Quick Navigation

- Report Scope

- Key Takeaways

- Analysts’ Viewpoint

- Key Statistics

- Regional Analysis

- By Spectrum

- By Image Processing Technology

- By Resolution

- By Industry Vertical

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

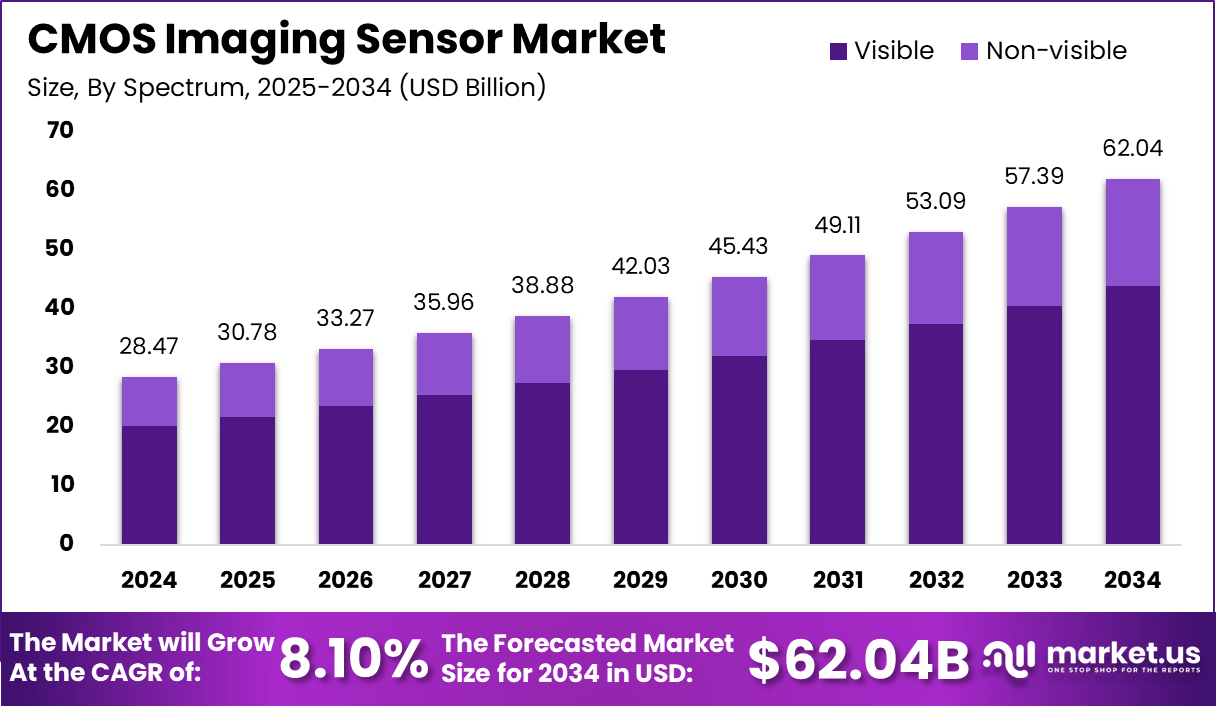

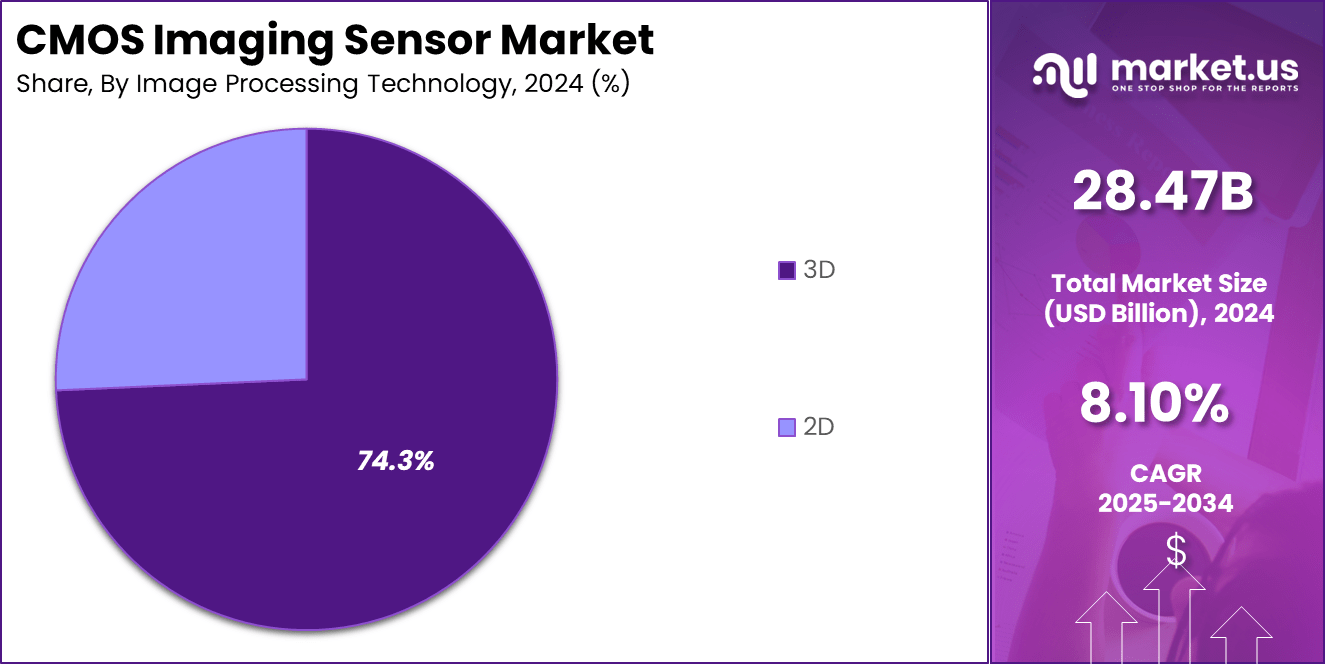

The Global CMOS Imaging Sensor Market is expected to be worth around USD 62.04 Billion by 2034, up from USD 28.47 Billion in 2024. It is expected to grow at a CAGR of 8.10% from 2025 to 2034.

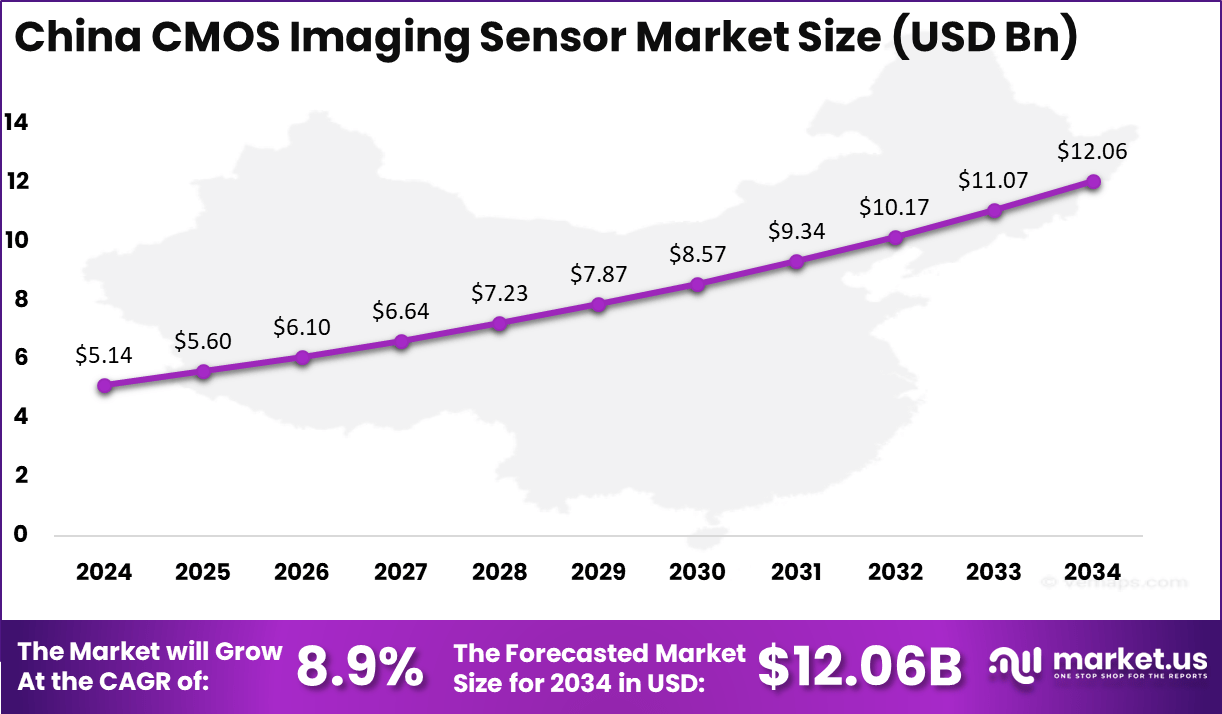

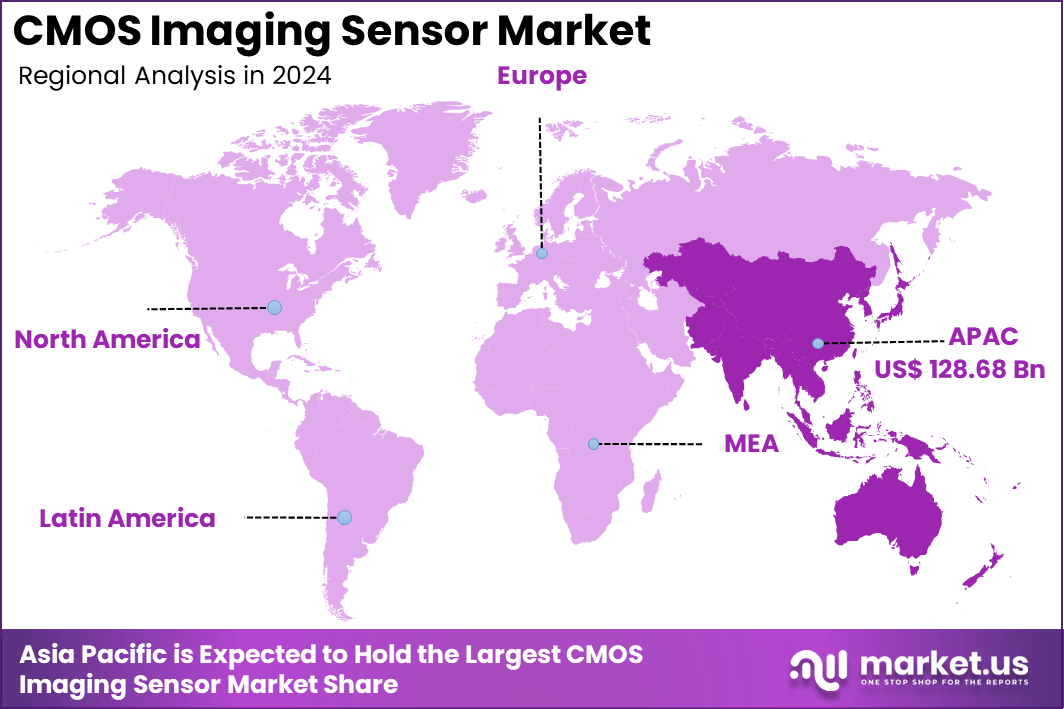

In 2024, Asia-Pacific held a dominant market position, capturing over a 45.2% share and earning USD 128.68 Billion in revenue. Further, China dominates the market by USD 5.14 Billion, steadily holding a strong position with a CAGR of 8.9%.

The CMOS (Complementary Metal-Oxide-Semiconductor) imaging sensor market has experienced significant growth over the past decade, establishing itself as a cornerstone in various imaging applications. The growth trajectory underscores the increasing adoption of CMOS sensors across multiple sectors, driven by their inherent advantages over traditional technologies.

Several factors are propelling the expansion of the CMOS imaging sensor market. The escalating demand for high-resolution cameras in smartphones and surveillance systems has significantly boosted the adoption of CMOS sensors.

In the automotive industry, the integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies relies heavily on CMOS sensors for real-time imaging and object detection. Additionally, the medical field’s growing dependence on imaging technologies for diagnostics and treatment has further amplified the demand for these sensors.

Key Takeaways

- Market Growth: The global CMOS imaging sensor market is expected to grow from USD 28.47 billion in 2024 to USD 62.04 billion by 2034, reflecting a CAGR of 8.10%.

- Dominant Spectrum: The visible spectrum segment holds the majority share at 70.7%, driven by its application in smartphones, cameras, and surveillance systems.

- Technological Shift: 3D imaging processing technology is leading with a 74.3% market share, emphasizing the rising demand for advanced imaging in automotive, healthcare, and AR/VR applications.

- Resolution Preference: High-resolution CMOS sensors are in demand, with the above 16 MP segment accounting for 42.7% of the market.

- Industry Leadership: Consumer electronics remains the largest industry vertical, holding a 36.7% market share, driven by smartphones, laptops, and wearables.

- Regional Dominance: Asia-Pacific leads the market with a 45.2% share, fueled by strong manufacturing capabilities and increasing adoption of CMOS sensors.

- China’s Market: The Chinese CMOS imaging sensor market is valued at USD 5.14 billion, with a CAGR of 8.9%, making it a key growth driver in the region.

Analysts’ Viewpoint

The market’s appetite for CMOS imaging sensors continues to grow, particularly in emerging applications such as artificial intelligence (AI), augmented reality (AR), and virtual reality (VR). These technologies require advanced imaging capabilities, positioning CMOS sensors as critical components.

Moreover, the industrial sector’s shift towards automation and machine vision systems presents substantial opportunities for CMOS sensor manufacturers. The trend towards smart cities and the proliferation of Internet of Things (IoT) devices also contribute to the increasing demand for compact, energy-efficient imaging solutions.

Technological advancements have been pivotal in enhancing the performance and adoption of CMOS imaging sensors. The transition from charge-coupled devices (CCDs) to CMOS technology has resulted in lower power consumption, faster processing speeds, and cost-effectiveness.

Innovations such as back-illuminated sensors have improved low-light performance, while stacked CMOS architectures have enabled higher pixel densities and enhanced image quality. These developments have broadened the applicability of CMOS sensors, making them suitable for a wider range of imaging applications.

Key Statistics

Segmentation and Applications

- Applications: Aerospace, automotive, consumer electronics, healthcare, industrial, entertainment, security & surveillance.

- Wafer Size Segmentation: 200mm, 300mm, and others.

User and Usage Statistics

- Consumer Electronics: CMOS image sensors are widely used in smartphones, laptops, and DSLR cameras.

- Automotive Sector: Increasing use in electric and autonomous vehicles for safety and navigation systems.

User and Usage Statistics

- Consumer Electronics:

- Smartphones: Over 1.5 billion units sold annually, with each device containing multiple CMOS image sensors.

- Laptops: Approximately 200 million units sold annually.

- DSLR Cameras: Around 10 million units sold annually.

- Automotive Sector:

- ADAS Systems: Over 50 million vehicles equipped with ADAS systems annually.

Technological Advancements

- Pixel Technology:

- Resolution: Up to 200 MP in smartphones.

- Sensors like Sony’s IMX735 and Samsung’s ISOCELL HP2: Enhance image quality and resolution.

- Innovation:

- Continuous R&D: Necessary to keep up with technological advancements.

- Quantum Dot and 3D Stacked Technologies: Emerging trends in CMOS image sensor development.

Regional Analysis

China Region Market Size

In Asia-Pacific, China dominates the market size, holding a strong position with a steady growth trajectory. The country leads the region’s CMOS sensor industry, driven by its well-established electronics manufacturing ecosystem and increasing adoption of smart technologies. With a market size of USD 5.14 billion and a CAGR of 8.9%, China continues to strengthen its foothold, making it a key player in the global CMOS imaging sensor market.

The CMOS imaging sensor market is witnessing significant growth, driven by advancements in imaging technology and increasing demand across various industries. The market is expected to expand at a steady pace, fueled by the rising adoption of high-resolution sensors, 3D imaging technology, and AI-powered applications. Consumer electronics, particularly smartphones, laptops, and wearables, remain the largest end-use segment, with continuous demand for improved camera performance.

Technological innovations, such as back-illuminated sensors and stacked CMOS architecture, have further enhanced image quality, low-light performance, and processing speed. The growing integration of CMOS sensors in the automotive industry, especially in advanced driver-assistance systems (ADAS), is another key driver of market expansion. Additionally, sectors such as healthcare, industrial automation, and security surveillance are contributing to the increasing adoption of these sensors.

Asia Pacific Market Size

In 2024, Asia-Pacific held a dominant market position in the CMOS imaging sensor industry, capturing more than a 45.2% share, equating to approximately USD 13.64 billion in revenue. This leadership is primarily attributed to the region’s robust consumer electronics sector, particularly the proliferation of smartphones and digital cameras that extensively utilize CMOS sensors. Countries like China, Japan, South Korea, and Taiwan have established themselves as major hubs for electronics manufacturing, further bolstering the market’s growth in this region.

The automotive industry’s rapid expansion in Asia-Pacific also plays a crucial role in this dominance. The integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies relies heavily on high-quality imaging sensors. As regional automotive manufacturers increasingly adopt these technologies, the demand for CMOS imaging sensors has surged, contributing significantly to market revenue.

Moreover, the region’s focus on industrial automation and smart manufacturing has led to increased adoption of machine vision systems, which depend on CMOS imaging sensors for quality control and inspection processes. This trend towards automation, coupled with supportive government initiatives promoting smart city projects, has further cemented Asia-Pacific’s leading position in the market.

In contrast, other regions like North America and Europe, while holding substantial market shares, trail behind Asia-Pacific. Their markets are characterized by a strong emphasis on research and development and early adoption of advanced technologies, but they lack the extensive manufacturing base that Asia-Pacific possesses. Latin America, the Middle East, and Africa are emerging markets with growing potential, primarily driven by increasing investments in infrastructure and technology, yet they currently account for a smaller portion of the global market share.

By Spectrum

In 2024, the Visible segment held a dominant market position, capturing more than a 70.7% share in the CMOS imaging sensor market. This dominance is primarily due to the widespread use of visible spectrum imaging in consumer electronics, particularly smartphones, digital cameras, and surveillance systems.

The growing demand for high-resolution imaging, enhanced low-light performance, and AI-powered camera features in smartphones has significantly driven the adoption of CMOS visible sensors. Additionally, industries such as automotive, healthcare, and industrial automation are integrating visible spectrum CMOS sensors for applications like ADAS (Advanced Driver Assistance Systems), medical imaging, and machine vision systems.

The increasing deployment of smart surveillance systems in urban areas and smart cities has also contributed to the segment’s leadership, as visible sensors provide high-quality image capture for security and monitoring purposes.

Furthermore, advancements in back-illuminated sensor technology and stacked CMOS architecture have improved the efficiency and performance of visible CMOS sensors, making them the preferred choice for most imaging applications. As a result, the Visible segment continues to lead the market, while the Non-visible segment, though growing, remains primarily focused on specialized applications like thermal imaging, night vision, and infrared sensing.

By Image Processing Technology

In 2024, the 3D segment held a dominant market position, capturing more than a 74.3% share in the CMOS imaging sensor market. This strong leadership is primarily driven by the increasing demand for depth-sensing technology across various industries, including smartphones, automotive, healthcare, and industrial automation.

The widespread adoption of 3D imaging in facial recognition, augmented reality (AR), virtual reality (VR), and LiDAR-based applications has significantly contributed to the segment’s growth. Smartphones now incorporate 3D CMOS sensors for enhanced biometric authentication, portrait photography, and immersive AR experiences, further fueling demand.

In the automotive sector, 3D CMOS sensors play a crucial role in ADAS (Advanced Driver-Assistance Systems) and autonomous driving, enabling real-time depth perception and obstacle detection. Similarly, in healthcare, 3D imaging is revolutionizing medical diagnostics, robotic surgeries, and dental scanning, making it an indispensable tool in modern medicine.

Industrial applications, such as machine vision and robotics, are also leveraging 3D imaging for precision measurement and object tracking. With continuous advancements in structured light, time-of-flight (ToF), and stereoscopic imaging technologies, the 3D segment remains at the forefront of innovation, making it the preferred choice over traditional 2D imaging solutions.

By Resolution

In 2024, the Above 16 MP segment held a dominant market position, capturing more than a 42.7% share in the CMOS imaging sensor market. This leadership is primarily driven by the increasing demand for high-resolution imaging in smartphones, professional cameras, medical imaging, and security surveillance systems.

With smartphone manufacturers continuously pushing for higher megapixel counts to enhance image quality, zoom capabilities, and low-light performance, CMOS sensors above 16 MP have become the industry standard. Flagship smartphones now feature 50 MP to 200 MP sensors, significantly contributing to the growth of this segment.

Beyond consumer electronics, professional photography and videography rely heavily on high-resolution sensors for detailed image capture and 8K video recording. In the healthcare sector, medical imaging applications such as digital pathology, ophthalmology, and radiology require ultra-high-resolution sensors for accurate diagnostics.

The security and surveillance industry also benefits from high-resolution sensors, as they provide clearer images with enhanced facial recognition capabilities. With continuous advancements in sensor technology, pixel-binning techniques, and AI-driven image processing, the Above 16 MP segment remains the preferred choice across industries, driving its sustained market dominance over lower-resolution categories.

By Industry Vertical

In 2024, the Consumer Electronics segment held a dominant market position, capturing more than a 36.7% share in the CMOS imaging sensor market. This leadership is driven by the rapid advancements in smartphone cameras, tablets, laptops, smart home devices, and wearable technology, all of which rely heavily on CMOS imaging sensors.

The increasing consumer demand for high-resolution imaging, AI-powered camera enhancements, and superior low-light performance has fueled the widespread adoption of CMOS sensors in mobile devices. Leading smartphone manufacturers are integrating multi-camera setups with ultra-high megapixel sensors, further propelling the growth of this segment.

Beyond smartphones, laptops and tablets are also adopting advanced CMOS sensors for improved webcams and facial recognition features, driven by the rising trend of remote work and virtual communication. Additionally, wearable devices, such as smartwatches and AR/VR headsets, are increasingly utilizing CMOS sensors for health monitoring and immersive experiences.

The gaming industry has also contributed to the demand, with AR/VR headsets requiring advanced image sensors for enhanced depth sensing and real-world interaction. With continuous innovations in sensor miniaturization, AI-driven image processing, and energy-efficient designs, the Consumer Electronics segment remains at the forefront of the CMOS imaging sensor market, solidifying its dominant position over other industry verticals.

Key Market Segments

By Spectrum

- Visible

- Non-visible

By Image Processing Technology

- 2D

- 3D

By Resolution

- Up to 5 MP

- 5 MP to 12 MP

- 12 MP to 16 MP

- Above 16 MP

By Industry Vertical

- Aerospace & Defense

- Automotive

- Consumer Electronics

- Healthcare & Lifesciences

- Industrial

- Security & Surveillance

- Others

Driving Factors

Proliferation of Smartphones with Advanced Imaging Capabilities

The rapid proliferation of smartphones equipped with advanced imaging capabilities has been a significant driving force behind the growth of the CMOS image sensor market. Consumers increasingly demand high-quality cameras in their mobile devices, seeking features such as high-resolution photography, enhanced low-light performance, and sophisticated computational photography functions.

This consumer preference has compelled smartphone manufacturers to integrate cutting-edge CMOS image sensors into their products. The versatility and cost-effectiveness of CMOS technology make it ideal for meeting these demands, allowing for the development of compact, energy-efficient sensors that deliver exceptional image quality. As a result, the widespread adoption of smartphones with superior camera functionalities continues to propel the CMOS image sensor market forward.

Restraining Factors

Price Volatility of Raw Materials

Despite the positive growth trajectory, the CMOS image sensor market faces challenges, notably the price volatility of raw materials. Fluctuations in the costs of essential components can significantly impact production expenses, leading to increased pricing pressures on manufacturers.

This volatility can hinder the profitability of companies within the market, particularly affecting smaller players who may struggle to absorb sudden cost increases. Consequently, managing these fluctuations becomes crucial for maintaining competitiveness and ensuring sustainable growth in the CMOS image sensor industry.

Growth Opportunities

Integration in Automotive Advanced Driver-Assistance Systems (ADAS)

The integration of CMOS image sensors into automotive advanced driver-assistance systems (ADAS) presents a substantial growth opportunity for the market. As the automotive industry advances towards higher levels of autonomy, the demand for reliable, high-quality imaging sensors has surged.

CMOS sensors are pivotal in enabling features such as lane departure warnings, collision avoidance, and parking assistance. Their ability to deliver real-time, high-resolution imaging under varying lighting conditions makes them indispensable in enhancing vehicle safety and driver experience. This expanding application in the automotive sector is poised to drive significant growth in the CMOS image sensor market.

Challenging Factors

Intense Market Competition and Innovation Pressure

The CMOS image sensor market is characterized by intense competition, compelling manufacturers to continually innovate to maintain their market positions. This competitive landscape poses challenges, especially for smaller companies that may lack the resources for extensive research and development. The constant pressure to enhance sensor performance, reduce costs, and introduce new features necessitates substantial investment in innovation.

Companies must balance the need for technological advancement with profitability, navigating a complex environment where rapid changes in consumer preferences and technological standards are the norms. This relentless drive for innovation, while fostering progress, also presents significant challenges in terms of resource allocation and strategic planning within the CMOS image sensor industry.

Growth Factors

Rising Demand in Automotive Safety Systems

The CMOS image sensor market is experiencing significant growth, largely driven by the automotive industry’s increasing emphasis on safety and automation. Advanced Driver-Assistance Systems (ADAS) and autonomous vehicles rely heavily on high-quality imaging sensors to function effectively.

These systems utilize CMOS sensors for applications such as lane departure warnings, collision avoidance, and parking assistance, enhancing overall vehicle safety. According to industry reports, the integration of ADAS is expected to grow at a compound annual growth rate (CAGR) of 9.16% from 2024 to 2031, directly influencing the demand for CMOS image sensors.

Emerging Trends

Adoption in Medical Imaging Technologies

An emerging trend in the CMOS image sensor market is their growing adoption in medical imaging technologies. Medical fields such as endoscopy, ophthalmology, and dental imaging are increasingly utilizing CMOS sensors due to their compact size, high resolution, and cost-effectiveness. The global medical imaging market is projected to reach USD 48.15 billion by 2034, with CMOS sensors contributing significantly to this growth.

The ability of CMOS sensors to provide real-time imaging with reduced power consumption makes them ideal for portable and wearable medical devices. This trend not only enhances diagnostic capabilities but also improves patient comfort and accessibility to medical imaging, indicating a promising avenue for market expansion.

Business Benefits

Cost Efficiency and Technological Advancements

Businesses are reaping substantial benefits from the advancements in CMOS image sensor technology, particularly in terms of cost efficiency and enhanced performance. The manufacturing process of CMOS sensors is compatible with standard semiconductor fabrication techniques, leading to lower production costs compared to traditional Charge-Coupled Devices (CCDs). This cost advantage enables companies to offer high-quality imaging solutions at competitive prices, thereby increasing their market share.

Technological advancements have also led to improved sensor performance, including higher resolution, faster frame rates, and better low-light sensitivity. These enhancements open up new application areas and revenue streams for businesses, from consumer electronics to industrial automation, thereby solidifying their market position.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In recent years, Panasonic Corporation has strategically focused on restructuring and partnerships to strengthen its market position. In December 2024, the company announced significant personnel changes aimed at enhancing its operational efficiency and global competitiveness. These changes reflect Panasonic’s commitment to adapting to evolving market dynamics and ensuring sustained growth.

Additionally, in July 2024, Panasonic Connect Co., Ltd., a subsidiary of Panasonic Corporation, entered into a strategic partnership with ORIX Corporation to launch a new projector business. In this venture, ORIX holds an 80% stake, while Panasonic Connect retains 20%. This collaboration aims to leverage ORIX’s investment capabilities and Panasonic’s technological expertise to drive innovation and growth in the projector market.

Canon Inc., a leader in imaging and optical products, continues to innovate in the CMOS imaging sensor market. The company has been focusing on developing high-resolution sensors to meet the growing demand for superior image quality in various applications, including consumer electronics and industrial equipment. Canon’s commitment to research and development ensures its products remain at the forefront of imaging technology.

OmniVision Technologies Inc. has been proactive in expanding its product portfolio and forming strategic partnerships. In January 2022, the company unveiled a rebranding initiative at CES 2022, reflecting its broadened product offerings beyond traditional imaging solutions. This rebranding signifies OmniVision’s commitment to innovation and diversification in the imaging sensor market.

Top Key Players in the Market

- Panasonic Corporation

- Canon Inc.

- OmniVision Technologies Inc.

- Sony Corporation

- ON Semiconductor Corporation

- ams OSRAM AG

- GalaxyCore Shanghai Limited Corporation

- Hamamatsu Photonics K.K.

- Himax Technologies, Inc.

- PixArt Imaging Inc.

- Other Major Players

Recent Developments

- In 2024, Canon unveiled a groundbreaking 35mm full-frame CMOS sensor boasting an unprecedented resolution of 410 megapixels, marking the highest pixel count achieved for this sensor type.

- In 2024, The market also saw a notable shift towards higher-end mobile and automotive products, with the average selling price (ASP) of CMOS image sensors remaining above $3, contributing to the total market’s projected growth to $28.6 billion by 2029.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 28.47 Billion |

| Forecast Revenue (2034) | USD 62.04 Billion |

| CAGR (2025-2034) | 8.10% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Spectrum (Visible, Non-visible), By Image Processing Technology (2D, 3D), By Resolution (Up to 5 MP, 5 MP to 12 MP, 12 MP to 16 MP, Above 16 MP), By Industry Vertical (Aerospace & Defense, Automotive, Consumer Electronics, Healthcare & Lifesciences, Industrial, Security & Surveillance, Others), By Revenue Model (Subscription-Based, Ad-Supported, Pay-Per-View, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Panasonic Corporation, Canon Inc., OmniVision Technologies Inc., Sony Corporation, ON Semiconductor Corporation, ams OSRAM AG, GalaxyCore Shanghai Limited Corporation, Hamamatsu Photonics K.K., Himax Technologies, Inc., PixArt Imaging Inc., Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |