Quick Navigation

Report Overview

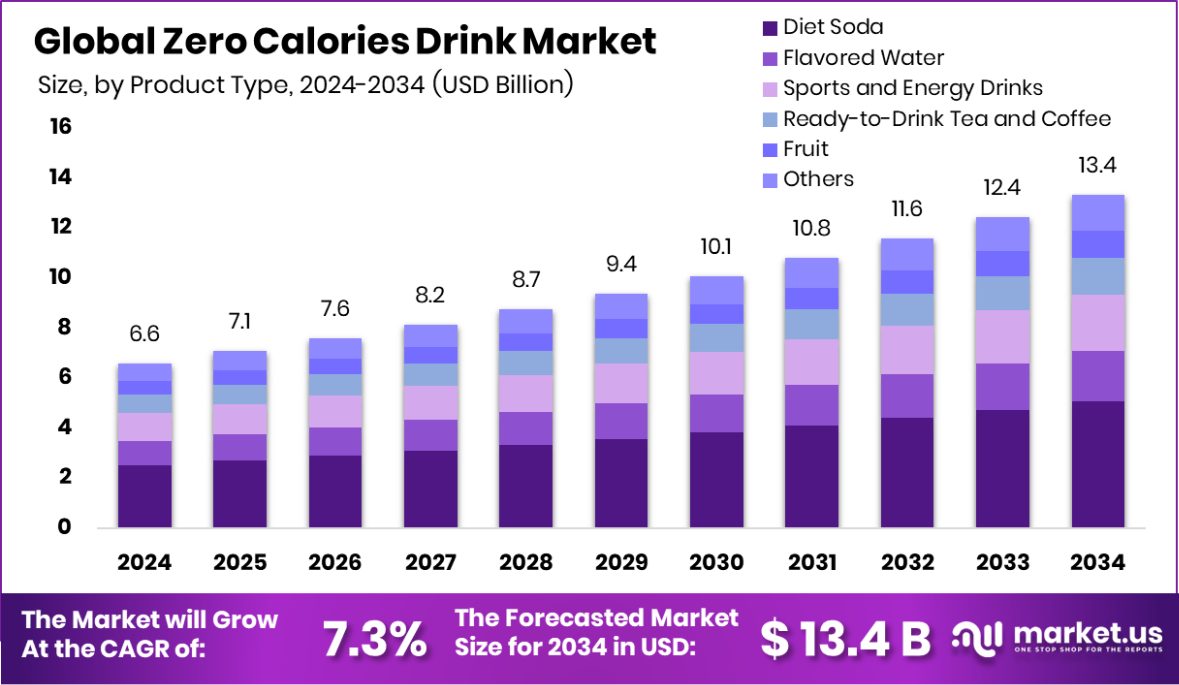

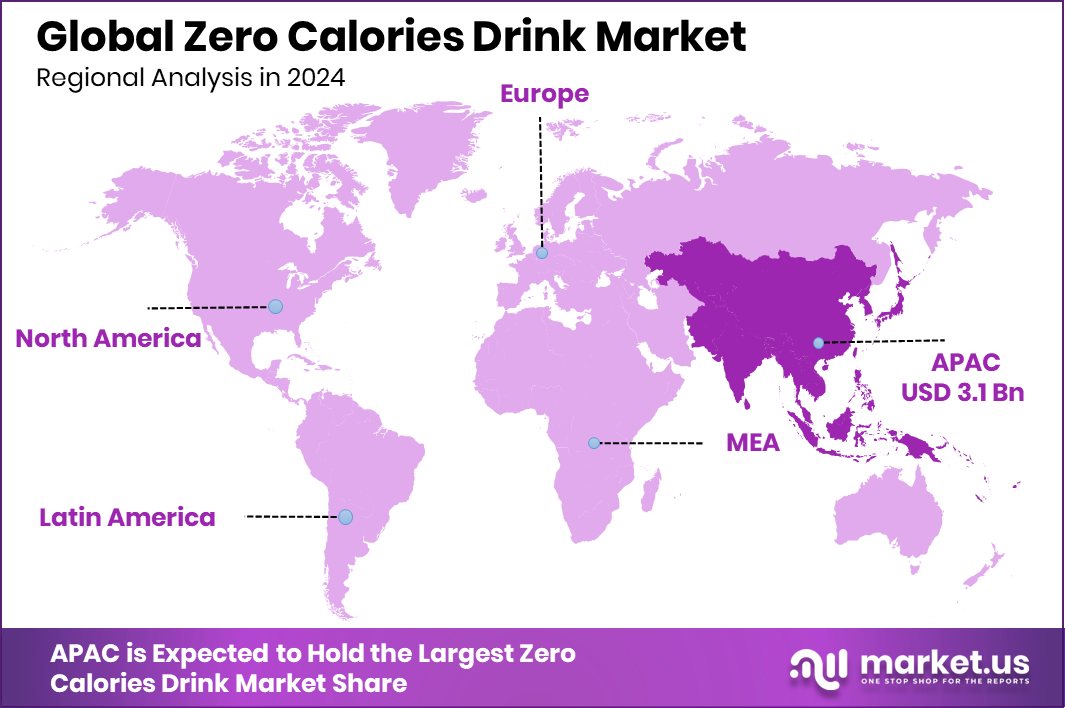

The Global Zero-Calorie Drink Market is expected to be worth around USD 13.4 billion by 2034, up from USD 6.6 billion in 2024, and grow at a CAGR of 7.3% from 2025 to 2034. With 47.20% dominance, Asia-Pacific’s Zero Calories Drink Market is worth USD 3.1 Bn.

A zero-calorie drink is a beverage that contains little to no calories per serving. These drinks are typically sweetened with artificial sweeteners or natural low-calorie substitutes to provide the sweet taste without the calorie content of sugar. Popular in diets and among those looking to reduce calorie intake without sacrificing sweet flavors, they include varieties such as sodas, teas, and flavored waters.

The zero-calorie drink market encompasses the production, distribution, and sale of beverages designed to offer the enjoyment of drinking without adding calories to the consumer’s diet. This market caters to health-conscious consumers and those managing dietary conditions like diabetes, where calorie intake needs to be controlled. Lucky Energy, a zero-calorie energy drink company, raised $14 million in a Series A1 round in March 2025, bringing its total funding to over $40 million.

The growth of the zero-calorie drink market is primarily driven by increasing health awareness among consumers worldwide. As obesity and related health issues like diabetes rise, more individuals are seeking healthier dietary options, including low-calorie beverages that align with a weight management or health-centric lifestyle. Additionally, advancements in food technology that improve the taste and variety of zero-calorie drinks have also contributed to their increased popularity.

Demand for zero-calorie drinks is bolstered by the shift in consumer preferences toward healthier food and beverage choices. The growing trend of maintaining a balanced diet and leading a healthier lifestyle has propelled the consumption of these beverages. Furthermore, the younger demographics, particularly millennials and Gen Z, who prefer trendy and healthy alternatives to traditional sugary drinks, significantly fuel this demand.

The zero-calorie drink market holds substantial opportunities in product innovation and geographic expansion. Developing new flavors and functional beverages that offer health benefits beyond calorie control, such as added vitamins or antioxidants, can attract a broader consumer base.

Key Takeaways

- The Global Zero-Calorie Drink Market is expected to be worth around USD 13.4 billion by 2034, up from USD 6.6 billion in 2024, and grow at a CAGR of 7.3% from 2025 to 2034.

- Diet soda dominates the zero-calorie drink market, holding a significant 38.20% share by product type.

- Artificial sweeteners lead in ingredient, comprising 42.20% of the zero-calorie drink market’s composition.

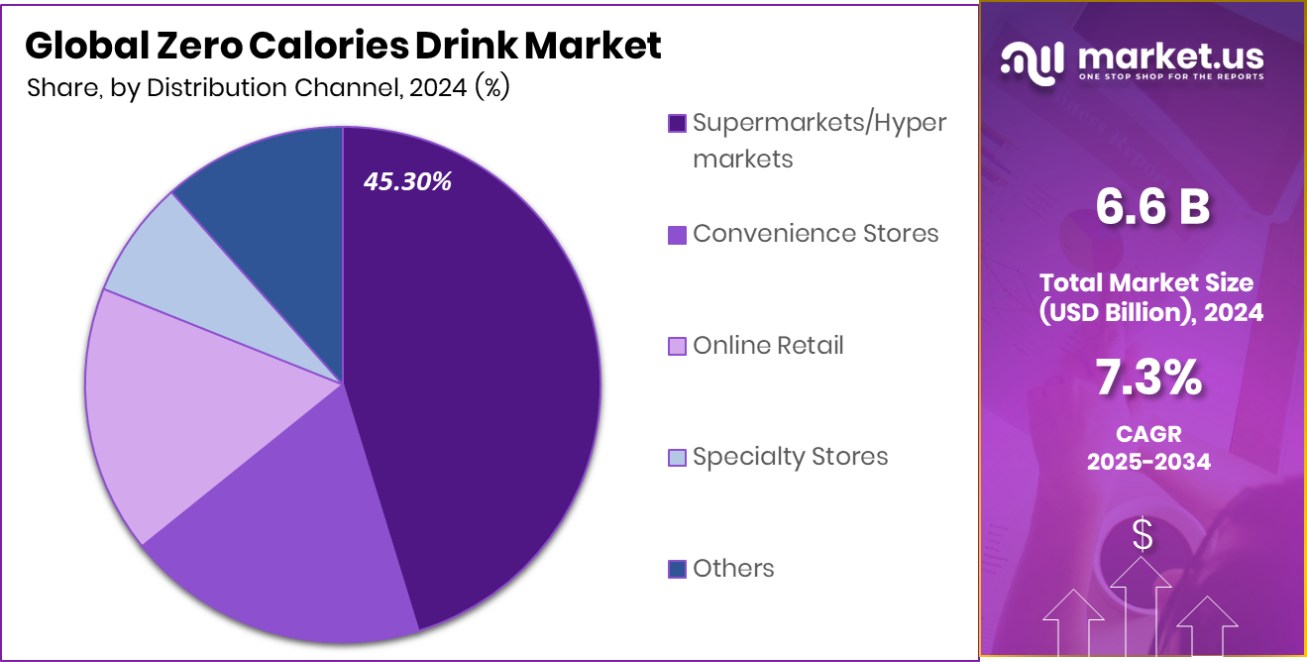

- In terms of distribution channels, Supermarkets/Hypermarkets take the largest share at 45.30%.

- Individuals are the primary end-users of zero-calorie drinks, accounting for an impressive 82.20% of the market.

- Asia-Pacific’s market value reaches USD 3.1 Bn, with a 47.20% market share.

By Product Type Analysis

Diet soda dominates the zero-calorie drink market with a 38.20% share.

In 2024, Diet Soda held a dominant market position in the By Product Type segment of the Zero-Calorie Drink Market, capturing a 38.20% share. This significant market presence underscores the continued consumer preference for diet soda options within the zero-calorie beverage category. The product’s appeal lies in its ability to offer a sweet, satisfying taste without the calorie content of traditional sodas, aligning with the growing consumer trend towards health-conscious eating and drinking habits.

The market’s inclination towards diet sodas is further supported by extensive distribution channels that ensure availability across various retail platforms, from supermarkets to online stores. This accessibility boosts consumer engagement and drives sales, reinforcing diet soda’s stronghold in the zero-calorie drink landscape.

Moreover, ongoing innovations in flavor and packaging, coupled with effective marketing strategies, have played crucial roles in maintaining the attractiveness of diet sodas. Brands have focused on appealing to a broader demographic by introducing a variety of flavors that cater to different taste preferences while also engaging in campaigns that emphasize the lifestyle benefits of zero-calorie consumption.

By Ingredients Analysis

Artificial sweeteners are preferred in zero-calorie drinks, holding a 42.20% market share.

In 2024, Artificial Sweeteners held a dominant market position in the By Ingredients segment of the Zero-Calorie Drink Market, with a 42.20% share. This substantial market share highlights the pivotal role of artificial sweeteners in crafting zero-calorie beverages that appeal to health-conscious consumers. Their ability to replicate the sweetness of sugar without the associated calories makes them an essential component in the formulation of diet drinks and other low-calorie alternatives.

The adoption of artificial sweeteners is driven by consumer demand for healthier beverage options that assist in managing weight and reducing sugar intake. This trend is further amplified by the rising incidence of health issues such as diabetes and obesity, which encourage consumers to opt for low-calorie, sugar-free products.

Additionally, the versatility of artificial sweeteners, capable of being used across a diverse range of beverages—from soft drinks to energy drinks—enhances their appeal. Their stability in various drink formulations allows manufacturers to innovate and expand their product lines without compromising on taste or quality.

As consumer preferences continue to evolve towards more healthful choices, artificial sweeteners are expected to maintain their dominance in the Zero-Calorie Drink Market, driven by both their functional benefits and alignment with current health trends.

By Distribution Channel Analysis

Supermarkets and hypermarkets lead distribution, capturing 45.30% of the zero-calorie drink market.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Zero-Calorie Drink Market, with a 45.30% share. This dominant share is indicative of the critical role supermarkets and hypermarkets play as primary shopping destinations for consumers seeking convenience and variety. These retail giants offer a wide array of zero-calorie drink options under one roof, catering to diverse consumer tastes and preferences, which significantly contributes to their market stronghold.

The strategic placement of zero-calorie drinks in high-traffic areas within these stores, coupled with aggressive promotional strategies and price discounts, further drives the visibility and accessibility of these products. Supermarkets and hypermarkets also benefit from strong supply chain efficiencies, which ensure a consistent and diverse availability of the latest and most preferred zero-calorie drink brands and flavors.

Additionally, the consumer experience in supermarkets and hypermarkets, characterized by the ability to physically inspect products before purchase, compare different brands, and enjoy instant gratification by taking purchases home immediately, enhances their appeal over other channels.

As health consciousness continues to rise among consumers, the role of supermarkets/hypermarkets is expected to remain significant in distributing zero-calorie drinks, maintaining their position as key facilitators in the access and consumption of healthier beverage alternatives.

By End-User Analysis

Individuals represent the largest end-user group, comprising 82.20% of market consumption.

In 2024, Individuals held a dominant market position in the By End-User segment of the Zero-Calorie Drink Market, with an 82.20% share. This substantial segment share reflects the significant consumer preference for zero-calorie drinks among individual buyers. This trend is largely driven by increasing health awareness and a growing inclination toward maintaining a healthier lifestyle, which includes reducing calorie intake and avoiding sugar.

Individual consumers are particularly attracted to zero-calorie beverages due to their benefits in weight management and reduced sugar-related health risks. The wide variety of flavors and options available also caters to personal tastes and preferences, further boosting their appeal. Additionally, the ease of purchasing these drinks through various channels, including online platforms, enhances their accessibility, making them a convenient choice for busy consumers.

The dominance of individuals in the market is supported by targeted marketing campaigns by beverage companies that focus on the personal health benefits and lifestyle enhancements associated with zero-calorie drinks. As the market continues to expand, individual consumers are likely to remain the predominant buyers, driven by ongoing trends in health and wellness and sustained product innovation tailored to meet their specific dietary needs.

Key Market Segments

By Product Type

- Diet Soda

- Flavored Water

- Sports and Energy Drinks

- Ready-to-Drink Tea and Coffee

- Fruit

- Others

By Ingredients

- Artificial Sweeteners

- Natural Sweeteners

- Electrolytes and Minerals

- Vitamins and Antioxidants

- Herbal and Botanical Ingredients

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Others

By End-User

- Individuals

- Commercial Use

Driving Factors

Growing Health Awareness Among Consumers

The most significant driving factor for the Zero-Calorie Drink Market is the growing health awareness among consumers. As more individuals become conscious of the impacts of sugar and calories on their health, there’s a noticeable shift toward beverages that offer healthier alternatives without compromising on taste. This trend is fueled by the increasing prevalence of obesity, diabetes, and other health-related issues that are directly linked to high sugar consumption.

Consumers are actively seeking out products that can help them maintain a healthier lifestyle while still enjoying the flavors they love. Zero-calorie drinks, with their promise of no sugar and low calories, perfectly align with these evolving consumer preferences, driving their popularity and market growth.

Restraining Factors

Concerns Over Artificial Sweeteners Limit Market Growth

One major restraining factor for the Zero-Calorie Drink Market is the growing consumer concern over the safety and health effects of artificial sweeteners. While these sweeteners provide the key benefit of reducing calorie intake, there is increasing scrutiny and skepticism regarding their long-term health impacts. Studies and media reports occasionally suggest potential links between artificial sweeteners and health issues, which can lead to consumer hesitation and distrust.

This skepticism is heightened by the trend toward natural and organic ingredients, with many consumers preferring products with easily recognizable and minimally processed ingredients. As a result, the perceived risks associated with artificial sweeteners could significantly hinder the market growth of zero-calorie drinks among health-conscious consumers.

Growth Opportunity

Expansion into Emerging Markets Offers Growth

A significant growth opportunity for the Zero-Calorie Drink Market lies in the expansion into emerging markets. As economic conditions improve in these regions, a larger number of consumers are gaining access to a variety of beverage options.

The increasing urbanization and rising middle class in countries such as India, Brazil, and China are particularly promising as these factors contribute to greater health awareness and changes in consumer lifestyle preferences.

Tapping into these markets with tailored marketing strategies and localized product offerings can open up substantial new avenues for growth. Furthermore, educating these new consumer bases about the benefits of zero-calorie drinks can create a lasting demand, driving market expansion and profitability.

Latest Trends

Natural and Organic Ingredients Trend Gains Momentum

A prominent trend in the Zero-Calorie Drink Market is the increasing consumer preference for natural and organic ingredients. As health consciousness grows, consumers are not just looking for low-calorie options but also products that are clean, transparent, and free from artificial additives.

This shift is driving beverage manufacturers to innovate by incorporating natural sweeteners like stevia, which offer the sweetness of sugar without the calories and are perceived as healthier alternatives.

Additionally, the use of organic ingredients appeals to environmentally conscious consumers who value sustainability in their purchasing decisions. This trend not only helps in attracting a broader consumer base but also aids in building trust and credibility among health-focused individuals, further propelling market growth.

Regional Analysis

In Asia-Pacific, Zero Zero-Calorie Drink Market holds a 47.20% share, valued at USD 3.1 Bn.

The Zero-Calorie Drink Market is experiencing varied growth across different regions, with Asia-Pacific leading the charge. Dominating the global landscape, Asia-Pacific holds a significant 47.20% market share and is valued at USD 3.1 billion. This robust performance is attributed to increasing health consciousness among the massive consumer base in countries like China and India, coupled with rising disposable incomes that allow for premium health-oriented purchases.

In contrast, North America and Europe also show substantial market engagement, driven by well-established health and wellness trends and high consumer awareness about dietary choices impacting health. These regions benefit from the presence of major market players who are continuously innovating and expanding their zero-calorie product lines.

Meanwhile, the Middle East & Africa, and Latin America are emerging as potential growth areas. These regions are gradually embracing healthier lifestyle choices, with urbanization and increasing health awareness playing pivotal roles in this shift. While currently smaller in market size compared to Asia-Pacific, North America, and Europe, these regions present new opportunities for expansion as consumer preferences continue to evolve towards health-conscious food and beverage choices.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Zero Calories Drink Market is significantly shaped by the strategic actions of key players such as the Coca-Cola Company, PepsiCo, Inc., and Dr Pepper Snapple Group. These industry giants not only have substantial influence due to their extensive distribution networks and brand recognition but also through their innovative approaches to meet evolving consumer demands in the zero-calorie segment.

Coca-Cola Company has been at the forefront of diversifying its portfolio to include a wider range of zero-calorie beverages, effectively capitalizing on the growing consumer preference for healthier drink options. The company’s commitment to product innovation, such as the introduction of flavored sparkling waters and reformulated versions of classic drinks with zero sugar, underscores its strategy to retain market dominance by aligning with health-conscious trends.

Similarly, PepsiCo has made significant strides in adapting to this market shift by expanding its zero-calorie offerings. The company leverages its strong global presence and robust marketing capabilities to effectively engage consumers and drive awareness about its healthier beverage alternatives. PepsiCo’s focus on R&D has enabled it to introduce products that maintain the taste and quality that consumers expect but with the added benefit of zero calories.

Dr Pepper Snapple Group, although smaller in scale compared to Coca-Cola and PepsiCo, holds a vital niche in the zero-calorie drinks market. The company focuses on targeted marketing and niche product offerings to carve out a unique space in the sector. By focusing on specific consumer segments and regional tastes, Dr Pepper Snapple Group has been able to compete effectively and maintain relevance in this highly competitive market.

Top Key Players in the Market

- Coca-Cola Company

- PepsiCo, Inc.

- Dr Pepper Snapple Group

- Nestlé S.A.

- Monster Beverage Corporation

- Red Bull GmbH

- Keurig Dr Pepper

- Diageo plc

- Unilever plc

- Hormel Foods Corporation

- Pure Leaf

- Bai Brands

- Zevia LLC

- AHA Sparkling Water

Recent Developments

- In 2025, Pepsi also expanded its Aquafina brand with FlavorSplash, a line of zero-calorie sparkling water beverages and liquid water enhancers, catering to the growing demand for versatile and healthy drink options.

- In 2024, Coca-Cola introduced Happy Tears Zero Sugar, a new zero-calorie drink available exclusively on social media platforms in the United States and Great Britain. This product is part of the Coke Creations platform and was aimed at engaging consumers digitally.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.6 Billion |

| Forecast Revenue (2034) | USD 13.4 Billion |

| CAGR (2025-2034) | 7.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Diet Soda, Flavored Water, Sports and Energy Drinks, Ready-to-Drink Tea and Coffee, Fruit, Others), By Ingredients (Artificial Sweeteners, Natural Sweeteners, Electrolytes and Minerals, Vitamins and Antioxidants, Herbal and Botanical Ingredients, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Others), By End-User (Individuals, Commercial Use) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Coca-Cola Company, PepsiCo, Inc., Dr Pepper Snapple Group, Nestlé S.A., Monster Beverage Corporation, Red Bull GmbH, Keurig Dr Pepper, Diageo plc, Unilever plc, Hormel Foods Corporation, Pure Leaf, Bai Brands, Zevia LLC, AHA Sparkling Water |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |