Quick Navigation

Report Overview

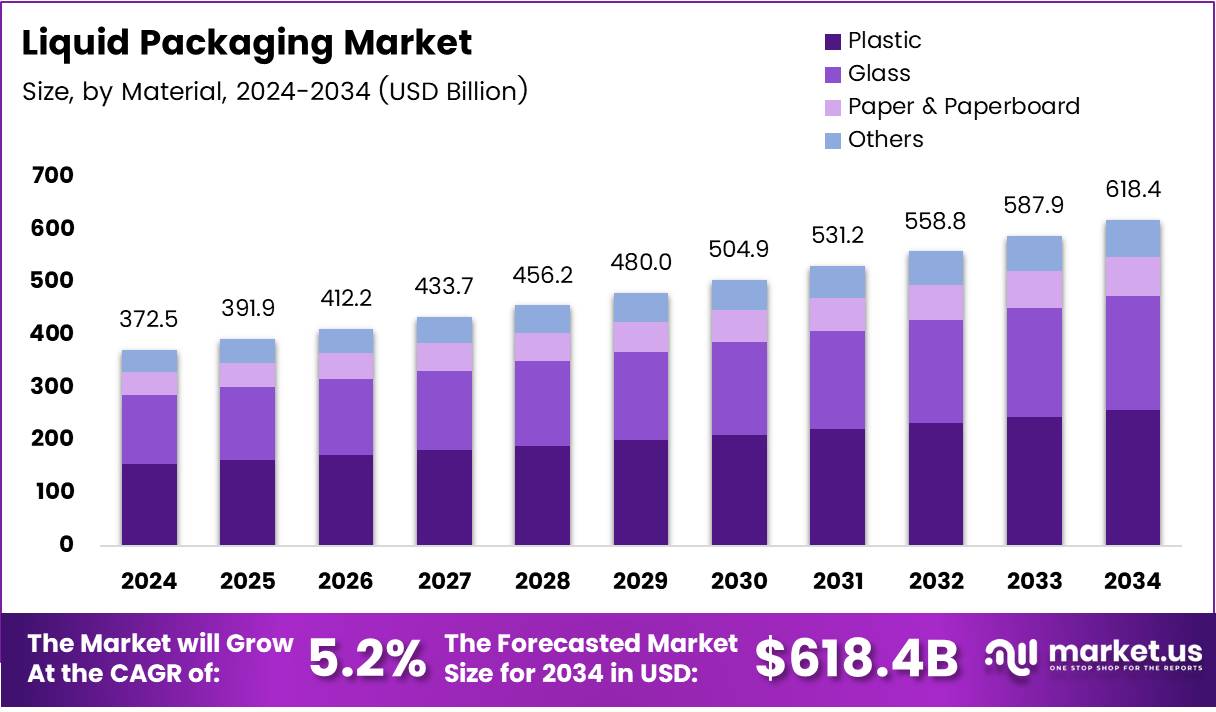

The Global Liquid Packaging Market size is expected to be worth around USD 618.4 Billion by 2034, from USD 372.5 Billion in 2024, growing at a CAGR of 5.2% during the forecast period from 2025 to 2034.

The liquid packaging market serves as a vital segment within the global packaging industry, focused on the safe storage, transport, and dispensing of liquids. It covers various product types such as cartons, bottles, pouches, and bag-in-box formats used across food, beverage, pharmaceutical, and personal care sectors. As urbanization and lifestyle changes increase, the need for hygienic and convenient liquid packaging continues to rise globally.

The industry is experiencing notable momentum due to the shift towards on-the-go consumption and longer shelf-life preferences. Consumer expectations around product integrity, leakage resistance, and user-friendliness are pushing innovations in materials and design. Additionally, the surge in e-commerce for beverages and liquid personal care products is reshaping distribution formats and durability requirements.

The market is scaling rapidly due to the expanding demand for ready-to-drink beverages and processed liquid foods. According to Tresu, annually more than 1,200 billion litres of packed liquid food are consumed globally, underscoring the scale of consumption driving packaging demand. Manufacturers are now focusing on advanced multilayer films and aseptic packaging to extend shelf life and reduce spoilage.

There is a vast opportunity in adopting biodegradable, recyclable, and reusable materials, particularly as sustainability becomes a business differentiator. According to RocketIndustrial, 82% of consumers are willing to pay more for sustainable packaging, while 90% of Gen-Z consumers actively seek such alternatives. This shift is prompting R&D investment in bio-based polymers and compostable solutions.

Public policies and funding are also steering market expansion. Governments across Europe and Asia have introduced incentives for sustainable packaging plants and recycling infrastructure. These programs are accelerating transitions from single-use plastics to eco-friendly alternatives, providing capital support and policy frameworks for liquid packaging innovation.

Stringent regulatory frameworks related to food safety, material toxicity, and environmental compliance are reshaping product development. Regulations like the EU Single-Use Plastics Directive and India’s Extended Producer Responsibility (EPR) mandate are compelling firms to innovate responsibly and align packaging with circular economy goals.

Looking ahead, the liquid packaging market is poised for strong growth driven by sustainability, regulatory reforms, and digital printing technologies. Smart packaging with traceability, QR codes, and freshness indicators is gaining traction, especially in the food and pharma sectors. Companies investing in eco-innovation and automation stand to benefit the most in this evolving market landscape.

Key Takeaways

- The global liquid packaging market is projected to reach USD 618.4 Billion by 2034, up from USD 372.5 Billion in 2024, growing at a CAGR of 5.2%.

- Plastic dominated the material segment in 2024 with a 39.1% share, due to its lightweight, cost-effectiveness, and liquid compatibility.

- Rigid packaging held a 58.2% market share in the type segment in 2024, owing to its durability and shelf presentation benefits.

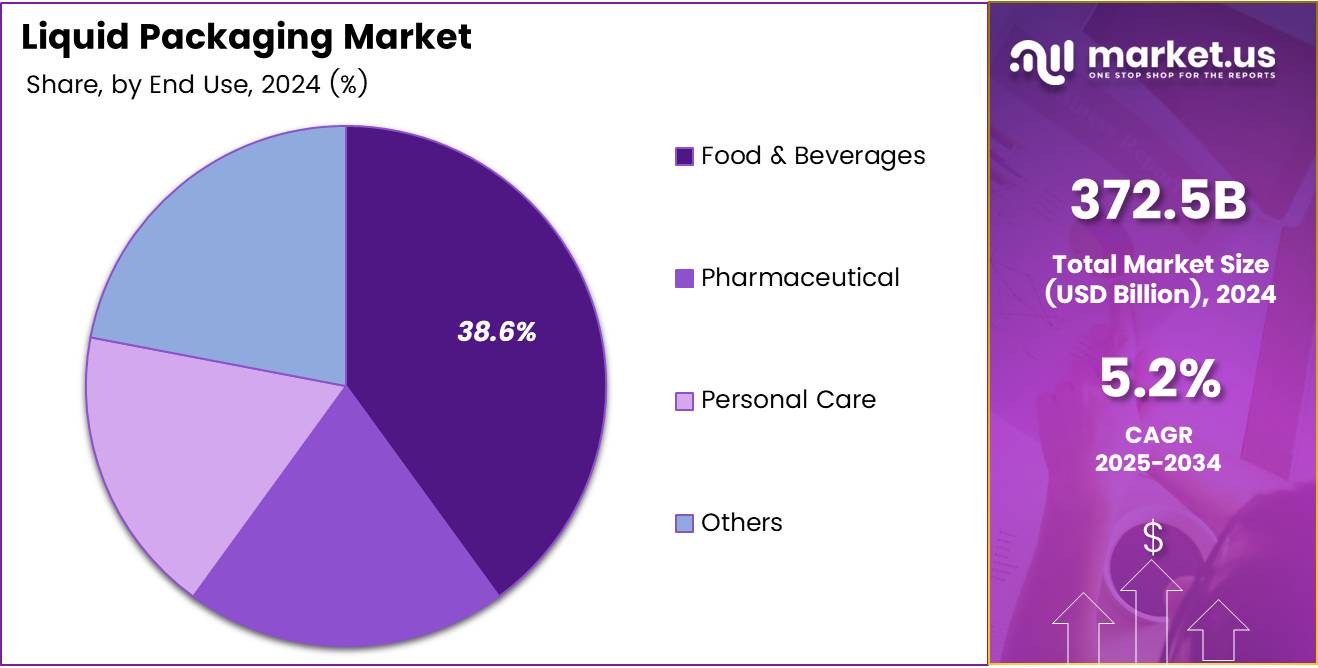

- Food & Beverages emerged as the leading end-use segment in 2024, capturing 38.6% of the market.

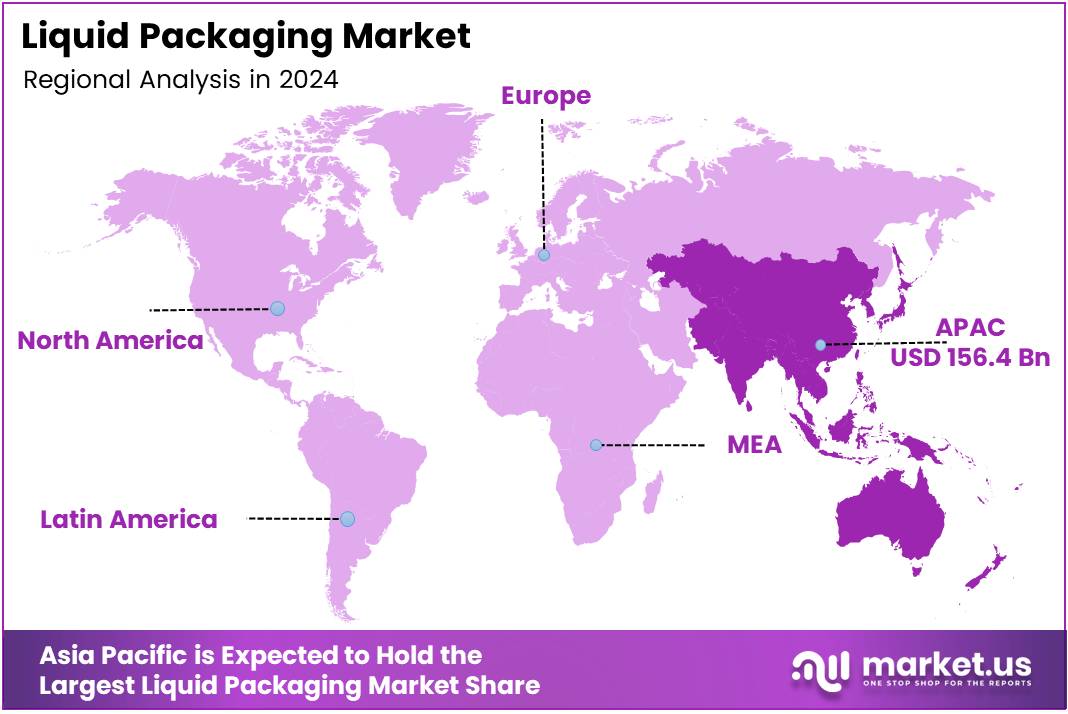

- Asia Pacific led the regional market in 2024 with a 42.5% share, driven by urbanization, rising consumption, and sustainability efforts.

Material Analysis

Plastic packaging leads with 39.1% due to its versatility and cost-efficiency in liquid containment.

In 2024, Plastic held a dominant market position in the By Material Analysis segment of the Liquid Packaging Market, with a 39.1% share. Plastic’s dominance stems from its lightweight, cost-effectiveness, and compatibility with a broad spectrum of liquids, including water, dairy, soft drinks, and household chemicals. Its high adaptability and low transportation cost further reinforce its market hold.

Glass, while more fragile, remains a preferred material in sectors demanding premium and inert packaging. Its non-reactive properties make it ideal for alcohol, juices, and pharmaceuticals, where product purity and extended shelf life are critical.

Paper & Paperboard are increasingly used in sustainable packaging strategies, particularly for short-life consumables. As environmental regulations tighten, brands are shifting toward recyclable and biodegradable options that align with consumer values.

Others, such as aluminum and bio-based materials, serve niche markets where innovation or premium branding is a priority. Though adoption remains limited, advancements in material science may enhance their future scalability.

Type Analysis

Rigid formats dominate with 58.2% due to their structural strength and widespread use across industries.

In 2024, Rigid held a dominant market position in the By Type Analysis segment of the Liquid Packaging Market, with a 58.2% share. Rigid packaging, including bottles, cartons, and containers, ensures product protection, stackability, and visual shelf appeal. It is especially prevalent in food, beverage, and healthcare industries that require structural integrity and leak-proof delivery.

Flexible packaging, while lighter and more cost-efficient in logistics, is growing in demand for single-use and portable formats. However, its recyclability and protective limitations still pose challenges in broader adoption for high-volume or long-shelf-life liquids.

End Use Analysis

Food & Beverages top the chart with 38.6% due to consistent consumption and diverse liquid packaging demand.

In 2024, Food & Beverages held a dominant market position in the By End Use Analysis segment of the Liquid Packaging Market, with a 38.6% share. The segment benefits from the continuous global consumption of liquids such as milk, juices, carbonated drinks, and edible oils. Brand competition and demand for shelf-ready convenience contribute to this strong market presence.

Pharmaceutical applications follow closely, driven by the need for secure, sterile, and dosage-specific packaging of syrups, suspensions, and other liquid drugs. Regulatory compliance and patient safety remain key drivers.

Personal Care products, including shampoos, conditioners, and cleansers, are witnessing rising demand, especially in emerging economies. Innovative packaging formats that enhance shelf appeal and user convenience are accelerating growth here.

Others include packaging for chemicals, lubricants, and industrial liquids, where durability, compliance, and compatibility with hazardous contents determine packaging choices. These markets, though smaller, require precision-engineered solutions.

Key Market Segments

By Material

- Plastic

- Glass

- Paper & Paperboard

- Others

By Type

- Rigid

- Flexible

By End Use

- Food & Beverages

- Pharmaceutical

- Personal Care

- Others

Drivers

Rising Demand for Convenience Boosts Liquid Packaging Market Growth

The rising demand for convenience plays a major role in accelerating the liquid packaging market. Today’s fast-paced lifestyle pushes consumers toward ready-to-drink and easy-to-carry products, such as bottled water, juices, and dairy beverages. This shift boosts the need for innovative liquid packaging that offers portability, safety, and long shelf life.

At the same time, technology is reshaping the market. New advancements like smart packaging and eco-friendly materials are helping brands extend product freshness, enhance consumer engagement, and reduce environmental impact. These innovations make liquid packaging more efficient and adaptable to evolving consumer preferences.

Additionally, the global rise in beverage consumption further fuels the market. As more people consume packaged drinks, including soft drinks, energy drinks, and alcoholic beverages, the demand for reliable, tamper-proof, and cost-effective liquid packaging continues to rise. Together, these factors are steadily driving market expansion.

Restraints

High Packaging Costs Pose Challenges to Market Expansion

One of the key restraints in the liquid packaging market is the high cost of materials and technologies. Advanced packaging solutions that enhance durability or sustainability often require costly production methods, which can deter smaller companies from entering or competing in the market.

Moreover, environmental concerns about plastic packaging remain a major challenge. Despite improvements in recyclable and biodegradable options, the overall reliance on plastic continues to attract regulatory scrutiny. Governments and environmental groups are pushing for stricter rules, which increases compliance costs for manufacturers and restricts growth in regions with strict policies.

Growth Factors

Shift Toward Eco-Friendly Packaging Creates New Opportunities

The growing shift toward eco-friendly packaging opens up strong growth avenues for liquid packaging companies. Consumers are becoming more aware of their environmental impact and are actively choosing brands that offer recyclable or biodegradable packaging. This trend encourages companies to innovate with plant-based or reusable materials, expanding their market reach.

The rise in demand for health-conscious beverages also supports market growth. Functional drinks, organic juices, and probiotic beverages require packaging that preserves quality while meeting safety standards. This creates demand for specialized packaging with barrier properties and informative labeling.

Furthermore, emerging markets such as Asia-Pacific and Latin America offer fresh business potential. These regions are experiencing rising incomes and modernizing retail infrastructure, which drives demand for packaged liquids. As urbanization continues, the need for convenient and hygienic packaging will only grow.

Emerging Trends

Smart Packaging Integration is Shaping Market Trends

The integration of smart technologies is one of the most prominent trends in the liquid packaging industry. Features like QR codes, freshness indicators, and temperature sensors are helping brands build trust and transparency with consumers, while also improving inventory tracking and quality control.

Lightweight packaging is another key trend. Consumers and manufacturers prefer materials that are easy to carry and reduce transportation costs. This shift supports the development of flexible packaging solutions that maintain product integrity without adding bulk.

Lastly, sustainability remains at the heart of evolving market trends. With growing pressure from consumers and regulators, brands are investing in sustainable innovations. From recycled materials to carbon-neutral production processes, companies are reshaping their supply chains to stay competitive and responsible.

Regional Analysis

Asia Pacific Leads the Liquid Packaging Market with a Share of 42.5%, Valued at USD 156.4 Billion

In 2024, Asia Pacific emerged as the leading region in the liquid packaging market, accounting for 42.5% of the global share, driven by strong demand from beverage, dairy, and personal care sectors.

Rising urbanization, increasing consumption of packaged liquids, and government focus on sustainable packaging have supported its dominance. The regional market was valued at USD 156.4 billion, with China, India, and Southeast Asia showing significant uptake of flexible and eco-friendly formats.

Regional Mentions:

North America is witnessing steady growth due to high consumer demand for convenient and ready-to-use beverage products, along with stringent packaging safety regulations. Advanced technologies and a shift towards recyclable packaging are contributing to the market’s maturity in the region, particularly in the U.S. and Canada.

Europe follows closely, bolstered by strong environmental regulations and a well-established food and beverage industry. The region emphasizes the use of biodegradable and paper-based packaging solutions, aligning with EU circular economy policies and sustainability targets.

Latin America is experiencing moderate expansion, supported by increasing urban populations and rising demand for packaged juices, dairy, and functional beverages. Brazil and Mexico are emerging as key contributors due to growing retail penetration and consumption trends.

Middle East & Africa shows gradual growth as packaged water and liquid food products gain popularity amid rising health awareness and economic development. Demand is also increasing for cost-effective and shelf-stable packaging solutions, especially in GCC countries and parts of Africa.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global liquid packaging market reflects strategic advancements and innovation-driven competition among leading industry players. Mondi continues to make strides in sustainable packaging solutions, focusing on flexible packaging formats with recyclable and paper-based alternatives that align with rising environmental regulations and consumer demand for eco-conscious products.

WestRock Company has capitalized on its integrated packaging operations by expanding its paper-based liquid carton solutions. Its commitment to circular economy practices and investments in packaging automation technologies have bolstered its presence across North America and Europe.

ProAmpac has gained significant market traction through its diverse product portfolio in both rigid and flexible liquid packaging. The company’s emphasis on proprietary film technologies and its push for customized, shelf-ready packaging have enhanced its appeal in the food and beverage sector.

Smurfit Kappa, known for its paper-based innovations, has extended its leadership through the development of Bag-in-Box® and other sustainable liquid containment systems. Its strong European footprint and consistent investment in R&D make it a key contributor to the market’s shift away from plastics.

Other prominent players such as Berry Global Inc, International Paper, and Sealed Air continue to innovate in barrier materials and sealing performance. Companies like SIG, Greiner Packaging, and Stora Enso are also investing in hybrid formats that blend paper with protective coatings, targeting both food safety and recyclability. With rising demand for secure and sustainable solutions, strategic developments from industry leaders are expected to shape the competitive dynamics of the liquid packaging landscape throughout 2024.

Top Key Players in the Market

- Mondi

- WestRock Company

- ProAmpac

- Smurfit Kappa

- Berry Global Inc

- International Paper

- Sealed Air

- SIG

- Greiner Packaging

- Stora Enso

- DS Smith

- Ball Corporation

- ALPLA

- Tetra Pak

- Sonoco Products Company

- Amcor plc

Recent Developments

- In October 2024, Notpla secured £20 million in funding to accelerate the development and commercialization of its sustainable packaging materials derived from seaweed and plants. The investment aims to scale eco-friendly alternatives to single-use plastics across global markets.

- In December 2024, Liquid AI raised $250 million in funding to drive advancements in general-purpose artificial intelligence. The capital will support research, infrastructure, and talent acquisition for next-gen AI applications.

- In December 2024, Movopack secured $2.5 million in funding to expand its sustainable e-commerce packaging solutions. The startup focuses on reusable and eco-friendly packaging designed to reduce waste in online retail.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 372.5 Billion |

| Forecast Revenue (2034) | USD 618.4 Billion |

| CAGR (2025-2034) | 5.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Plastic, Glass, Paper & Paperboard, Others), By Type (Rigid, Flexible), By End Use (Food & Beverages, Pharmaceutical, Personal Care, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Mondi, WestRock Company, ProAmpac, Smurfit Kappa, Berry Global Inc, International Paper, Sealed Air, SIG, Greiner Packaging, Stora Enso, DS Smith, Ball Corporation, ALPLA, Tetra Pak, Sonoco Products Company, Amcor plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |