Quick Navigation

Report Overview

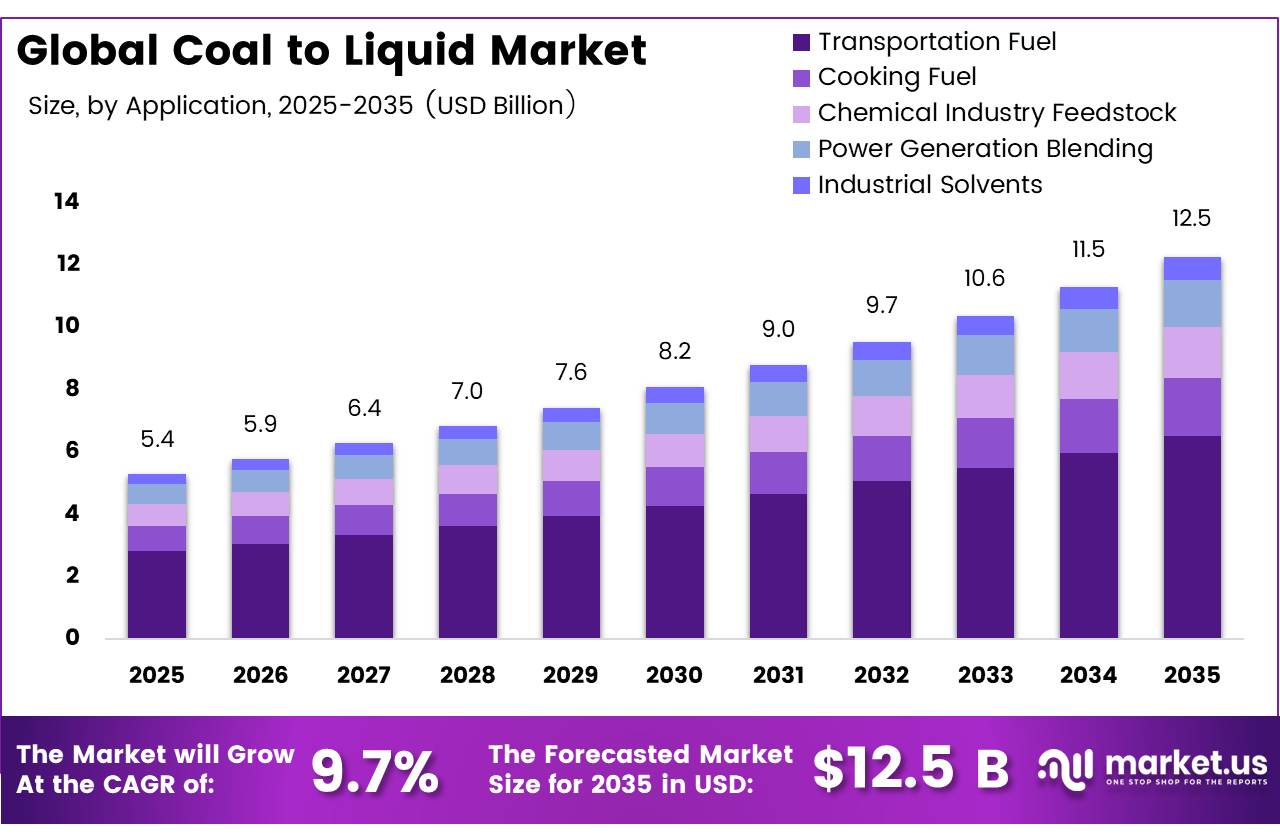

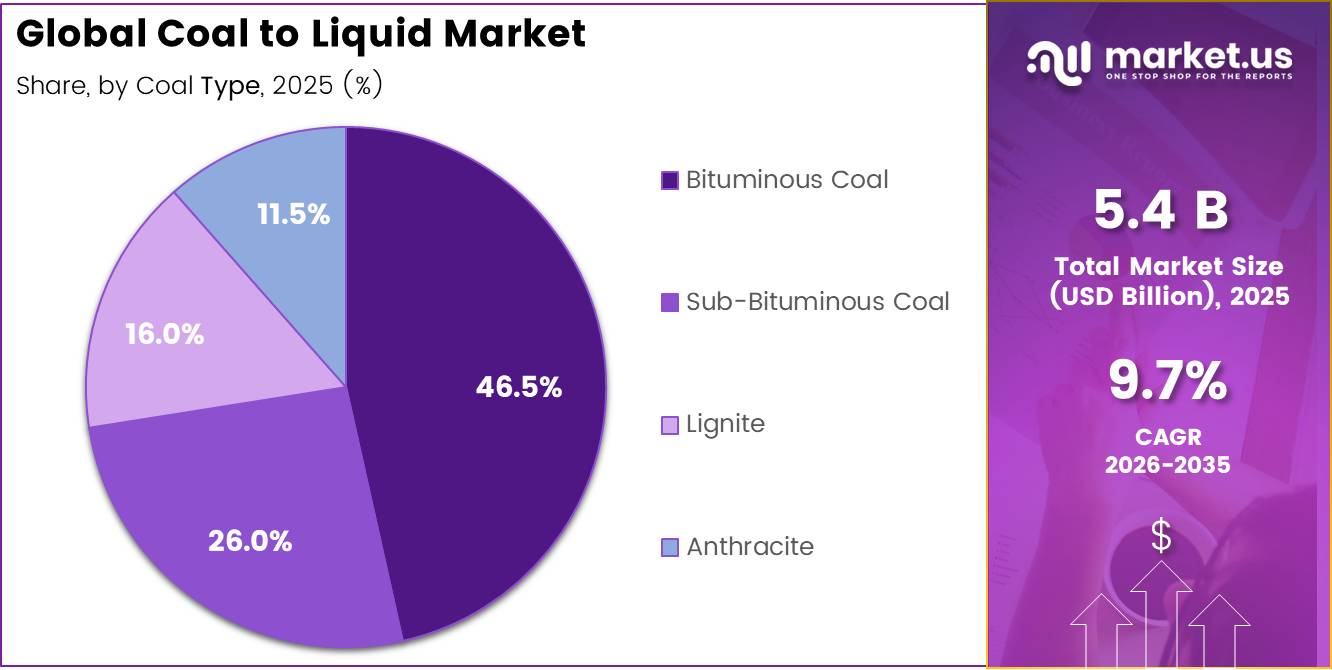

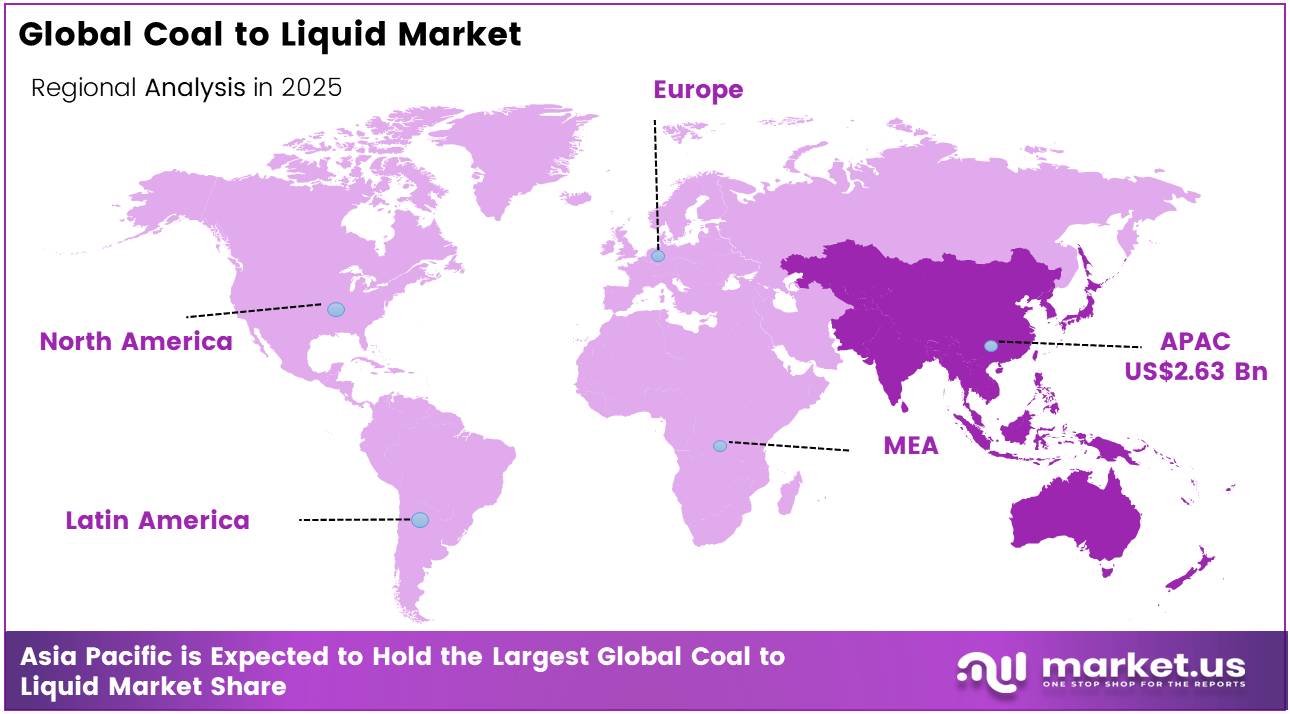

In 2025, the Global Coal to Liquid Market was valued at US$5.4 billion, and between 2026 and 2035, this market is projected to grow at a CAGR of 9.7%, reaching about US$12.5 billion by 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 48.5% share, holding USD 2.63 Billion revenue.

Coal-to-liquid (CTL) technology converts coal into synthetic diesel, gasoline, aviation fuel and chemical feedstocks through coal gasification and Fischer–Tropsch synthesis. The industry remains strategically relevant for coal-rich economies seeking domestic fuel production, although high capital expenditure, intensive energy use and lifecycle emissions continue to limit new commercial projects.

- In April 2024, according to the U.S. Department of Energy, existing point-source systems were generally capable of capturing at least 90% of carbon dioxide, while federal development programs targeted capture rates of at least 95%. This creates opportunities to integrate carbon capture with CTL facilities and lower process-related emissions.

In September 2024, according to the U.S. Department of Energy, approximately USD 138 million had been committed since 2021 to projects advancing cleaner hydrogen production and hydrogen-turbine technologies. Cleaner hydrogen can support syngas conditioning and improve the carbon performance of future synthetic-fuel plants.

In September 2024, according to the U.S. Department of Energy, approximately USD 138 million had been committed since 2021 to projects advancing cleaner hydrogen production and hydrogen-turbine technologies. Cleaner hydrogen can support syngas conditioning and improve the carbon performance of future synthetic-fuel plants.

In January 2025, according to the U.S. Department of Energy, the United States operated 18 commercial-scale carbon capture and storage projects out of approximately 50 operating worldwide. Future CTL opportunities are therefore expected in carbon-managed fuels, waste-and-coal co-gasification, higher-efficiency catalysts and lower-emission aviation-fuel production.

Key Takeaways

- The global Coal to Liquid market was valued at USD 5.4 billion in 2025.

- The global market is projected to grow at a CAGR of 9.7% and is estimated to reach USD 12.5 billion by 2035.

- On the basis of Technology, the indirect coal Liquefaction (ICL) dominated the market, constituting 54.5% of the total market share.

- Based on the Product type, the Diesel dominated the Coal to Liquid market, with a substantial market share of around 42.5%.

- Based on the Coal type, Bituminous Coal led the market, comprising 46.5% of the total market.

- Among the Application, the Transportation Fuel held a major share in the Coal to Liquid market, 52% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the Coal to Liquid market, accounting for 62.3% of the total global consumption.

Technology Analysis

Indirect Coal Liquefaction (ICL) represents dominant Segment in the Market.

ICL technology occupies the largest share in the CTL market, having captured a share of 54.5%, owing to its economic feasibility, established performance, and higher quality of fuel products compared to other technologies. Indirect coal liquefaction (ICL) accounts for the largest share of the global coal-to-liquids (CTL) market because it is the most commercially proven and widely deployed technology for producing high-quality transportation fuels at a large industrial scale. Unlike direct coal liquefaction, ICL converts coal into synthesis gas (syngas) and then into liquid fuels through the Fischer Tropsch process, allowing better control over fuel quality and product composition.

The dominance of ICL is strongly supported by its large-scale adoption in coal-rich countries, especially China and South Africa. China consumed nearly 4.6 billion tons of thermal coal in 2024, representing around 55% of global thermal coal consumption, making coal a critical feedstock for its energy and chemical industries. The technology also integrates well with existing refining, storage, and pipeline infrastructure, reducing overall system integration costs compared with alternative pathways.

In addition, the International Energy Agency (IEA) identifies coal-to-liquids and coal-to-chemicals as major contributors to the growth of non-power coal demand in China, reflecting continued investment in large integrated CTL facilities based primarily on indirect coal liquefaction technology. These operational, economic, and infrastructure advantages continue to position ICL as the leading technology in the global CTL market.

Product Type Analysis

Diesel a significant type.

Diesel is the largest product segment in the global coal-to-liquid (CTL) market, accounting for approximately 42.5% of total output. Its leading position is driven by its strong demand across the transportation, mining, construction, agriculture, and industrial sectors, where diesel remains the primary fuel for heavy-duty vehicles and equipment. According to the International Energy Agency (IEA), the transport sector accounts for nearly 30% of global final energy demand, while road transport alone consumes around 90% of transport energy.

This creates a stable and long-term requirement for middle-distillate fuels such as diesel. In addition, the U.S. Energy Information Administration (EIA) reported that global liquid fuel consumption exceeded 102 million barrels per day in 2024, with diesel representing one of the most widely used fuel categories for commercial and industrial operations.

CTL-derived diesel further strengthens its market position because it contains ultra-low sulfur levels, burns more efficiently, and produces lower emissions than conventional diesel. These properties help industries comply with increasingly strict environmental regulations without requiring modifications to existing diesel engines, fuel storage systems, or distribution infrastructure. The ability to use CTL diesel directly in current fleets reduces investment costs and supports faster adoption, particularly in regions seeking greater energy security and fuel diversification.

Coal Type Analysis

Bituminous Coal Are the Most Widely Used Type.

Bituminous coal holds 46.5% of the market share making it the largest share of the global coal-to-liquid (CTL) market because it offers the best balance of fuel quality, conversion efficiency, and commercial availability. Its relatively high carbon content, moderate volatile matter, and favorable hydrogen-to-carbon ratio make it an ideal feedstock for both indirect liquefactions through Fischer–Tropsch synthesis and direct coal liquefaction technologies. The widespread global production and trade of bituminous coal also ensure a stable raw material supply for large-scale CTL projects.

According to the U.S. Energy Information Administration (EIA), the average price of bituminous coal was USD 86.72 per short ton in 2024, reflecting its strong commercial presence in international markets.

The dominance of bituminous coal is further supported by demand patterns in the Asia-Pacific region, where most commercial CTL facilities are located. According to the International Energy Agency (IEA), China and India together accounted for 71% of global coal consumption in 2024, while the Asia-Pacific region represented 77% of total global coal demand. These countries continue to invest in CTL technology to strengthen energy security and reduce dependence on imported crude oil.

Application Analysis

Transportation Fuel Held a Major Share of the Coal to Liquid Market.

Transportation fuel remains the largest application segment with a market share of 52%, because of the continued high demand for liquid fuels across the transport sector.

According to the International Energy Agency (IEA), transportation accounts for nearly 30% of global final energy consumption, while road transport represents around 90% of domestic transport energy use. Heavy-duty trucks, aviation, and maritime transport continue to rely on liquid fuels as large-scale electrification in these sectors is still limited. Although electric vehicles reduced oil demand by more than 1.3 million barrels per day in 2024, this has had only a limited impact compared with global oil demand exceeding 100 million barrels per day.

CTL fuels have properties similar to conventional diesel and jet fuel, allowing them to be used in existing engines, storage facilities, and fuel distribution networks without major infrastructure changes. This compatibility, combined with the need for reliable fuel supply, supports the strong position of transportation fuel in the CTL market. The segment is particularly important in coal-rich countries seeking to improve energy security, reduce dependence on imported crude oil, and make better use of domestic coal resources.

Key Market Segments

By Technology

- Indirect Coal Liquefaction (ICL)

- Direct Coal Liquefaction (DCL)

- Hybrid Processes

By Product Type

- Diesel

- Gasoline

- Jet Fuel

- Lubricants

- Chemical Feedstock

- LPG (Liquefied Petroleum Gas)

- Others

By Coal Type

- Bituminous Coal

- Sub-Bituminous Coal

- Lignite

- Anthracite

By Application

- Transportation Fuel

- Road Transportation

- Aviation

- Marine

- Cooking Fuel

- Chemical Industry Feedstock

- Power Generation Blending

- Industrial Solvents

- Others

Drivers

Energy security and liquid fuel diversification via domestic coal

Countries like China, India and South Africa collectively hold many tens of billions of tons of recoverable coal reserves, giving them domestic feedstock horizons measured in decades at current extraction rates; China alone has built multiple large CTL complexes with nameplate capacities in the millions of tons per year range to hedge against crude‑import volatility and maritime chokepoint risks. In an era where oil‑price swings of USD 20–40 per barrel within 12–24 months remain plausible due to OPEC+ policy, geopolitical shocks or demand surprises, CTL offers governments a way to smooth import bills and guarantee priority supply for critical sectors such as aviation, mining and defense, even if levelized costs per barrel are above mid‑cycle crude in purely commercial terms.

Strategically, this driver shifts CTL project sponsoring from purely corporate to state‑linked and policy‑anchored, with financing structures that often blend commercial debt, policy banks and fiscal incentives; it supports long‑dated offtake contracts and capacity utilization guarantees that de‑risk investments and add roughly 2–2.5 percentage points of CAGR on top of a baseline where coal is used only for power and CTL is treated as a niche technology without explicit energy‑security framing.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy security and liquid fuel diversification via domestic coal | +2.3% | China core, India, South Africa, U.S. | Medium term (2-4 years) |

| Rising jet fuel, diesel and petrochemicals demand in hard-to-abate sectors | +2.0% | APAC corridors, Middle East, Africa | Long term (≥ 4 years) |

| Technology efficiency gains in direct and indirect liquefaction | +1.7% | China, South Africa, R&D hubs in U.S., EU, Japan | Long term (≥ 4 years) |

| Integration of CCS and low-carbon hydrogen to decarbonize CTL plants | +1.6% | China, Middle East, U.S., EU demonstration sites | Long term (≥ 4 years) |

| Utilization of stranded, low-grade and lignite coal resources | +1.5% | China inland, India eastern coal belts, Indonesia, Mongolia | Medium term (2-4 years) |

| Strategic industrial policy and state-backed mega-projects | +1.4% | China core, Middle East, select African states | Medium term (2-4 years) |

Restraints

Very high CTL capex intensity and project financing risk

Historical experiences in China, South Africa and U.S. pilot projects show that CTL construction periods can run 5–7 years from FID to full ramp‑up, during which time interest during construction accumulates, debt‑service windows approach and macro conditions can change dramatically, including oil prices, carbon policy and domestic coal regulation. Financiers therefore demand high projected IRRs and often require sovereign backing, offtake guarantees or regulated‑tariff style arrangements; absent such structures, CTL projects struggle to achieve financial close, and even with support they are exposed to cost‑overrun risks that can inflate capex per installed barrel by double‑digit percentages, as has been seen in analogous mega‑projects.

Strategically, this restraint means that only a subset of potential CTL concepts progress beyond feasibility: project sponsors must be large, often state‑linked entities with strong balance sheets, and must be willing to concentrate risk in a few mega‑assets, limiting global project count and slowing geographic diversification; the resulting capex bottleneck and risk‑averse lending environment plausibly remove around 2–2.5 percentage points from otherwise attainable CAGR by keeping many technically feasible CTL projects on the drawing board rather than in execution.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Very high CTL capex intensity and project financing risk | -2.4% | China core, South Africa, India, U.S. | Long term (≥ 4 years) |

| Carbon- and water-intensive emissions profile under tightening climate policy | -2.2% | EU, U.S., OECD Asia, climate-active EMs | Long term (≥ 4 years) |

| Coal mining, ash and CCR disposal environmental liabilities | -1.9% | U.S., China, India, South Africa | Medium term (2-4 years) |

| Crude oil price volatility and refining overcapacity risk | -1.8% | Global, with high exposure in import-dependent CTL adopters | Medium term (2-4 years) |

| Technology, feedstock and O&M complexity versus competing low-carbon fuels | -1.6% | China, South Africa, R&D hubs | Long term (≥ 4 years) |

| ESG, investor and offtaker decarbonization commitments constraining CTL pipelines | -1.5% | EU, U.S., Japan, global capital markets | Medium term (2-4 years) |

Opportunity

CTL–biomass co-feed for low-carbon synfuels

CTL–biomass co‑feed for low‑carbon synfuels is a genuine future opportunity rather than a current driver because, although technical pathways for co‑gasifying coal and biomass exist, very few commercial CTL plants today operate at meaningful biomass shares or claim low‑carbon fuel attributes, leaving a large decarbonization and policy‑driven TAM untapped. Co‑feeding 10–40% biomass (by energy) into CTL gasifiers and integrating high‑rate CO₂ capture could, on a lifecycle basis, push synthetic diesel or jet fuels toward parity with or even below conventional fuels in net GHG emissions, positioning such fuels as “transition‑aligned” in markets where sustainable aviation fuel (SAF) and low‑carbon fuel standards start to bite but pure power‑to‑liquids or advanced biofuels remain constrained by cost and feedstock.

Large coal‑rich countries like China and India also have significant agricultural and forestry residues currently underutilized or openly burned, representing tens of millions of tons per year of potential biomass feed, while South Africa and the U.S. possess forestry and energy‑crop potential near existing coal basins. If CTL operators can technically validate stable co‑feeding at, say, 20–30% biomass shares, secure biomass supply chains within 100–200 km radii of plants, and demonstrate lifecycle emissions reductions that qualify for SAF mandates or low‑carbon fuel credits, they could access premium pricing, long‑term offtake into aviation and heavy transport, and potentially green‑finance instruments that are currently unavailable to unabated CTL.

Strategically, this would reframe selected CTL assets as “coal‑biomass‑to‑liquids” platforms with both security and climate roles, expanding their regulatory headroom and monetizable volumes; even if only a fraction of existing and planned CTL capacity adopts co‑feed configurations by the early‑to‑mid 2030s, the associated premium offtake and utilization uplift could realistically add around 2 percentage points of CAGR upside above a baseline that treats CTL as purely coal‑based and largely excluded from transition‑aligned fuel pools.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| CTL–biomass co-feed for low-carbon synfuels | +2.1% | China, India, South Africa, U.S. | Long term (≥ 4 years) |

| CTL–H₂ hubs with shared gasification and blue hydrogen | +1.9% | China inland, Middle East, U.S. Gulf, South Africa | Medium term (2-4 years) |

| Aviation and mining offtake-backed CTL SAF/diesel platforms | +1.8% | APAC corridors, Africa, Middle East | Medium term (2-4 years) |

| Brownfield coal-chemicals integration and high-value liquids | +1.7% | China coal-chem clusters, South Africa, India | Medium term (2-4 years) |

| CTL technology/IP licensing and modular blocks export | +1.5% | China, South Africa to EM importers | Long term (≥ 4 years) |

| Consolidation and M&A roll-ups into CTL–transition energy platforms | +1.4% | China, global energy majors, PE infrastructure | Medium term (2-4 years) |

Challenges

High opex sensitivity to coal, power and water inputs

High opex sensitivity to coal, power and water inputs is a persistent challenge because CTL’s unit economics depend heavily on feedstock and utilities costs that can move by double‑digit percentages over a typical 20‑ to 30‑year project life, compressing margins and forcing continuous cost‑management without shutting existing plants. Coal prices at mine mouth, which can represent 40–60% of CTL operating expenditure depending on process configuration, are exposed to domestic policy changes, rail tariffs, labor costs and, in some markets, export dynamics; even a USD 10–15 per ton swing in delivered coal costs can translate into several dollars per barrel change in synthetic‑fuel cash costs.

Strategically, operators must hedge coal procurement, secure long‑term power and water agreements, and invest in efficiency upgrades and process optimization to defend margins, but the residual volatility still forces cautious growth planning and higher hurdle rates; across the global CTL project set, this ongoing opex pressure likely subtracts around 1–1.5 percentage points from maximum feasible CAGR by limiting the number of marginal projects that can clear investment committees under realistic fuel and utility price scenarios.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| High opex sensitivity to coal, power and water inputs | -1.4% | China core, South Africa, India inland, U.S. | Medium term (2-4 years) |

| Operational complexity of large integrated CTL complexes | -1.3% | China, South Africa, U.S. pilots | Long term (≥ 4 years) |

| Regulatory uncertainty on carbon, ash and local pollution | -1.2% | EU, U.S., OECD Asia, emerging climate actors | Medium term (2-4 years) |

| Supply chain and EPC execution risk for mega-scale CTL projects | -1.1% | China inland, India, Middle East, Africa | Medium term (2-4 years) |

| Talent and know-how concentration in a few CTL clusters | -1.0% | China, South Africa, limited OECD centers | Long term (≥ 4 years) |

| Competitive pressure from cheaper renewables and alternative low-carbon fuels | -0.9% | Global, especially EU, U.S., advanced APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Coal to Liquid Manufacturing.

Geopolitical tensions are increasing costs and supply risks across the global coal-to-liquids (CTL) market. Global coal consumption reached a record 8,771 million tonnes in 2024, rising about 1% from the previous year, keeping demand high and supporting coal prices. This has increased feedstock costs for CTL plants, particularly those using high-grade coal for gasification. At the same time, disruptions in global oil markets, including the temporary closure of the Strait of Hormuz through late May 2026, pushed Brent crude prices to around USD 106 per barrel, improving the economic appeal of CTL fuels compared with conventional petroleum products. However, higher oil prices have also raised the cost of petroleum-based chemicals, auxiliary fuels, and other operating inputs. Although coal prices remained more stable than oil between 2022 and 2024, regional price increases, policy uncertainty, and conflict-related supply disruptions have encouraged CTL producers to maintain larger inventories and expand hedging strategies, increasing overall production costs.

Geopolitical disruptions are also affecting CTL transportation and project execution. The Red Sea shipping crisis and longer trade routes have increased freight costs and delivery times for coal, catalysts, process equipment, and synthetic fuels. Freight rates from Shanghai to Europe more than tripled after December 2023, significantly raising export costs for CTL products. Rerouted shipping routes have extended transit times by 7–10 days, while higher marine insurance costs and port congestion have increased working capital requirements. In addition, higher tariffs on industrial equipment and fuel imports in some regions have raised project capital costs. These factors are encouraging CTL developers to prioritize domestic coal sourcing, regional supply chains, and local fuel distribution to reduce exposure to global trade disruptions and improve cost stability.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Coal to Liquid Market.

Asia Pacific holds the lead in the global CTL market with a share of 48.50%, backed by an abundance of coal reserves, government-supported liquefaction capacity, and increasing dependence on imported crude oil. According to the INTERNATIONAL ENERGY AGENCY’s Global Energy Review 2025, the proportion of global coal consumption in Developing Asia rose to about four-fifths in 2024 from less than two-fifths in 2000. China alone produced 4,666 million tonnes of coal in 2024, according to the INTERNATIONAL ENERGY AGENCY Coal Mid-Year Update 2025, ensuring sufficient feedstock volumes for the nation’s large-scale CTL projects. China, India, and ASEAN nations cumulatively made up roughly 77% of global coal consumption in 2024, underscoring the pivotal status of Asia Pacific at each level of the CTL chain.

Europe is the fastest growing regional segment, influenced by revised focus on energy security and synthetic fuels post-Ukraine. As mentioned by INTERNATIONAL ENERGY AGENCY’s Coal 2025 report, the annual decline in EU’s coal consumption slowed down significantly in 2025 due to insufficient wind energy generation capacity, while non-power use of coal, including production of synthetic fuel through gasification, remains in place in Central & Eastern Europe owing to local coal reserves.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Coal to Liquid companies strive to build upon their technological distinction, process efficiency, and logistics integration in order to remain competitive. The companies’ emphasis on innovation encompasses developing next generation Fischer-Tropsch synthesis, better direct liquefaction catalysts, as well as advanced configurations of gasification facilities that increase fuel yields, efficiency of heat exchange, and conversion of coal into liquid fuels. Moreover, the companies place significant importance on increasing the capacity of indirect liquefaction, since it produces higher quality fuels as well as greater product flexibility. This allows them to produce not only transportation fuels but also other chemicals that can be used by a variety of customers. The vertical integration with the mines as well as refining facilities provides greater security of inputs and cost reduction amid fluctuating prices for energy input commodities. Capacity expansion is conducted primarily in the provinces in China abundant in coal resources, namely Xinjiang, Inner Mongolia, and Shaanxi, because it is necessary to align production capabilities with demands of the fuel and petrochemical industry ecosystem. In addition, the companies consider preparation for carbon capture, process automation, and standardization of the emissions standards along with signing offtake agreements with the state enterprises.

The Major Players In The Industry

- Sasol Limited

- China Shenhua Energy Company

- Yankuang Energy Group Company Limited

- Inner Mongolia Yitai Coal Co., Ltd.

- China National Petroleum Corporation (CNPC)

- Shell Plc

- ExxonMobil Corporation

- Chevron Corporation

- TransGas Development Systems LLC

- DKRW Energy LLC

- Envidity Energy Inc.

- Altona Energy Plc

- Celanese Corporation

- Linc Energy Ltd.

- Eastman Chemical Company

Key Development

- In March 2025, Sasol Limited revealed the continued operation of their Fischer-Tropsch synthetic fuels plant in Secunda, South Africa, which remains the world’s biggest CTL plant, maintaining its focus on coal-based liquid fuels whilst undertaking further investigations into integrating CCUS technologies into its indirect liquefaction processes.

- In January 2025, China Shenhua Energy Company confirmed that its direct coal liquefaction plant in Ordos, Inner Mongolia, had been producing consistently, solidifying its status as the sole operational DCL plant in the world and working on improving process efficiency through second-generation technology development.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$5.43 Bn |

| Forecast Revenue (2035) | US$12.53 Bn |

| CAGR (2026-2035) | 9.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Indirect Coal Liquefaction (ICL), Direct Coal Liquefaction (DCL), Hybrid Processes), By Product Type (Diesel , Gasoline, Jet Fuel, Lubricants, Chemical Feedstock, LPG (Liquefied Petroleum Gas), Others), By Coal Type (Bituminous Coal, Sub-Bituminous Coal, Lignite, Anthracite), By Application (Transportation Fuel, Cooking Fuel, Chemical Industry Feedstock, Power Generation Blending ,Industrial Solvents, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Sasol Limited, China Shenhua, Yankuang, Inner Mongolia, China National, Shell Plc, ExxonMobil, Chevron Corp, TransGas Development, DKRW Energy, Envidity Energy, Altona Energy, Celanese Corp, Linc Energy, Eastman Chemical |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |