Quick Navigation

Report Overview

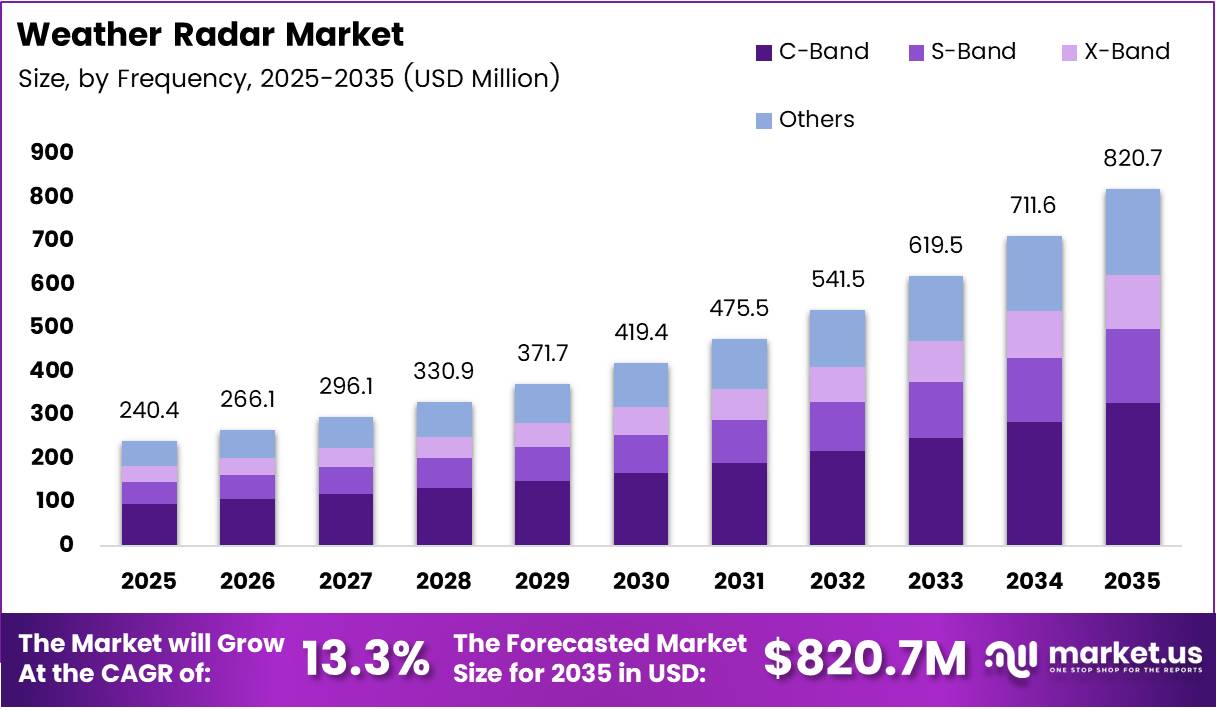

The Global Weather Radar Market size is expected to be worth around USD 820.7 Million by 2035 from USD 240.4 Million in 2025, growing at a CAGR of 13.3% during the forecast period 2026 to 2035.

Weather radar systems form the backbone of national meteorological infrastructure. These systems detect precipitation, wind patterns, and storm intensity by emitting microwave pulses and analyzing return signals. Governments, aviation authorities, and defense agencies rely on radar networks to protect lives, infrastructure, and commercial operations from weather-related disruptions.

The case for continued investment in weather radar is structural, not cyclical. Extreme weather events — including wildfires, flash floods, and hurricanes — now occur with greater frequency and economic cost. This forces governments to upgrade aging radar networks from legacy mechanically scanned systems to faster, more accurate technologies capable of real-time threat detection.

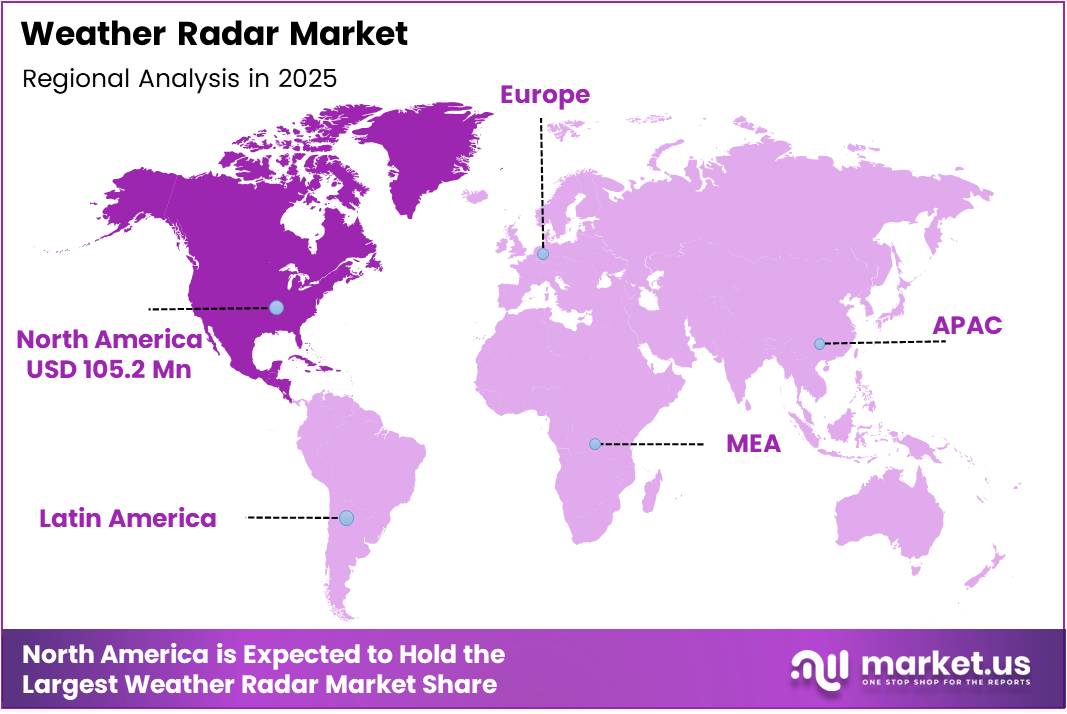

North America holds the leading regional position, accounting for 43.80% of global market share, valued at USD 105.2 Million. This dominance reflects decades of federally mandated radar network investment, particularly through NOAA and the WSR-88D system. These infrastructure commitments create a high reorder baseline that sustains revenue even outside major upgrade cycles.

Aviation safety mandates and military modernization programs represent two additional demand channels that operate independently of civilian meteorology budgets. As air traffic volume recovers and defense agencies prioritize situational awareness, radar procurement timelines compress — creating a shorter selling cycle for specialized manufacturers with proven system certifications.

In May 2024, Vaisala secured a contract worth approximately EUR 25 Million from Spain’s State Meteorological Agency (AEMET) to supply 18 dual-polarization C-band WRM200 weather radars. This single contract illustrates the scale of national upgrade programs now entering execution phase across Europe — a signal that government budget commitments made post-COVID are converting into active procurement.

According to NOAA’s Advanced Technology Demonstrator program, phased-array weather radar reduces volume scan update intervals from 4–5 minutes to approximately 30 seconds — an improvement of roughly 8–10 times in temporal resolution. This performance gap between legacy and next-generation systems is the primary technical argument driving national radar modernization budgets globally.

According to a 2026 dual-polarization flood study published in Nature, a polarimetric ZDR-based algorithm reduced root-mean-square error of hourly precipitation totals by approximately 37% compared with the standard Marshall-Palmer relationship. This accuracy improvement directly reduces false alarms and missed flood warnings — translating to measurable reductions in emergency response costs for government buyers.

Key Takeaways

- The Global Weather Radar Market was valued at USD 240.4 Million in 2025 and is forecast to reach USD 820.7 Million by 2035.

- The market advances at a CAGR of 13.3% during the forecast period 2026 to 2035.

- By Platform, Land-Based systems dominate with a 67.1% market share in 2025.

- By Component, Transmitter leads the component segment with a 31.8% share.

- By Frequency, C-Band holds the largest frequency segment share at 38.5%.

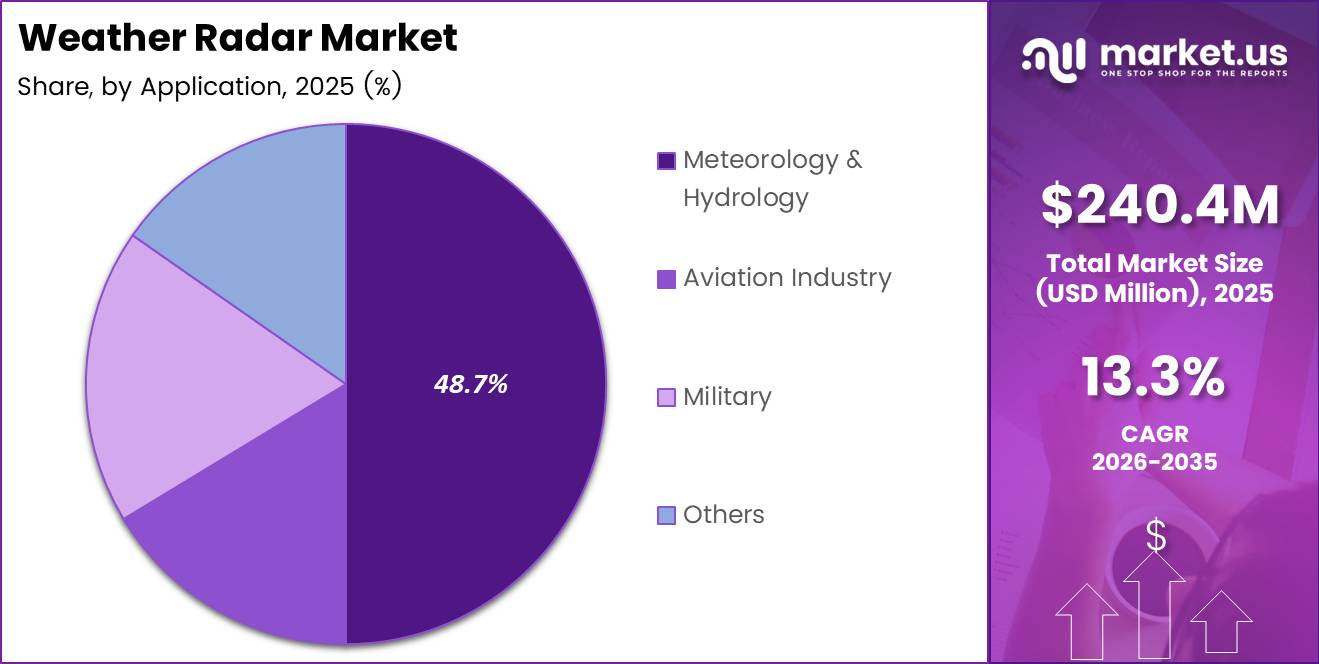

- By Application, Meteorology and Hydrology accounts for the largest share at 48.7%.

- North America leads all regions with a 43.80% share, valued at USD 105.2 Million in 2025.

Product Analysis

Land-Based dominates with 67.1% due to fixed-network government procurement requirements.

In 2025, Land-Based platforms held a dominant market position in the By Platform segment of the Weather Radar Market, with a 67.1% share. National meteorological agencies worldwide operate dense fixed radar networks that require periodic technology upgrades, creating a stable and recurring procurement base that airborne systems cannot replicate at comparable scale.

Airborne radar systems serve defense, maritime patrol, and airborne weather reconnaissance missions where land-based coverage is physically impossible. However, unit costs for airborne radar are substantially higher and procurement volumes remain limited to fleet-size constraints of military and specialized aviation operators, making this a niche but margin-rich sub-segment.

Component Analysis

Transmitter dominates with 31.8% due to its function as the core signal-generation unit.

In 2025, Transmitter held a dominant market position in the By Component segment of the Weather Radar Market, with a 31.8% share. The transmitter generates the high-power microwave pulses that determine a radar system’s range and detection capability. Upgrading from magnetron-based to solid-state transmitters represents the single largest cost driver in current modernization programs.

Antenna systems determine the spatial resolution and beam steering capability of a radar installation. The shift toward phased-array architectures requires electronically steered antenna panels rather than mechanically rotating dishes — a design change that increases per-unit antenna cost but eliminates mechanical failure points and enables sub-minute volume scans.

Receiver components process the reflected microwave signals returned from precipitation targets. Modern dual-polarization receivers must simultaneously handle horizontal and vertical signal channels, doubling processing complexity compared with single-polarization legacy systems and consequently raising per-unit receiver values.

Display systems present processed radar data to operators in meteorological offices, air traffic control centers, and military command posts. The migration to cloud-connected display platforms reduces hardware costs at the terminal level but shifts revenue toward software licensing and data services — a structural shift that changes how display vendors monetize their installed base.

Others in the component category include radomes, signal processors, power supplies, and data communication hardware. These ancillary components represent recurring replacement revenue because they degrade faster than primary radar hardware, giving component suppliers a reliable aftermarket alongside initial system contracts.

Frequency Analysis

C-Band dominates with 38.5% due to its balance of range, resolution, and cost efficiency.

In 2025, C-Band held a dominant market position in the By Frequency segment of the Weather Radar Market, with a 38.5% share. C-band systems operate at frequencies that deliver effective precipitation detection across ranges of 100–250 km, making them the standard choice for national weather networks. The AEMET contract with Vaisala for 18 C-band WRM200 radars in May 2024 illustrates that C-band remains the default specification for large government tenders.

S-Band radar operates at longer wavelengths that penetrate heavy precipitation with lower signal attenuation, making it the preferred choice for severe weather monitoring in tropical and high-rainfall regions. The WSR-88D network across the United States operates primarily in S-band, establishing a large installed base that anchors U.S. maintenance and upgrade expenditure.

X-Band radars offer higher spatial resolution at shorter ranges, making them suitable for urban flood monitoring, airport wind-shear detection, and portable field deployments. EWR Radar Systems supplied both C-band and X-band transportable systems to NOAA in January 2026, demonstrating that X-band fills operational gaps where fixed long-range systems cannot provide adequate local resolution.

Others in the frequency segment include Ka-band and Ku-band systems used primarily in airborne and satellite-linked applications. These higher-frequency systems offer narrow-swath, high-resolution precipitation profiling — the Ku-band configuration covers a 245 km swath while the Ka-band covers 125 km — positioning them for specialized research and dual-frequency measurement programs rather than general network deployment.

Application Analysis

Meteorology and Hydrology dominates with 48.7% due to mandatory national weather monitoring obligations.

In 2025, Meteorology and Hydrology held a dominant market position in the By Application segment of the Weather Radar Market, with a 48.7% share. Every sovereign government maintains legal obligations to issue severe weather warnings and flood forecasts. These mandates translate directly into non-discretionary radar procurement budgets, insulating this application segment from economic downturns that affect other technology markets.

Aviation Industry applications span airport wind-shear detection, en-route weather avoidance, and approach-path precipitation monitoring. Regulatory authorities including the FAA and EASA require weather radar coverage at commercial airports above defined traffic thresholds — a compliance-driven demand source that expands automatically as new airports reach passenger volume triggers.

Military applications include battlefield weather support, missile range monitoring, and force protection from extreme weather events. Defense radar procurement operates on classified budget cycles with longer lead times but higher unit values and stricter performance specifications, creating a separate commercial track from civilian meteorological contracts.

Others in application include renewable energy site assessment, agricultural weather services, and research institutions. The renewable energy sector’s need for wind and solar resource data is converting from project-level contracted studies to permanent on-site radar installations — a shift that creates a new recurring revenue stream outside traditional meteorological and defense procurement channels.

Key Market Segments

By Platform

- Land-Based

- Airborne

By Component

- Transmitter

- Antenna

- Receiver

- Display

- Others

By Frequency

- C-Band

- S-Band

- X-Band

- Others

By Application

- Meteorology & Hydrology

- Aviation Industry

- Military

- Others

Drivers

Mandatory Weather Forecasting Requirements and Aviation Safety Standards Accelerate Radar Procurement

Governments face legally binding obligations to issue accurate severe weather warnings and protect civilian air traffic from weather hazards. These obligations are not optional budget lines — they are statutory requirements enforced by national meteorological agencies and aviation regulators. When legacy radar systems fail to meet required detection thresholds, procurement cycles accelerate regardless of broader fiscal conditions.

According to a 2025 quality-control study, standard radar quantitative precipitation estimation underestimated high-intensity rainfall events at or above 40 mm per hour and failed to detect many such events entirely. This documented detection failure creates a direct compliance liability for meteorological agencies still operating legacy systems — converting technical shortcomings into urgent upgrade mandates.

In September 2024, NOAA awarded EWR Radar Systems a contract to supply three transportable E800LP solid-state weather radar systems for fire-weather and post-wildfire hydrology research. This contract reflects a broader pattern: as extreme weather events generate documented economic losses, government agencies expand radar coverage beyond fixed national networks into mobile, event-responsive deployments — widening the addressable market for radar manufacturers.

Restraints

High System Costs and Infrastructure Gaps Limit Radar Network Expansion in Developing Markets

Weather radar systems carry significant capital requirements. Installation involves civil construction, tower infrastructure, power supply systems, and data communication links — costs that extend well beyond the radar hardware itself. For lower-income governments, these cumulative installation costs make national radar network deployment economically prohibitive without external grant funding or multilateral development bank financing.

Maintenance costs compound the initial investment burden. Radar components including transmitters, waveguides, and mechanical scan drives require scheduled replacement on multi-year cycles. In December 2024, the Cayman Islands Government contracted Leonardo Germany to upgrade the Kearney Gomez Doppler radar specifically because aging components had degraded system performance — a scenario that repeats across networks where maintenance budgets have been deferred, creating backlogs that deter rather than accelerate upgrade investment.

Remote and geographically complex regions face an additional structural barrier: limited telecommunications infrastructure cannot support real-time radar data transmission to central processing centers. Without reliable data links, even a correctly installed radar system cannot deliver operationally useful weather products — effectively negating the capital investment and discouraging procurement decisions in exactly the regions where coverage gaps are most acute.

Growth Factors

AI Integration, Dual-Polarization Expansion, and Renewable Energy Demand Open New Revenue Streams

The integration of artificial intelligence and big data analytics into weather prediction platforms fundamentally changes how radar data generates commercial value. AI algorithms can extract precipitation patterns, storm track predictions, and flood risk assessments from raw radar returns faster and at higher resolution than traditional processing pipelines — enabling radar network operators to offer premium data products to commercial buyers beyond standard government contracts.

According to a 2025 idealized data-assimilation study, assimilating phased-array weather radar reflectivity every 30 seconds instead of every 5 minutes increased assimilation frequency by a factor of 10 and significantly improved analysis accuracy for vertical velocity fields. This improvement in input data quality directly benefits AI-based forecast models, creating a compounding performance advantage for networks that upgrade to phased-array hardware alongside AI processing infrastructure.

Renewable energy developers require precise, site-specific wind and solar irradiance data to optimize turbine placement and grid dispatch decisions. Permanent X-band or C-band radar installations at wind farm sites provide this data continuously, converting a one-time project assessment cost into a recurring instrumentation contract. This application has not historically appeared in traditional radar procurement pipelines — meaning it represents incremental addressable market for manufacturers who develop specialized renewable-sector configurations.

Emerging Trends

Phased Array Technology and Cloud-Based Data Platforms Redefine Radar System Architecture

Phased-array radar systems eliminate the mechanical rotation drive that limits conventional radar scan speeds. By steering the beam electronically, phased-array systems complete full atmospheric volume scans in seconds — a capability that conventional dish radars cannot replicate regardless of software upgrades. Manufacturers investing in phased-array product lines now are positioning for the next major network replacement cycle, which government agencies in North America and Japan are already defining in procurement specifications.

According to a 2025 C-band radar benchmarking study, optimized specific differential phase (KDP) processing across a reflectivity range of 20 to 55 dBZ reduced uncertainties in rainfall rate retrievals for moderate to heavy precipitation. This improvement demonstrates that algorithmic advances in existing C-band hardware extend useful system life — a finding that influences both upgrade timing decisions and the commercial argument for software-driven radar enhancement contracts.

Cloud-based weather data platforms decouple radar data access from physical proximity to radar installations. Commercial users — including insurance underwriters, commodity traders, and logistics operators — can now subscribe to real-time radar data feeds without operating their own hardware. This distribution model converts radar network operators from hardware vendors into data service providers, expanding total addressable revenue well beyond the capital equipment sale.

Regional Analysis

North America Dominates the Weather Radar Market with a Market Share of 43.80%, Valued at USD 105.2 Million

North America commands 43.80% of the global weather radar market, valued at USD 105.2 Million in 2025. The United States operates the WSR-88D network — one of the world’s densest national radar infrastructures — funded through NOAA’s mandatory meteorological mandate. Federal investment continuity and active NOAA modernization programs sustain procurement volumes that far exceed those of any other single-country market.

Europe Weather Radar Market Trends

Europe maintains a well-coordinated radar network through EUMETNET’s OPERA program, which standardizes data exchange and system specifications across member states. National agencies in Spain, Germany, France, and the UK are executing dual-polarization upgrade cycles, with the AEMET-Vaisala EUR 25 Million contract for 18 C-band radars exemplifying the scale of active European procurement. Semiconductor transmitter adoption is also emerging through AEMET’s option for WRS300 systems.

Asia Pacific Weather Radar Market Trends

Asia Pacific represents the fastest-growing geographic opportunity for radar manufacturers. China, Japan, India, and South Korea operate large and expanding national radar networks driven by high exposure to typhoons, monsoon flooding, and severe convective storms. Japan Radio Co. demonstrated a prototype C-band dual-polarization phased-array radar in Namerikawa City in 2025, signaling that Asia Pacific is also a source of next-generation radar innovation, not merely a buyer of Western-designed systems.

Middle East and Africa Weather Radar Market Trends

The Middle East and Africa region presents a fragmented market where radar coverage density varies sharply between Gulf states with modern infrastructure and sub-Saharan nations with minimal installed networks. Gulf Cooperation Council governments are investing in weather radar as part of broader climate resilience and aviation expansion programs, while multilateral development funding remains the primary financing mechanism for Sub-Saharan deployments.

Latin America Weather Radar Market Trends

Latin America faces a persistent gap between weather risk exposure and radar network coverage. Brazil and Mexico operate the largest regional networks, with Brazil’s REDEMET aviation weather radar program providing partial tropical coverage. However, coverage gaps across Andean, Amazonian, and Caribbean zones remain significant. International climate finance programs increasingly include radar infrastructure as an eligible expenditure, gradually improving the financing environment for network expansion.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Collins Aerospace positions itself at the intersection of aviation weather radar and defense meteorological systems. Its integration within the broader RTX defense and aerospace portfolio gives it direct access to classified military procurement channels and airline fleet upgrade programs simultaneously. This dual-channel positioning reduces revenue concentration risk — a structural advantage over pure-play meteorological radar suppliers who depend almost entirely on civilian government contracts.

Honeywell International Inc. competes across both airborne weather radar for commercial aviation and ground-based weather sensing solutions. Honeywell’s installed base across global airline fleets creates a captive aftermarket for software updates, component replacements, and sensor recertification — revenue streams that sustain margins between major procurement cycles. This aftermarket density is difficult for new entrants to replicate without decades of fleet deployment history.

EWR Radar Systems Inc. has built a differentiated position around solid-state, containerized, and truck-mounted radar configurations that serve mobile and rapid-deployment use cases. The company’s sequential NOAA contracts — including delivery of seven container-based E800LP systems in July 2024 and three truck-mounted systems in January 2026 — demonstrate validated operational performance across multiple NOAA research programs, which functions as the most credible public-sector reference an emerging radar supplier can hold.

Enterprise Electronics Corporation specializes in weather radar systems and satellite ground receiving stations across meteorology, hydrology, research, and aviation markets. Leonardo’s January 2026 agreement to acquire EEC signals that larger defense and aerospace primes view specialized weather radar expertise as a strategic asset worth consolidating — an indication that independent niche suppliers in this sector face increasing acquisition pressure as the market scales.

Key players

- Collins Aerospace

- Honeywell International Inc.

- EWR Radar Systems Inc.

- Enterprise Electronics Corporation

- LEONARDO Germany GmbH

- Beijing Minstar Radar Co., Ltd.

- Vaisala Oyj

- GAMIC mbH

- FURUNO ELECTRIC CO., LTD.

- Telephonics Corporation

Recent Developments

- July 2024 – EWR Radar Systems announced delivery of seven shipping container-based E800LP solid-state weather radar systems. Each unit featured auto-lift towers, climate-controlled radomes, operator rooms, backup power, and additional meteorological sensors and communications equipment.

- October 2025 – EWR Radar Systems confirmed a new contract to supply six additional container-based E800LP solid-state dual-polarization weather radar systems to a defense customer in Southeast Asia. This order brought that customer’s total to 13 container-based E800LP systems.

- January 2026 – EWR Radar Systems confirmed delivery of three custom truck-based mobile E800LP weather radar systems — one C-band and two X-band — to NOAA’s National Severe Storms Laboratory. The delivery fulfilled the transportable radar contract awarded by NOAA in September 2024.

- January 2026 – Leonardo announced that its subsidiary Leonardo US Corporation had signed an agreement to acquire Enterprise Electronics Corporation (EEC). EEC is a US-based specialist in weather radar systems and satellite ground receiving stations serving meteorology, hydrology, research, and aviation markets.

- January 2026 – Leonardo stated that the closing of the EEC acquisition was expected in the first quarter of 2026. The acquisition is designed to strengthen Leonardo’s meteorology and environmental remote-sensing business led by Leonardo Germany.

- December 2025 – The Cayman Islands National Weather Service reported that Leonardo Germany completed the Kearney Gomez Doppler Radar upgrade ahead of schedule. The upgrade, valued at USD 622,260, is expected to extend the radar’s service life by more than a decade beyond its original 15-year design life.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 240.4 Million |

| Forecast Revenue (2035) | USD 820.7 Million |

| CAGR (2026-2035) | 13.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform (Land-Based, Airborne), By Component (Transmitter, Antenna, Receiver, Display, Others), By Frequency (C-Band, S-Band, X-Band, Others), By Application (Meteorology & Hydrology, Aviation Industry, Military, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Collins Aerospace, Honeywell International Inc., EWR Radar Systems Inc., Enterprise Electronics Corporation, LEONARDO Germany GmbH, Beijing Minstar Radar Co., Ltd., Vaisala Oyj, GAMIC mbH, FURUNO ELECTRIC CO., LTD., Telephonics Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |