Quick Navigation

Report Overview

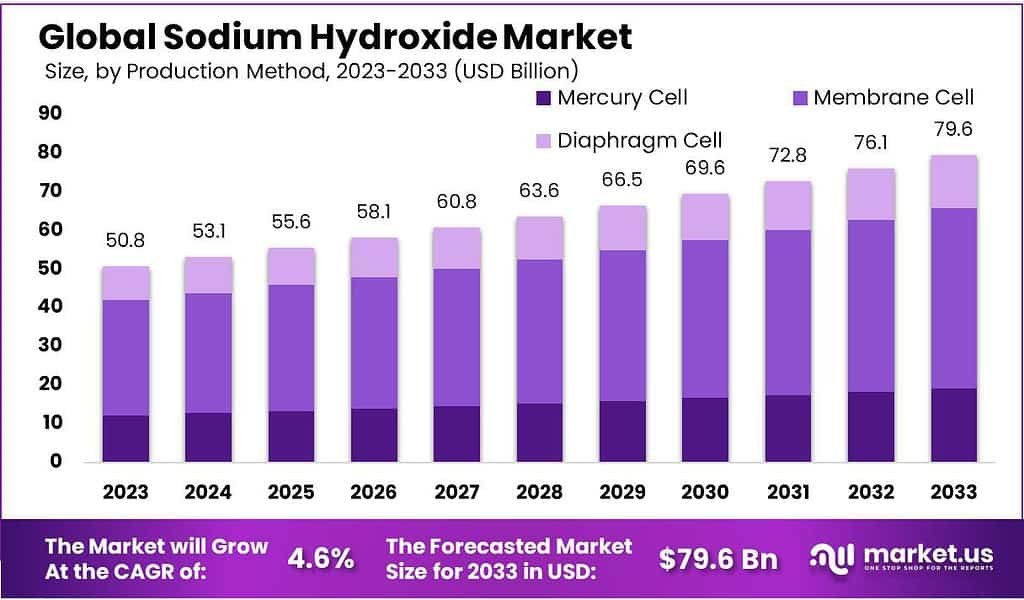

The global Sodium Hydroxide Market size is expected to be worth around USD 79.6 billion by 2033, from USD 50.8 billion in 2023, growing at a CAGR of 4.6% during the forecast period from 2023 to 2033.

The sodium hydroxide market refers to the global industry involved in the production, distribution, and consumption of sodium hydroxide, also known as caustic soda. This versatile chemical is essential in numerous industrial applications, including chemical manufacturing, pulp and paper processing, water treatment, and textile production.

The market covers various aspects such as production capacities, supply chain logistics, end-use industries, regulatory frameworks, and economic factors influencing the demand and supply dynamics. Key elements include the roles of major producers and consumers, import-export activities, technological advancements, and strategic initiatives like mergers, acquisitions, and government investments that shape the market’s growth and development.

The chemical manufacturing sector, which consumes 30% of the global sodium hydroxide supply, uses it in producing solvents, plastics, and pharmaceuticals. This makes it one of the largest consumers of sodium hydroxide. The pulp and paper industry, accounting for 20% of the demand, relies on sodium hydroxide for pulping and bleaching processes, highlighting its importance in producing paper products.

Water treatment facilities, representing 15% of the market, employ sodium hydroxide to adjust pH levels and remove heavy metals from water, ensuring safe and clean water supplies. The textile industry, which constitutes 10% of the consumption, applies sodium hydroxide in dyeing, bleaching, and fabric processing, underscoring its role in textile manufacturing.

Government regulations significantly influence the sodium hydroxide market. For instance, the European Union’s REACH regulation and the U.S. Environmental Protection Agency’s Clean Water Act promote the use of sodium hydroxide in environmental protection measures.

These regulations drive the demand for sodium hydroxide by ensuring industries comply with environmental standards. Additionally, in 2022, the U.S. government allocated USD 38 billion for water infrastructure improvements. This substantial investment further supports the sodium hydroxide market, as improved infrastructure requires chemicals like sodium hydroxide for maintenance and operation.

The global production capacity of sodium hydroxide reached 92 million metric tons in 2023. The Asia-Pacific region is the largest consumer, accounting for 45% of the market, followed by North America at 25% and Europe at 20%. The import-export landscape is robust, with the United States, China, and Germany being key exporters. In 2023, the United States exported approximately 1.2 million metric tons of sodium hydroxide, generating USD 1.5 billion in revenue. This highlights the significant role of international trade in the sodium hydroxide market.

Key Takeaways

- The sodium hydroxide market is to reach USD 79.6 billion by 2033, growing at 4.6% CAGR from USD 50.8 billion in 2023.

- Asia-Pacific leads with a 45% market share.

- The membrane Cell method dominates with over 58.6% market share.

- Liquid form holds a 62.7% market share due to ease of handling.

- High purity >90% sodium hydroxide captures 66.4% market share.

- Industrial Grade Accounts for 72.6% market share, widely used in various industries.

- Soaps and Detergent sector held a dominant position, capturing more than a 56.4% share.

By Production Method

In 2023, the Membrane Cell method held a dominant market position in the sodium hydroxide production landscape, capturing more than a 58.6% share. This method is favored for its environmental efficiency and ability to produce high-purity sodium hydroxide with lower energy consumption compared to other methods. Its widespread adoption is driven by stringent environmental regulations that discourage mercury and asbestos use, components common in older production technologies. As industries prioritize sustainability, the Membrane Cell method’s share is expected to grow further.

The Diaphragm Cell method, while less efficient than the Membrane Cell in terms of energy consumption and product purity, still plays a significant role in the market. It accounted for a considerable segment of the market, valued for its cost-effectiveness and reliability in various industrial applications. This method is particularly prevalent in regions with less stringent environmental regulations or with limited initial investment capital.

The Mercury Cell method, once a prominent production technique for sodium hydroxide, has declined usage, primarily due to environmental concerns over mercury emissions. This method now holds a smaller market share, reflecting the global shift towards more sustainable and environmentally friendly production processes. The decline is also influenced by international agreements and regulations aimed at phasing out technologies that use hazardous materials like mercury.

By Form

In 2023, the liquid form of sodium hydroxide held a dominant market position, capturing more than a 62.7% share. This form is preferred due to its ease of handling, transport, and application in various industrial processes. Liquid sodium hydroxide is particularly favored in industries where precise dosage and rapid integration of chemicals are required, such as in water treatment facilities and the chemical manufacturing sector. Its dominance in the market is further supported by the convenience it offers in terms of storage and use, reducing the need for complex handling equipment.

Solid sodium hydroxide, which includes flakes, pellets, and powder forms, accounted for the remainder of the market. This form is valued for its long shelf life and economic shipping costs, especially suitable for applications where storage conditions are controlled, and usage rates are not as immediate. Solid sodium hydroxide is commonly used in applications requiring gradual chemical release or where product purity is paramount, such as in the manufacture of paper and soap.

By Purity

In 2023, sodium hydroxide with a purity of above 90% held a dominant market position, capturing more than a 66.4% share. This high-purity sodium hydroxide is crucial for industries where product quality and process efficiency are paramount. Industries such as pharmaceuticals, food processing, and electronics manufacturing prefer this higher purity grade to ensure the safety, efficacy, and quality of their products. The demand in these sectors is particularly driven by stringent regulatory standards and the need for precision in manufacturing processes.

Conversely, sodium hydroxide with a purity of up to 90% is utilized in applications where such high levels of purity are not critical. This includes sectors like textiles and cleaning products, where sodium hydroxide is used in less sensitive processes. Although this segment holds a smaller share of the market, it remains significant due to its cost-effectiveness and suitability for a wide range of general industrial applications.

The distinction in market share between these two segments reflects their varied applications across different industries. Sodium hydroxide with a purity of above 90% dominates due to its essential role in high-stakes industries that require uncompromised quality and adherence to strict regulatory environments.

By Grade

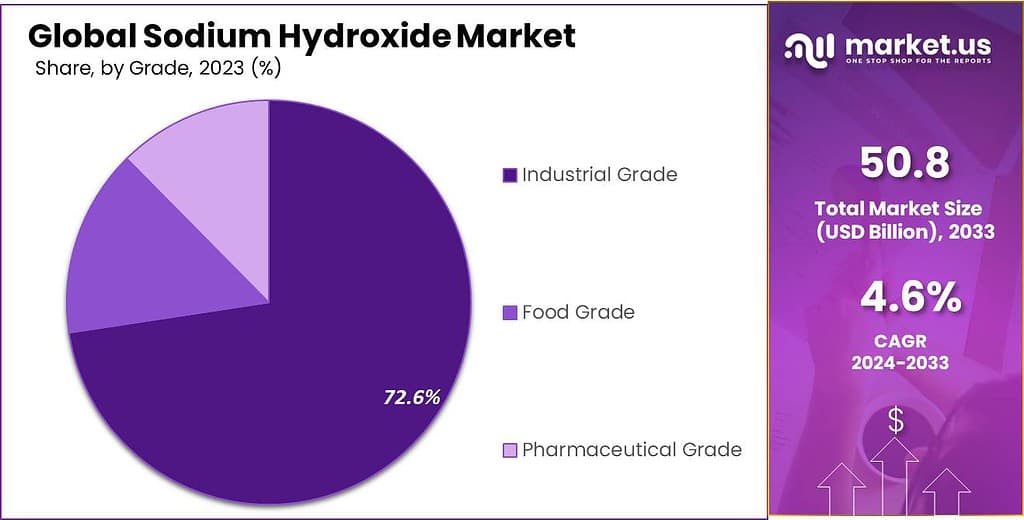

In 2023, industrial-grade sodium hydroxide held a dominant market position, capturing more than a 72.6% share. This grade is extensively used across a broad spectrum of industries, including chemical manufacturing, pulp and paper, and water treatment. Its widespread use is attributed to its effectiveness in processes such as cleaning, pH regulation, and chemical synthesis. The high demand for industrial-grade sodium hydroxide is driven by its robust performance in harsh industrial environments and its cost-effectiveness, making it a fundamental choice for large-scale industrial applications.

Food-grade sodium hydroxide, although holding a smaller market share, is critical in the food industry where it is used for cleaning and sanitation purposes, as well as in the processing of foods like olives and baked goods to adjust pH. This grade must meet stringent safety standards set by food safety authorities to ensure it is safe for use in food-related applications.

Pharmaceutical-grade sodium hydroxide also occupies a niche segment of the market. It is used in the pharmaceutical industry for drug formulation and manufacturing, where high purity and adherence to strict pharmaceutical regulations are mandatory. This grade is essential for ensuring the safety and efficacy of pharmaceutical products.

By End-Use

In 2023, the Soaps and Detergent sector held a dominant position in the sodium hydroxide market, capturing more than a 56.4% share. This substantial market share is due to the critical role sodium hydroxide plays in the production of soaps and detergents, where it is a key ingredient in the saponification process. This chemical reaction converts fats into soap and glycerol, meeting the ongoing demand for effective cleaning products in both domestic and industrial applications.

Other significant end-use sectors for sodium hydroxide include the Pulp and Paper industry, which utilizes it in the pulping process to break down wood and release fibers, essential for producing high-quality paper products. Although this sector holds a smaller market share compared to soaps and detergents, its role is indispensable.

The Water Treatment sector also relies heavily on sodium hydroxide, using it to adjust pH levels and remove impurities, which is crucial for maintaining safe water supplies. The demand in this segment is driven by increasing environmental regulations and the necessity for efficient water purification processes.

In the Textile industry, sodium hydroxide is employed in the mercerization of cotton, a process that strengthens fibers and enhances dye affinity, vital for producing high-grade textile products.

The Alumina sector uses sodium hydroxide in the Bayer process to produce alumina from bauxite ore. This segment leverages sodium hydroxide’s properties to extract pure aluminum hydroxide from bauxite, which is a critical step in aluminum production.

Additionally, in the Pharmaceuticals industry, sodium hydroxide is utilized to maintain and control pH levels during the manufacturing of medicines, ensuring product stability and efficacy.

Key Market Segments

By Production Method

- Mercury Cell

- Membrane Cell

- Diaphragm Cell

By Form

- Solid

- Liquid

By Purity

- Upto 90%

- Above 90%

By Grade

- Industrial Grade

- Food Grade

- Pharmaceutical Grade

By End-Use

- Alumina

- Textile

- Pulp and Paper

- Soaps and Detergent

- Dyes and Inks

- Pesticides

- Pharmaceuticals

- Water Treatment

- Others

Driving Factors

Major Driving Factor for the Sodium Hydroxide Market: Water Treatment

The water treatment sector stands out as a primary driving force behind the demand for sodium hydroxide, accounting for significant market growth. The escalating need for clean water and compliance with strict environmental standards are central to this trend. Sodium hydroxide plays a crucial role in water treatment processes, where it is used to adjust pH levels and neutralize acidic or alkaline contaminants. This ensures the provision of safe and potable water supplies, which is becoming increasingly critical amidst global concerns about water quality and sustainability.

In response to heightened urbanization and the imperative for effective wastewater management, the demand for sodium hydroxide in water treatment applications is projected to grow robustly. This growth is supported by the ongoing global push towards sustainable practices and the implementation of stringent environmental regulations aimed at enhancing water quality. For instance, in the European market, there is a marked increase in applications related to water treatment due to rising concerns about water purity and the implementation of eco-friendly processes.

Moreover, the market’s growth is further buoyed by strategic collaborations and advancements in manufacturing processes, which enhance the efficiency of production methods and align with the shift towards sustainable and eco-friendly products. These innovations are crucial in maintaining sodium hydroxide’s essential role in the burgeoning water treatment industry and supporting its demand trajectory in the coming years.

The importance of sodium hydroxide in this sector is underlined by its ability to meet the stringent regulatory standards imposed on water treatment processes, thereby affirming its status as a key chemical in addressing global environmental challenges.

Restraining Factors

Regulatory and Safety Challenges

One of the primary restraining factors for the growth of the sodium hydroxide market is its hazardous nature, which necessitates stringent regulations on its storage, usage, and disposal. Sodium hydroxide, also known as caustic soda, is highly corrosive, posing significant safety risks if not handled properly. This characteristic leads to comprehensive regulatory scrutiny, which can slow down manufacturing processes, increase operational costs, and limit the flexibility in the usage and disposal of the chemical.

These safety and regulatory challenges are not only a concern for producers but also for users across various industries, requiring them to implement rigorous safety protocols and to invest in specialized equipment to handle the chemical safely. The need for such precautions can deter new entrants and can lead to increased costs for existing players, ultimately restraining market growth.

Moreover, the hazardous nature of sodium hydroxide also impacts its transportation. Transporting caustic soda requires adherence to specific regulations to prevent accidents, which can be costly and logistically challenging. These transportation issues add another layer of complexity and cost, which can act as a barrier to market growth.

Additionally, the environmental impact of improper handling of sodium hydroxide, such as potential harm to aquatic life and water quality, further necessitates stringent environmental compliance. This not only adds to operational challenges but also the potential legal and reputational risks industries might face due to non-compliance.

Growth Opportunities

Expansion in Emerging Markets

A significant growth opportunity for the sodium hydroxide market lies in the rapid industrialization of emerging economies. These regions are experiencing a surge in manufacturing activities and infrastructure development, which in turn boosts the demand for chemicals and materials, including sodium hydroxide. As industries such as pulp and paper, chemical manufacturing, and water treatment expand, the requirement for sodium hydroxide amplifiesdue to its essential role in various industrial processes.

Particularly, the Asia-Pacific region, led by countries like India and China, is witnessing robust growth in the sodium hydroxide market. India, for example, is becoming a hub for textile and chemical production, which heavily relies on sodium hydroxide. The country’s market is expected to capture a significant share in the South Asia Pacific region, driven by its strengths in textile production and an expanding chemical sector.

The ongoing developments in infrastructure and an increase in foreign direct investments are pivotal in this growth. Moreover, the demand in India is not just for domestic consumption; it also includes export activities, particularly in regions like Africa, where the chemical market is still developing.

Similarly, in China, the demand for sodium hydroxide is bolstered by strong domestic production capacities and substantial industrial manufacturing. The country’s large-scale industrial activities support not only local demand but also contribute significantly to the Asia Pacific market size.

The expansion in these markets is further facilitated by the globalization of trade and the strategic expansion of key market players in these regions. Companies are increasingly setting up manufacturing facilities and distribution centers in emerging economies to tap into local markets and reduce logistical costs.

Thus, the combination of industrial growth, strategic company expansions, and the inherent demand for sodium hydroxide in critical industries presents a lucrative growth trajectory for the sodium hydroxide market in emerging economies, promising continued expansion and profitability in the coming years.

Latest Trends

Increasing Application in Alumina Production

One of the most prominent trends in the sodium hydroxide market is its increasing application in alumina production, particularly as the demand for aluminum continues to rise globally. This trend is largely driven by the burgeoning automotive and packaging industries, which extensively use aluminum due to its lightweight and recyclable properties.

The demand for sodium hydroxide in alumina refining is critical as it is used to dissolve bauxite ore, the primary raw material for aluminum production. This process, known as the Bayer process, separates alumina from bauxite, with sodium hydroxide playing a key role in the extraction. The increasing utilization of aluminum in various industries, including automotive, packaging, and construction, significantly propels the demand for sodium hydroxide.

Additionally, the global emphasis on sustainability and the shift towards lightweight materials for better fuel efficiency in vehicles further boost the aluminum industry, subsequently increasing the demand for sodium hydroxide. Regions like Asia Pacific, especially China and India, are leading this demand surge due to rapid industrialization and urbanization, which in turn fuels the growth of the sodium hydroxide market in these areas.

Moreover, advancements in production technologies, such as improvements in the efficiency of the Bayer process, are enhancing the overall market dynamics. These technological advancements not only improve the efficiency of sodium hydroxide use but also aim to reduce the environmental impact associated with its production and use in industrial processes.

Regional Analysis

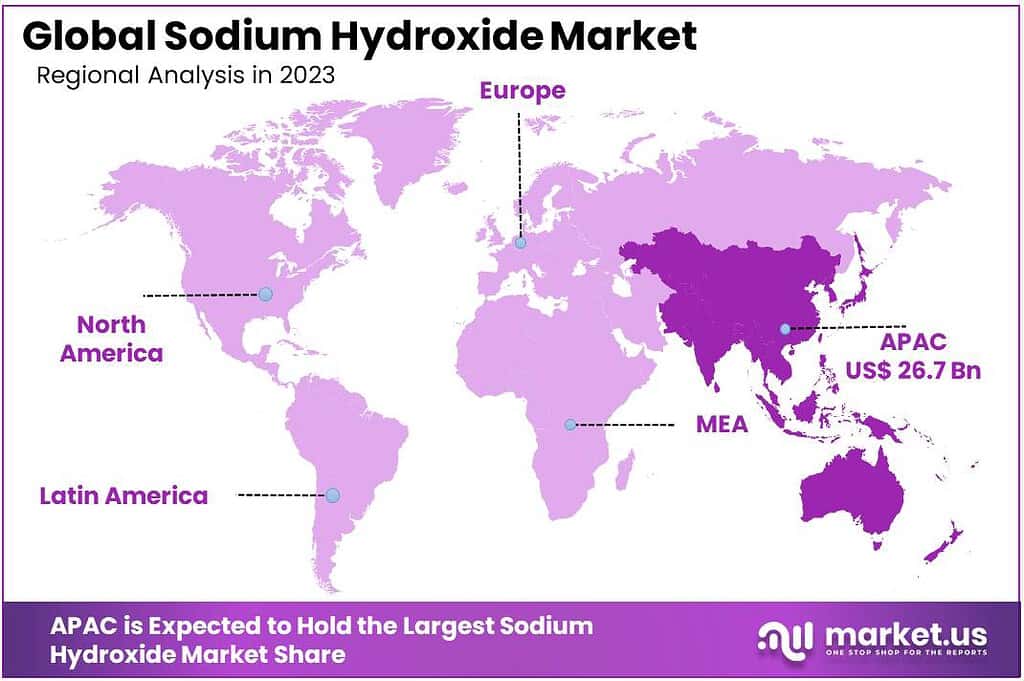

In 2023, the sodium hydroxide market demonstrated significant regional variations in demand and consumption. The Asia Pacific (APAC) region dominated the market, capturing a substantial 52.6% share, valued at approximately USD 26.72 billion. This dominance is attributed to the robust industrial base in countries like China, India, and Japan, where sodium hydroxide is heavily used in the manufacturing of soaps, detergents, textiles, and paper products. The rapid industrialization and urbanization in these countries further bolster the demand.

North America is another significant region in the sodium hydroxide market. The region benefits from a well-established chemical industry, with the United States being a major contributor. In North America, the demand is driven by the extensive use of sodium hydroxide in water treatment, pharmaceuticals, and the production of alumina. The region’s market share is supported by stringent environmental regulations requiring effective water treatment solutions.

Europe holds a considerable share in the sodium hydroxide market, driven by its robust chemical and pharmaceutical industries. Countries like Germany, France, and the United Kingdom lead in the consumption of sodium hydroxide, especially in the pulp and paper industry and for the manufacturing of various chemical products. The region also focuses on sustainable industrial practices, which drives the demand for efficient chemical processing agents.

The Middle East & Africa region shows a growing demand for sodium hydroxide, primarily due to the expanding water treatment and textile industries. The increasing industrial activities and the need for effective water purification methods contribute to the steady market growth in this region.

Latin America, though holding a smaller share compared to APAC, North America, and Europe, shows potential growth driven by the burgeoning industrial sector in countries like Brazil and Mexico. The increasing use of sodium hydroxide in local manufacturing and water treatment facilities is expected to drive the market in the coming years.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The sodium hydroxide market is dominated by several key players who contribute significantly to its growth and dynamics. Leading the market is Dow Chemical Company, which has a robust production capacity and extensive distribution networks globally. Olin Corporation, another major player, benefits from its comprehensive portfolio of chlor-alkali products, positioning itself strongly in the market. Occidental Petroleum Corporation also holds a significant share, leveraging its integrated chemical operations to drive efficiency and output.

INOVYN, a subsidiary of INEOS, is a key player in Europe, focusing on innovation and sustainability in chemical production. BASF SE and Solvay S.A. are prominent in the European market, with BASF being a global leader in diversified chemical products and Solvay focusing on advanced materials and specialty chemicals. Tata Chemicals Limited represents a strong presence in the Indian market, emphasizing sustainable practices and diversification.

In the Asian market, Formosa Plastics Corporation and Hanwha Chemical Corporation are noteworthy. Formosa Plastics, based in Taiwan, is a major producer with significant market influence in Asia, while Hanwha Chemical, based in South Korea, focuses on expanding its global footprint. AkzoNobel N.V., PPG Industries, Inc., and Tosoh Corporation are also key players, with AkzoNobel and PPG Industries having a strong presence in the paints and coatings sector, and Tosoh Corporation being influential in the Japanese market.

Shin-Etsu Chemical Co., Ltd., FMC Corporation, and Westlake Chemical Corporation round out the list of major players. Shin-Etsu, based in Japan, is renowned for its high-quality chemical products, FMC Corporation focuses on agricultural solutions and specialty chemicals, and Westlake Chemical, an American company, emphasizes performance and sustainability in its operations. These companies collectively drive innovation, sustainability, and growth in the global sodium hydroxide market, adapting to market demands and regulatory changes to maintain their competitive edge.

Market Key Players

- Dow Chemical Company

- Olin Corporation

- Occidental Petroleum Corporation

- INOVYN

- BASF SE

- Solvay S.A.

- Tata Chemicals Limited

- Formosa Plastics Corporation

- Hanwha Chemical Corporation

- AkzoNobel N.V.

- PPG Industries, Inc.

- Tosoh Corporation

- Shin-Etsu Chemical Co., Ltd.

- FMC Corporation

- Westlake Chemical Corporation

Recent Development

In January 2023, Dow increased production by 5% at its Freeport, Texas facility, reaching 1.1 million metric tons annually.

In January 2023, Olin reported a monthly production of 95,000 metric tons. By March, this increased to 100,000 metric tons, driven by high demand from the pulp and paper and water treatment sectors.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 50.8 Bn |

| Forecast Revenue (2033) | US$ 79.6 Bn |

| CAGR (2024-2033) | 4.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Production Method(Mercury Cell, Membrane Cell, Diaphragm Cell), By Form(Solid, Liquid), By Purity(Upto 90%, Above 90%), By Grade(Industrial Grade, Food Grade, Pharmaceutical Grade), By End-Use(Alumina, Textile, Pulp and Paper, Soaps and Detergent, Dyes and Inks, Pesticides, Pharmaceuticals, Water Treatment, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Dow Chemical Company, Olin Corporation, Occidental Petroleum Corporation, INOVYN, BASF SE, Solvay S.A., Tata Chemicals Limited, Formosa Plastics Corporation, Hanwha Chemical Corporation, AkzoNobel N.V., PPG Industries, Inc., Tosoh Corporation, Shin-Etsu Chemical Co., Ltd., FMC Corporation, Westlake Chemical Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Sodium Hydroxide Market size is expected to be worth around USD 79.6 billion by 2033, from USD 50.8 billion in 2023

Dow Chemical Company, Olin Corporation, Occidental Petroleum Corporation, INOVYN, BASF SE, Solvay S.A., Tata Chemicals Limited, Formosa Plastics Corporation, Hanwha Chemical Corporation, AkzoNobel N.V., PPG Industries, Inc., Tosoh Corporation, Shin-Etsu Chemical Co., Ltd., FMC Corporation, Westlake Chemical Corporation