Quick Navigation

- Report Overview

- Key Takeaways

- Level of Autonomy Analysis

- Software Type Analysis

- Propulsion Type Analysis

- Vehicle Type Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Regional Analysis

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

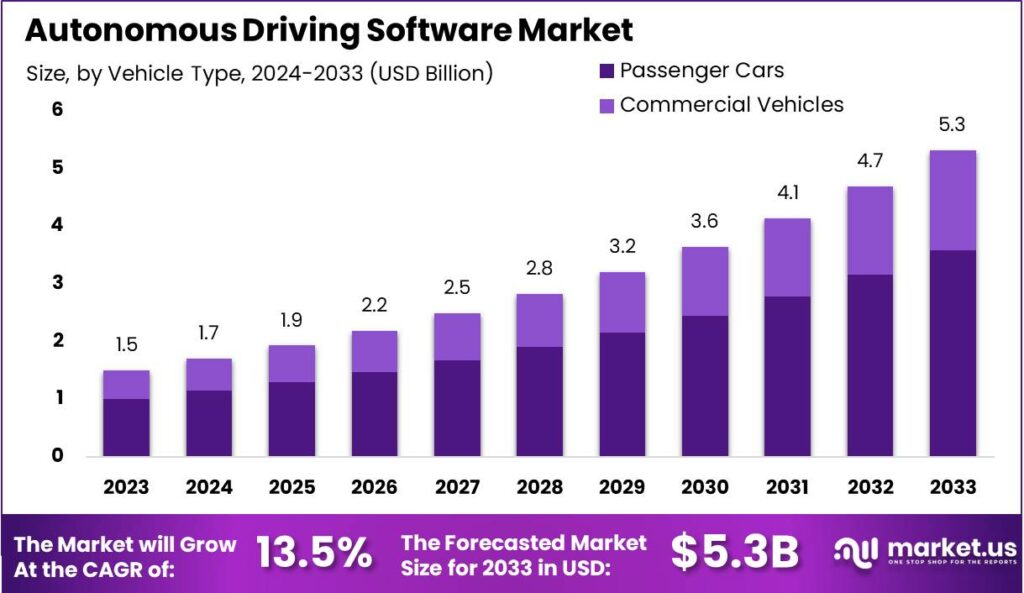

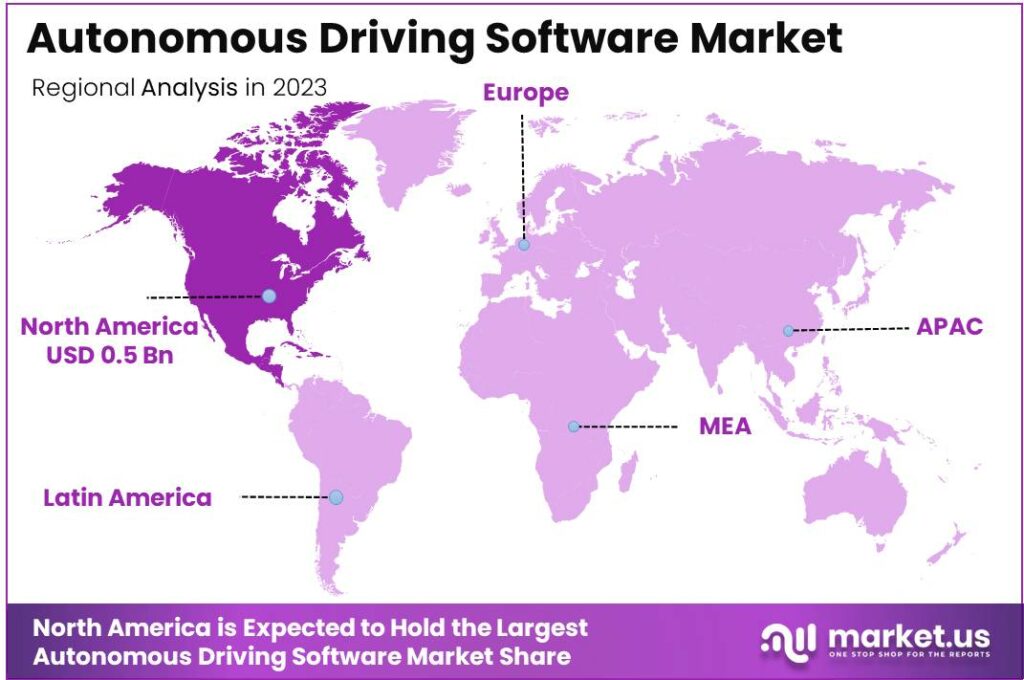

The Global Autonomous Driving Software Market size is expected to be worth around USD 5.3 Billion By 2033, from USD 1.5 Billion in 2023, growing at a CAGR of 13.50% during the forecast period from 2024 to 2033. In 2023, North America dominated the autonomous driving software market, capturing more than 36.8% share, with revenues totaling USD 0.5 billion.

Autonomous driving software is a complex system designed to enable vehicles to operate without human intervention. It integrates various technologies, including artificial intelligence (AI), machine learning, and advanced sensors like LiDAR and radar, to interpret the vehicle’s surroundings, make decisions, and control the vehicle’s movement. This software handles functions such as steering, braking, and navigating, allowing the car to perform all driving tasks.

The autonomous driving software market is experiencing significant growth, driven by advancements in artificial intelligence and the increasing adoption of autonomous vehicles across commercial and consumer sectors. This market includes a range of products from basic automated assistance software to fully autonomous driving solutions. It caters to various end-users including automotive manufacturers, technology companies, and mobility service providers.

The growth of the autonomous driving software market can be attributed to several key factors. Increasing safety concerns and a push for reduced traffic congestion are driving demand for vehicles that can autonomously handle driving tasks. Additionally, regulatory support and incentives for eco-friendly and technologically advanced vehicles are propelling the market forward.

The efficiency and potential cost savings in logistics and transportation further boost the adoption of autonomous driving technologies. Market demand for autonomous driving software is primarily fueled by the automotive sector’s shift towards electric and autonomous vehicles. Consumer demand for safer and more efficient driving options also plays a crucial role.

As urbanization continues to rise, cities are looking for innovative solutions to manage traffic flow and enhance public transportation systems, thereby increasing the demand for autonomous driving solutions. The autonomous driving software market presents numerous opportunities. One major area is the integration of autonomous driving technology with electric vehicles, which are becoming increasingly popular.

There is also potential in developing markets, where urbanization and increasing vehicle ownership are creating a need for innovative transportation solutions. Partnerships between automotive manufacturers and tech companies can accelerate technology development and market penetration.

Technological advancements are the cornerstone of the autonomous driving software market. Improvements in machine learning algorithms, sensor accuracy, and data processing speeds are making autonomous vehicles more reliable and efficient. Developments in connectivity technologies like 5G also enhance vehicle-to-vehicle and vehicle-to-infrastructure communication, essential for the real-time data exchange required for autonomous driving.

Key Takeaways

- The Autonomous Driving Software Market size is expected to reach USD 5.3 Billion by 2033, growing from USD 1.5 Billion in 2023, with a CAGR of 13.50% during the forecast period from 2024 to 2033.

- In 2023, the L2 segment held a dominant position in the market, capturing more than 60.1% share.

- In 2023, the Perception and Planning Software segment led the market, holding more than 41.5% share.

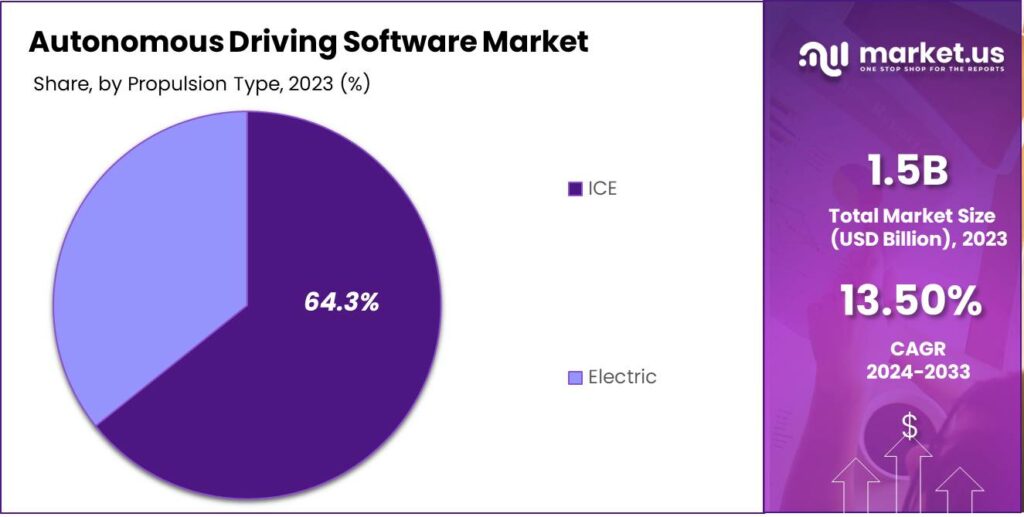

- The Internal Combustion Engine (ICE) segment also dominated the market in 2023, with more than 64.3% share.

- In 2023, the Passenger Cars segment accounted for over 67.4% share of the autonomous driving software market.

- North America was the leading region in 2023, capturing more than 36.8% share, with revenues of USD 0.5 billion.

Level of Autonomy Analysis

In 2023, the L2 segment held a dominant position in the autonomous driving software market, capturing more than a 60.1% share. This segment encompasses systems that provide advanced driver-assistance features such as lane keeping assistance, adaptive cruise control, and collision avoidance without full automation, requiring the driver to remain engaged with the driving process.

The lead of the L2 segment in the market is primarily driven by consumer preference for vehicles equipped with safety-enhancing technologies that do not completely relinquish control to the vehicle. This level of autonomy is appealing because it offers a significant improvement in safety and convenience while allowing consumers to retain a sense of control and familiarity with the vehicle’s operations.

Additionally, the regulatory landscape has favored the L2 segment as regulations for fully autonomous vehicles (L4 and L5) remain stringent and under development in many regions. The slower adaptation of laws governing higher levels of autonomy ensures that L2 technologies remain the most feasible and widely accepted form of autonomous driving in the current market.

Software Type Analysis

In 2023, the Perception and Planning Software segment held a dominant market position, capturing more than a 41.5% share of the autonomous driving software market. This segment is crucial as it involves the real-time processing and interpretation of data from various sensors, including LIDAR, radar, and cameras.

The software analyzes this data to perceive the surrounding environment and plan the vehicle’s path accordingly. The critical nature of these tasks, combined with the rapid advancements in sensor technology, has propelled the demand for this market.

Although not as predominant as perception and planning, the Supervision/Monitoring Software segment plays an essential role in the safety and reliability of autonomous vehicles. This software oversees the autonomous system’s operations, ensuring that all components function correctly and intervene when necessary.

Interior Sensing Software focuses on monitoring vehicle cabins to improve safety and comfort by detecting passengers, ensuring seat belts are fastened, and tracking driver alertness in semi-autonomous cars. Though it holds a small market share, its growth is fueled by rising demand for advanced safety and passenger-centric features.

Propulsion Type Analysis

In 2023, the Internal Combustion Engine (ICE) segment held a dominant position in the autonomous driving software market, capturing more than a 64.3% share. This substantial market share can primarily be attributed to the extensive existing infrastructure supporting ICE vehicles, including widespread service networks and fuel stations globally.

Additionally, the gradual adoption curve of electric vehicles (EVs) allows ICE vehicles to maintain a strong foothold in the market. Despite the growing environmental concerns, ICE vehicles continue to benefit from incremental improvements in engine efficiency and emissions reductions, which prolongs their viability and attractiveness to consumers.

The predominance of the ICE segment is further reinforced by the lower initial cost of ICE vehicles compared to their electric counterparts. The affordability of ICE vehicles makes them a preferred choice in emerging markets where cost sensitivity is a significant factor.

This price advantage is crucial, considering the higher upfront costs associated with electric vehicles, which include not only the vehicle itself but also the charging infrastructure and higher maintenance expenses. Moreover, the economic context of various regions continues to play a critical role in shaping consumer preferences towards more familiar and economically feasible ICE vehicles.

Vehicle Type Analysis

In 2023, the Passenger Cars segment held a dominant market position in the autonomous driving software market, capturing more than a 67.4% share. This leadership is primarily due to the higher volume of passenger vehicles equipped with advanced driver-assistance systems (ADAS) and the growing consumer demand for safer and more efficient personal transportation options.

The proliferation of autonomous features in passenger cars, including automatic braking, lane-keeping assistance, and adaptive cruise control, has significantly driven the segment’s growth. Additionally, the increasing affordability of these technologies has made them accessible to a broader range of consumers, further boosting the segment’s expansion.

The Passenger Cars segment benefits from substantial investments by major automakers and tech companies in autonomous driving technologies, aiming to enhance safety and convenience for individual drivers. These investments are supported by a robust technological infrastructure, which is more rapidly implemented in personal vehicles than in commercials.

Consumer preference for autonomy in driving is also a key factor propelling the Passenger Cars segment. As urbanization continues and traffic conditions grow more complex, the demand for vehicles that can automate driving tasks to alleviate commuter stress is increasing.

Key Market Segments

By Level of Autonomy

- L1

- L2

- L3

- L4

- L5

By Software Type

- Perception and Planning Software

- Supervision/Monitoring Software

- Interior Sensing Software

- Chauffeur Software

By Propulsion Type

- Electric

- ICE

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

Driver

Technological Advancements

The rapid development of artificial intelligence (AI), machine learning, and sensor technologies has significantly propelled the autonomous driving software market. These innovations enable vehicles to interpret complex environments, make informed decisions, and enhance safety.

Machine learning allows systems to improve decision-making over time by learning from real-world driving data. Additionally, advancements in sensor technology provide precise environmental mapping, crucial for autonomous navigation. These technological strides have made autonomous driving software more reliable and efficient, fostering increased adoption in the automotive industry.

Restraint

High Development Costs

Developing autonomous driving software involves substantial financial investment, posing a significant restraint to market growth. The integration of advanced sensors, high-performance computing systems, and sophisticated algorithms requires considerable capital.

Moreover, extensive testing and validation processes are necessary to ensure safety and compliance with regulatory standards, further escalating costs. These financial barriers can deter smaller companies from entering the market and may slow the pace of innovation. Additionally, the high costs are often passed on to consumers, potentially limiting widespread adoption of autonomous vehicles.

Opportunity

Government Initiatives and Funding

Government initiatives and funding present a significant opportunity for the autonomous driving software market. Many governments are investing in research and development of autonomous technologies to enhance transportation efficiency and safety.

Additionally, subsidies and grants for companies working on autonomous driving solutions can lower financial barriers, encouraging innovation and collaboration within the industry. Such governmental support can facilitate the integration of autonomous vehicles into public transportation systems, further expanding market opportunities.

Challenge

Regulatory and Safety Concerns

Regulatory and safety concerns pose significant challenges to the autonomous driving software market. The lack of standardized regulations across different regions creates uncertainty for manufacturers and developers.

Ensuring software robustness and reliability in diverse and unpredictable road conditions is critical to gaining public trust. Additionally, addressing potential cybersecurity threats is essential to prevent unauthorized access and ensure passenger safety. Navigating these regulatory landscapes and meeting stringent safety standards require continuous collaboration between industry stakeholders and policymakers.

Emerging Trends

Autonomous driving software is rapidly evolving, with several key trends shaping its future. One significant development is the integration of artificial intelligence (AI) and machine learning, enabling vehicles to interpret complex environments and make real-time decisions. This advancement enhances safety and efficiency on the roads.

Another trend is the shift towards software-defined vehicles, where the majority of vehicle functions are controlled by software rather than hardware. This approach allows for continuous updates and improvements, ensuring vehicles remain up-to-date with the latest features and safety protocols.

Connectivity is also playing a crucial role, with vehicles increasingly linked to the Internet of Things (IoT). This connectivity facilitates communication between vehicles and infrastructure, leading to smarter traffic management and improved navigation systems.

The development of advanced driver-assistance systems (ADAS) is bridging the gap between traditional vehicles and fully autonomous ones. ADAS features, such as adaptive cruise control and lane-keeping assistance, are becoming more sophisticated, providing drivers with enhanced support and gradually introducing autonomous functionalities.

Business Benefits

- Enhanced Safety: Self-driving vehicles can reduce accidents by minimizing human errors. For instance, Waymo’s autonomous cars have shown a 92% decrease in injury claims compared to human-driven vehicles.

- Cost Savings: By eliminating the need for human drivers, companies can save on labor costs. Additionally, autonomous trucks have demonstrated fuel savings of 10% to 20%, leading to lower operational expenses.

- Increased Efficiency: Autonomous vehicles can operate continuously without breaks, enhancing productivity. This is particularly beneficial in logistics, where timely deliveries are crucial.

- New Business Models: The rise of autonomous vehicles paves the way for services like robotaxis, offering convenient and cost-effective transportation options. Companies like Tesla are developing affordable robotaxis to compete in this emerging market.

- Improved Traffic Management: Widespread use of autonomous vehicles can lead to smoother traffic flow and reduced congestion, enhancing overall transportation efficiency.

Regional Analysis

In 2023, North America held a dominant market position in the autonomous driving software market, capturing more than a 36.8% share, with revenues amounting to USD 0.5 billion.

This leadership is primarily due to the advanced technological infrastructure and the presence of key industry players in the region. North America has been at the forefront of developing and implementing autonomous driving technologies, driven by significant investments from both private and public sectors in research and development.

The region’s market dominance is further bolstered by favorable regulatory frameworks that encourage the testing and deployment of autonomous vehicles. U.S. states like California, Arizona, and Nevada are pioneers, offering regulatory sandboxes for testing autonomous vehicle technologies. This supportive regulatory environment has facilitated rapid advancements and adoption within the market.

Moreover, the high consumer acceptance of autonomous technologies in North America contributes significantly to its leading position. The population’s readiness to adopt new technologies, combined with a robust economic landscape, makes North America a lucrative market for autonomous driving software. The demand for autonomous driving capabilities is further driven by the widespread recognition of their potential to enhance road safety and reduce traffic congestion.

Additionally, the strategic collaborations between automotive manufacturers and technology giants in Silicon Valley and beyond have accelerated the development and sophistication of autonomous driving systems. These partnerships leverage cutting-edge artificial intelligence and machine learning technologies, enhancing the capabilities and reliability of autonomous driving software, thus promoting greater market penetration in North America compared to other regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In the rapidly evolving autonomous driving software market, Alphabet Inc., through its subsidiary Waymo, is a leader in self-driving technology. Waymo’s advanced AI and extensive real-world testing set industry standards. With strong financial backing and strategic partnerships, Alphabet is effectively scaling its autonomous driving solutions across public transportation and logistics.

NVIDIA Corporation is another key player in the autonomous driving software arena. Renowned for its powerful GPUs, NVIDIA has seamlessly transitioned its high-performance computing capabilities to support complex autonomous driving algorithms. The company’s DRIVE platform is integral to developing AI-enabled vehicles, providing the computational power necessary for real-time, onboard decision-making processes in autonomous vehicles.

Aurora Innovation Inc. is a noteworthy entity focused on developing self-driving technology aimed at commercializing autonomous freight and passenger transit. Aurora’s approach integrates unique hardware, software, and data services to deliver a dependable and scalable autonomous driving system.

Top Key Players in the Market

- Alphabet Inc.

- NVIDIA Corporation

- Aurora Innovation Inc.

- Mobileye

- Aptiv

- Nuro, Inc.

- Wayve Technologies Ltd.

- Phantom AI

- PlusAI, Inc.

- Other Key Players

Top Opportunities Awaiting for Players

The autonomous driving software market presents several promising opportunities for industry players in the coming years.

- Expansion into Emerging Markets: As the autonomous driving market matures in developed regions, emerging markets offer new growth avenues. Countries in the Asia Pacific region, such as China and India, are rapidly developing their automotive industries and infrastructure, which creates significant opportunities for deploying autonomous driving technologies.

- Integration with Electric and Hybrid Vehicles: The shift towards electric vehicles (EVs) and hybrids offers a dual opportunity for autonomous software developers. These vehicles often come with advanced electronic architectures that are more adaptable to the integration of autonomous software, enhancing both vehicle efficiency and software capabilities.

- Advancements in Vehicle Connectivity and 5G: The rollout of 5G networks enhances vehicle-to-everything (V2X) connectivity, enabling more reliable and faster communication between vehicles and infrastructure. This technological advancement supports more sophisticated and safer autonomous driving functions.

- Software Subscription Models: There is a growing trend towards software as a service (SaaS) in the automotive sector. Autonomous driving software providers can explore recurring revenue models through subscriptions for software updates, enhanced features, and real-time data services, which can improve the functionality and safety of autonomous systems over time.

- Partnerships with Technology and Automotive Companies: Collaborations between software developers and automotive manufacturers are crucial for the advancement of autonomous driving technologies. Technological innovation from tech companies and manufacturing scale and expertise from automotive firms. These collaborations are essential for developing more advanced and integrated autonomous driving solutions.

Recent Developments

- Uber and Wayve Partnership (August 2024): Uber Technologies, Inc. teamed up with Wayve to harness its AI for self-driving. With Uber’s financial backing, Wayve is set to accelerate partnerships with global automotive manufacturers. Their focus includes upgrading consumer vehicles with Level 2 advanced driver assistance systems (ADAS) and Level 3 automation. Looking ahead, Wayve aims to develop Level 4 fully autonomous vehicles for Uber’s platform.

- PlusAI’s Launch of PlusProtect (May 2024): PlusAI introduced PlusProtect, a cutting-edge AI safety technology designed for global automotive suppliers and manufacturers. This system enhances safety by improving crash avoidance and advanced emergency braking (AEB). Its scalable design meets or exceeds new regulatory safety standards, making it ideal for passenger vehicles, trucks, and other vehicle types.

- Horizon Robotics Unveils Horizon SuperDrive (April 2024): Horizon Robotics launched the Horizon SuperDrive, a full-stack autonomous driving solution combining advanced software and hardware. This system is built for urban, highway, and parking scenarios, emphasizing safety and reliability. With its unique co-optimized design, Horizon Robotics is positioned as a leader in comprehensive ADAS solutions.

- IVECO’s Semi-Automated Truck Pilot in Germany (July 2024): IVECO, in collaboration with PlusAI, dm-drogerie markt, and DSV, announced a semi-automated truck pilot program in Germany. The IVECO S-Way heavy-duty truck features PlusAI’s PlusDrive® software, enabling highly automated and driver-supervised capabilities. Following months of testing, this pilot highlights progress in heavy-duty vehicle automation.

- Rivian and Volkswagen Joint Venture (June 2024): Rivian and Volkswagen Group revealed a joint venture to create advanced vehicle software technology. Volkswagen committed an initial investment of $1 billion, with plans to increase funding to $4 billion. This partnership signals a strong move toward collaboration in developing next-generation vehicle tech

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.5 Bn |

| Forecast Revenue (2033) | USD 5.3 Bn |

| CAGR (2024-2033) | 13.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Level of Autonomy (L1, L2, L3, L4, L5), By Software Type (Perception and Planning Software, Supervision/Monitoring Software, Interior Sensing Software, Chauffeur Software), By Propulsion Type (Electric, ICE), By Vehicle Type (Passenger Cars, Commercial Vehicles) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alphabet Inc., NVIDIA Corporation, Aurora Innovation Inc., Mobileye, Aptiv, Nuro, Inc., Wayve Technologies Ltd., Phantom AI, PlusAI, Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |