Quick Navigation

Report Overview

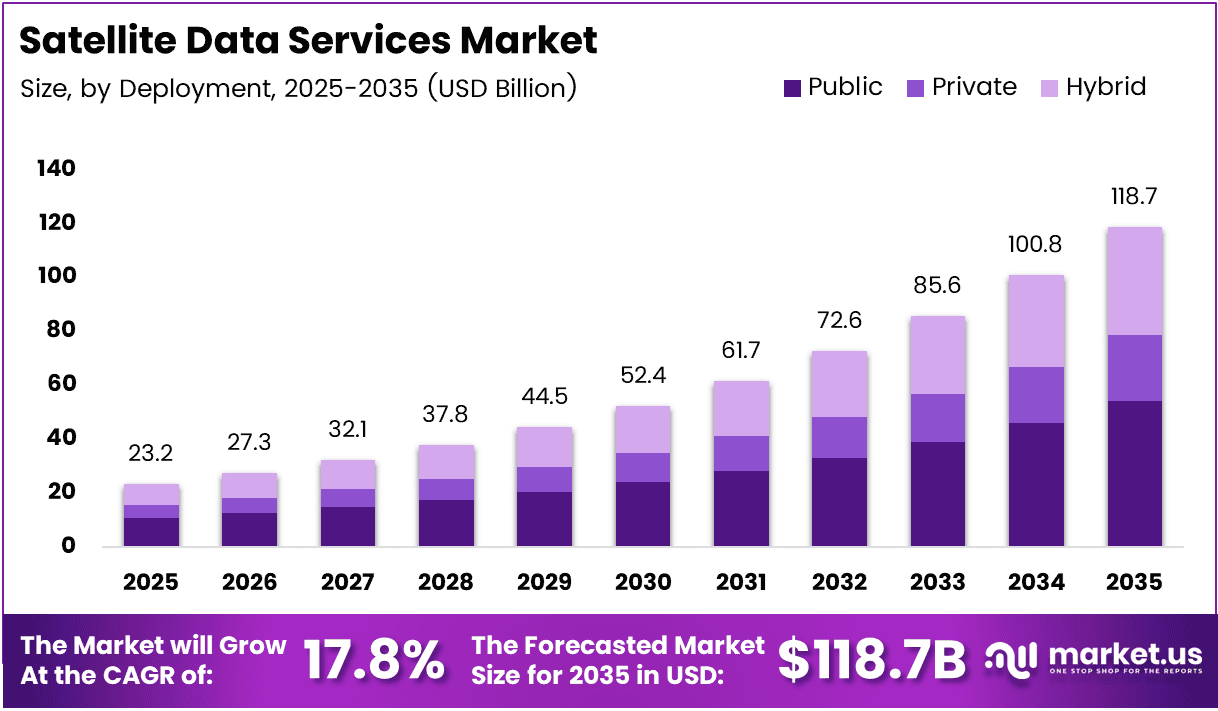

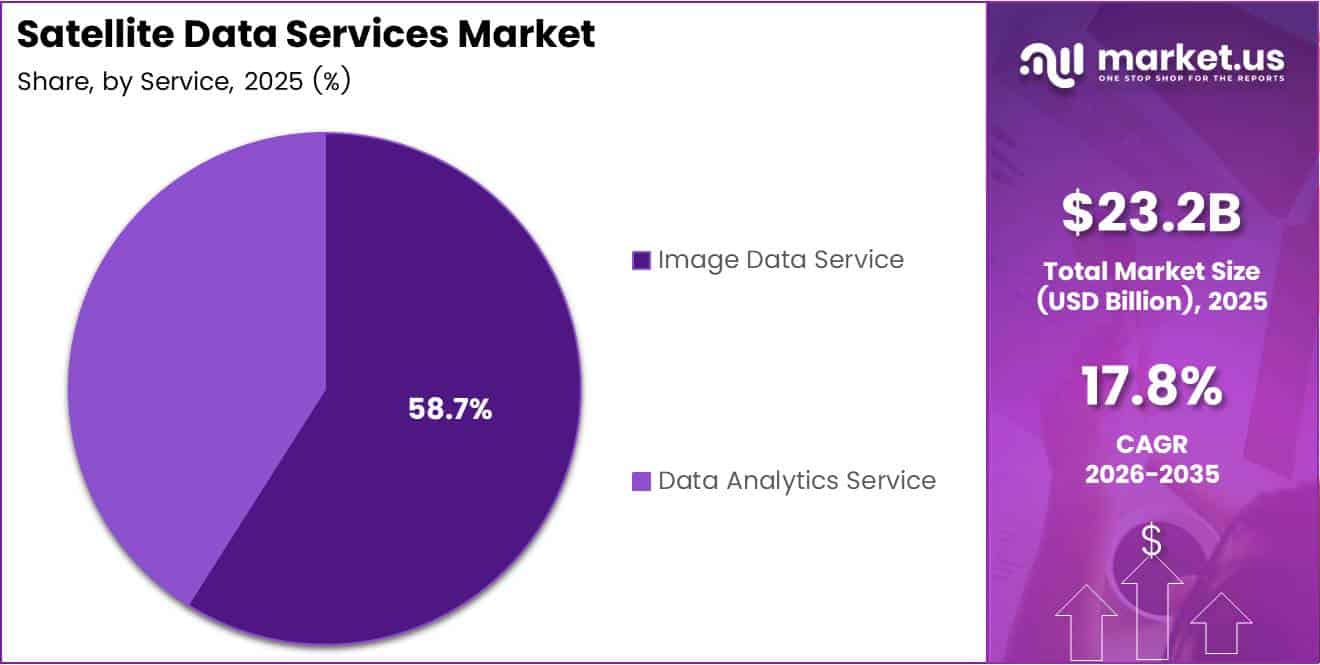

Global Satellite Data Services Market size is expected to be worth around USD 118.7 Billion by 2035 from USD 23.2 Billion in 2025, growing at a CAGR of 17.8% during the forecast period 2026 to 2035.

Satellite data services encompass the acquisition, processing, and delivery of earth observation imagery, geospatial analytics, and connectivity solutions from orbital platforms. Governments, defense agencies, agricultural operators, and energy companies rely on these services to make time-sensitive decisions that ground-based systems cannot support. The market spans public and private deployment models, serving commercial and military end-users across all major geographies.

The 17.8% CAGR reflects a structural shift — enterprise and government buyers no longer treat satellite data as supplemental intelligence. They embed it directly into operational workflows. This transition from periodic reporting to continuous, decision-grade data consumption compresses vendor sales cycles and raises switching costs, creating durable revenue streams for platform-first providers.

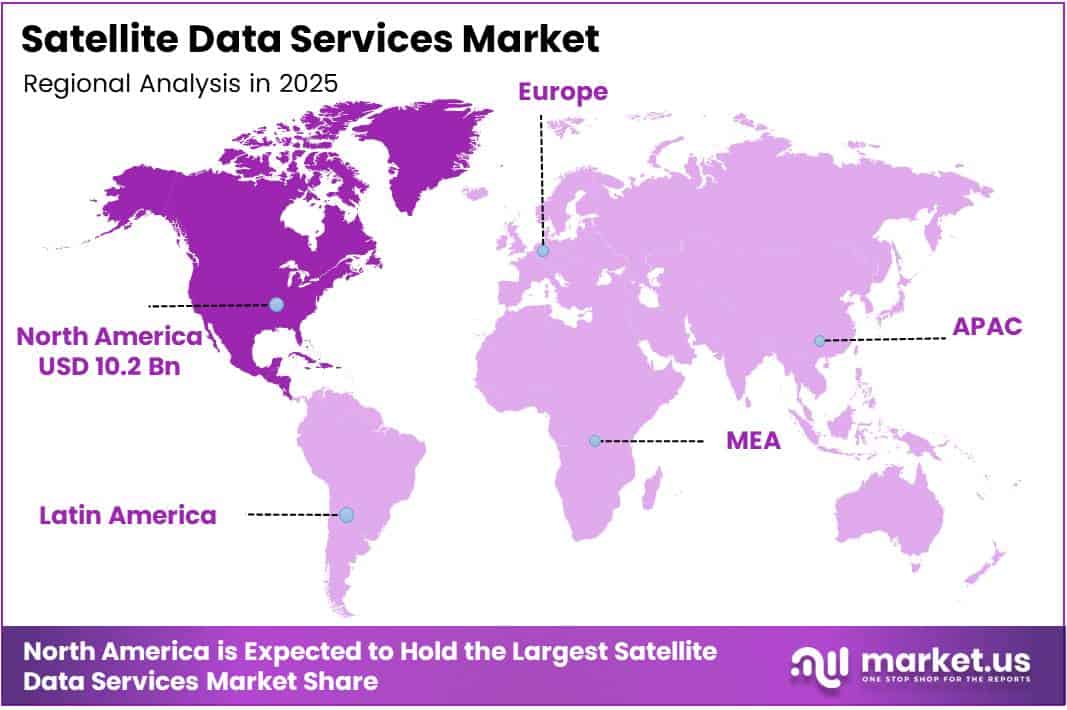

North America holds the largest regional share at 43.80%, valued at approximately USD 10.2 Billion in 2025. This position reflects decades of defense procurement infrastructure, mature commercial geospatial industries, and federal investment in space-based programs. These structural advantages now act as a template that other regions — particularly Western Europe and Asia Pacific — are actively replicating through domestic satellite programs.

Defense and security applications dominate by end-use application, capturing 34.8% share. This concentration signals that the satellite data market’s initial scaling engine is military and intelligence procurement — sectors characterized by long contract cycles, high data quality thresholds, and non-discretionary budgets. Commercial expansion into agriculture, infrastructure, and climate monitoring builds on this foundation, diversifying revenue beyond government cycles.

In April 2024, ICEYE signed a five-year contract with NASA under the Commercial Smallsat Data Acquisition (CSDA) Program to provide SAR data for Earth science — a development that illustrates how government agencies increasingly source satellite data commercially rather than building proprietary infrastructure. This shift reduces capital barriers for private vendors and accelerates data platform scaling across civilian and defense applications alike.

According to a study published in Frontiers in Agronomy, integrating UAV and satellite remote sensing with machine learning reduces irrigation costs by 20–25% and nitrogen application by up to 31 kg/ha without compromising crop productivity. This quantified efficiency gain explains why precision agriculture is becoming a primary commercial growth vector — buyers can now calculate direct ROI from satellite data subscriptions, rather than treating them as exploratory tools.

The commercial segment holds a 67.4% end-use share, confirming that private-sector demand now outpaces government procurement in volume terms. However, government contracts retain higher per-contract values, creating a two-speed market dynamic: commercial clients drive data volume and platform scale, while government contracts anchor revenue stability and fund constellation expansion for vendors serving both.

Key Takeaways

- The Global Satellite Data Services Market was valued at USD 23.2 Billion in 2025 and is forecast to reach USD 118.7 Billion by 2035.

- The market grows at a CAGR of 17.8% from 2026 to 2035.

- By Deployment, Public deployment leads with a 56.2% share in 2025.

- By Service, Image Data Service holds the dominant share at 58.7%.

- By Application, Defense & Security accounts for the largest application share at 34.8%.

- By End-use, the Commercial segment dominates with a 67.4% share.

- North America leads regional markets with a 43.80% share, valued at USD 10.2 Billion in 2025.

Product Analysis

Public deployment dominates with 56.2% due to government-mandated open data access and procurement scale.

In 2025, Public deployment held a dominant market position in the By Deployment segment of the Satellite Data Services Market, with a 56.2% share. Government agencies and defense departments use publicly deployed infrastructure to centralize data access across multiple agencies. This structure concentrates procurement budgets under a small number of large contracts, making public deployment the market’s highest-value revenue segment for vendors.

Private deployment serves enterprise operators who require proprietary data pipelines, controlled access, and commercially sensitive analytics. Energy companies, financial institutions, and large agricultural operators use private satellite data platforms to protect competitive intelligence derived from geospatial analysis. Moreover, private deployment creates higher per-user contract values than public platforms, making it a margin-rich segment despite its smaller overall share.

Hybrid deployment combines publicly sourced data layers with privately managed analytics environments, serving organizations that need both open data access and controlled proprietary outputs. Hybrid architectures are most common in defense-adjacent commercial operations — such as infrastructure monitoring and border logistics — where users require the data breadth of public networks and the security controls of private systems. Consequently, hybrid adoption expands as organizations scale from single-use cases to enterprise-wide geospatial operations.

Service Analysis

Image Data Service dominates with 58.7% due to foundational demand across defense, agriculture, and infrastructure.

In 2025, Image Data Service held a dominant market position in the By Service segment of the Satellite Data Services Market, with a 58.7% share. Raw and processed satellite imagery forms the data input layer for nearly every downstream application — from crop monitoring to military reconnaissance. This foundational role means image data demand scales in direct proportion to overall satellite service adoption, reinforcing its structural market lead across all geographies.

In September 2024, Planet Labs entered a multi-year partnership with Google Cloud to integrate satellite data into cloud-based geospatial analytics — a move that signals how Data Analytics Service providers are positioning analytics as the high-margin layer above raw imagery. As image data becomes increasingly commoditized through constellation expansion, analytics services carry higher per-unit value. Buyers willing to pay premium prices for processed intelligence rather than raw imagery will shift vendor revenue mix toward analytics over the forecast period.

Application Analysis

Defense & Security dominates with 34.8% due to non-discretionary budgets and high data reliability requirements.

In 2025, Defense & Security held a dominant market position in the By Application segment of the Satellite Data Services Market, with a 34.8% share. Military and intelligence agencies require continuous, high-resolution earth observation that commercial infrastructure cannot replicate at scale. This procurement concentration means defense contracts provide vendors with revenue predictability and funding for constellation upgrades that simultaneously benefit commercial product lines.

According to a study published in SATSAWB, satellite-based precision farming reduces pesticide usage by up to 30% and cuts input costs by up to 20% through variable-rate applications and site-specific crop management. This cost evidence drives Agriculture & Forestry adoption beyond early-adopter operators into mainstream commercial farming enterprises, making it one of the fastest-expanding application verticals outside defense in the current forecast period.

Energy & Utilities operators use satellite data to monitor pipeline integrity, track offshore asset conditions, and optimize grid infrastructure investments. This application segment benefits from the same high-consequence, low-tolerance-for-error requirements that characterize defense procurement — creating premium pricing conditions for vendors who can meet reliability and resolution thresholds.

Environmental & Climate Monitoring applications connect satellite data directly to regulatory compliance programs, carbon accounting frameworks, and disaster response logistics. Government agencies and multilateral institutions fund these use cases, creating stable public-sector revenue streams that are less cyclical than commercial application segments.

Engineering & Infrastructure Development uses satellite imagery and analytics for construction progress monitoring, land-use planning, and structural deformation analysis. The scalability of satellite coverage over large-area infrastructure projects — pipelines, roads, rail corridors — makes it cost-superior to drone or ground-based inspection alternatives at the national and continental scale.

Marine applications span vessel tracking, port operations management, and offshore weather intelligence. Satellite-derived Automatic Identification System (AIS) data gives maritime operators persistent vessel visibility beyond terrestrial radar range, directly reducing cargo loss risk and improving fleet scheduling efficiency in open-ocean routes.

Others encompasses urban planning, insurance risk modeling, and telecom network planning — all early-stage but structurally supported by broader satellite data platform adoption. As satellite data platforms reduce per-query pricing through scale, marginal use cases in this category will convert from experimental to operational faster than current market models anticipate.

End-use Analysis

Commercial end-use dominates with 67.4% due to diverse private-sector applications and subscription platform adoption.

In 2025, Commercial end-use held a dominant market position in the By End-use segment of the Satellite Data Services Market, with a 67.4% share. Private enterprises across agriculture, energy, logistics, and financial services now consume satellite data at scale through API-driven and subscription-based platforms. This volume-led adoption creates data network effects — the more commercial users process data on a platform, the more valuable that platform’s analytics benchmarks become.

Government and Military end-use captures the remaining share but commands disproportionately high contract values relative to its user count. Defense ministries, civilian space agencies, and national mapping organizations require classified data pipelines and dedicated satellite tasking capacity that commercial platforms do not provide by default. Therefore, government contracts anchor vendor revenue floors even as commercial volumes grow at a faster absolute rate.

Key Market Segments

By Deployment

- Public

- Private

- Hybrid

By Service

- Image Data Service

- Data Analytics Service

By Application

- Defense & Security

- Energy & Utilities

- Agriculture & Forestry

- Environmental & Climate Monitoring

- Engineering & Infrastructure Development

- Marine

- Others

By End-use

- Commercial

- Government and Military

Drivers

Small Satellite Constellation Expansion and Government Space Investment Accelerate Real-Time Data Availability

Commercial small satellite constellations now deliver observation frequency that legacy single-satellite systems cannot match. According to XRTechGroup, a 28-satellite LEO constellation achieves up to 25 revisit passes per day over any point on Earth, compared to days between passes for a single-satellite system. This revisit density directly enables near-real-time earth observation for defense, agriculture, and energy operators — use cases that were technically impossible five years ago.

In September 2024, Planet Labs signed a three-year agreement with the German Space Agency (DLR) to provide Earth observation data including PlanetScope and RapidEye imagery. This contract reflects a broader pattern: national space agencies are outsourcing data acquisition to commercial constellations rather than funding sovereign satellite programs at full cost. Consequently, commercial vendors gain long-term, government-backed revenue while agencies access data at lower capital expenditure.

Government investments in space infrastructure now serve a dual function — funding sovereign capabilities and catalyzing private market demand. When a defense ministry mandates satellite-based intelligence inputs for operational planning, it creates procurement requirements that cascade through the supply chain to commercial data providers. This government-to-commercial demand transfer creates a structural floor under satellite data service revenue that persists regardless of short-term commercial budget cycles.

Restraints

High Deployment Costs and GPS Signal Vulnerabilities Constrain Reliable Satellite Data Operations

Satellite constellation deployment requires capital investment in launch vehicles, ground stations, and orbital insurance that most new market entrants cannot self-fund. This capital intensity concentrates supply among a small number of well-capitalized incumbents, limiting competitive pressure on pricing and creating access barriers for smaller commercial buyers who need customized data services rather than standard platform subscriptions.

According to IATA data, GPS signal loss events per 1,000 flights rose from 31 in 2022 to 56 in 2024, with a projected 59 events per 1,000 flights in 2025. This near-doubling of GPS disruption incidents exposes a critical vulnerability in satellite-dependent navigation and timing systems — not just in aviation, but across any application that relies on accurate satellite positioning, including precision agriculture, maritime routing, and infrastructure monitoring.

Regulatory barriers further compound operational constraints, particularly for cross-border satellite data services. Data sovereignty laws in several jurisdictions restrict where satellite imagery can be processed, stored, and transmitted — adding compliance overhead that increases operational costs for vendors serving international clients. Additionally, privacy regulations governing high-resolution imagery create approval delays that slow enterprise sales cycles and limit the speed at which new application verticals can commercialize satellite data.

Growth Factors

AI Integration, Climate Mandate Funding, and Emerging Market Connectivity Create New Revenue Layers

AI and big data analytics convert raw satellite data into decision-grade intelligence — shifting vendor value from data delivery to insight generation. According to IATA’s 2025 Safety Report, GPS spoofing incidents rose 193% and jamming events increased 67% in 2025 compared to 2023. This threat environment accelerates procurement of AI-powered signal validation and anomaly detection tools layered on top of satellite data platforms, opening a new cybersecurity-adjacent revenue stream for vendors with analytics capabilities.

Climate monitoring mandates from international regulatory bodies are creating dedicated funding pools for satellite-based environmental data services. Governments reporting under carbon accounting frameworks require continuous, auditable land-use and emissions data that only satellite observation can provide at the required geographic scale. This regulatory requirement converts what was previously a discretionary data purchase into a compliance necessity, structurally enlarging the addressable market without depending on discretionary budget cycles.

Satellite-based internet connectivity targets regions where terrestrial broadband infrastructure investment is economically unviable. As LEO constellations increase coverage density, per-terminal equipment costs decline — making satellite internet commercially viable for agricultural communities, remote industrial sites, and maritime operators in underserved geographies. Each new connectivity subscriber also becomes a potential consumer of value-added satellite data services, compounding the addressable market beyond raw connectivity revenue.

Emerging Trends

High-Resolution Near-Real-Time Imaging and Cloud-Based Processing Redefine Satellite Data Platform Economics

In October 2025, Planet Labs introduced its “Owl” satellite targeting near-daily 1-meter resolution imagery, with a demo launch planned for late 2026. This resolution threshold — near-daily at sub-meter scale — moves satellite imagery from a monitoring tool into an operational one. Buyers who previously refreshed data weekly can now trigger decisions based on imagery delivered within hours, compressing the competitive advantage window for early-access platform subscribers.

Cloud-based satellite data processing eliminates the historical requirement for dedicated on-premise infrastructure to handle large geospatial datasets. Vendors who transition users onto cloud processing architectures reduce their own data delivery costs while increasing buyer platform stickiness — cloud-hosted workflows are significantly harder to migrate than file-based data subscriptions. This dynamic favors vendors who can offer integrated cloud analytics platforms over those selling imagery on a per-image basis.

Partnerships between space agencies and private companies are accelerating capability transfer in both directions — agencies gain access to commercial constellation capacity, while private vendors gain government credibility and long-term contract visibility. This convergence reshapes competitive dynamics: the vendors best positioned in the next growth phase are not the largest satellite operators but those with the deepest integration into both government and commercial data workflows simultaneously.

Regional Analysis

North America Dominates the Satellite Data Services Market with a Market Share of 43.80%, Valued at USD 10.2 Billion

North America captures 43.80% of the global Satellite Data Services Market, valued at USD 10.2 Billion in 2025. The United States drives this position through defense procurement programs, commercial geospatial industry maturity, and NASA’s active Commercial Smallsat Data Acquisition initiatives. These institutional demand anchors sustain North America’s lead even as constellation capacity expands globally.

Europe Satellite Data Services Market Trends

Europe represents the second-largest regional market, supported by the European Space Agency’s Copernicus program and national defense modernization budgets across Germany, France, and the UK. Germany’s December 2025 commitment of a €1.7 Billion SAR reconnaissance contract through Rheinmetall and ICEYE signals that European defense ministries are actively funding commercial satellite data infrastructure at sovereign scale. This procurement signals Europe’s near-term trajectory toward higher market share.

Asia Pacific Satellite Data Services Market Trends

Asia Pacific combines the world’s largest agricultural land base with national space programs in China, India, Japan, and South Korea — creating multi-sector demand for satellite data services across crop monitoring, urban development, and maritime surveillance. China’s domestic constellation programs and India’s expanding commercial space licensing framework are building independent satellite data supply chains that will reshape the regional competitive landscape through the forecast period.

Middle East and Africa Satellite Data Services Market Trends

The Middle East combines high-value energy infrastructure monitoring requirements with sovereign wealth fund-backed space program investments, creating premium-priced procurement conditions for satellite data vendors. Africa’s agricultural monitoring and climate adaptation programs attract multilateral funding that converts into satellite data service contracts, particularly for environmental and crop productivity applications across sub-Saharan growing regions.

Latin America Satellite Data Services Market Trends

Latin America’s satellite data demand centers on agricultural productivity optimization — Brazil and Argentina hold two of the world’s largest commercial farming footprints, where satellite-based crop monitoring and soil analysis services address measurable yield gap problems. Infrastructure development monitoring across the Amazon basin and mineral extraction corridors adds a secondary application demand layer that supports market expansion beyond agriculture alone.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Maxar Technologies Holdings Inc. positions itself as a high-resolution imagery and geospatial intelligence provider serving defense, government, and commercial buyers. Its strategic advantage lies in owning both satellite assets and analytics platforms — a vertical integration model that allows Maxar to capture margin at multiple points in the satellite data value chain rather than competing on raw data pricing alone. This structure creates high switching costs for enterprise government clients.

Planet Labs PBC differentiates through constellation scale and revisit frequency rather than single-image resolution. By operating the world’s largest Earth observation constellation, Planet delivers data coverage breadth that individual high-resolution satellite operators cannot match economically. Its September 2024 Google Cloud partnership extends this strategy into cloud-based analytics, signaling a deliberate move toward platform revenue rather than data commodity sales — which carries significantly higher long-term margin potential.

Airbus SE applies its aerospace manufacturing scale and multinational government relationships to satellite data services, giving it procurement access in European defense and civil markets that pure-play data companies struggle to enter. Its integration of satellite imagery with broader aerospace intelligence products allows Airbus to offer bundled solutions that raise per-contract value beyond standalone data subscriptions. This cross-sector leverage is a durable competitive advantage in government procurement environments.

ICEYE has emerged as the leading commercial SAR satellite operator, combining aggressive constellation expansion — reaching 62 satellites after its November 2025 SpaceX deployment — with high-value government contracts including the €1.7 Billion German Armed Forces agreement. ICEYE’s Gen4 SAR satellite offering 16 cm resolution at 400 km coverage resets the technical benchmark for commercial radar imagery, directly threatening incumbent providers whose resolution capabilities lag this new standard.

Key players

- Maxar Technologies Holdings Inc.

- Planet Labs PBC.

- Airbus SE

- ICEYE

- L3Harris Technologies, Inc.

- Earth-i Ltd

- Geocento Limited

- NV5 Global, Inc.

- Satellite Imaging Corporation

- Satpalda

- Telstra

- Ursa Space Systems Inc.

- Geospatial Intelligence Pty Ltd

Recent Developments

- December 2024 – ICEYE closed a $65 million extension to its growth funding round, bringing its total 2024 funding to $158 million, with participation from Solidium Oy, BlackRock, Seraphim Space, and Plio Limited. This capital raise expanded ICEYE’s constellation development budget and accelerated its SAR satellite production pipeline heading into 2025.

- December 2025 – ICEYE raised €150 million in new funding plus €50 million in secondary transactions, reaching a €2.4 billion (~$2.8 billion) valuation, led by General Catalyst. The round confirmed ICEYE’s position as the highest-valued commercial SAR satellite operator globally and funded continued constellation and analytics platform expansion.

- October 2025 – Planet Labs introduced its “Owl” satellite targeting near-daily 1-meter resolution imagery, with a demo launch planned for late 2026. The Owl program represents Planet’s move into sub-meter resolution competitive territory previously dominated by larger, more expensive government-grade imaging satellites.

- September 2025 – ICEYE launched its Gen4 SAR satellite, offering 16 cm resolution, 400 km coverage, and improved data efficiency. The Gen4 platform resets commercial SAR performance benchmarks and directly expands ICEYE’s addressable contract base in defense and disaster response applications requiring centimeter-grade radar imagery.

- November 2025 – ICEYE deployed five new SAR satellites via SpaceX Transporter-15 mission, expanding its constellation to 62 satellites, supporting programs including Greek, Polish (MikroSAR), and BAE Systems initiatives. This deployment increased ICEYE’s per-location revisit capacity and strengthened its multi-government contract delivery commitments across Europe.

- December 2025 – ICEYE secured a €1.7 billion contract with the German Armed Forces via its Rheinmetall joint venture, covering SAR reconnaissance, AI analytics, and ground operations through 2030. This single contract represents the largest commercial SAR data services agreement disclosed publicly and anchors ICEYE’s European defense revenue through the first half of the forecast period.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 23.2 Billion |

| Forecast Revenue (2035) | USD 118.7 Billion |

| CAGR (2026-2035) | 17.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment (Public, Private, Hybrid), By Service (Image Data Service, Data Analytics Service), By Application (Defense & Security, Energy & Utilities, Agriculture & Forestry, Environmental & Climate Monitoring, Engineering & Infrastructure Development, Marine, Others), By End-use (Commercial, Government and Military) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Maxar Technologies Holdings Inc., Planet Labs PBC., Airbus SE, ICEYE, L3Harris Technologies Inc., Earth-i Ltd, Geocento Limited, NV5 Global Inc., Satellite Imaging Corporation, Satpalda, Telstra, Ursa Space Systems Inc., Geospatial Intelligence Pty Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |