Quick Navigation

Report Overview

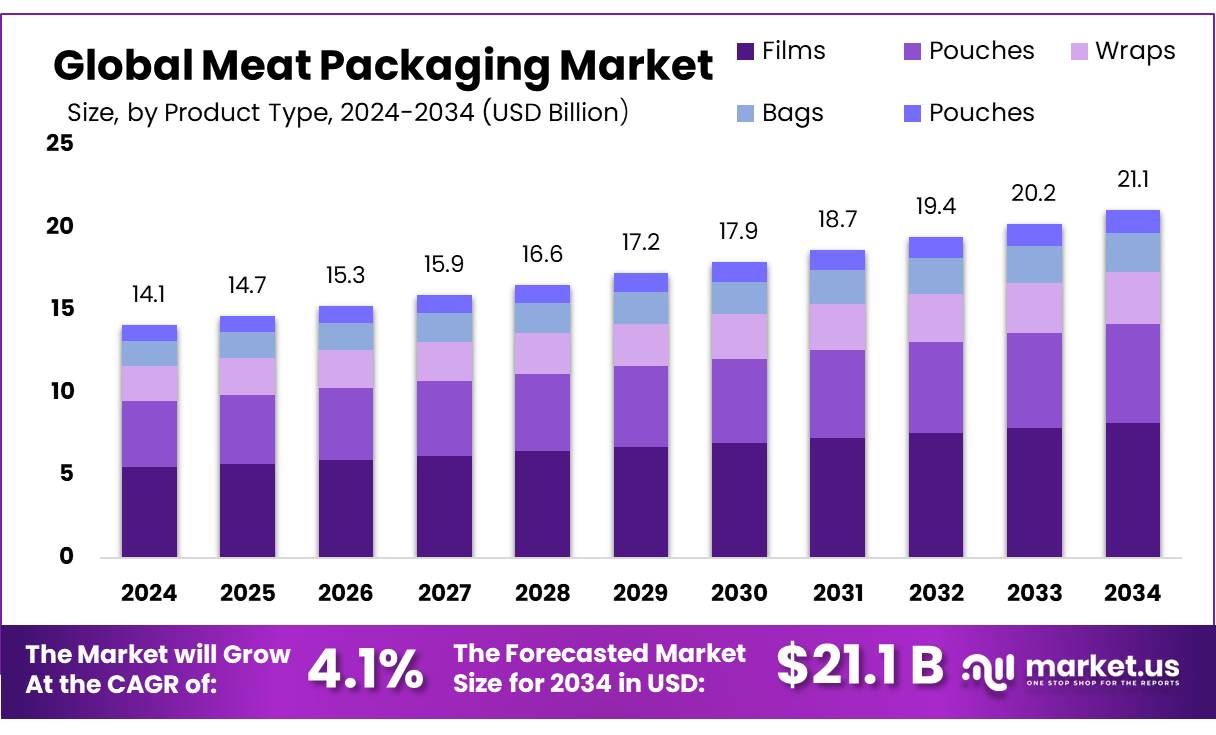

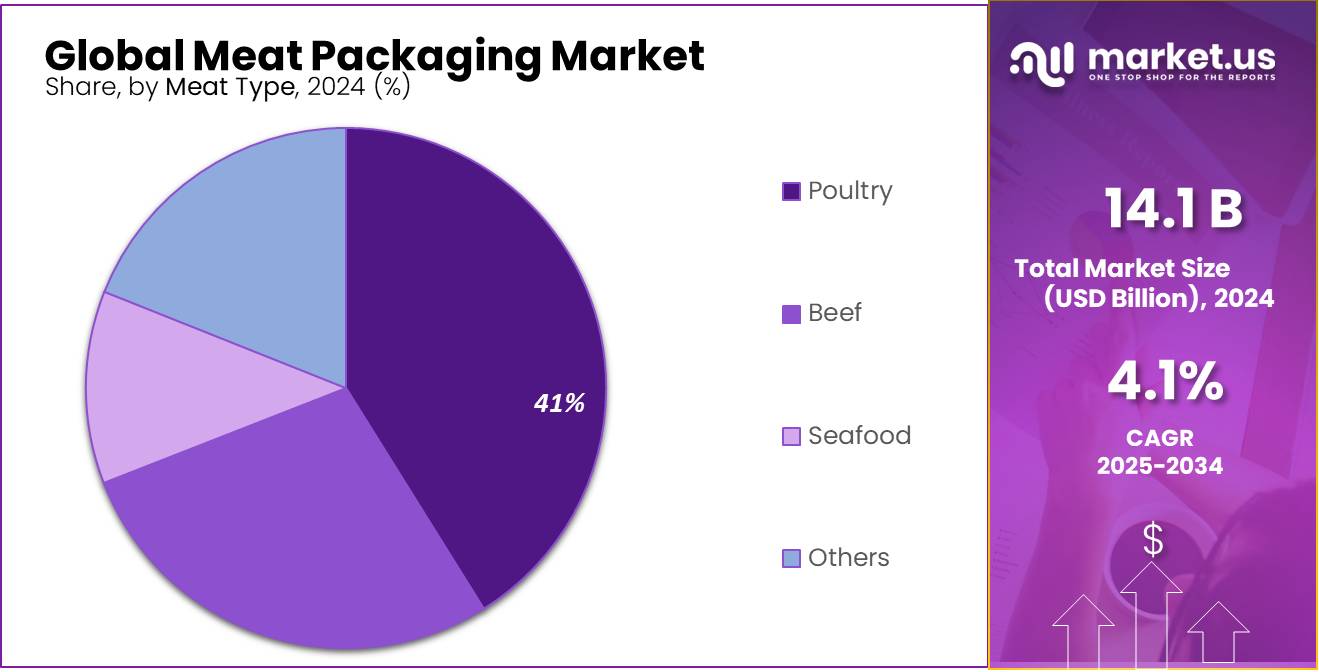

The Global Meat Packaging Market size is expected to be worth around USD 21.1 Billion by 2034, from USD 14.1 Billion in 2024, growing at a CAGR of 4.1% during the forecast period from 2025 to 2034.

The meat packaging concentrates industry plays a crucial role in the preservation, safety, and quality assurance of meat products across the global food supply chain. These concentrates, often composed of natural and synthetic compounds, are applied in packaging films or coatings to extend shelf life by inhibiting microbial growth and oxidation. With rising consumer demand for fresh and minimally processed meat products, the sector has witnessed robust growth, driven by advancements in packaging technologies and increasing awareness of food safety standards.

Government initiatives have been instrumental in propelling the growth of the meat packaging sector. The Production Linked Incentive Scheme for Food Processing Industry (PLISFPI), with an outlay of INR 10,900 crore, aims to support the creation of global food manufacturing champions and promote Indian brands of food products. Additionally, the Animal Husbandry Infrastructure Development Fund (AHIDF), amounting to INR 15,000 crore, facilitates the development of meat processing units and animal feed plants, thereby strengthening the overall meat supply chain.

The meat packaging concentrates is shaped by stringent regulations and evolving consumer preferences. According to the U.S. Department of Agriculture (USDA), approximately 27% of meat losses in the United States are attributed to spoilage caused by microbial contamination and oxidation, underscoring the need for improved packaging solutions. Governments worldwide are actively promoting sustainable packaging and food safety through various initiatives.

For instance, the European Union’s Horizon 2020 program has allocated significant funding toward innovative packaging materials that reduce food waste and improve preservation. Similarly, the U.S. Food and Drug Administration (FDA) enforces regulations on food contact substances that directly impact the formulation of meat packaging concentrates, ensuring consumer safety.

Several driving factors propel growth in the meat packaging concentrates industry. Increasing global meat consumption, projected to reach 366 million metric tons by 2025 according to the Food and Agriculture Organization (FAO) of the United Nations, creates a rising demand for enhanced packaging solutions.

Additionally, heightened consumer awareness regarding foodborne illnesses and product freshness has fueled the adoption of active and intelligent packaging technologies incorporating antimicrobial and antioxidant concentrates. The global push toward sustainability also encourages the development of biodegradable and bio-based packaging concentrates, aligning with government mandates such as the U.S. Environmental Protection Agency’s (EPA) Sustainable Materials Management program.

Key Takeaways

- Meat Packaging Market size is expected to be worth around USD 21.1 Billion by 2034, from USD 14.1 Billion in 2024, growing at a CAGR of 4.1%.

- Films held a dominant market position, capturing more than a 38.9% share of the global meat packaging market.

- Poultry held a dominant market position, capturing more than a 41.2% share of the global meat packaging market.

- 80–150 μm held a dominant market position, capturing more than a 39.1% share of the global meat packaging market.

- Vacuum Skin Packaging held a dominant market position, capturing more than a 33.8% share of the global meat packaging market.

- Plastic held a dominant market position, capturing more than a 67.4% share of the global meat packaging market.

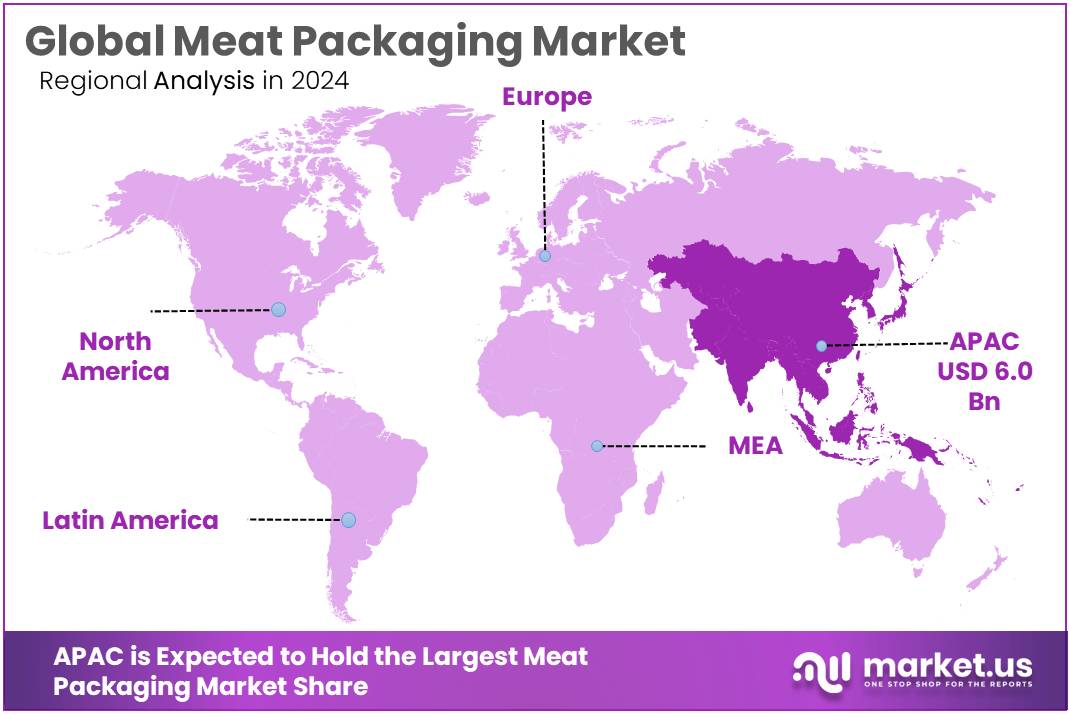

- Asia-Pacific (APAC) region emerged as the dominant force in the global meat packaging market, capturing a 43.1% share with a market value of approximately USD 6.0 billion.

Analysts’ Viewpoint

From an investment perspective, the meat packaging market presents a compelling opportunity, underpinned by robust growth and evolving consumer preferences. Consumer insights reveal a strong demand for packaging solutions that ensure product freshness, safety, and convenience. Innovations such as vacuum skin packaging and modified atmosphere packaging are gaining traction, offering extended shelf life and enhanced product presentation. However, the industry faces challenges, including environmental concerns over plastic waste and the need for sustainable packaging alternatives.

Regulatory bodies are increasingly implementing stringent guidelines to address these issues, necessitating investments in eco-friendly materials and technologies. For instance, the U.S. Environmental Protection Agency (EPA) proposed amendments in 2024 to reduce pollutants from meat processing facilities by approximately 100 million pounds per year, emphasizing the importance of sustainable practices.

Technological advancements are pivotal in shaping the future of meat packaging. Automation and smart packaging solutions are enhancing efficiency and traceability, meeting both consumer expectations and regulatory requirements. Investors should consider the balance between growth opportunities and potential risks, such as fluctuating raw material costs and compliance with evolving regulations. Companies that proactively adapt to these dynamics by investing in sustainable and innovative packaging solutions are well-positioned to capitalize on the market’s growth trajectory.

By Product Type

Films lead the Meat Packaging Market with 38.9% share in 2024, driven by freshness protection and visual appeal.

In 2024, Films held a dominant market position, capturing more than a 38.9% share of the global meat packaging market. This leading share is largely due to the material’s strong barrier properties, cost-efficiency, and versatility across different meat types—whether fresh, frozen, or processed. Films are widely used in both industrial and retail packaging because they help maintain meat freshness, reduce contamination risk, and enhance shelf appeal with transparent visibility. Their role has become even more critical as consumers demand safer and longer-lasting packaged meat options, especially in urban markets.

By Meat Type

Poultry leads the Meat Packaging Market with 41.2% share in 2024, fueled by rising demand for lean protein and quick-cook products.

In 2024, Poultry held a dominant market position, capturing more than a 41.2% share of the global meat packaging market. This dominance is strongly supported by the increasing global preference for leaner protein sources, affordability of poultry products, and shorter cooking times, which align well with modern consumer lifestyles. The surge in demand for ready-to-cook and portion-controlled poultry items has further pushed retailers and processors to invest more in effective and hygienic packaging formats specifically suited for chicken, turkey, and other poultry meats.

By Thickness

80–150 μm thickness dominates Meat Packaging Market with 39.1% share in 2024, balancing strength and flexibility for everyday meat applications.

In 2024, 80–150 μm held a dominant market position, capturing more than a 39.1% share of the global meat packaging market. This specific thickness range has gained popularity because it offers a practical balance between durability and material flexibility. It is widely used in vacuum-sealed packs, thermoforming films, and multilayer packaging systems, providing enough strength to protect meat from punctures while still being flexible enough to wrap various product shapes. These films also perform well under refrigeration and freezing conditions, which is critical for meat shelf life.

By Technology

Vacuum Skin Packaging leads the Meat Packaging Market with 33.8% share in 2024, driven by its superior shelf life and product visibility.

In 2024, Vacuum Skin Packaging held a dominant market position, capturing more than a 33.8% share of the global meat packaging market. This method is highly favored for its ability to tightly seal meat cuts against the film without damaging the product, effectively reducing oxygen exposure and extending shelf life. Retailers and processors prefer it not only for its excellent protective barrier but also because it showcases the product’s natural appearance, giving consumers a clear view of freshness and quality at the point of sale.

By Material

Plastic dominates the Meat Packaging Market with 67.4% share in 2024, due to its cost-efficiency, barrier strength, and wide adaptability.

In 2024, Plastic held a dominant market position, capturing more than a 67.4% share of the global meat packaging market. Its widespread use is mainly driven by its affordability, lightweight nature, and strong protective qualities. Plastic materials like polyethylene (PE), polyethylene terephthalate (PET), and polyvinyl chloride (PVC) offer excellent barrier properties that help preserve meat freshness, prevent contamination, and extend shelf life. These materials are also flexible enough to support various packaging types—ranging from trays and pouches to vacuum-sealed formats—making them the most practical choice for both industrial and retail use.

Key Market Segments

By Product Type

- Films

- Pouches

- Wraps

- Bags

- Pouches

By Meat Type

- Poultry

- Beef

- Seafood

- Others

By Thickness

- Below 80 μm

- 80-150 μm

- 150-250 μm

- Above 250 μm

By Technology

- Vacuum Skin Packaging

- Thermoforming

- Modified Atmosphere Packaging

- Others

By Material

- Plastic

- Plastic polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others

- Paper & Paperboard

- Aluminum Foil

- Biodegradable & Compostable Material

- Glass

- Metal & Foam

- Aluminum

- Steel

- Others

- Others

Drivers

Rising Meat Consumption as a Key Driver for the Meat Packaging Market

The global meat packaging industry is experiencing significant growth, primarily driven by the increasing demand for meat products worldwide. In 2024, global meat production is projected to reach 373 million tonnes, marking a 1.4% increase from the previous year. This growth is largely attributed to higher production of poultry and bovine meat, reflecting strong consumer demand and favorable operational margins .

In India, the trend is similarly upward. The country’s meat production rose to 10.25 million tonnes in the fiscal year 2023-24, registering a growth of 4.95% over the previous year. This increase is part of a broader trend, with meat production growing at a Compound Annual Growth Rate (CAGR) of 4.85% over the past decade . States like West Bengal, Uttar Pradesh, and Maharashtra are leading contributors to this growth.

Government initiatives have played a crucial role in supporting this expansion. The Animal Husbandry Infrastructure Development Fund (AHIDF), with an allocation of ₹15,000 crore, aims to boost private sector investment in developing animal husbandry infrastructure, including meat processing units . Such initiatives are expected to enhance the efficiency and capacity of meat production and processing in the country.

As meat consumption continues to rise, the demand for effective packaging solutions becomes more critical. Packaging not only ensures the safety and quality of meat products but also extends shelf life and meets the evolving preferences of consumers for convenience and sustainability. Therefore, the meat packaging industry is poised for continued growth, driven by both increasing consumption and supportive government policies.

Restraints

Environmental Concerns Over Plastic Waste in Meat Packaging

One significant challenge facing the meat packaging industry is the environmental impact of plastic waste. Plastic packaging, while effective in preserving meat products, contributes substantially to environmental pollution. According to the European Commission, in 2019, the European Union generated approximately 15.4 million tonnes of plastic packaging waste, with only 41% being recycled . This indicates a substantial amount of plastic waste that could potentially end up in landfills or the natural environment.

In India, the situation is equally concerning. The Central Pollution Control Board reported that in the financial year 2019-2020, India generated approximately 3.4 million tonnes of plastic waste, with a significant portion attributed to packaging materials . The accumulation of plastic waste not only poses a threat to terrestrial and marine ecosystems but also contributes to the broader issue of environmental degradation.

Recognizing the environmental hazards posed by plastic waste, the Indian government has initiated several measures to mitigate the impact. The Ministry of Environment, Forest and Climate Change has implemented the Plastic Waste Management Rules, which aim to phase out single-use plastics and promote the use of biodegradable alternatives . Additionally, the government has been encouraging industries to adopt sustainable packaging solutions through various incentives and awareness programs.

Despite these efforts, the transition to environmentally friendly packaging in the meat industry faces challenges. The primary concerns include the cost implications of adopting sustainable materials and the need for technological advancements to ensure that alternative packaging solutions meet the required standards for preserving meat products. Furthermore, there is a need for increased consumer awareness and demand for sustainably packaged products to drive significant change in the industry.

Opportunity

Government Initiatives Fueling Growth in India’s Meat Packaging Sector

India’s meat packaging industry is poised for significant growth, driven by robust government initiatives aimed at enhancing the food processing sector. The Ministry of Food Processing Industries (MoFPI) has launched several schemes to bolster infrastructure, encourage private investment, and promote sustainable practices.

One such initiative is the Production Linked Incentive Scheme for Food Processing Industry (PLISFPI), which aims to expand processing capacities and generate processed food output worth ₹33,494 crore. This scheme is expected to create employment opportunities and attract substantial investment in the sector.

Additionally, the Pradhan Mantri Kisan SAMPADA Yojana (PMKSY) focuses on creating modern infrastructure with efficient supply chain management from farm gate to retail outlet. This comprehensive package is designed to reduce wastage, increase processing levels, and enhance the export of processed foods.

The government’s emphasis on developing Mega Food Parks provides a platform for food processing units to operate in a cluster-based approach. These parks offer state-of-the-art facilities, reducing logistics costs and ensuring better value for farmers.

Trends

Adoption of Sustainable Packaging Solutions in the Meat Industry

The meat packaging industry is witnessing a significant shift towards sustainable packaging solutions, driven by increasing environmental concerns and consumer demand for eco-friendly products. Traditional plastic packaging, while effective in preserving meat products, contributes substantially to environmental pollution. According to the Ministry of Food Processing Industries (MoFPI), the Indian government has implemented the Plastic Waste Management Rules to phase out single-use plastics and promote biodegradable alternatives.

In response to these regulations, meat packaging companies are exploring innovative materials and technologies. For instance, the use of biodegradable films made from plant-based materials is gaining traction. These films not only reduce environmental impact but also maintain the quality and safety of meat products. Additionally, vacuum skin packaging (VSP) is being adopted for its ability to extend shelf life and reduce the need for preservatives.

Consumer awareness plays a crucial role in this transition. A study by the Food Safety and Standards Authority of India (FSSAI) indicates that consumers are increasingly prioritizing sustainability in their purchasing decisions. The demand for transparent labeling and environmentally responsible packaging is influencing manufacturers to adopt greener practices.

Regional Analysis

Asia-Pacific dominates the global Meat Packaging Market with 43.1% share, valued at USD 6.0 billion, driven by rising meat consumption and urbanization.

In 2024, the Asia-Pacific (APAC) region emerged as the dominant force in the global meat packaging market, capturing a 43.1% share with a market value of approximately USD 6.0 billion. This regional leadership is driven by a sharp increase in meat consumption, rapid urban development, and expansion of organized retail. Countries such as China, India, Japan, and Australia are playing a central role in this growth due to growing middle-class populations, changing dietary patterns, and a shift toward protein-rich diets. According to the Food and Agriculture Organization (FAO), China alone consumes over 28% of the world’s meat, reflecting strong domestic demand for safe, packaged meat products.

Moreover, increasing demand for hygienic and extended-shelf-life packaging, especially in the context of rising exports and urban consumption, has accelerated the adoption of vacuum packaging, MAP, and recyclable plastic films across the region. As APAC continues to invest in automation, logistics, and food processing zones, it is expected to remain the global hub for meat packaging innovation and volume in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Amcor plc is a leading global packaging player with a strong footprint in meat packaging through flexible and rigid plastic solutions. The company focuses on recyclable and high-barrier packaging materials that enhance shelf life and food safety. With operations in over 40 countries and advanced R&D capabilities, Amcor continues to innovate in vacuum skin and MAP technologies tailored for meat processors. In 2024, the company emphasized circular packaging initiatives aligned with sustainability goals and increased investment in APAC meat packaging markets.

Berry Global plays a crucial role in the meat packaging segment, specializing in polyethylene and multilayer films designed for freshness and leak prevention. With over 290 global facilities, the company supports meat processors with form-fill-seal films, vacuum bags, and thermoforming solutions. In 2024, Berry enhanced its focus on post-consumer recycled content and downgauging technologies to reduce environmental impact. Its strong U.S. base and increasing demand from Asia contribute significantly to its market presence in meat packaging.

Smurfit Kappa brings fiber-based, sustainable packaging solutions to the meat industry, primarily through corrugated packaging used in cold chain logistics and bulk meat transportation. Headquartered in Ireland and active in over 30 countries, it has focused on replacing plastic trays with paper-based solutions where possible. In 2024, the company introduced innovations in moisture-resistant cardboard and enhanced printing technologies to meet retailer and export needs. Its eco-smart packaging lines cater strongly to European and Latin American meat markets.

Top Key Players in the Market

- Amcor plc

- Bery Global Group, Inc.

- Smurfit Kappa plc

- Faerch A/S

- Constantia Flexibles Group GmbH

- Flavorseal

- Mannok Pack

- PLASTOPIL

- Cibapac

- Bollore Group

- Uniflex

- SP Group

- Foster International Packaging

- Winpak, Ltd.

Recent Developments

In 2024, Smurfit Kappa, now operating as Smurfit Westrock, strengthened its position in the meat packaging sector by focusing on sustainable, paper-based solutions tailored for fresh and frozen meat products. The company reported a revenue of €2.7 billion in the first quarter of 2024, with an EBITDA of €487 million and an EBITDA margin of 18.0%.

In 2024, Amcor reported net sales of $13.64 billion for the fiscal year 2024, with the Flexibles Packaging segment contributing $10.33 billion, underscoring the company’s robust presence in flexible packaging solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 14.1 Bn |

| Forecast Revenue (2034) | USD 21.1 Bn |

| CAGR (2025-2034) | 4.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Films, Pouches, Wraps, Bags, Pouches), By Meat Type (Poultry, Beef, Seafood, Others), By Thickness (Below 80 μm, 80-150 μm, 150-250 μm, Above 250 μm), By Technology (Vacuum Skin Packaging, Thermoforming, Modified Atmosphere Packaging, Others), By Material (Plastic, Paper and Paperboard, Aluminum Foil, Biodegradable and Compostable Material, Glass, Metal and Foam, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Amcor plc, Bery Global Group, Inc., Smurfit Kappa plc, Faerch A/S, Constantia Flexibles Group GmbH, Flavorseal, Mannok Pack, PLASTOPIL, Cibapac, Bollore Group, Uniflex, SP Group, Foster International Packaging, Winpak, Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |