Quick Navigation

Report Overview

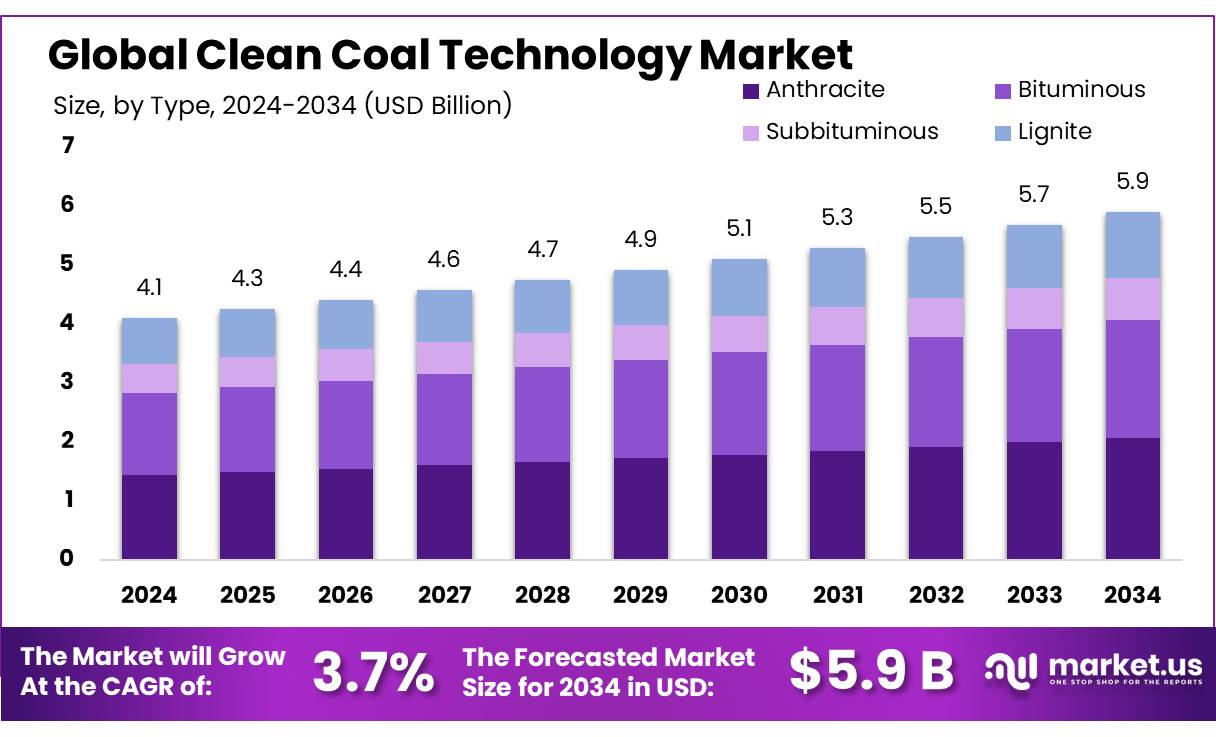

The Global Clean Coal Technology Market size is expected to be worth around USD 5.9 Bn by 2034, from USD 4.1 Bn in 2024, growing at a CAGR of 3.7% during the forecast period from 2025 to 2034.

Clean Coal Technology (CCT) refers to a range of technologies aimed at reducing the environmental impact of coal-based power generation, focusing on minimizing emissions of pollutants such as sulfur dioxide (SO₂), nitrogen oxides (NOₓ), and particulate matter, as well as carbon dioxide (CO₂).

These technologies enhance the efficiency of coal plants while reducing their environmental footprint. Clean coal encompasses various approaches, including carbon capture and storage (CCS), integrated gasification combined cycle (IGCC), and fluidized bed combustion (FBC).

In 2020, coal-fired power plants accounted for nearly 38% of the global electricity generation, and in many developing economies, coal continues to be an affordable energy source. The transition to cleaner energy systems, however, requires the integration of clean coal technologies to reduce the harmful environmental impacts.

Governments globally have taken measures to promote clean coal technologies. In the U.S., the Department of Energy (DOE) has allocated funding to projects focusing on carbon capture and storage (CCS), with significant investments in the development of technologies like Direct Air Capture (DAC).

Similarly, China, as the world’s largest coal producer and consumer, has launched multiple initiatives under its “Clean Coal Technology Development Plan” to reduce air pollution and carbon emissions. Additionally, in Europe, the EU’s Horizon 2020 research program has funded multiple clean coal projects aimed at improving the environmental performance of coal plants.

Key Takeaways

- Clean Coal Technology Market size is expected to be worth around USD 5.9 Bn by 2034, from USD 4.1 Bn in 2024, growing at a CAGR of 3.7%.

- Bituminous coal held a dominant market position in the clean coal technology sector, capturing more than a 34.5% share.

- Carbon Capture, Utilization, and Storage (CCUS) held a dominant market position in the clean coal technology sector, capturing more than a 27.1% share.

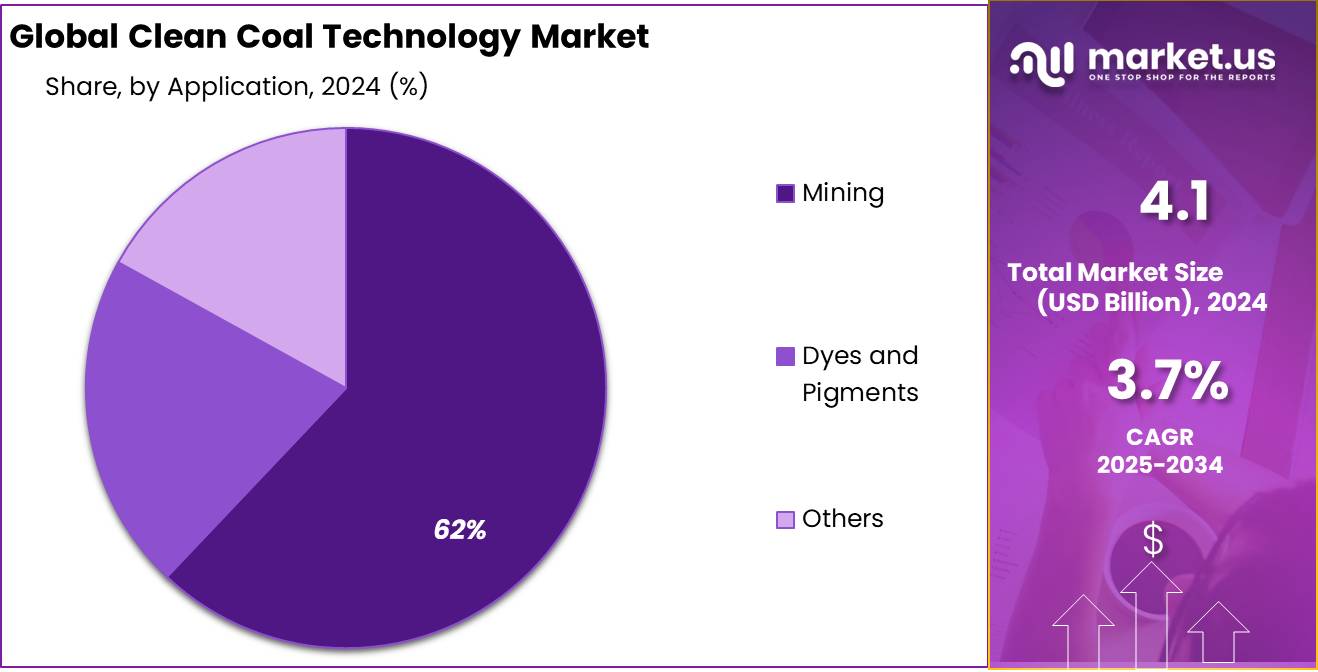

- Mining sector held a dominant market position in the clean coal technology market, capturing more than a 62.2% share.

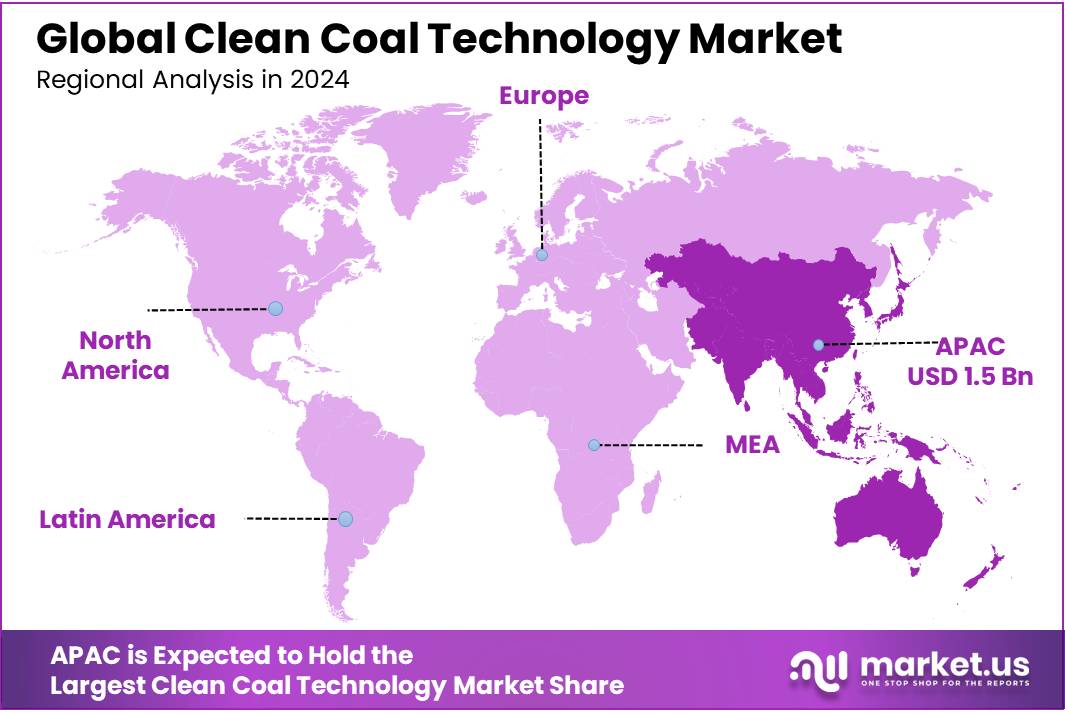

- Asia-Pacific (APAC) region is a key player globally, contributing significantly to the sector’s growth. With a market share of approximately 38.4%, valued at USD 1.5 billion.

By Type

In 2024, bituminous coal held a dominant market position in the clean coal technology sector, capturing more than a 34.5% share. This significant market presence was driven by its widespread availability and cost-effectiveness compared to other coal types. Bituminous coal’s high energy content and compatibility with advanced clean coal technologies, such as carbon capture and storage (CCS) and supercritical and ultra-supercritical power generation, further solidified its position.

This growth is fueled by ongoing investments in upgrading existing coal-fired power plants to meet stricter environmental regulations. Additionally, the development of integrated gasification combined cycle (IGCC) technology, which efficiently utilizes bituminous coal, is anticipated to drive further adoption. However, the market may face challenges from increasing competition from renewable energy sources and stricter carbon emission policies in certain regions. Despite these hurdles, bituminous coal is likely to remain a key player in the clean coal technology market due to its reliability and adaptability to emerging clean energy solutions.

By Technology

In 2024, Carbon Capture, Utilization, and Storage (CCUS) held a dominant market position in the clean coal technology sector, capturing more than a 27.1% share. This technology emerged as a critical solution for reducing carbon emissions from coal-based power plants and industrial processes. Governments and private sectors worldwide invested heavily in CCUS to meet climate goals and comply with stricter environmental regulations. The technology’s ability to capture up to 90% of CO2 emissions from coal combustion made it a preferred choice for industries aiming to balance energy demands with sustainability.

This growth will be fueled by advancements in capture technologies and the increasing commercialization of CO2 utilization in industries such as enhanced oil recovery (EOR) and manufacturing. Additionally, the development of large-scale CCUS projects, particularly in Asia-Pacific, is anticipated to boost market expansion. However, high initial costs and infrastructure challenges may slow down adoption in some regions. Despite these hurdles, CCUS is projected to remain a cornerstone of clean coal technology, playing a vital role in the global transition toward low-carbon energy systems.

By Application

In 2024, the mining sector held a dominant market position in the clean coal technology market, capturing more than a 62.2% share. This significant share was driven by the extensive use of coal in mining operations, particularly in regions with large coal reserves like Asia-Pacific and North America. Clean coal technologies, such as advanced filtration systems and low-emission combustion techniques, were increasingly adopted by mining companies to reduce their environmental footprint and comply with stringent regulations.

This growth will be supported by ongoing investments in modernizing mining infrastructure and the rising demand for cleaner energy sources in mining operations. Additionally, the development of technologies like carbon capture and storage (CCUS) tailored for mining applications is expected to further drive adoption. However, challenges such as high implementation costs and the gradual shift toward renewable energy in some regions may pose constraints. Despite these factors, the mining sector is likely to remain a key driver of the clean coal technology market, given its reliance on coal and the increasing emphasis on sustainable practices.

Key Market Segments

By Type

- Anthracite

- Bituminous

- Subbituminous

- Lignite

By Technology

- Carbon Capture, Utilization, and Storage (CCUS)

- Washing

- Flue Gas Desulfurization

- Low NOX Burners

- Pressurized Fluidized Bed Combustion (PFBC)

- Integrated Gasification Combined Cycle (IGCC)

- Supercritical and Ultra Supercritical Pulverized Coal

- Others

By Application

- Mining

- Dyes and Pigments

- Others

Drivers

Government Initiatives & Policy Support for Clean Coal Technology

One of the major driving factors for the adoption and development of clean coal technology (CCT) is the increased support and initiatives from governments across the globe. Governments are recognizing the importance of reducing carbon emissions while continuing to rely on coal as an energy source. Clean coal technologies help mitigate the environmental impact of coal by capturing carbon dioxide (CO2) emissions, making coal energy generation cleaner and more sustainable.

A clear example of governmental support comes from the U.S. government’s investment in clean coal research and development. For instance, in 2020, the U.S. Department of Energy (DOE) allocated over $150 million in funding for clean coal technology projects. These funds are directed towards advancing technologies like carbon capture and storage (CCS), which can capture up to 90% of CO2 emissions from coal plants. Additionally, the DOE’s Coal FIRST initiative, launched in 2020, focuses on designing the next generation of advanced coal plants with zero emissions.

Similarly, China, the world’s largest coal producer, is heavily investing in clean coal technology as part of its strategy to reduce carbon emissions. The Chinese government plans to achieve carbon neutrality by 2060 and has included CCS as one of the key technologies to meet this target. By 2021, China had already launched more than 20 CCS projects, demonstrating significant government backing.

These governmental efforts reflect a global commitment to reducing coal-related emissions while maintaining energy security. The financial incentives and policy frameworks put in place by various countries highlight the urgent need for innovation in the coal sector to meet climate goals while continuing to generate reliable energy.

Restraints

High Implementation Costs of Clean Coal Technology

One of the significant challenges facing the widespread adoption of clean coal technology is the high upfront cost of implementation. Despite its potential environmental benefits, the financial burden associated with developing and installing clean coal technologies such as carbon capture and storage (CCS) remains a key restraining factor. The cost of setting up CCS systems can range between $1 billion to $2 billion per coal-fired plant, depending on the scale and technology used.

For instance, the Petra Nova carbon capture project in Texas, one of the largest CCS projects in the U.S., cost approximately $1 billion to implement. However, the plant struggled to achieve profitability due to the high operational costs, further demonstrating the financial challenge clean coal faces. According to a 2021 report from the International Energy Agency (IEA), the cost of capturing CO2 is typically between $40 to $120 per tonne, which can add significant operating expenses for energy producers.

This financial challenge is compounded by the fact that many coal plants are already operating on tight margins and may find it difficult to justify the high costs of retrofitting with clean coal technologies. Even with government subsidies and incentives, which can help offset some costs, many energy companies are hesitant to invest in these technologies without clear, long-term financial returns.

Additionally, the food and agricultural industries, which are significant consumers of energy, face rising costs of energy production, including from coal. With global food prices increasing, driven partly by rising energy prices, many food industry leaders have pointed out that implementing clean coal technology might drive up operational costs even further. These concerns add to the hesitance of sectors relying on affordable energy.

Opportunity

Expanding Carbon Capture and Storage (CCS) Capacity

One of the most promising growth opportunities for clean coal technology lies in the expansion of Carbon Capture and Storage (CCS) capacity. CCS is a vital component of clean coal technology, enabling power plants to capture carbon dioxide (CO2) emissions before they reach the atmosphere. As the world increasingly focuses on reducing greenhouse gas emissions to meet climate targets, the need for scalable and cost-effective CCS solutions continues to grow.

The global CCS market is expected to experience significant growth in the coming years. According to the International Energy Agency (IEA), to achieve net-zero emissions by 2050, the world will need to capture and store around 7.6 billion tonnes of CO2 annually by mid-century. As of 2021, CCS capacity worldwide stood at roughly 40 million tonnes annually, highlighting a major gap in the technology’s current capabilities. The potential for growth here is enormous, as governments, especially in carbon-heavy regions, are actively seeking ways to expand CCS infrastructure to meet climate goals.

Government initiatives, like the U.S. Department of Energy’s (DOE) “Carbon Management Initiative,” provide a strong boost to the growth of CCS projects. In 2021, the DOE allocated $3.5 billion to support the development of large-scale CCS projects. This funding is expected to accelerate the construction of CCS facilities in industrial sectors that are difficult to decarbonize, such as cement, steel, and power generation.

Trends

Integration of Clean Coal with Renewable Energy Systems

One of the most exciting recent trends in clean coal technology is the integration of coal power plants with renewable energy systems, such as solar and wind power. This hybrid approach aims to reduce coal’s environmental impact while maintaining the reliability and stability of the energy grid. By combining the steady, dispatchable power from coal plants with the variable but clean power from renewables, this trend is gaining traction as a potential solution for achieving a balanced, low-carbon energy mix.

In recent years, several countries have started exploring the potential of this hybrid model. For instance, in 2022, China launched a pilot project that integrates coal-fired power with solar energy. The goal of this project is to enhance the efficiency of coal plants by using renewable energy to offset peak coal usage, thus reducing CO2 emissions without compromising energy output. According to China’s National Energy Administration, this approach could lower coal consumption by up to 10% in some regions, significantly reducing emissions without sacrificing grid reliability.

The United States is also showing interest in this hybrid model. In 2021, the U.S. Department of Energy (DOE) announced an initiative to research and develop systems that combine clean coal with renewables. The DOE has set aside $40 million in funding to explore technologies that allow for seamless integration between coal plants and renewable sources. This trend represents a promising pathway for coal to remain a key energy source in a low-carbon future, while contributing to the global shift toward sustainable energy.

Regional Analysis

The Clean Coal Technology (CCT) market in the Asia-Pacific (APAC) region is a key player globally, contributing significantly to the sector’s growth. With a market share of approximately 38.4%, valued at USD 1.5 billion, APAC is the largest and most dominant region in the Clean Coal Technology industry. The region’s large-scale coal consumption, industrialization, and urbanization drive the demand for more efficient and environmentally friendly coal technologies.

Countries like China and India lead the market, accounting for the largest shares due to their heavy reliance on coal for energy production, coupled with ambitious government initiatives to reduce carbon emissions. For instance, China, the largest coal consumer in the world, is investing heavily in clean coal technologies such as Integrated Gasification Combined Cycle (IGCC) and carbon capture and storage (CCS) solutions.

Additionally, India’s increasing energy demand has prompted government policies that support the development and adoption of clean coal technologies to minimize the environmental impact of coal-based power generation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ALSTOM Holdings, a global leader in energy and transportation infrastructure, is a prominent player in the clean coal technology market. The company specializes in providing energy-efficient and environmentally friendly solutions, including advanced technologies for coal-fired power generation. ALSTOM has been at the forefront of developing and deploying carbon capture and storage (CCS) technologies. Their innovative solutions help reduce emissions from coal plants, contributing to cleaner energy generation.

A subsidiary of ALSTOM, Alstom Power focuses on providing sustainable energy solutions for the global market, including clean coal technologies. Alstom Power has been instrumental in the development of efficient coal-fired power plants that incorporate CCS technologies to minimize carbon emissions. Their expertise in plant engineering, coupled with a focus on emission reduction technologies, positions them as a key player in the clean coal market.

Babcock and Wilcox Enterprises Inc. (B&W) is another major player in the clean coal technology space, specializing in providing energy solutions for the power generation industry. The company offers advanced clean coal technologies, including combustion systems that reduce harmful emissions, and systems for capturing and storing carbon dioxide. B&W’s Clean Coal technology portfolio includes solutions for both existing coal plants and new projects, allowing utilities to reduce emissions and improve plant efficiency.

Top Key Players

- ALSTOM Holdings

- Alstom Power

- Babcock and Wilcox Enterprises Inc.

- Bharat Heavy Electricals Ltd.

- BHEL

- Clean Coal Technologies Inc.

- Dakota Gasification Company

- Dong Fang Electric

- Duke Energy Corporation

- Dynegy Energy Services LLC

- Environmental Energy Services Corporation

- General Electric Company

- Harbin Electric Company Limited

- KBR, Inc.

- Mitsubishi Heavy Industries Ltd.

- Shanghai Electric Group Co. Ltd.

- Shell PLC

- Siemens Energy AG

- Toshiba

- Wood PLC

Recent Developments

In 2024, ALSTOM and GE partnered to bring advanced emissions reduction technologies to new markets, setting ambitious goals for future clean coal projects.

In 2024, GE’s energy division, including Alstom Power’s contributions, generated over $11 billion in revenue, with a portion directed towards research and development of cleaner coal technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.1 Bn |

| Forecast Revenue (2034) | USD 5.9 Bn |

| CAGR (2025-2034) | 3.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Anthracite, Bituminous, Subbituminous, Lignite), By Technology (Carbon Capture, Utilization, and Storage (CCUS), Washing, Flue Gas Desulfurization, Low NOX Burners, Pressurized Fluidized Bed Combustion (PFBC), Integrated Gasification Combined Cycle (IGCC), Supercritical and Ultra Supercritical Pulverized Coal, Others, By Application (Mining, Dyes and Pigments, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ALSTOM Holdings, Alstom Power, Babcock and Wilcox Enterprises Inc., Bharat Heavy Electricals Ltd., BHEL, Clean Coal Technologies Inc., Dakota Gasification Company, Dong Fang Electric, Duke Energy Corporation, Dynegy Energy Services LLC, Environmental Energy Services Corporation, General Electric Company, Harbin Electric Company Limited, KBR, Inc., Mitsubishi Heavy Industries Ltd., Shanghai Electric Group Co. Ltd., Shell PLC, Siemens Energy AG, Toshiba, Wood PLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |