transport costs have influenced project schedules too. While geopolitical issues may influence costs, they have certainly led to rapid investments in dependable and localized battery energy storage systems around the world.

Regional Analysis

North America holds a dominant position in the Commercial Battery Energy Storage as a Service (CBESS) market, accounting for over 37.0% share with a revenue of US$ 0.4 Billion. The region’s leadership is driven by widespread adoption of renewable energy, advanced grid infrastructure, and strong demand from data centers and commercial enterprises. The United States remains the key contributor, supported by government incentives, tax credits, and significant investments in clean energy storage. Continuous efforts toward power grid modernization and carbon emission reduction are further strengthening market growth in the region.

The Asia Pacific region is set to become the world’s fastest-growing market owing to rapid industrialization, growing electricity needs, and substantial investment in renewable energy sources in countries such as China, India, Japan, and South Korea. Favorable government policies and smart grid infrastructure deployment have led to the adoption of batteries as a service solutions.

Key Regions and Countries Covered

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Firms engaged in the CBESS sector have shown increased interest in providing reliable, scalable, and affordable energy solutions to clients who require sustainable solutions that address energy security and savings needs. The differentiation of players in the market can be based on whether they provide end-to-end solutions such as installation of energy storage solutions, energy management using Artificial Intelligence, monitoring services, and grid optimization.

Companies in the Commercial Battery Energy Storage as a Service (CBESS) market are increasingly investing in software solutions that can forecast energy demand, automate energy management, and enable real-time energy trading, providing added value to commercial and industrial customers. Leading players in this space include Tesla, Fluence Energy, LG Energy Solution, ABB, and Wartsila, which combine battery hardware with advanced energy management platforms to deliver integrated services.

The Major Players In The Industry

- Enel X S.r.l.

- Bernhard Energy Solutions

- Honeywell International Inc.

- Wärtsilä Corporation

- Renewance Inc.

- Veolia Environnement S.A.

- NRStor Inc.

- Hydrostor Inc.

- Suntuity

- YSG Solar

- Customized Energy Solutions Ltd.

- Others

Key Development

- In December 2025, Bernhard Energy Solutions entered a USD 54.2 million, 30-year partnership with Beacon Health System, targeting USD 191 million in utility savings, a 35.5% reduction in annual utility costs and a 26.2% reduction in carbon emissions. In April 2026, ENFRA also formed a 30-year partnership with Memorial Health, covering four hospital campuses and expected to generate USD 115.3 million in total savings, including approximately USD 2 million in the first year after construction.

- In May 2026, Enel X received another 32 MW VPP award in New South Wales, increasing its Roadmap-backed portfolio beyond the existing 95 MW and supporting around 300 MW of flexible capacity across the state. The company also secured 480 MW in Great Britain’s 2026 T-4 Capacity Market auction, where participating commercial battery and flexible-load customers could earn about GBP 54,000 per MW annually for four years. By June 2026, Enel X managed 10 GW of global flexible capacity across 14 countries, more than 100 programs, 8,000 customers and 16,000 sites.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.2 Bn |

| Forecast Revenue (2035) | USD 6.9 Bn |

| CAGR (2026-2035) | 19.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Subscription Model, Pay-Per-Use Model, Others), By Deployment Mode(Behind-the-meter, Front-the-Meter), By Enterprise Mode (Large Enterprises, Small and Medium Enterprises), By Industrial Vertical (Data Centered, Retailed & Hospitality, Healthcare Facilities, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Tesla Inc., BYD Company Limited, ABB Ltd., Fluence Energy Inc., Sungrow Power Supply Co., Ltd., Contemporary Amperex Technology, Siemens AG, Schneider Electric SE, ENGIE SA, Enel X S.r.l., Bernhard Energy Solutions, Honeywell International Inc., Wärtsilä Corporation, Renuwance Inc., Veolia Environnement S.A., NRStor Inc., Hydrostor Inc., Suntuity, YSG Solar, Customized Energy Solutions Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |