Quick Navigation

Report Overview

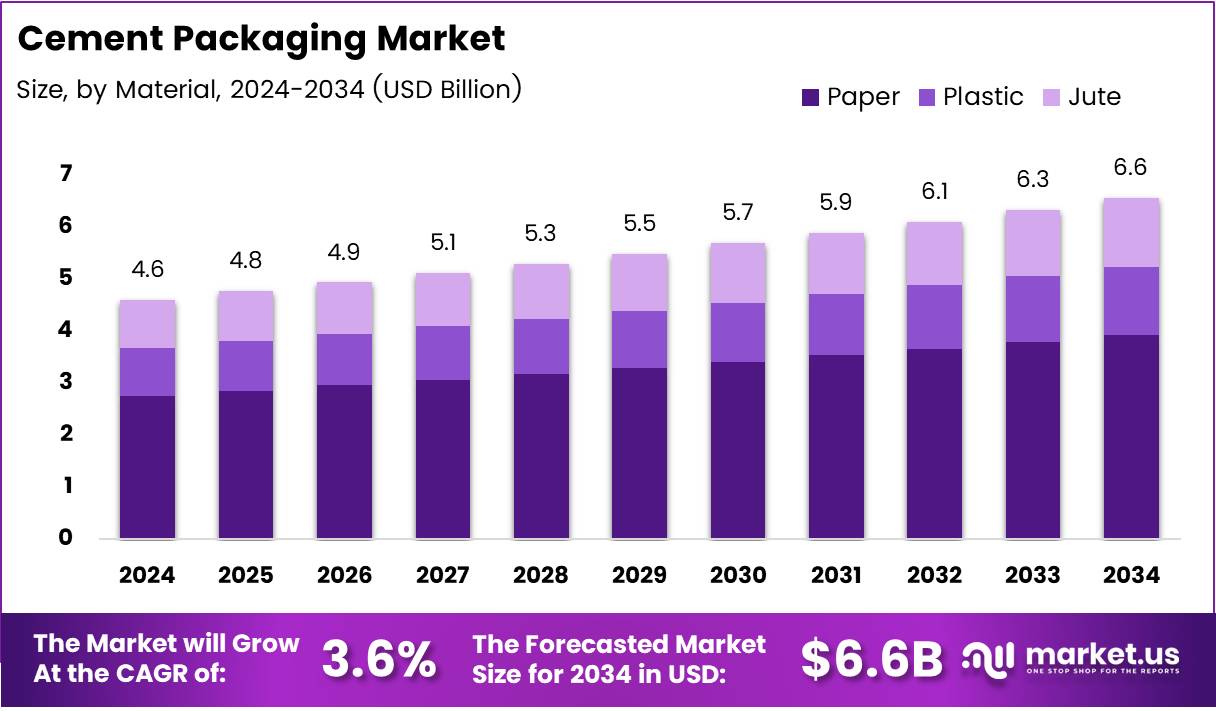

The Global Cement Packaging Market size is expected to be worth around USD 6.6 Billion by 2034, from USD 4.6 Billion in 2024, growing at a CAGR of 3.6% during the forecast period from 2025 to 2034. This growth is primarily driven by rising construction activities and increasing demand for sustainable and efficient packaging solutions worldwide.

Key Takeaways

- The global cement packaging market is projected to reach USD 6.6 Billion by 2034, growing from USD 4.6 Billion in 2024.

- The market is expected to grow at a CAGR of 3.6% from 2025 to 2034.

- In 2024, paper held a dominant 59.4% share in the By Material segment due to its sustainability and cost-effectiveness.

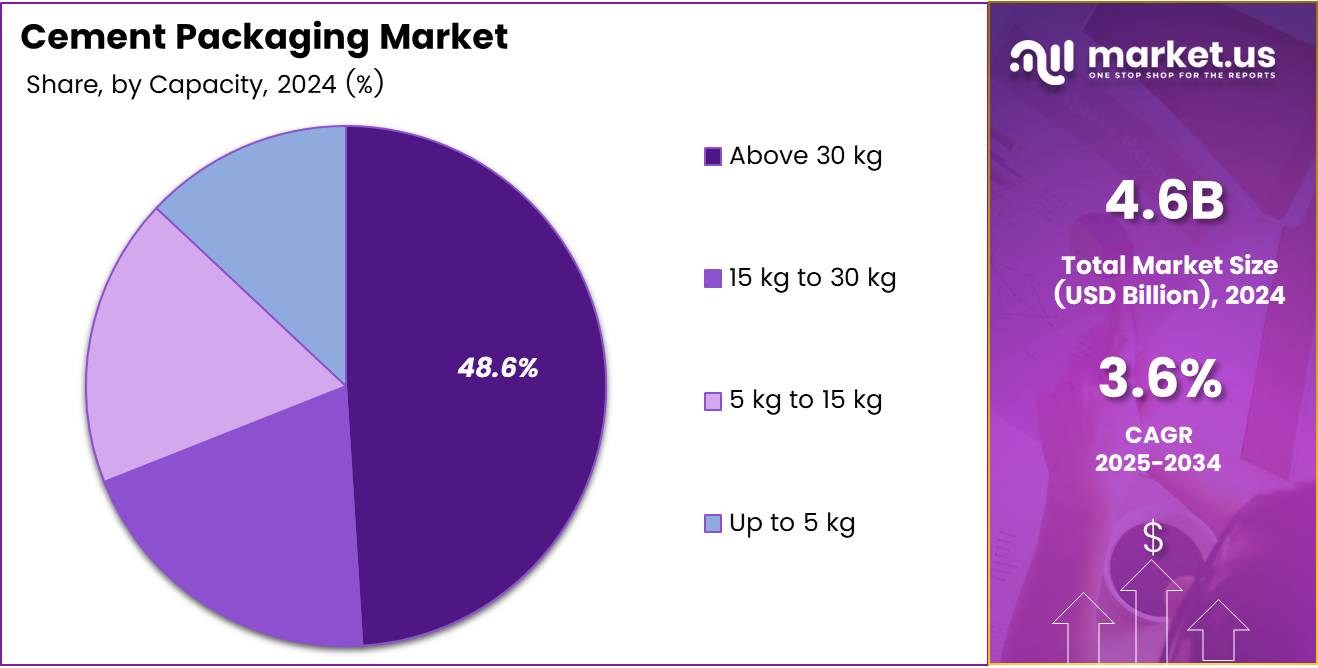

- Bags with capacity above 30 kg led the By Capacity segment in 2024, accounting for 48.6% of the market.

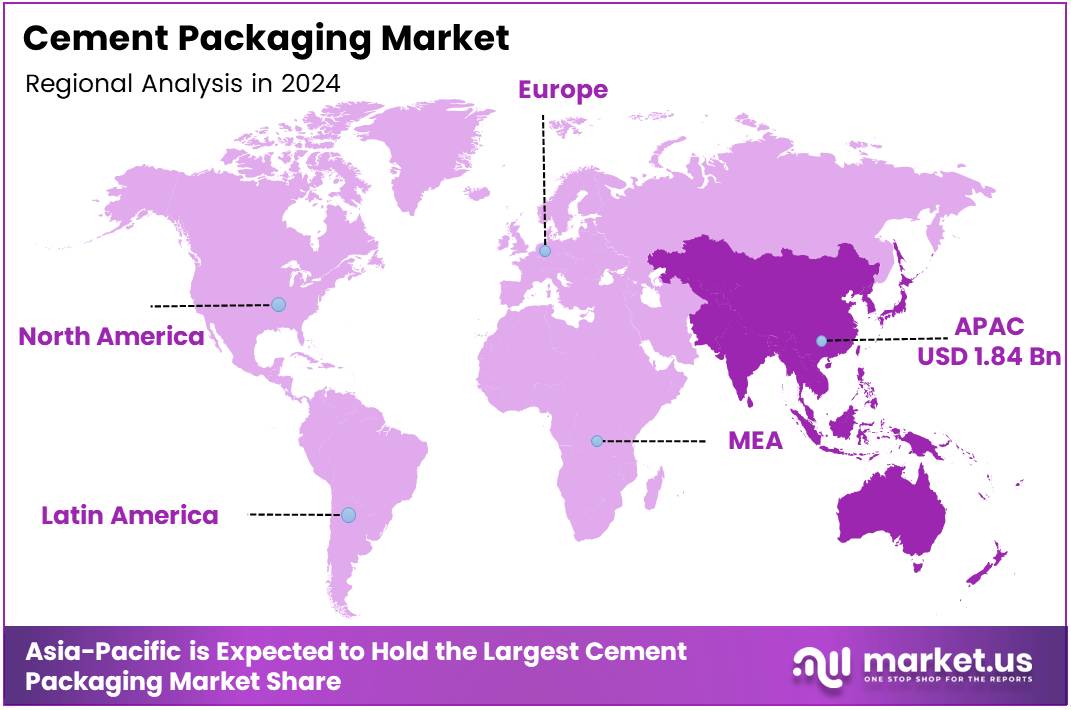

- Asia Pacific is the largest regional market, holding a 40.2% share and valued at around USD 1.84 Billion in 2024.

- Growth in Asia Pacific is driven by rapid industrialization and increasing construction activities in emerging economies.

The Cement Packaging Market refers to the specialized segment of the packaging industry focused on providing durable, efficient, and sustainable packaging solutions for cement products. This market plays a critical role in ensuring the safe transport, storage, and handling of cement, which is a vital construction material globally.

Growth in the cement packaging market is largely driven by the expanding construction and infrastructure sectors worldwide. As urbanization accelerates, the demand for packaged cement in various forms—such as bags, sacks, and bulk containers—is witnessing a steady rise, facilitating easier distribution and end-user convenience.

Opportunities abound within the market due to increasing government investments in infrastructure development and housing projects. These investments not only boost cement production but also raise the demand for innovative packaging that minimizes wastage and improves shelf life, thereby enhancing supply chain efficiency.

Furthermore, stringent government regulations aimed at environmental sustainability and safety standards are shaping the cement packaging market. Policies encouraging the use of recyclable and biodegradable materials compel manufacturers to innovate, promoting eco-friendly packaging solutions within the industry.

According to industry statistics, producing 1 ton of Portland cement requires grinding at least 3 tons of raw material, consuming more than 60% of the total power in cement plants. This highlights the energy-intensive nature of cement manufacturing, indirectly influencing packaging choices that support efficient logistics and handling.

According to World Population Review, China remains the dominant cement producer, generating approximately 2,100,000 metric tons in 2023. This production volume significantly impacts the global cement packaging market, as China’s demand for high-quality packaging materials sets standards followed internationally.

Moreover, global trade of cement reached a value of US$15.6 billion in 2023, as reported by OEC Overview. This substantial trade volume underscores the need for robust, reliable packaging to safeguard cement during long-distance transportation across diverse regions.

Material Analysis

Paper leads the cement packaging market with a 59.4% share in 2024, reflecting its strong preference among manufacturers and consumers.

In 2024, paper dominated the By Material Analysis segment of the cement packaging market, holding a commanding 59.4% share. This dominance can be attributed to paper’s sustainable nature, ease of recycling, and cost efficiency. Its eco-friendly appeal aligns well with increasing regulatory emphasis on sustainable packaging solutions.

Plastic, although less favored than paper, remains a significant material choice due to its durability and moisture resistance. It offers advantages in protection during transportation and storage but faces challenges from environmental regulations and rising demand for biodegradable alternatives.

Jute holds a smaller portion of the market but is gaining attention for its natural fiber properties and biodegradability. It appeals to niche markets focused on eco-conscious packaging and is valued for its strength and renewable attributes. However, its limited use compared to paper and plastic keeps its market share relatively modest.

Overall, the material preferences reflect a balance between sustainability, functionality, and cost-effectiveness, with paper leading due to its well-rounded benefits and regulatory support.

Capacity Analysis

Above 30 kg bags dominate the cement packaging market with a 48.6% share in 2024, favored for bulk transportation and construction needs.

In 2024, the By Capacity Analysis segment of the cement packaging market was led by bags above 30 kg, accounting for 48.6% of the market. This preference stems from the efficiency of transporting larger quantities in fewer units, reducing handling costs and logistics complexity.

The 15 kg to 30 kg capacity range also holds a significant portion of the market, appealing to smaller construction projects and regional suppliers who require manageable packaging sizes for ease of use and storage.

Smaller capacities, such as 5 kg to 15 kg and up to 5 kg, cater to specific segments like retail consumers or minor construction tasks. These smaller sizes are less common but important for customer convenience and specialized applications.

The market segmentation by capacity clearly indicates that larger bags remain the preferred choice for commercial construction and industrial use, while smaller capacities serve niche markets needing flexible packaging solutions.

Key Market Segments

By Material

- Paper

- Plastic

- Jute

By Capacity

- Above 30 kg

- 15 kg to 30 kg

- 5 kg to 15 kg

- Up to 5 kg

Drivers

Rising Adoption of Sustainable and Automated Packaging Solutions Drives Cement Packaging Market Growth

The demand for sustainable and eco-friendly cement packaging solutions is gaining significant momentum. Consumers and companies alike are focusing on reducing environmental impact, which is fueling the preference for recyclable and biodegradable materials in cement packaging. This trend aligns with global efforts to promote sustainability and reduce waste.

Simultaneously, the construction sector is expanding rapidly, especially in emerging economies. Growing urbanization and infrastructure development create a strong need for reliable cement packaging that ensures product safety during transit and storage. This growth in construction activities directly boosts the demand for efficient packaging solutions.

Moreover, automation is transforming the cement packaging industry. The rising adoption of automated packaging technologies improves operational efficiency and consistency while reducing labor costs. Automation also enables better handling of packaging materials, reducing damage and waste.

Lastly, governments worldwide are enforcing stringent regulations on packaging waste management and recyclability. Such regulatory frameworks compel manufacturers to innovate and adopt eco-friendly packaging options that comply with legal standards. This regulatory pressure acts as a key driver for market growth and technological advancement in cement packaging.

Restraints

High Costs and Lack of Standardization Challenge Cement Packaging Market Expansion

One of the major restraints in the cement packaging market is the high cost of advanced packaging materials. While eco-friendly and technologically advanced options are preferred, their affordability remains a challenge for many manufacturers, especially in cost-sensitive regions.

Fluctuations in raw material prices also affect the overall production costs of packaging materials. Volatile prices for paper, plastic, and other inputs make it difficult for companies to maintain stable pricing, which can impact profit margins.

Additionally, the lack of standardization in packaging sizes and formats across different regions causes inefficiencies. This inconsistency complicates logistics, storage, and compatibility with automated machinery, hindering smooth operations.

Maintaining package integrity during long-distance transportation is another concern. Cement bags are prone to damage from moisture, tearing, and rough handling, which can lead to product loss and customer dissatisfaction. These factors collectively restrain the growth and widespread adoption of advanced packaging solutions in the cement industry.

Growth Factors

Biodegradable Materials and Smart Technologies Open New Doors in Cement Packaging Market

The development of biodegradable and compostable packaging materials presents a promising growth opportunity for the cement packaging market. These innovative materials cater to increasing environmental concerns and regulatory demands, allowing companies to offer greener solutions.

Expansion into ready-mix concrete and specialty cement markets also offers substantial potential. These segments require specialized packaging to meet unique handling and storage needs, driving demand for customized packaging solutions.

Integration of smart packaging technologies, such as RFID tags and QR codes, enables better tracking and supply chain transparency. This advancement helps companies improve inventory management and reduce losses.

Furthermore, growing investments in infrastructure projects worldwide increase the volume of cement consumption. This surge creates an opportunity for the cement packaging market to innovate and scale in line with rising demand for packaged cement products.

Emerging Trends

Shift to Multi-Layer Packaging and Digital Customization Shape Cement Packaging Trends

There is a clear shift towards multi-layer and composite packaging in the cement industry. These types of packaging offer enhanced durability and protection against moisture and mechanical damage, which improves product quality during storage and transit.

Rising consumer awareness about environmental impact is driving demand for recyclable packaging materials. Customers now expect sustainable options, prompting manufacturers to focus on eco-friendly packaging innovations.

Adoption of digital printing on cement bags is also becoming a popular trend. Customized branding and detailed product information help companies differentiate their products in a competitive market, while also facilitating marketing efforts.

Additionally, lightweight packaging materials are gaining traction as they help reduce logistics and transportation costs. Lighter packages allow for easier handling and lower fuel consumption during shipping, contributing to overall cost savings.

Regional Analysis

Asia Pacific Dominates the Cement Packaging Market with a Market Share of 40.2%, Valued at USD 1.84 Billion

The Asia Pacific region leads the cement packaging market, accounting for a dominant share of 40.2% and valued at approximately USD 1.84 Billion. Rapid industrialization and expansive construction activities across emerging economies are the main growth drivers. Increasing urbanization and large infrastructure investments fuel demand for sustainable and efficient cement packaging solutions.

North America Cement Packaging Market Overview

North America exhibits steady growth, supported by advanced packaging technologies and stringent environmental regulations promoting eco-friendly materials. The region benefits from well-established construction sectors and increasing demand for automation in packaging processes, fostering innovation and efficiency within the cement packaging landscape.

Europe Cement Packaging Market Trends

Europe’s market is shaped by strong regulatory frameworks focusing on sustainability and waste management. Investments in green packaging solutions and the shift towards recyclable materials are notable drivers. Growth is moderate but steady, supported by developed infrastructure and increasing adoption of automated packaging systems.

Middle East and Africa Cement Packaging Market Insights

The Middle East and Africa region is witnessing gradual market development owing to expanding construction activities and infrastructural projects. Growing urbanization and government initiatives to improve building standards are propelling demand for durable and efficient cement packaging formats. Market penetration is increasing despite infrastructural challenges.

Latin America Cement Packaging Market Dynamics

Latin America presents emerging opportunities driven by rising investments in residential and commercial construction. Increasing awareness about sustainable packaging and gradual adoption of automated technologies contribute to market growth. However, economic volatility and logistical challenges continue to restrain rapid expansion in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Cement Packaging Company Insights

In 2024, the global Cement Packaging Market is shaped by several influential players who are driving innovation and sustainability in packaging solutions.

Shalimar Group continues to expand its footprint by focusing on eco-friendly cement packaging materials, aligning with the increasing global demand for sustainable solutions. Their emphasis on durability and recyclability strengthens their position in key emerging markets.

UltraTech leverages its vast industry experience and strong supply chain network to cater to the growing construction sector, particularly in Asia. Their adoption of automated packaging technologies enhances efficiency, ensuring timely delivery and high-quality packaging performance, which is crucial in cement transportation and storage.

NNZ Inc. has made notable advancements by integrating advanced materials in cement bags that improve resistance to moisture and physical damage. This innovation helps reduce product loss during transit and storage, offering significant value to cement manufacturers and end-users.

Mondi is recognized for its leadership in sustainable packaging solutions and robust research and development capabilities. They focus on producing recyclable and biodegradable packaging options, which resonates well with stringent environmental regulations and the rising consumer awareness regarding waste management.

Together, these key players are instrumental in steering the cement packaging market towards more sustainable, durable, and technologically advanced solutions, meeting the evolving needs of the construction industry globally.

Top Key Players in the Market

- Shalimar Group

- UltraTech

- NNZ Inc.

- Mondi

- Stora Enso

- Umasree Texplast Pvt. Ltd.

- Billerud

- FORMOSA SYNTHETICS PVT. LTD.

- Dhuleva Industries

- Westrock

- R. G. Plasto-packs Pvt. Ltd.

- Knack Polymers

- Yiyang Wanlin Weave Packing Co., Ltd.

- Smurfit

- ARODO BV

Recent Developments

- In July 2024, Berlin-based Alcemy secured €9.2 million in funding aimed at advancing decarbonization efforts within the global cement and concrete industry. This investment supports the company’s mission to reduce carbon emissions and promote sustainable construction materials worldwide.

- In March 2024, Stockholm-based Cemvision raised €10 million to strengthen its leadership in the net-zero cement sector. The funding will accelerate Cemvision’s development of innovative technologies targeting carbon-neutral cement production.

- In May 2024, Phinma Corporation completed the acquisition of Petra Cement, expanding its footprint in the cement manufacturing industry. This strategic move aims to enhance Phinma’s production capabilities and market presence in the region.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.6 Billion |

| Forecast Revenue (2034) | USD 6.6 Billion |

| CAGR (2025-2034) | 3.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Paper, Plastic, Jute), By Capacity (Above 30 kg, 15 kg to 30 kg, 5 kg to 15 kg, Up to 5 kg) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Shalimar Group, UltraTech, NNZ Inc., Mondi, Stora Enso, Umasree Texplast Pvt. Ltd., Billerud, FORMOSA SYNTHETICS PVT. LTD., Dhuleva Industries, Westrock, R. G. Plasto-packs Pvt. Ltd., Knack Polymers, Yiyang Wanlin Weave Packing Co., Ltd., Smurfit, ARODO BV |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |