Global Z-Air Batteries Market Size, Share, And Industry Analysis Report By Type (Non-Rechargeable, Rechargeable), By Application (Hearing Aids, Military Devices, Safety Lamps, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: December 2025

- Report ID: 168830

- Number of Pages: 265

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

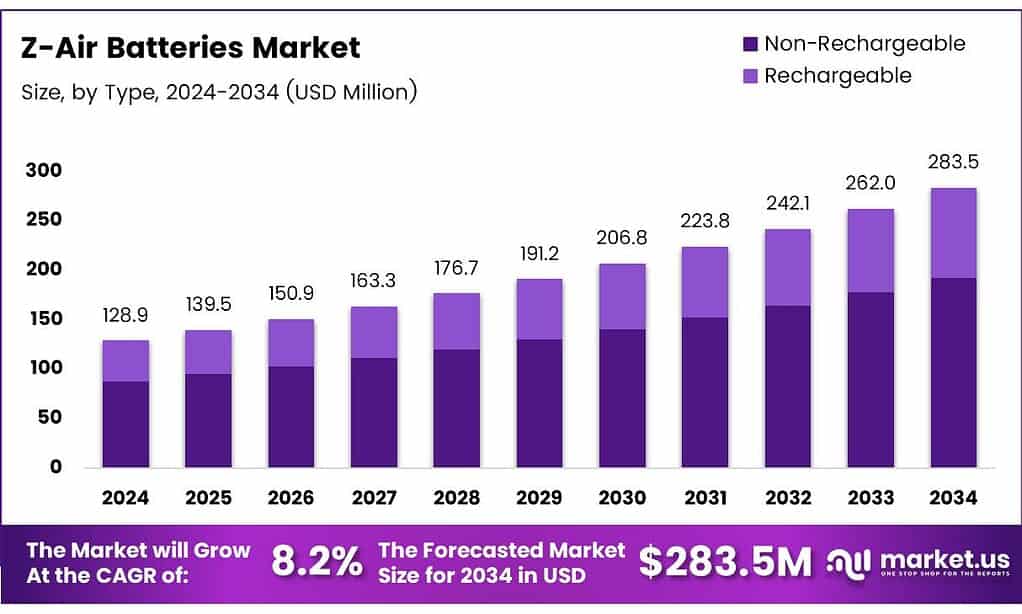

The Global Z-Air Batteries Market size is expected to be worth around USD 283.5 Million by 2034, from USD 128.9 Million in 2024, growing at a CAGR of 8.2% during the forecast period from 2025 to 2034.

The Z-Air Batteries Market refers to the commercial landscape built around zinc–air electrochemical energy storage systems for stationary and portable power needs. These batteries use zinc metal and atmospheric oxygen, enabling cost-efficient, safe, and scalable energy solutions. Consequently, the market aligns strongly with long-duration storage, backup power, and off-grid infrastructure requirements.

Z-air batteries themselves are metal-air systems known for simplicity, high material availability, and inherent safety advantages. Zinc is abundant, recyclable, and stable compared with lithium, supporting predictable lifecycle economics. Z-air batteries are increasingly evaluated for applications requiring reliability, long shelf life, and low environmental risk.

- Performance validation further strengthens commercial confidence in this market. Practical Z-air batteries achieve 500–600 Wh kg−1 energy density. Theoretical values reach 1086 Wh kg−1, nearly double advanced lithium-ion systems, enabling high-value stationary deployments.

Additionally, Z-air batteries sustain discharge current densities of 10 mA cm−2, supporting real-world systems like lighthouses and rail networks. While lithium–air batteries offer 11.68 kWh kg−1 theoretical density compared with 1.084 kWh kg−1 for Z-air, lithium’s reactivity limits practicality. Research from the U.S. Department of Energy highlights perovskite catalysts enabling over 100 stable room-temperature cycles for rechargeable Z-air systems.

Regulatory frameworks increasingly favor non-flammable and recyclable battery chemistries for public and defense assets. Energy agencies promote chemistries with low supply-chain exposure and minimal geopolitical risk. Zinc-based energy storage benefits from policy alignment focused on sustainability, resource security, and long-term cost stability. Opportunities are particularly strong in railway signaling, remote navigation aids, telecom backup, and microgrid storage.

Key Takeaways

- The Global Z-Air Batteries Market is projected to grow from USD 128.9 Million in 2024 to USD 283.5 Million by 2034, at a CAGR of 8.2%.

- Non-Rechargeable Z-Air batteries dominate the market by type, holding a leading share of 73.7% in 2024.

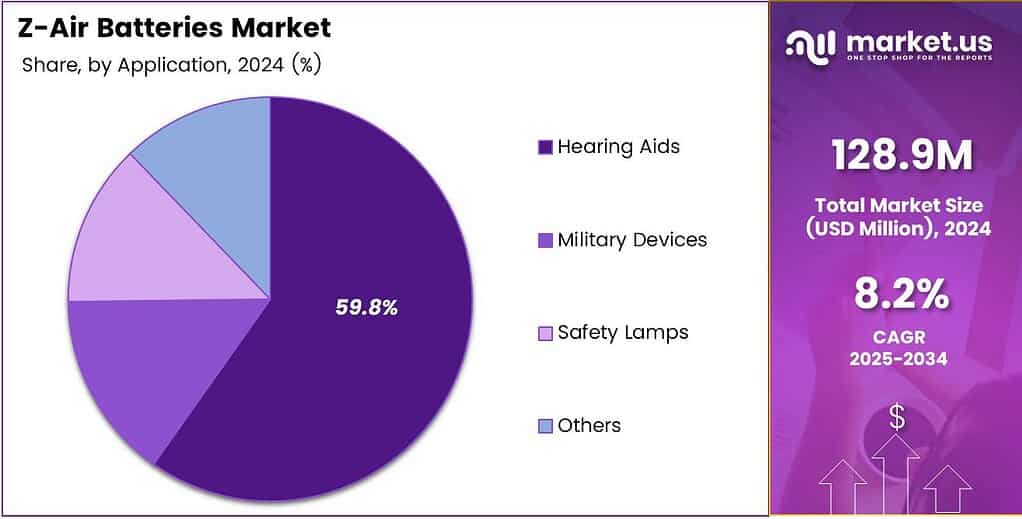

- Hearing Aids represent the largest application segment, accounting for a significant 59.8% market share in 2024.

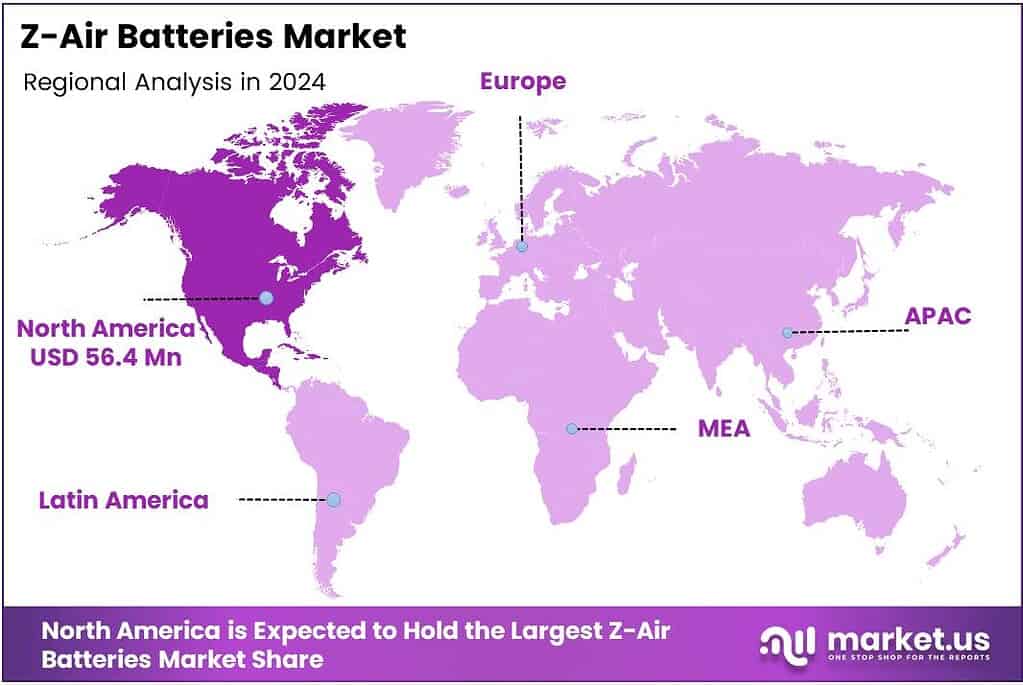

- North America is the dominating region, capturing 43.8% of the global market and valued at USD 56.4 Million in 2024.

By Type Analysis

Non-Rechargeable dominates with 73.7% due to its reliability, compact design, and strong adoption in low-drain medical applications.

In 2024, Non-Rechargeable held a dominant market position in the By Type Analysis segment of the Z-Air Batteries Market, with a 73.7% share. This leadership is supported by consistent performance, long shelf life, and low maintenance needs. As a result, manufacturers prefer these batteries for steady, single-use applications.

Rechargeable Z-Air batteries play a developing role in the By Type segment. Although adoption remains limited, innovation is gradually improving recharge efficiency and cycle stability. Therefore, rechargeable variants attract interest for future sustainable energy storage uses. However, technical complexity and higher costs still restrain widespread commercial penetration.

By Application Analysis

Hearing Aids dominate with 59.8% owing to the continuous demand for compact, high-energy-density power solutions.

In 2024, Hearing Aids held a dominant market position in the By Application Analysis segment of the Z-Air Batteries Market, with a 59.8% share. This dominance is fueled by growing aging populations and the need for reliable, long-lasting power sources. Additionally, Z-Air technology offers a stable voltage output ideal for sensitive hearing devices.

Military Devices represent a strategic application segment where reliability and energy density remain critical. Z-Air batteries support portable defense equipment due to dependable operation in extreme environments. Meanwhile, defense agencies value their lightweight structure and silent discharge characteristics, which enhance operational efficiency during field deployment.

The Safety Lamps segment benefits from Z-Air batteries’ long shelf life and emergency readiness. These batteries ensure dependable illumination in mines, tunnels, and industrial sites. Consequently, industries continue to adopt Z-Air-powered safety lamps for risk-prone environments where power reliability directly impacts worker safety.

The Others segment includes niche electronics and signaling equipment using Z-Air batteries for a stable, low-drain energy supply. Although smaller in scale, this segment supports market diversification. Over time, expanding use of specialized instruments helps sustain overall Z-Air Batteries Market demand.

Key Market Segments

By Type

- Non-Rechargeable

- Rechargeable

By Application

- Hearing Aids

- Military Devices

- Safety Lamps

- Others

Emerging Trends

Technology Improvements and Sustainability Focus Shape Market Trends

A key trend in the Z-Air batteries market is increasing research into rechargeable designs. Companies are working to overcome traditional limitations by improving electrode materials and air flow management. Sustainability is another strong market trend. Industries are shifting toward batteries made from abundant and recyclable materials.

- Zinc fits well into this direction, supporting environmentally responsible energy storage. Miniaturization of electronic devices also influences market trends. Battery storage deployment grew dramatically — deployment additions more than doubled, adding 42 GW globally. Compact Z-Air battery designs are being developed to meet space-efficient requirements in wearable and medical devices.

The integration of smart battery monitoring systems is gaining attention. Sensors that track battery health and performance improve reliability and user confidence. Finally, government interest in alternative energy storage supports market visibility. Policies encouraging safer and greener battery solutions indirectly benefit Z-Air technology.

Drivers

High Energy Density and Long Shelf Life Drive Z-Air Batteries Adoption

Z-Air batteries are gaining demand because they can store more energy than many traditional battery types. This makes them useful for devices that need long operating hours without frequent replacement. Users value their ability to deliver steady power over extended periods, especially in critical applications.

Another key driver is the long shelf life of Z-Air batteries. They can remain unused for years and still perform reliably when activated. This feature supports their use in medical, safety, and emergency devices where readiness is essential. Cost efficiency also supports market growth. Zinc is widely available and less expensive than many battery metals.

Environmental considerations further push demand. Z-Air batteries use fewer toxic materials and are easier to recycle than some conventional batteries. As sustainability goals gain importance, industries are looking at cleaner battery options. Technology improvements are also improving performance consistency.

Restraints

Limited Rechargeability and Performance Stability Restrain Market Expansion

One major restraint in the Z-Air batteries market is limited rechargeability. Many Z-Air batteries are designed for single use or have restricted recharge cycles. This limits their adoption in applications where frequent recharging is required. Another challenge is sensitivity to environmental conditions.

- Factors such as humidity and temperature can affect battery performance. This makes Z-Air batteries less reliable in harsh or uncontrolled environments. Global zinc reserves are estimated at 1.9 billion tons, whereas lithium reserves are only around 86 million tons.

Power output control is another concern. While energy density is high, Z-Air batteries may struggle to deliver sudden high power demands. This restricts their use in power-intensive devices. Manufacturing complexity also acts as a restraint. Air electrode stability and electrolyte management require precise engineering. This increases technical difficulty and slows mass production scaling.

Growth Factors

Rising Medical and Small Power Devices Create Growth Opportunities

The growing medical device sector presents strong opportunities for the Z-Air batteries market. Hearing aids, medical sensors, and portable monitoring devices benefit from long-lasting and lightweight power solutions. Another opportunity lies in wireless and low-power electronics.

Defense and safety equipment also support future growth. Backup power units, signaling devices, and emergency tools need batteries with long shelf life and high reliability. Advancements in rechargeable Z-Air technology open further opportunities. Ongoing research focuses on improving cycle life and air electrode durability, making them suitable for broader applications.

Emerging markets also provide growth potential. Cost-sensitive regions prefer affordable and efficient energy storage solutions, where zinc-based batteries fit well. With continued innovation and expanding end-use sectors, Z-Air batteries are positioned to move beyond niche applications into wider commercial use.

Regional Analysis

North America Dominates the Z-Air Batteries Market with a Market Share of 43.8%, Valued at USD 56.4 Mn

North America leads the Z-Air Batteries Market due to strong demand from healthcare devices, particularly hearing aids, along with steady defense and safety equipment usage. In 2024, the region accounted for a dominant 43.8% share, valued at USD 56.4 Million, supported by advanced medical infrastructure and high adoption of compact, long-lasting battery solutions. Continuous innovation, favorable reimbursement policies for medical devices, and early acceptance of alternative battery chemistries further strengthen regional leadership.

Europe shows stable growth driven by the rising use of zinc-air batteries in hearing healthcare, emergency lighting, and safety lamps. Strong environmental regulations encourage mercury-free and recyclable battery technologies, supporting zinc-air adoption. Aging population trends and increased focus on sustainable energy storage solutions further contribute to consistent market expansion across developed European economies.

Asia Pacific is emerging as a high-potential region due to growing healthcare access, rising disposable incomes, and expanding electronics manufacturing. Increased awareness of hearing health, especially in densely populated nations, drives demand for zinc-air batteries. Government support for medical device manufacturing and improving distribution networks also enhances regional growth prospects.

The Middle East and Africa market is gradually developing, supported by improvements in healthcare infrastructure and rising demand for portable power solutions in remote and off-grid areas. Zinc-air batteries are increasingly used in medical and safety applications where reliability and long shelf life are essential. Public health initiatives contribute to slow but steady adoption.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Duracell brings strong brand recognition and distribution capabilities to the emerging Z-air batteries space. The company can leverage its experience in consumer and specialty batteries to pilot zinc-air formats for hearing aids, medical devices, and backup power. Duracell’s scale positions it well to drive standardization, reliability, and confidence among OEMs evaluating next-generation chemistries.

Ravoyac remains closely associated with hearing-aid and button-cell formats, aligning naturally with Z-air technology’s strengths in high energy density and compact form factors. Its focus on value and performance in small batteries makes it a practical partner for medical and assistive device manufacturers. The company could use Z-air chemistries to differentiate on runtime and sustainability.

Electric Fuel Battery Corporation has a long history in metal-air and specialty power solutions, giving it a technical head start in Z-air system design. Its portfolio in defense, industrial, and backup power aligns with applications where long duration, safety, and low maintenance are critical. This know-how can accelerate the commercialization of modular Z-air packs for niche, high-value segments.

ZAF Energy System is positioned as an innovation-driven player focused on advanced zinc-based chemistries. Its R&D orientation and partnerships with equipment makers and integrators can help translate lab-scale Z-air advances into scalable products. By targeting stationary storage, telecom backup, and mobility auxiliaries, ZAF can carve out early adopter markets that value lower cost, longer life, and recyclability compared with conventional lithium systems.

Top Key Players in the Market

- Duracell

- Ravoyac

- Electric Fuel Battery Corporation

- ZAF Energy System

- Varta AG

- GP Batteries

- Phinenergy

- Renata SA

- AZA Battery

Recent Developments

- In 2025, Duracell, a Berkshire Hathaway subsidiary, maintains a strong presence in primary zinc-air batteries for hearing aids and medical devices, leveraging its historical innovations in zinc-based chemistries. Recent efforts emphasize safety enhancements and manufacturing expansions rather than new zinc-air breakthroughs.

- In 2025, Rayovac, often stylized as Ravoyac in sector references, specializes in zinc-air hearing aid batteries and has focused on supply chain stability and incremental performance tweaks amid sector growth. Developments are modest, prioritizing reliability for medical uses.

Report Scope

Report Features Description Market Value (2024) USD 128.9 Million Forecast Revenue (2034) USD 283.5 Million CAGR (2025-2034) 8.2% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Non-Rechargeable, Rechargeable), By Application (Hearing Aids, Military Devices, Safety Lamps, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Duracell, Ravoyac, Electric Fuel Battery Corporation, ZAF Energy System, Varta AG, GP Batteries, Phinenergy, Renata SA, AZA Battery Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Z-Air Batteries MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample

Z-Air Batteries MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Duracell

- Ravoyac

- Electric Fuel Battery Corporation

- ZAF Energy System

- Varta AG

- GP Batteries

- Phinenergy

- Renata SA

- AZA Battery

Our Clients

- 168830

- December 2025