Global Caustic Soda Flakes Market Size, Share, Growth Analysis By Form (Flake, Granular, Pellet), By Purity Level (Lower Purity, Standard Purity, High Purity), By Application (Chemical Manufacturing, Pulp and Paper, Textile Processing, Water Treatment, Food Processing), By End Use (Construction, Automotive, Electronics, Pharmaceuticals, Agriculture), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: May 2026

- Report ID: 186236

- Number of Pages: 240

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

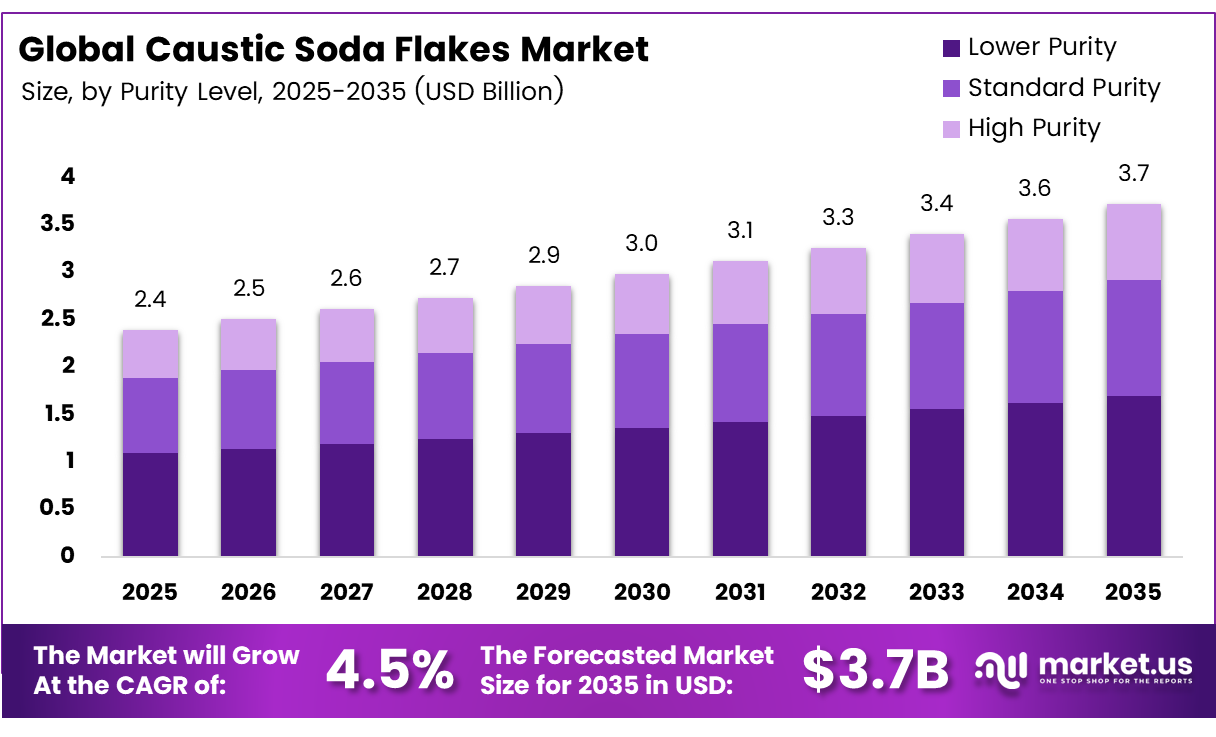

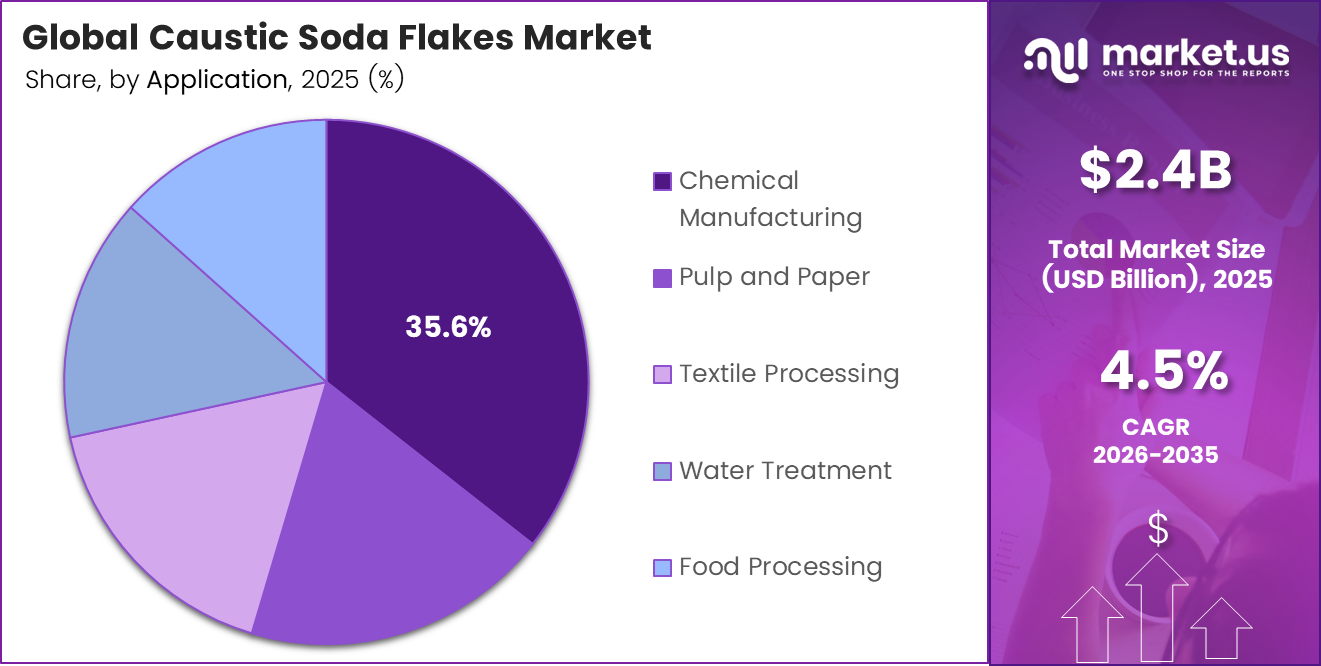

The Global Caustic Soda Flakes Market size is expected to be worth around USD 3.7 billion by 2035 from USD 2.4 billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

Caustic soda flakes — the solid form of sodium hydroxide — serve as a foundational industrial alkali across chemical manufacturing, pulp and paper, textile processing, water treatment, and food processing. Their solid form makes handling, storage, and transport more practical than liquid caustic soda, which directly supports adoption in mid-scale industrial operations.

Alumina refining and aluminum processing represent one of the most volume-intensive demand sources, as both processes require large and consistent quantities of high-purity alkaline input. Expansion of smelting and refining capacity across Southeast Asia and the Middle East directly extends the addressable market for flake-form caustic soda producers.

U.S. Gulf Coast liquid caustic soda exports reached 3.16 million dmt over the latest 12 months, up 19% from 2.64 million dmt. This export acceleration confirms that producers are finding stronger demand signals abroad than domestic consumption alone would justify, a structural indicator that global industrial activity is absorbing available supply faster than new capacity comes online.

DCM Shriram’s Kota plant grew steadily from an initial 30 TPD to a current 550 TPD, reflecting a phased expansion strategy aligned with demand growth. Globally, the caustic soda market showed signs of balance, with Argus Media reporting U.S. Gulf Coast export prices at $390–$440/dmt FOB for the third straight week, while U.S. liquid caustic soda exports rose 19% year-on-year to 3.16 million dmt, highlighting strong international demand absorption.

Key Takeaways

- The Global Caustic Soda Flakes Market was valued at USD 2.4 billion in 2025 and is forecast to reach USD 3.7 billion by 2035 at a CAGR of 4.5% over the forecast period 2026 to 2035.

- The Flake segment leads with a 52.3% market share in 2025.

- Standard Purity holds the dominant position with a 54.2% share.

- Chemical Manufacturing accounts for 35.6% of total demand.

- Construction represents the largest segment at 29.1% share.

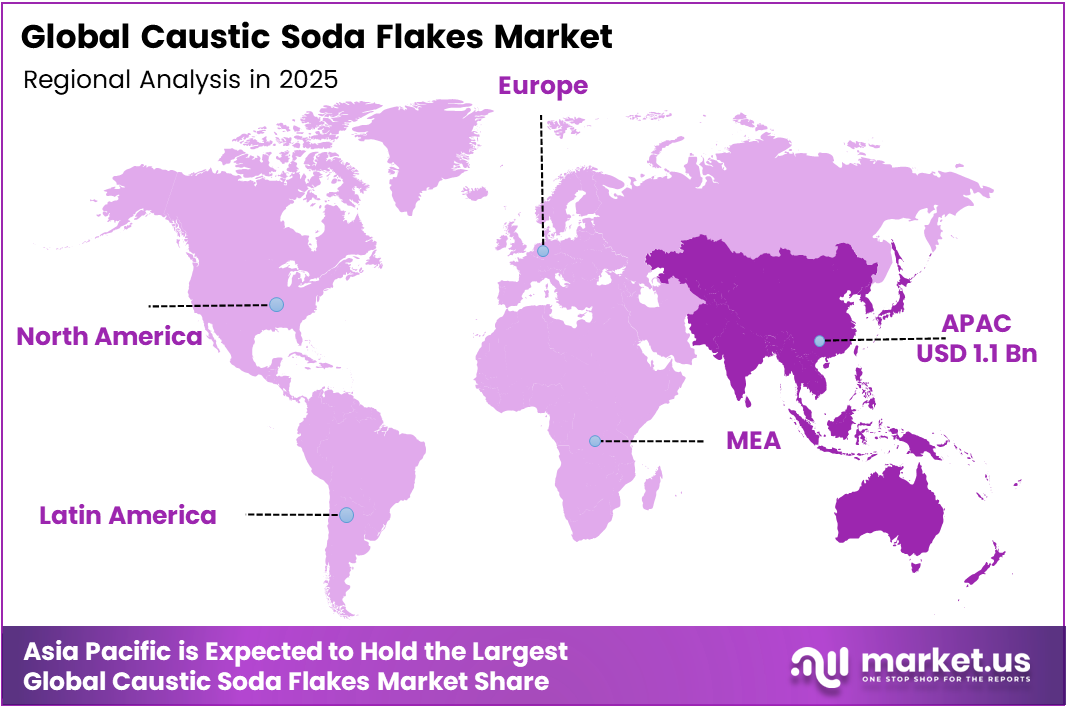

- Asia-Pacific dominates regional demand with a 44.4% share, valued at approximately USD 1.1 billion.

Product Analysis

Flake dominates with 52.3% due to superior handling and transport efficiency.

In 2025, Flake held a dominant market position in the By Form segment of the Caustic Soda Flakes Market, with a 52.3% share. Flake-form caustic soda dissolves faster than pellets and stores more safely than liquid alternatives, making it the preferred input for mid-scale chemical processors, textile units, and food-grade applications where precision dosing matters.

Granular caustic soda serves buyers who prioritize flow control and reduced dust exposure during bulk handling. It occupies a smaller but defensible share among construction chemical producers and water treatment operators who blend dry alkaline inputs into automated dosing systems, where granule uniformity reduces measurement error and process downtime.

Purity Level Analysis

Standard Purity dominates with 54.2% due to a cost-effective fit for mainstream industrial processes.

In 2025, Standard Purity held a dominant market position in the By Purity Level segment of the Caustic Soda Flakes Market, with a 54.2% share. Standard purity grades meet the technical specifications of the highest-volume application sectors — pulp and paper, textile processing, and water treatment — where purity thresholds do not require pharmaceutical-grade input, keeping procurement costs predictable.

Lower Purity grades serve cost-sensitive applications such as certain construction chemical formulations and industrial cleaning processes where alkalinity level matters more than contamination control. Buyers in these segments treat caustic soda as a commodity input, making price per unit the primary procurement criterion rather than technical specification compliance.

Application Analysis

Chemical Manufacturing dominates with 35.6% due to high-volume continuous process requirements.

In 2025, Chemical Manufacturing held a dominant market position in the By Application segment of the Caustic Soda Flakes Market, with a 35.6% share. Chemical synthesis operations consume caustic soda in continuous, large-batch processes — creating predictable, high-frequency purchasing patterns that make this segment the most commercially stable demand source for flake producers.

Pulp and Paper processing uses caustic soda in the kraft pulping process to break down wood fibers and in the bleaching stages. This application ties directly to global paper and packaging consumption cycles, meaning producers serving this segment benefit from relatively stable off-take volumes, even as individual paper mill capacity fluctuates by region.

End Use Analysis

Construction dominates with 29.1% due to large-scale alkaline chemical demand in surface treatment.

In 2025, Construction held a dominant market position in the By End Use segment of the Caustic Soda Flakes Market, with a 29.1% share. The sector consumes caustic soda in concrete surface treatments, alumina-based binding agents, and construction chemical formulations — applications that scale directly with infrastructure project pipelines across emerging markets in Asia and Africa.

Automotive manufacturing uses caustic soda in metal surface treatment, aluminum parts cleaning, and battery chemical production. The shift toward electric vehicle platforms increases aluminum component intensity per vehicle, which indirectly expands caustic soda consumption within the automotive supply chain at a rate faster than traditional vehicle production volumes alone would suggest.

Electronics manufacturing applies caustic soda in printed circuit board etching, semiconductor cleaning, and display panel production. As chip fabrication expands across Taiwan, South Korea, and newly established facilities in the United States and India, demand for high-purity caustic soda from the electronics segment grows alongside capital investment in fab infrastructure.

Key Market Segments

By Form

- Flake

- Granular

- Pellet

By Purity Level

- Lower Purity

- Standard Purity

- High Purity

By Application

- Chemical Manufacturing

- Pulp and Paper

- Textile Processing

- Water Treatment

- Food Processing

By End Use

- Construction

- Automotive

- Electronics

- Pharmaceuticals

- Agriculture

Emerging Trends

High-Purity Demand and Digital Automation Reshape Caustic Soda Flakes Production Economics

The Standard Purity segment holds 54.2% of volume — yet specialty chemical formulators are actively upgrading toward high-purity grades for more demanding applications. This shift creates a bifurcating market structure where commodity-grade producers face margin pressure while membrane-cell operators with purity-certified output capture incremental value.

Global producers now pursue strategic capacity expansion backed by long-term supply agreements rather than spot market reliance. DCM Shriram’s Bharuch captive power plant uses biomass as up to 40% fuel blend, demonstrating that sustainability integration at the plant level is moving from a compliance consideration to a procurement differentiator for buyers with ESG supply chain commitments.

Digital process automation is entering caustic soda production networks, allowing real-time monitoring of electrolyser performance, energy consumption, and product purity. Producers who deploy these systems first reduce per-unit production costs and create a data-driven quality assurance capability — a competitive distinction that becomes more valuable as buyer specifications tighten in pharmaceutical and electronics applications.

Drivers

Alumina Refining, Textile Expansion, and Water Infrastructure Investment Converge to Drive Industrial Caustic Soda Consumption

Alumina refining requires caustic soda as a direct process input in the Bayer process, where it dissolves aluminum oxide from bauxite ore. Expanding refining capacity across Southeast Asia and the Middle East creates sustained, high-volume demand that commodity chemical spot markets cannot absorb through short-term contracts alone — pushing refiners toward long-term flake supply agreements.

DCM Shriram expanded its Bharuch chlor-alkali complex to a combined production capacity of 2,225 TPD across 25 electrolysers and four production lines, making it one of India’s largest single-site membrane-cell chlor-alkali facilities. The company’s total installed caustic soda capacity has now reached 1 million metric tonnes per annum, strengthening its position among the country’s leading chlor-alkali producers by nameplate capacity.

Water treatment infrastructure investments in developing economies create recurring, government-backed demand for industrial alkaline chemicals. Additionally, the U.S. alone imports approximately 500,000 dmt per year of caustic soda — roughly 350,000 dmt to the West Coast and 150,000 dmt to the East Coast — confirming that even the world’s largest chemical-producing economies rely on import flows to balance domestic consumption gaps.

Restraints

Energy Cost Volatility and Environmental Compliance Obligations Constrain Chlor-Alkali Capacity Expansion

Chlor-alkali production is one of the most energy-intensive industrial chemical processes, with electricity accounting for a substantial share of total manufacturing cost. When energy prices spike — as they did across Europe and Asia through recent industrial cycles — producers face a cost structure that makes margin management extremely difficult without long-term power purchase agreements already in place.

U.S. Gulf Coast spot caustic soda exports were assessed at $390–$440/dmt FOB in week 40 of 2025, marking the third consecutive week of flat pricing. Flat export prices in a rising-cost environment compress producer margins directly — a condition that discourages discretionary capacity investment and signals to smaller operators that expansion carries elevated financial risk.

Environmental compliance regulations governing chlorine and mercury handling restrict where new chlor-alkali plants can be permitted and how existing plants can operate. China’s export of just 5–6% of its domestic caustic soda production to other regions — despite being the world’s largest producer — reflects in part the regulatory constraints that limit merchant export ambitions and keep production volumes tied to captive domestic applications.

Growth Factors

Emerging Market Chemical Hubs, Eco-Friendly Formulations, and Membrane Cell Technology Unlock New Revenue Streams

Chemical manufacturing hubs expanding across South and Southeast Asia and sub-Saharan Africa create geographically new demand centers that existing global suppliers cannot efficiently serve through long-distance export logistics alone. This geographic gap between supply infrastructure and emerging demand concentration opens opportunities for regional producers to establish captive customer relationships before global majors build local presence.

Middle East caustic soda demand rose 7% in 2025 while regional supply stayed stable. A demand increase of this scale against flat regional supply creates an immediate structural import gap — one that international exporters and local capacity investors can target with high confidence of off-take before additional regional production comes online.

Membrane-cell chlor-alkali technology improves energy efficiency and produces higher-purity output compared to legacy diaphragm and mercury-cell processes. DCM Shriram’s Bharuch facility raised capacity to 900 TPD after commissioning its new flaker unit, demonstrating that producers who invest in membrane-cell upgrades achieve both cost and quality advantages simultaneously — making them more competitive across multiple customer tiers at once.

Regional Analysis

Asia-Pacific Dominates the Caustic Soda Flakes Market with a Market Share of 44.4%, Valued at USD 1.1 Billion

Asia-Pacific accounts for 44.4% of global demand, valued at USD 1.1 billion in 2025. The region’s dominance reflects simultaneous scale across alumina refining, textile manufacturing, and chemical processing — three of the highest-volume application sectors. China, India, and Southeast Asian producers drive both consumption and expanding domestic production capacity, creating a self-reinforcing industrial ecosystem.

North America sustains strong industrial demand supported by active chemical manufacturing, water treatment infrastructure, and a structurally import-dependent West Coast market. The region’s imports of caustic soda, confirming a persistent supply gap between domestic production and consumption, position international exporters with favorable logistics as reliable long-term suppliers.

Europe’s caustic soda flakes market faces a dual constraint: legacy mercury-cell facilities facing mandatory phase-out under EU environmental directives, and high industrial energy costs following the post-2022 energy market disruption. Consequently, European producers are investing in membrane-cell transitions to restore cost competitiveness, while procurement teams increasingly source from export-oriented suppliers in the Middle East and Asia.

Latin America’s caustic soda flakes market centers on Brazil and Mexico, where active pulp and paper, textile, and agricultural chemical sectors create consistent base demand. However, regional production capacity remains limited relative to industrial consumption, making the region structurally dependent on imports from U.S. Gulf Coast exporters and increasingly from Asian producers offering competitive landed-cost pricing.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Olin Corporation positions itself as a vertically integrated chlor-alkali producer, operating both caustic soda and chlorine production at scale across North America and Europe. Its integrated model gives Olin a cost structure advantage over merchant importers — particularly in contract pricing negotiations with large chemical and water treatment buyers who prioritize supply reliability over spot market flexibility.

Westlake Corporation leverages its combined chlor-alkali and downstream chemical manufacturing footprint to create captive demand for its own caustic soda output. This internal consumption model insulates Westlake from external market price volatility and allows the company to optimize production volumes based on integrated margin performance rather than standalone caustic soda commodity pricing cycles.

Tata Chemicals Ltd operates across India, the United Kingdom, and Kenya — a geographic spread that gives it access to three structurally different demand environments simultaneously. Its presence in India positions Tata directly within the highest-growth caustic soda demand corridor, while its international operations provide margin diversification that pure-play domestic producers cannot replicate.

Occidental Petroleum Corporation applies its large-scale chemical processing infrastructure to compete in the chlor-alkali segment as part of a broader industrial chemicals portfolio. Its cost discipline and access to competitively priced feedstocks — particularly in the U.S. Gulf Coast — give it a structural export pricing advantage, directly supporting its participation in the growing international caustic soda trade flows.

Key Players

- Olin Corporation

- Westlake Corporation

- Tata Chemicals Ltd

- Occidental Petroleum Corporation

- Formosa Plastics Corporation

- Solvay

- Tosoh Corporation

- Hanwha Solutions Corporation

- Nirma Limited

- AGC, Inc.

- Dow

Recent Developments

- In 2025, Westlake Corporation approved the closure of one Lake Charles South diaphragm chlor-alkali unit with an annual capacity of 825M lb chlorine and 910M lb caustic soda; after the closure, Westlake expects global caustic soda capacity of 7,510M lb/year.

- In 2025, Tata Chemicals Ltd.’s report lists caustic soda under Other inorganic products and notes soda ash volume growth of 6% (+205 KT), but margin pressure from global oversupply and price decline of over 25%. Latest company updates include Mithapur reaching 1M tonnes soda ash production milestone in FY2025–26 and ₹515 crore (~$53.4 million) investment in a new IVSD facility; both are adjacent basic-chemicals developments.

Report Scope

Report Features Description Market Value (2025) USD 2.4 Billion Forecast Revenue (2035) USD 3.7 Billion CAGR (2026-2035) 4.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Flake, Granular, Pellet), By Purity Level (Lower Purity, Standard Purity, High Purity), By Application (Chemical Manufacturing, Pulp and Paper, Textile Processing, Water Treatment, Food Processing), By End Use (Construction, Automotive, Electronics, Pharmaceuticals, Agriculture) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Olin Corporation, Westlake Corporation, Tata Chemicals Ltd, Occidental Petroleum Corporation, Formosa Plastics Corporation, Solvay, Tosoh Corporation, Hanwha Solutions Corporation, Nirma Limited, AGC, Inc., Dow Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Olin Corporation

- Westlake Corporation

- Tata Chemicals Ltd

- Occidental Petroleum Corporation

- Formosa Plastics Corporation

- Solvay

- Tosoh Corporation

- Hanwha Solutions Corporation

- Nirma Limited

- AGC, Inc.

- Dow

Our Clients

- 186236

- May 2026