Quick Navigation

Report Overview

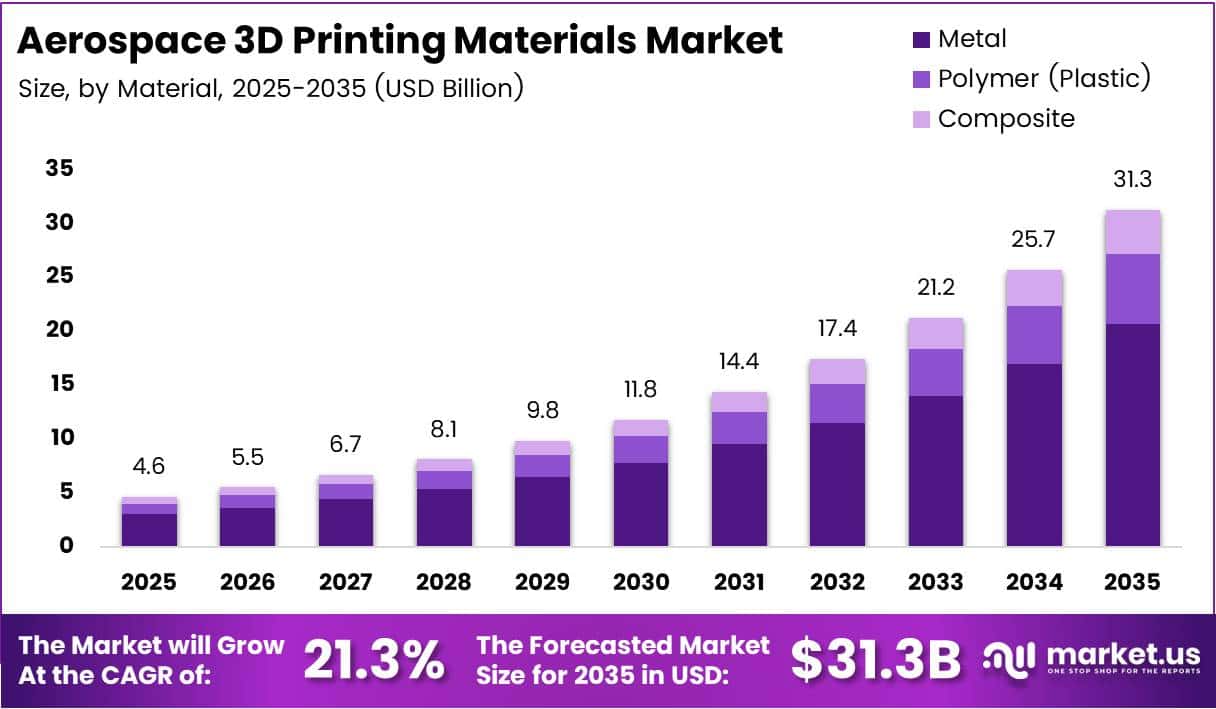

Global Aerospace 3D Printing Materials Market size is expected to be worth around USD 31.3 Billion by 2035 from USD 4.6 Billion in 2025, growing at a CAGR of 21.3% during the forecast period 2026 to 2035.

The aerospace 3D printing materials market covers metals, polymers, and composites used in additive manufacturing processes for aircraft, UAVs, and spacecraft. These materials enable production of flight-certified components through technologies such as Selective Laser Melting and Electron Beam Melting. Aerospace OEMs now treat additive manufacturing as a core production method, not an experimental one.

Metal alloys — particularly titanium, aluminum, and nickel superalloys — form the structural backbone of this market. Their ability to produce near-net-shape parts with minimal waste directly addresses aerospace’s twin pressures of cost and weight reduction. Consequently, metal materials account for the largest share, reflecting where engineering and procurement decisions currently concentrate.

Software infrastructure drives adoption as strongly as materials themselves. Design, inspection, and printer management software determines whether a manufacturer can certify and scale printed parts. This software-led dependency creates a recurring revenue layer on top of material sales, which explains why the software segment commands a dominant share within the component breakdown.

Government and commercial investment continues to push industrialization of additive manufacturing. In January 2024, GKN Aerospace committed £50 million (~$64 million) to additive manufacturing capabilities at its Trollhättan facility in Sweden, with £12 million co-funded by Sweden’s Industriklivet sustainability initiative — signaling that national industrial policy now treats aerospace AM as a strategic priority, not merely a cost experiment.

Certification and supply chain maturity are closing the gap between prototype use and serial production. According to Stratasys, Airbus now produces more than 25,000 flight-ready 3D-printed parts annually, with over 200,000 certified polymer parts in active service across the A320, A350, and A400M fleets. This scale confirms that polymer AM has crossed the threshold from low-volume trial to production-line standard.

The weight and lead time gains are equally significant. In the Airbus A350 programme, 3D-printed components deliver a 43% part weight reduction and an 85% reduction in lead time versus conventionally manufactured equivalents. For aircraft operators, lighter parts translate directly into fuel savings per flight cycle — making the economic case for AM materials self-reinforcing as fuel costs remain a primary airline cost driver.

Prototyping remains the entry application, but functional parts and engine components represent the higher-margin, faster-growth frontier. Manufacturers that secure material certification for structural and propulsion applications will access a much larger revenue base than those serving prototyping alone. The 21.3% CAGR reflects precisely this shift — from a niche materials supplier market toward a certified production materials platform.

Key Takeaways

- The global Aerospace 3D Printing Materials Market is valued at USD 4.6 Billion in 2025 and is forecast to reach USD 31.3 Billion by 2035, at a CAGR of 21.3%.

- By Component, Software leads with a 56.3% share, reflecting the critical role of design, inspection, and printer management platforms in certified AM production.

- By Technology, Selective Laser Melting (SLM) holds the largest share at 34.2%, driven by its precision and compatibility with aerospace-grade metal alloys.

- By Application, Prototyping commands 35.8% of the market, though functional parts and engine components represent the faster-scaling revenue segments.

- By Material, Metal holds a dominant 65.5% share, underpinned by titanium and nickel alloy demand in structural and propulsion components.

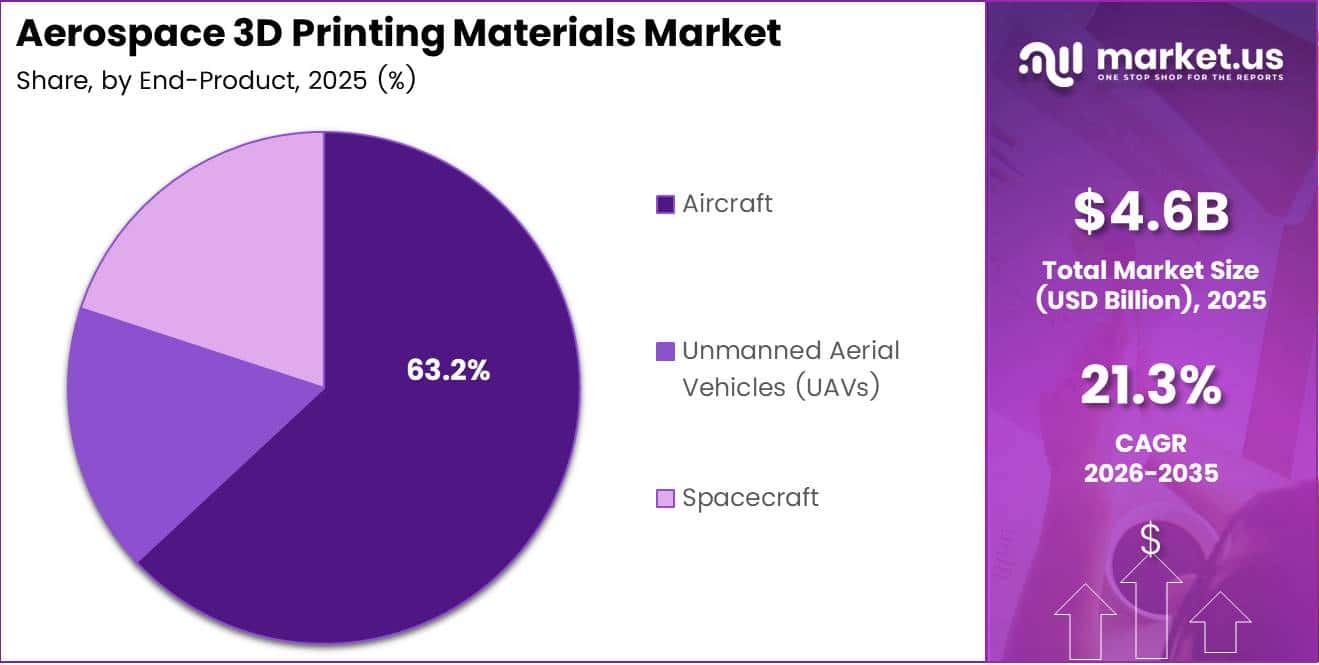

- By End-Product, Aircraft accounts for 63.2%, with UAVs and spacecraft forming the next wave of certified AM adoption.

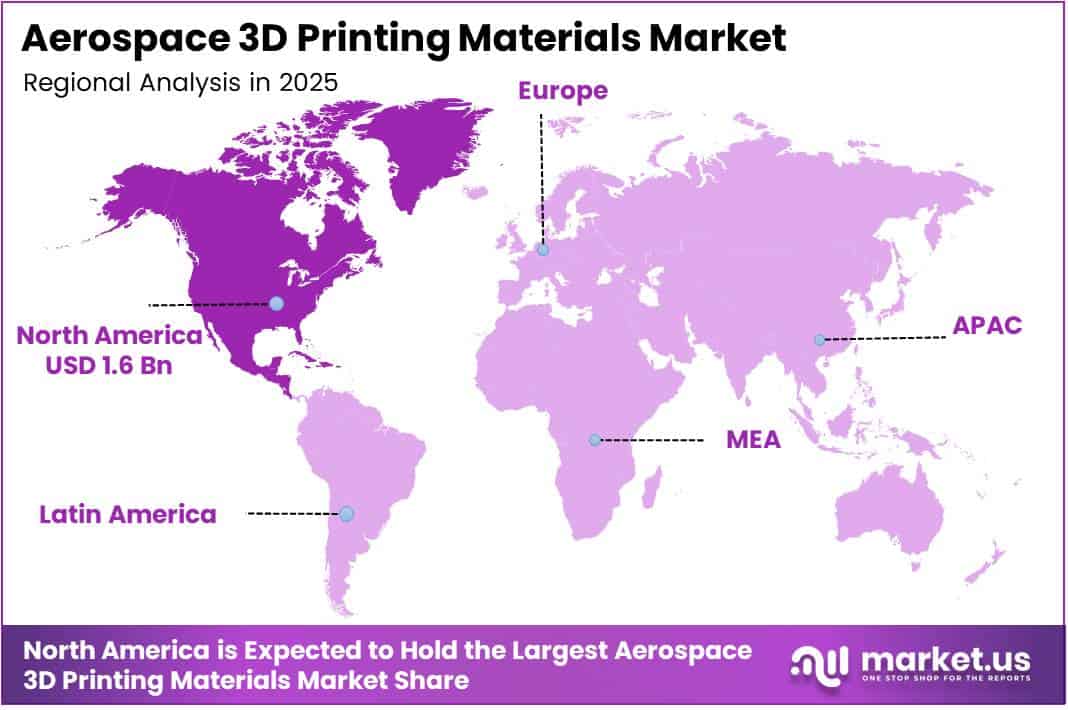

- North America leads regional markets with a 34.80% share, valued at USD 1.6 Billion, supported by defense procurement and leading OEM concentration.

Component Analysis

Software dominates with 56.3% due to certification-driven design and inspection dependency.

In 2025, Software held a dominant market position in the By Component segment of the Aerospace 3D Printing Materials Market, with a 56.3% share. Aerospace manufacturers cannot print and fly a component without software-controlled design validation, inspection, and process monitoring. This regulatory necessity converts software from a productivity tool into a compliance requirement, anchoring its lead position across the value chain.

Design Software serves as the entry point where engineers define part geometry, topology optimization, and material parameters before a single layer is deposited. Its influence on material selection and waste reduction makes it a direct cost lever, not just a design aid. Consequently, aerospace OEMs invest heavily in design software to achieve the geometry complexity that conventional manufacturing cannot produce.

Inspection Software carries the highest certification weight within the software stack. Aviation authorities require documented, repeatable quality verification at every production stage, making inspection software non-negotiable for flight-certified parts. Manufacturers that deploy advanced inspection platforms can accelerate part approval timelines — a competitive advantage when new aircraft programmes demand rapid material qualification.

Printer Software controls process parameters — layer thickness, laser power, scan speed — that determine material microstructure and final mechanical properties. Small deviations in these parameters can render a part non-compliant. Therefore, aerospace-grade printer software commands a significant premium over industrial equivalents, reflecting the cost of precision and traceability at scale.

Scanning Software integrates dimensional verification and surface analysis directly into the production loop. By capturing real-time geometric data against CAD references, it reduces post-production rejection rates. For high-value titanium and nickel alloy parts, catching defects in-process rather than post-process represents substantial cost avoidance per component.

Hardware encompasses the actual additive manufacturing machines — SLM, EBM, and DMLS systems — that process aerospace-grade materials. While hardware represents the lower share segment, it forms the capital investment anchor of any AM program. Hardware procurement decisions lock manufacturers into specific material ecosystems, making hardware selection a long-term strategic commitment, not a transactional purchase.

Technology Analysis

Selective Laser Melting (SLM) dominates with 34.2% due to precision metal fusion for certified structural parts.

In 2025, Selective Laser Melting (SLM) held a dominant market position in the By Technology segment of the Aerospace 3D Printing Materials Market, with a 34.2% share. SLM’s ability to fully melt metal powder bed layers produces dense, high-strength components that meet aerospace fatigue and structural standards. This makes SLM the preferred process for flight-critical titanium and nickel superalloy parts across leading OEM programmes.

Electron Beam Melting (EBM) differentiates through its vacuum processing environment, which prevents oxidation in reactive metals such as titanium aluminide and cobalt-chrome. EBM produces parts with lower residual stress than laser-based methods, making it particularly suitable for turbine blades and implantable-grade aerospace structures where stress-induced distortion is a rejection risk.

Direct Metal Laser Sintering (DMLS) serves the high-complexity, low-volume segment where part consolidation justifies the process cost. DMLS shares the certified material library with SLM but operates at slightly different energy densities, giving manufacturers flexibility across part geometries. Its established certification track record with aviation authorities makes it a lower-risk entry point for new AM production programs.

Stereolithography (SLA) operates in the polymer domain, producing high-accuracy tooling masters, jigs, and non-structural cabin components. SLA’s material base — photopolymer resins — cannot match metal AM for structural load-bearing applications, but it delivers cost-efficient solutions for interior and maintenance tooling. GE Aerospace’s CFM RISE programme targets at least 20% better fuel efficiency, and lightweight SLA-produced tooling reduces the assembly costs that support such efficiency goals.

Others in this technology segment include Binder Jetting, Material Extrusion, and Directed Energy Deposition (DED). These processes are gaining traction in MRO and large-structure repair applications where material deposition rate and part scale matter more than the precision achieved by powder-bed methods. Their share will expand as MRO operators build AM capability to reduce dependence on legacy spare part inventories.

Application Analysis

Prototyping dominates with 35.8% due to lower certification barriers and faster design iteration cycles.

In 2025, Prototyping held a dominant market position in the By Application segment of the Aerospace 3D Printing Materials Market, with a 35.8% share. Prototyping requires no flight certification, allowing engineers to test complex geometries without regulatory approval delays. This accessibility makes it the highest-volume entry application, but it also represents the lowest-margin segment — functional parts and engine components carry significantly greater revenue per kilogram of material consumed.

Tooling bridges the gap between prototyping and serial production by enabling manufacturers to 3D print jigs, fixtures, and molds that support conventional assembly lines. Additive tooling reduces lead times from weeks to days and eliminates minimum order quantities, directly lowering production support costs. As aerospace programmes accelerate their build rates, tooling demand scales proportionally without requiring individual part certification.

Functional Parts represent the highest-value, fastest-converting application segment. These are certified, flight-ready components — brackets, ducts, housings, fuel system parts — that replace conventionally manufactured equivalents. Stratasys’s December 2025 announcement that Airbus operates over 200,000 certified polymer functional parts across active fleets demonstrates that this segment has moved from qualification into full-scale serial production.

Material Analysis

Metal dominates with 65.5% due to structural and propulsion requirements demanding certified alloys.

In 2025, Metal held a dominant market position in the By Material segment of the Aerospace 3D Printing Materials Market, with a 65.5% share. Titanium, nickel superalloys, and aluminum alloys are the only material families that satisfy aerospace structural, thermal, and fatigue specifications. Metal AM’s dominance reflects the fact that aircraft manufacturers cannot substitute lower-performing materials in primary and propulsion structures without compromising airworthiness certification.

Polymer (Plastic) materials serve interior, tooling, and non-structural applications where weight reduction matters more than metal-grade mechanical performance. Polymer AM’s primary competitive advantage is speed and cost — cycle times are shorter, material costs are lower, and the certification burden is reduced for non-load-bearing parts. The Airbus A350 programme’s deployment of tens of thousands of printed polymer parts confirms this segment’s production-scale viability.

Composite materials combine fibre reinforcement with polymer or metal matrices to deliver strength-to-weight ratios that neither pure metal nor pure polymer can achieve. Continuous fibre composites, in particular, target structural applications where traditional carbon fibre layup is cost-prohibitive at low volumes. As composite AM printing platforms mature, this segment is positioned to capture share from both metal and polymer in secondary structural applications.

End-Product Analysis

Aircraft dominates with 63.2% due to high certified-part volume across commercial and defence programmes.

In 2025, Aircraft held a dominant market position in the By End-Product segment of the Aerospace 3D Printing Materials Market, with a 63.2% share. Commercial and military aircraft programmes consume the largest absolute volume of certified AM materials, driven by long production runs and continuous MRO demand. Airlines operating fleets of thousands of aircraft create a sustained, predictable material pull that spacecraft and UAV programmes cannot yet match in volume.

Unmanned Aerial Vehicles (UAVs) represent the fastest-expanding end-product segment, driven by defence procurement of strike, surveillance, and logistics UAVs. The speed of UAV programme development cycles makes additive manufacturing particularly valuable — traditional tooling lead times are incompatible with rapid capability deployment. Additionally, military UAV programmes tolerate higher per-unit material costs in exchange for faster part availability and design flexibility.

Spacecraft demonstrates the most ambitious AM application — Relativity Space manufactures approximately 85% of its Terran rocket structure using additive manufacturing, including all Aeon R engines on Terran R’s 13-engine first stage. This is the highest AM content of any orbital launch vehicle, signaling that the spacecraft segment will drive demand for the highest-performance, most precisely characterized metal AM materials as commercial launch competition intensifies.

Key Market Segments

By Component

- Software

- Design Software

- Inspection Software

- Printer Software

- Scanning Software

- Hardware

By Technology

- Selective Laser Melting (SLM)

- Electron Beam Melting (EBM)

- Direct Metal Laser Sintering (DMLS)

- Stereolithography (SLA)

- Others

By Application

- Prototyping

- Tooling

- Functional Parts

By Material

- Metal

- Polymer (Plastic)

- Composite

By End-Product

- Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Spacecraft

Drivers

Demand for Lightweight Components and Complex Geometries Accelerates Additive Manufacturing Adoption in Aerospace Production

Aerospace manufacturers face a structural cost problem: traditional subtractive manufacturing removes up to 90% of raw material in complex titanium parts, creating waste costs that additive manufacturing eliminates. The shift to AM is therefore not discretionary — it is a direct response to procurement economics. Manufacturers that retain conventional processes face a growing cost disadvantage against AM-enabled competitors.

According to Stratasys, 3D-printed components in the Airbus A350 programme deliver a 43% part weight reduction and an 85% reduction in lead time versus conventionally manufactured equivalents. These figures translate directly into airline operating economics — lighter structures reduce fuel burn per cycle, while shorter lead times compress programme costs. Both outcomes reinforce OEM investment in AM materials and equipment at scale.

In January 2024, GKN Aerospace committed £50 million (~$64 million) to additive manufacturing capabilities at its Trollhättan, Sweden facility, with approximately 150 new jobs expected. This investment reflects a supplier-tier conviction that AM will be a primary production method — not a supplementary one — for the next generation of aerospace structures. Suppliers that build certified AM capacity now will be better positioned to win long-term programme contracts from OEMs already committed to the technology.

Restraints

Limited Certified Material Availability and High Equipment Costs Constrain Aerospace AM Adoption at Tier-2 and Tier-3 Suppliers

The aerospace industry’s certification requirements create a fundamental bottleneck: only materials that have passed FAA or EASA qualification testing can enter flight-critical production. The qualification process is expensive and time-consuming, limiting the approved material library to a fraction of what the broader AM industry offers. Smaller suppliers cannot absorb certification costs, restricting adoption to well-capitalized tier-1 manufacturers and OEMs.

High capital expenditure for industrial AM equipment — particularly SLM and EBM systems capable of aerospace-grade output — creates a significant barrier for smaller producers. Systems designed for aerospace tolerances can cost several hundred thousand to over one million dollars per unit, before accounting for facility modification, post-processing equipment, and quality assurance infrastructure. This concentration of capability at large manufacturers limits the competitive supply base and sustains pricing power for established vendors.

The combination of restricted certified material availability and high equipment costs means the market cannot scale through a broad supplier network. Instead, growth concentrates in a small number of vertically capable players. For material suppliers, this creates volume risk — their sales growth depends on a narrow customer base making large, infrequent capital commitments rather than a distributed base of frequent buyers expanding incrementally.

Growth Factors

High-Performance Alloy Development, MRO Expansion, and On-Demand Manufacturing Open New Revenue Layers for Aerospace AM Material Suppliers

Development of next-generation metal alloys — including gamma titanium aluminide, refractory high-entropy alloys, and nickel superalloy variants — directly expands the addressable application range for AM material suppliers. Each new certified alloy unlocks a new application category, from turbine hot-section components to hypersonic structural parts. Suppliers that lead alloy qualification programmes establish long-term material specification advantages that competitors cannot easily displace.

According to GE Aerospace, the company achieved a 28% increase in LEAP engine output in 2025, with its critical component line improving on-time delivery from 20% to 96%. This operational improvement was enabled in part by additive manufacturing process investment. For material suppliers, GE’s output scaling confirms that AM-enabled engine production is moving toward sustained high-volume demand — not a one-time ramp — creating a durable commercial pull for certified metal AM materials.

In June 2025, Velo3D signed a Cooperative Research and Development Agreement (CRADA) with two U.S. Naval Air Systems Command (NAVAIR) federal laboratories to advance additive manufacturing capabilities for aerospace and defense applications. MRO and on-demand manufacturing represent a structural shift — military operators that replace centralized spare part inventories with distributed AM production need a continuous and qualified material supply chain. This creates a new, recurring revenue model for material vendors beyond the OEM production cycle.

Emerging Trends

AI-Driven Design Optimization and Cross-Industry Certification Collaboration Redefine Competitive Positioning in Aerospace AM

AI integration in topology optimization software now enables engineers to generate part geometries that no human designer would conceive — structures that minimize weight while satisfying multiple simultaneous load cases. This design capability increases the performance premium of AM over conventional manufacturing, directly expanding the number of components where additive production becomes technically superior and economically justified.

Certification and standardization efforts between OEMs and material suppliers are compressing the qualification timeline for new alloys and processes. Historically, qualification could take several years per material-process combination. Collaborative frameworks — where OEMs share test data with material suppliers and certification bodies simultaneously — are shortening that cycle, which means new high-performance materials reach production programmes faster, accelerating the overall market’s material refresh rate.

According to Relativity Space, approximately 85% of the Terran rocket structure uses additive manufacturing — the highest AM content of any orbital launch vehicle. This benchmark signals a directional shift: the most AM-intensive programmes now operate at the frontier of spacecraft design, not aerospace heritage manufacturing. For early movers in composite and refractory metal AM materials, the spacecraft segment offers a high-value, specification-driven demand pipeline that conventional aerospace supply chains are structurally unable to serve.

Regional Analysis

North America Dominates the Aerospace 3D Printing Materials Market with a Market Share of 34.80%, Valued at USD 1.6 Billion

North America holds a 34.80% share of the global market, valued at USD 1.6 Billion, driven by the concentration of leading aerospace OEMs, defence primes, and tier-1 suppliers operating certified AM programs. U.S. Department of Defense procurement of AM-enabled components and GE Aerospace’s $650 million manufacturing investment across 22 sites reinforce the region’s structural lead in certified production-scale additive manufacturing.

Europe Aerospace 3D Printing Materials Market Trends

Europe benefits from Airbus’s large-scale deployment of certified 3D-printed polymer parts — over 200,000 units across active fleets — alongside GKN Aerospace’s £50 million additive manufacturing investment in Sweden. National industrial policy, including Sweden’s Industriklivet co-funding, signals that European governments treat AM capability as a sovereign industrial priority. This policy backing accelerates supplier investment beyond what market demand alone would drive.

Asia Pacific Aerospace 3D Printing Materials Market Trends

Asia Pacific combines Japan’s precision manufacturing culture and South Korea’s advanced materials industry with China’s state-backed aerospace expansion. These structural factors push AM material adoption across both commercial aviation programmes and domestic defence procurement. Regional manufacturers increasingly view certified AM capability as a requirement to participate in global aerospace supply chains, rather than a differentiating feature.

Middle East and Africa Aerospace 3D Printing Materials Market Trends

The Middle East, particularly the UAE and Saudi Arabia, invests in aerospace manufacturing capability as part of economic diversification strategies beyond hydrocarbon revenues. MRO operations supporting large regional carrier fleets create initial demand for AM materials in maintenance and repair applications. As these nations build sovereign aerospace manufacturing capacity, their AM material demand will shift progressively toward higher-value structural and propulsion applications.

Latin America Aerospace 3D Printing Materials Market Trends

Latin America’s aerospace AM market centers on Brazil, where Embraer’s regional jet programmes and a developed tier-1 supplier base create structured demand for advanced manufacturing materials. AM adoption in the region currently concentrates in tooling and prototyping, reflecting the earlier industrialization stage of the local supply chain. As OEM build rates increase and certification frameworks mature, functional parts production will expand the region’s material consumption base.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Spirit AeroSystems operates as a tier-1 aerostructures supplier with direct responsibility for primary aircraft structures — fuselages, nacelles, and pylons — where additive manufacturing reduces assembly complexity and part count. Its position at the OEM interface gives Spirit privileged access to new programme requirements before they reach the broader supply market. However, its heavy customer concentration means AM investment returns depend largely on Boeing and Airbus programme health.

Thales approaches aerospace AM from the avionics and defence electronics angle, where AM enables miniaturized, thermally optimized housings and structural brackets with performance specifications that conventional manufacturing cannot cost-effectively meet. Thales’s strength lies in its systems integration capability — it does not just produce AM components but qualifies them within complex certified systems. This integration depth creates a differentiated value proposition that material-only suppliers cannot replicate.

Lockheed Martin applies additive manufacturing across its F-35, space, and hypersonics programmes, where the performance requirements for materials — high-temperature alloys, radiation-resistant composites — sit at the absolute frontier of AM material science. Lockheed’s scale of defence programme involvement gives it the purchasing power to co-develop proprietary material specifications with alloy suppliers, creating long-term supply chain dependencies that reinforce its production cost position.

Melrose Industries, through GKN Aerospace, has committed £50 million to additive manufacturing infrastructure at its Trollhättan facility — a deliberate move to capture engine component and structural part contracts as OEMs qualify AM production for serial manufacturing. GKN’s April 2026 TITAN-AM programme with the U.S. Air Force Research Laboratory targets large titanium structure production with material waste reductions exceeding 70%, positioning it directly in the highest-value AM application segment.

Key Players

- Spirit AeroSystems

- Thales

- Lockheed Martin

- Melrose Industries

- Booz Allen Hamilton

- Stratasys

- EOS GmbH

- Danaher

- Formlabs

- ExOne

Recent Developments

- March 2024 — GE Aerospace invested over $650 million in manufacturing and supply chain upgrades across 22 sites in 14 U.S. states plus international facilities, with over $150 million specifically dedicated to additive manufacturing equipment. This investment represents the largest single-cycle AM infrastructure commitment by a commercial engine OEM, directly expanding certified production capacity for LEAP and next-generation engine components.

- December 2025 — Stratasys announced that Airbus now 3D prints over 25,000 flight-ready plastic parts annually using Stratasys technology, with more than 200,000 certified polymer parts in active service across the A320, A350, and A400M fleets. This milestone confirms serial-scale polymer AM production within a tier-1 commercial aviation programme, validating the market’s transition from prototype-volume to production-line material consumption.

- April 2026 — GKN Aerospace and the U.S. Air Force Research Laboratory launched the TITAN-AM programme, a $8.4 million initiative to industrialize Laser Metal Deposition with Wire (LMD-w) for large titanium aerospace structures at GKN’s Global Technology Centre in Fort Worth, Texas. The programme targets material waste reductions of more than 70%, addressing one of the highest cost barriers to titanium structural AM at production scale.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.6 Billion |

| Forecast Revenue (2035) | USD 31.3 Billion |

| CAGR (2026-2035) | 21.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software (Design Software, Inspection Software, Printer Software, Scanning Software), Hardware), By Technology (Selective Laser Melting (SLM), Electron Beam Melting (EBM), Direct Metal Laser Sintering (DMLS), Stereolithography (SLA), Others), By Application (Prototyping, Tooling, Functional Parts), By Material (Metal, Polymer (Plastic), Composite), By End-Product (Aircraft, Unmanned Aerial Vehicles (UAVs), Spacecraft) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Spirit AeroSystems, Thales, Lockheed Martin, Melrose Industries, Booz Allen Hamilton, Stratasys, EOS GmbH, Danaher, Formlabs, ExOne |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |