Quick Navigation

Report Overview

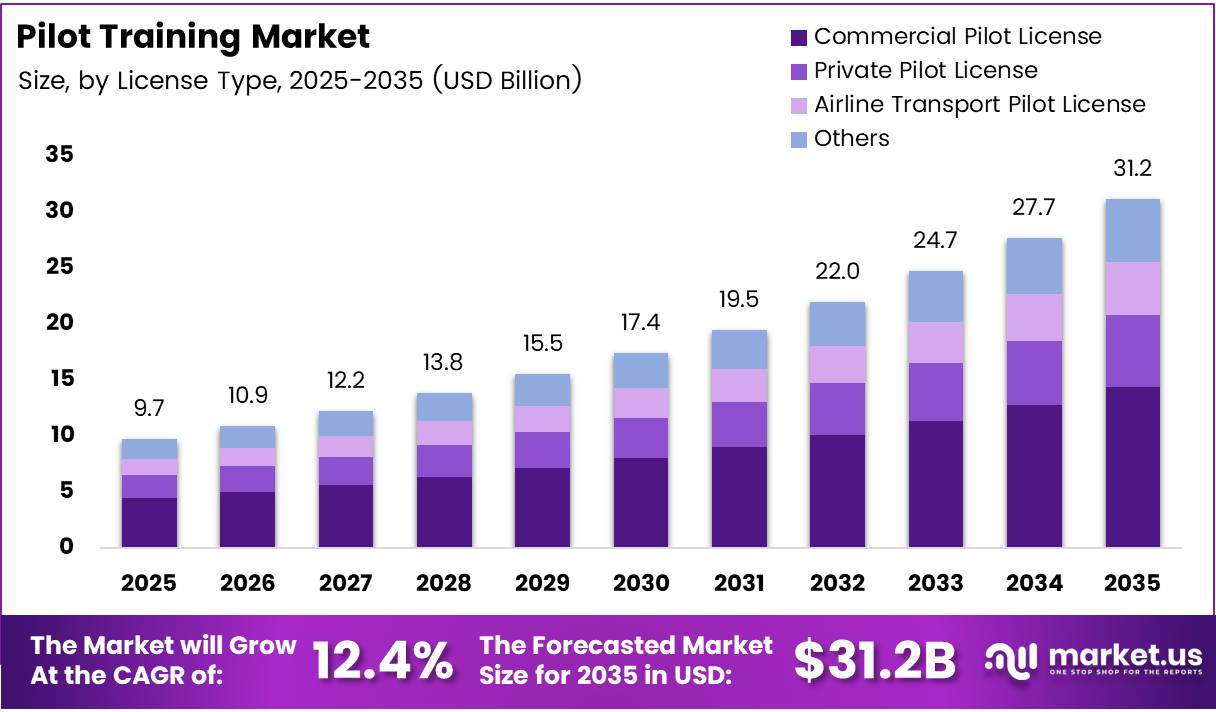

Global Pilot Training Market size is expected to be worth around USD 31.2 Billion by 2035 from USD 9.7 Billion in 2025, growing at a CAGR of 12.4% during the forecast period 2026 to 2035.

The pilot training market covers structured programs that prepare candidates for commercial, private, and military aviation careers. These programs span flight hours, simulator sessions, and ground instruction. Demand is structurally linked to airline fleet growth and mandatory certification requirements enforced by civil aviation authorities worldwide.

Commercial aviation has entered a sustained expansion phase following post-pandemic traffic recovery. Airlines across Asia Pacific, the Middle East, and Latin America are ordering new aircraft at record volumes. Each new aircraft added to a fleet creates a direct, non-negotiable requirement for certified crew — making pilot training a supply-constrained bottleneck, not a discretionary spend.

Aviation regulatory bodies including ICAO, FAA, and EASA require recurrent simulator checks, type-rating renewals, and competency-based assessments for all licensed pilots. These mandates create a recurring revenue base for training providers that is independent of airline profitability cycles. Regulatory compliance is therefore a structural demand floor, not a variable.

Simulator technology has matured to the point where full-flight simulators can replicate emergency scenarios, adverse weather, and system failures with high fidelity. Airlines now prefer simulator-based training for both cost efficiency and safety outcomes. This shift compresses delivery timelines and reduces the cost-per-training-hour — improving margins for established training providers with simulator assets.

In November 2025, Adani Defence Systems and Technologies announced the acquisition of approximately 73% of Flight Simulation Technique Centre — India’s largest independent pilot training company — for an enterprise value of approximately $97 million. This signals that institutional capital now views pilot training infrastructure as a strategic asset, not simply a service business.

According to IATA, commercial aviation achieved zero Loss of Control In-Flight accidents in 2025 across 38.7 million commercial flights — only the second time in recorded history this milestone was reached. This outcome reflects the compounding safety benefits of advanced simulator training and competency-based curricula, reinforcing regulatory confidence in structured training investment.

According to IATA, the member airline all-accident rate reached 0.72 per million flights in 2025, compared to 3.09 for non-IATA member carriers. This gap directly demonstrates that standardized, continuous training programs reduce operational risk — a data point that regulators and airline procurement teams use to justify mandatory training expenditures and certifications.

Key Takeaways

- The global Pilot Training Market was valued at USD 9.7 Billion in 2025 and is forecast to reach USD 31.2 Billion by 2035, at a CAGR of 12.4%.

- By Aircraft Type, Airplane holds the dominant share at 76.2% of the market in 2025.

- By License Type, Commercial Pilot License leads with 45.5% share, reflecting the highest volume of professional aviation certifications.

- By Training Program, Commercial Pilot Training Program accounts for 41.9% of the market, driven by airline demand for entry-level certified crew.

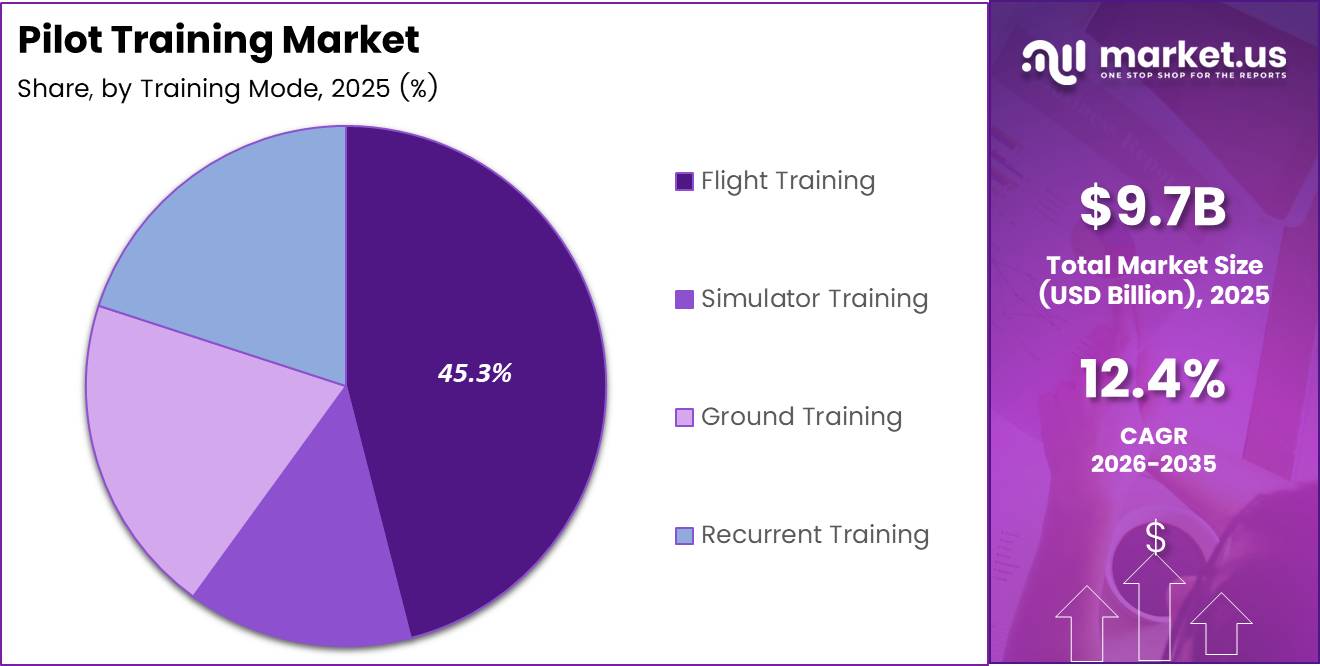

- By Training Mode, Flight Training holds the largest share at 45.3%, maintaining primacy despite rising simulator adoption.

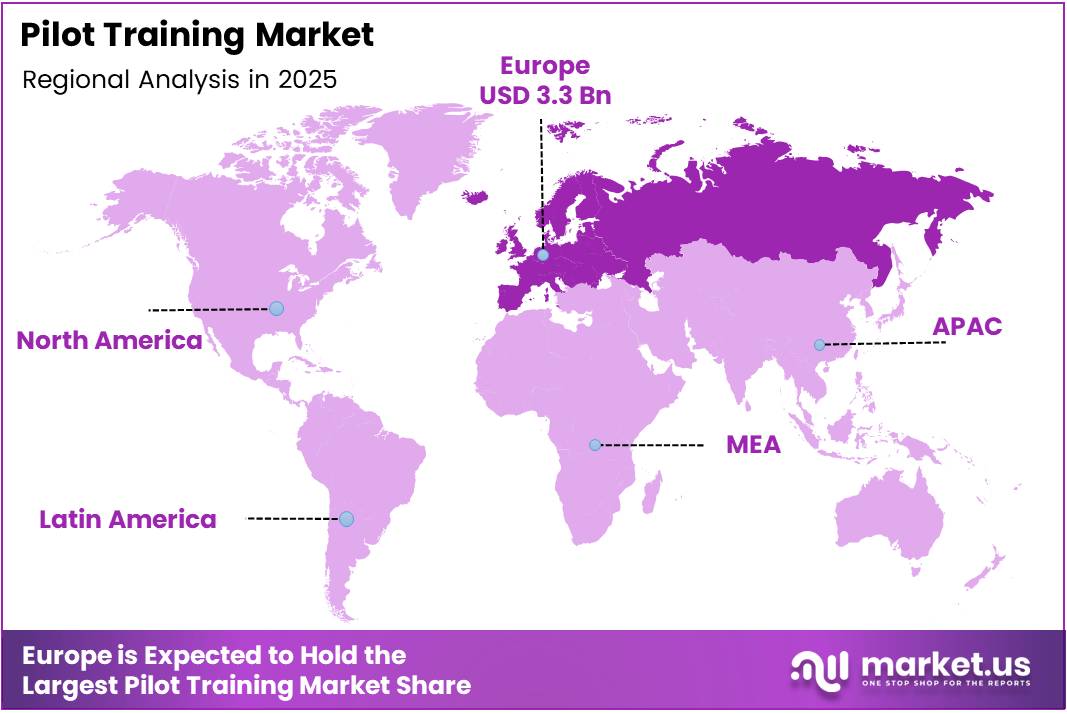

- Europe dominates regional market share at 34.70%, valued at approximately USD 3.3 Billion in 2025.

- In March 2025, L3Harris Technologies completed the sale of its Commercial Aviation Solutions business for $800 million to TJC L.P.

Aircraft Type Analysis

Airplane dominates with 76.2% due to high commercial fleet volume and regulatory demand.

In 2025, Airplane held a dominant market position in the By Aircraft Type segment of the Pilot Training Market, with a 76.2% share. Commercial and regional airlines operate fleets almost entirely composed of fixed-wing aircraft, creating a structurally larger certified crew requirement than any other aviation category. This concentration gives airplane training providers a recurring, regulation-backed demand base.

Helicopter training serves a structurally distinct buyer group — operators in offshore energy, emergency medical services, law enforcement, and military aviation. Consequently, helicopter training demand does not move in sync with commercial airline cycles. However, growth in offshore wind energy and urban air mobility projects signals expanding demand for rotary-wing qualifications in coming years.

License Type Analysis

Commercial Pilot License dominates with 45.5% due to airline entry-level certification volumes.

In 2025, Commercial Pilot License (CPL) held a dominant market position in the By License Type segment of the Pilot Training Market, with a 45.5% share. Airlines across Asia Pacific and the Middle East are actively running cadet programs to address near-term crew shortfalls, and CPL attainment is the prerequisite step. This structural demand from organized airline hiring pipelines sustains CPL program enrollment above all other license categories.

Private Pilot License (PPL) training serves general aviation enthusiasts, aspiring career pilots building initial flight hours, and business aviation operators. PPL programs are price-sensitive and geographically dispersed, typically delivered by smaller independent flight schools. However, PPL completions often serve as a feeder pipeline into CPL programs, making them a soft demand indicator for the broader market.

Airline Transport Pilot License (ATPL) represents the highest certification tier, required for pilots in command of commercial aircraft above certain weight thresholds. ATPL programs generate the highest revenue per candidate because of their extensive flight hour requirements and multi-stage examination structure. Airlines treat ATPL-qualified pilots as the most deployment-ready workforce segment, creating strong institutional demand for ATPL-specific training programs.

Others in the license category include multi-engine ratings, instrument ratings, and instructor certifications. While smaller in aggregate volume, these add-on qualifications generate margin-accretive revenue for training providers because they are purchased by already-enrolled candidates looking to expand their qualifications before or immediately after initial license attainment.

Training Program Analysis

Commercial Pilot Training Program dominates with 41.9% due to structured airline demand and cadet pipelines.

In 2025, Commercial Pilot Training Program held a dominant market position in the By Training Program segment of the Pilot Training Market, with a 41.9% share. Airlines have moved toward sponsoring structured cadet programs as a strategic response to forecast crew shortfalls, directing large cohorts into integrated commercial training tracks. This institutional purchasing behavior stabilizes enrollment volumes and extends average contract durations for training providers.

Cadet Pilot Training Program is the fastest-growing sub-segment within training programs, driven by airline-sponsored partnerships with flight academies. Cadets enter with zero experience and complete a full integrated curriculum through to CPL or ATPL — making this the highest-revenue-per-candidate program type. Airlines operating cadet programs effectively pre-buy trained crew, reducing external recruitment costs and improving crew retention rates.

Others in training programs cover type rating courses, recurrent proficiency training, and instructor development programs. These programs serve experienced pilots rather than new entrants, and their demand is driven by fleet renewals and regulatory recurrency requirements. They represent a more predictable, renewal-driven revenue stream compared to the enrollment-dependent new-pilot programs.

Training Mode Analysis

Flight Training dominates with 45.3% due to regulatory minimum flight hour requirements for licensing.

In 2025, Flight Training held a dominant market position in the By Training Mode segment of the Pilot Training Market, with a 45.3% share. Aviation authorities mandate minimum flight hours for every license category, and these hours cannot be substituted by simulator time alone during initial training. This regulatory constraint preserves flight training’s share despite the lower cost and higher scalability of simulator alternatives.

Simulator Training captures the largest share of recurrent and type-rating training hours, as airlines actively shift from live aircraft to full-flight simulators for cost and operational efficiency reasons. As global simulator capacity increases and simulator fidelity improves, this mode will continue to absorb a greater proportion of total training hours — putting pressure on training providers that rely solely on actual aircraft utilization revenue.

Ground Training delivers the theoretical foundation for all pilot certifications, covering subjects including air law, meteorology, navigation, and aircraft systems. It functions as the entry point into any training program, meaning enrollment in ground training is a leading indicator of future flight and simulator demand. E-learning platforms are now expanding ground training delivery beyond physical classrooms.

Recurrent Training across all modes is mandated by regulatory bodies to maintain active licenses. This segment produces recurring, predictable cash flows for certified training centers and is structurally detached from new-pilot enrollment trends. Airlines with large fleets generate a constant, calendar-driven demand for recurrent checks regardless of new hiring activity.

Key Market Segments

By Aircraft Type

- Airplane

- Flight Training

- Simulator Training

- Ground Training

- Recurrent Training

- Airbus 320

- Boeing 737

- Others

- Helicopter

By License Type

- Commercial Pilot License

- Private Pilot License

- Airline Transport Pilot License

- Others

By Training Program

- Commercial Pilot Training Program

- Cadet Pilot Training Program

- Others

By Training Mode

- Flight Training

- Simulator Training

- Ground Training

- Recurrent Training

Drivers

Mandatory Safety Regulations and Airline Expansion Drive Structural Demand for Certified Pilots

Airlines worldwide are expanding fleets at a pace that outstrips the current supply of certified crew. Each new aircraft entering service requires multiple fully rated pilots with current type endorsements. This fleet-crew ratio dynamic means training demand is structurally driven by capital expenditure decisions made years earlier — not simply by short-term hiring sentiment.

Regulatory compliance mandates from ICAO, EASA, and the FAA require airlines to maintain specific crew qualification standards, including recurrent simulator checks and proficiency assessments. According to the FAA, the fatal accident rate in U.S. general aviation reached 0.61 per 100,000 flight hours in FY2025 — the lowest since 1989 and below the stated reduction goal of 0.92. This outcome reflects decades of mandated training investment and validates continued regulatory pressure on training standards.

Advanced simulation technology now enables training providers to deliver higher-quality outcomes at lower cost per candidate. GE Aerospace’s AI-powered Blade Inspection Tool has halved inspection times and improved detection precision for critical engine components, demonstrating how AI integration across aviation operations creates parallel demand for pilots trained on technology-augmented aircraft systems. Training curricula must continuously update to reflect these operational changes, extending the program lifecycle and creating additional training touchpoints.

Restraints

High Training Costs and Instructor Shortages Limit Market Entry and Capacity Expansion

Pilot training programs carry among the highest per-candidate costs of any professional certification pathway globally. Integrated ATPL programs can exceed USD 100,000 per candidate when aircraft rental, simulator hours, examiner fees, and living costs are combined. This cost barrier filters out a large portion of qualified applicants, artificially constraining the supply of new pilots and limiting market volume growth below its demand-side ceiling.

The shortage of qualified flight instructors creates a parallel bottleneck. Experienced pilots with the hours and certifications required for instructing roles typically earn more in commercial airline positions, creating persistent attrition from training academies to airlines. According to IATA, IOSA-registered airlines recorded an all-accident rate of 0.98 per million flights in 2025, versus 2.55 for non-IOSA carriers. This gap demonstrates that training quality is directly tied to instructor standards — making the instructor shortage not just an operational problem but a safety risk.

Infrastructure constraints compound these pressures. Building or expanding certified training facilities requires significant capital investment in simulators, aircraft fleets, and regulatory approvals — processes that take years. Emerging markets with the strongest pilot demand often have the weakest domestic training infrastructure, forcing candidates to travel internationally for certification. This geographic mismatch raises total training costs further and delays workforce deployment timelines for airlines in high-growth regions.

Growth Factors

Emerging Market Academies, VR Technology, and Airline Partnerships Unlock New Revenue Channels

Training academies establishing operations in Southeast Asia, South Asia, and the Middle East are positioned to capture the structural demographic advantage these regions offer — large youth populations, expanding middle classes, and airlines placing multi-hundred-aircraft orders. Countries like India, Vietnam, and Saudi Arabia have announced national aviation expansion programs that include pilot training infrastructure as a strategic priority, creating government-backed demand for certified training capacity.

Virtual Reality and Augmented Reality technologies are beginning to change the economics of early-stage training. According to ePlaneAI, airlines deploying AI-powered predictive maintenance systems report up to a 98% decrease in unexpected groundings, extending component lifespans and reducing emergency repair costs. The same data infrastructure that enables predictive maintenance can feed adaptive training simulators — creating a feedback loop where operational aircraft data directly informs simulator scenario design and training outcomes.

Partnerships between airlines and training institutes are emerging as a structural market reshaper. When an airline co-invests in a training academy or guarantees cadet intake from a partner school, it reduces the financial risk of building new training capacity while securing a prioritized crew supply. These integrated pipeline arrangements shift the training market from a fragmented, academy-driven model toward an institutionalized, airline-anchored supply chain — creating competitive advantages for training providers with strong airline relationships.

Emerging Trends

AI Integration and Simulator-Led Models Redefine How Pilots Are Trained and Assessed

The shift from traditional flight-hours-led training toward simulator-primary curricula is now supported by regulatory bodies in multiple jurisdictions. Full-flight simulators allow training centers to expose candidates to emergency scenarios that are legally impermissible in live aircraft — engine failures on takeoff, hydraulic loss, windshear encounters — producing more comprehensively prepared pilots with fewer total flight hours required.

AI-driven performance monitoring is transforming how training providers assess candidate progress. Real-time analysis of pilot inputs, response times, and decision patterns allows instructors to identify skill gaps earlier and personalize remedial training before high-stakes proficiency checks. According to ePlaneAI, AI-driven flight path optimization using machine learning to process weather, air traffic, and aircraft performance data achieves fuel savings of 1–3% per flight. Pilots trained on these AI-integrated systems add operational value beyond regulatory compliance.

E-learning platforms are restructuring the delivery of ground school content, allowing candidates to complete theoretical training modules remotely and at their own pace. This decouples the geographic constraint from early-stage training, enabling academies to recruit from wider catchment areas before moving candidates to physical facilities for flight and simulator phases. Competency-based training models, which assess demonstrated skill rather than logged hours, are the regulatory direction of travel — favoring providers that invest in assessment technology over those relying on time-based curriculum structures.

Regional Analysis

Europe Dominates the Pilot Training Market with a Market Share of 34.70%, Valued at USD 3.3 Billion

Europe leads the global pilot training market with a 34.70% share, valued at approximately USD 3.3 Billion in 2025. EASA’s harmonized regulatory framework across member states creates a unified certification standard that training providers can serve from centralized academy locations. High airline density, mature infrastructure, and strong simulator capacity give European providers a structural cost and scale advantage over most other regions.

North America Pilot Training Market Trends

North America holds the second-largest share, supported by the FAA’s established regulatory framework and the world’s largest general aviation fleet. The U.S. regional airline sector faces acute pilot shortfalls driven by mandatory retirement age rules and ATP certificate requirements introduced under the Pilot Flying Qualifications Act. These structural supply pressures sustain high enrollment volumes at U.S. flight academies across both commercial and ATP training tracks.

Asia Pacific Pilot Training Market Trends

Asia Pacific represents the highest forward growth potential in the pilot training market, driven by fleet expansion across Chinese, Indian, and Southeast Asian carriers. China alone requires tens of thousands of additional certified pilots over the next decade, and domestic training capacity remains insufficient relative to projected demand. This supply-demand imbalance is redirecting airline investment toward building and acquiring training infrastructure across the region.

Middle East and Africa Pilot Training Market Trends

The Middle East is building pilot training infrastructure in parallel with aggressive fleet expansion at Gulf carriers. State-backed aviation authorities in the UAE and Saudi Arabia have identified domestic pilot training capacity as a strategic priority, supporting academy establishment through regulatory facilitation and capital. Africa remains in early-stage development, with most training candidates still traveling internationally for certification.

Latin America Pilot Training Market Trends

Latin America presents a developing market where aviation growth in Brazil, Mexico, and Colombia is creating localized demand for certified pilot training capacity. The region’s training infrastructure is concentrated in Brazil and Mexico, leaving other countries dependent on imported certification services. As low-cost carrier penetration increases across the region, training demand will outpace current domestic capacity, creating an entry opportunity for regional academy expansion.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

CAE Inc. holds a structurally dominant position in the global pilot training market through the combination of simulator manufacturing, certified training center operations, and long-term airline contracts. Its vertical integration — designing simulators and then operating them commercially — creates a cost structure and intellectual property moat that pure-play training providers cannot easily replicate. CAE’s network of training centers across every major aviation market gives airlines a single-vendor solution for global crew qualification.

BAA Training operates one of Europe’s largest independent flight academies, with a portfolio spanning CPL, ATPL, and type rating programs. Its strategic positioning in the European market benefits directly from EASA regulatory harmonization, which allows a candidate certified under BAA’s programs to operate commercially across all EU member states. This pan-European license portability increases the marketable value of BAA’s training products and supports premium pricing relative to non-EASA-aligned providers.

ATP Flight School has established a dominant footprint in the U.S. market by aligning its curriculum with ATP certificate requirements — the mandatory qualification introduced under U.S. law for first officers at regional airlines. By positioning itself as the primary pathway to the U.S. regional airline pipeline, ATP has converted regulatory compliance requirements into a structural enrollment advantage. Its airline partnerships and job placement track record function as differentiated marketing assets in a cost-sensitive candidate market.

FlightSafety International Inc. focuses on high-fidelity simulator-based training for commercial, business, and military aviation segments. Its technical depth in simulator operations and recurrent training programs serves the repeat-purchase segment of the market — experienced pilots requiring mandatory recurrency checks. This positions FlightSafety in a stable, recurring-revenue model that is less exposed to new-candidate enrollment volatility than integrated ab initio academies.

Key Players

- CAE Inc.

- BAA Training

- ATP Flight School

- FlightSafety International Inc.

- Lufthansa Aviation Training GmbH

- L3Harris Technologies Inc.

- Pan AM Flight Academy

- Airbus Flight Academy

- Thrust Flight

- Indra Sistemas S.A.

Recent Developments

- March 2025 — L3Harris Technologies completed the sale of its Commercial Aviation Solutions (CAS) pilot and aircrew training business to private equity firm TJC L.P. for $800 million cash. This divestiture signals a strategic realignment by L3Harris away from commercial aviation training toward its core defense and government markets, while TJC’s acquisition suggests institutional investor confidence in long-term pilot training demand fundamentals.

- December 2025 — Adani Enterprises completed the first phase of its acquisition of Flight Simulation Technique Centre (FSTC), securing a 39% effective stake. FSTC operates 11 full-flight simulators and 17 training aircraft, generated Rs 195 crore revenue in FY2024–25, and holds certifications from both DGCA and EASA — making it the most comprehensively accredited independent training platform in India.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.7 Billion |

| Forecast Revenue (2035) | USD 31.2 Billion |

| CAGR (2026-2035) | 12.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Aircraft Type (Airplane, Helicopter), By License Type (Commercial Pilot License, Private Pilot License, Airline Transport Pilot License, Others), By Training Program (Commercial Pilot Training Program, Cadet Pilot Training Program, Others), By Training Mode (Flight Training, Simulator Training, Ground Training, Recurrent Training) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CAE Inc., BAA Training, ATP Flight School, FlightSafety International Inc., Lufthansa Aviation Training GmbH, L3Harris Technologies Inc., Pan AM Flight Academy, Airbus Flight Academy, Thrust Flight, Indra Sistemas S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |