Quick Navigation

Report Overview

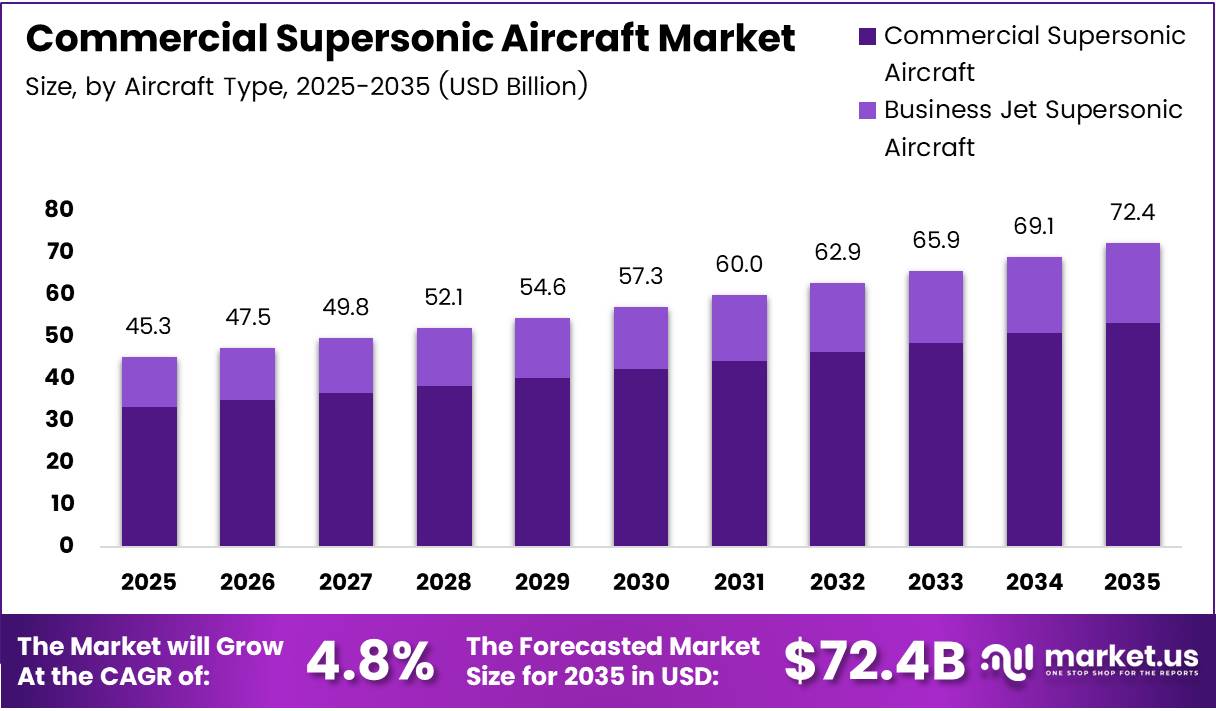

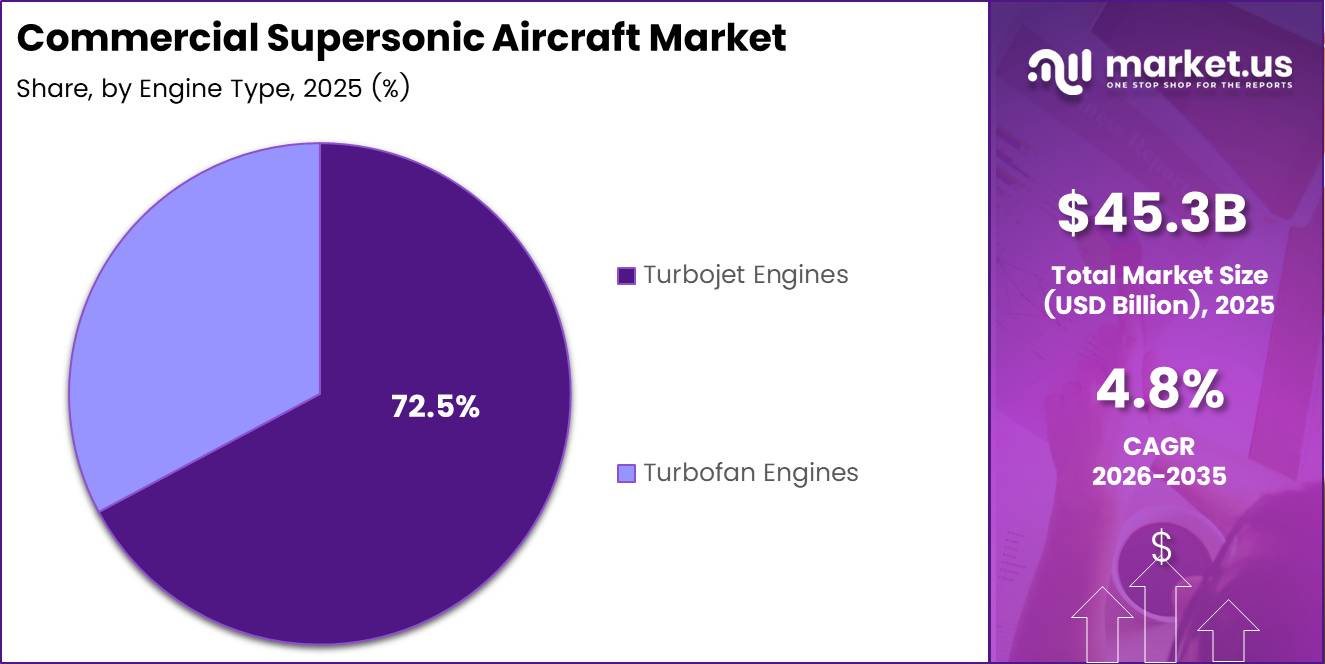

Global Commercial Supersonic Aircraft Market size is expected to be worth around USD 72.4 Billion by 2035 from USD 45.3 Billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

The commercial supersonic aircraft market covers the design, manufacture, and operation of passenger-carrying jets that travel faster than the speed of sound. This includes both commercial airline-grade supersonic jets and business-class supersonic aircraft. The market sits at the intersection of aerospace engineering, premium travel demand, and sustainable aviation technology.

Long-haul travel economics drive this market more than raw speed alone. Business travelers and premium-class passengers on transatlantic and transpacific routes represent the core demand pool. Airlines targeting these high-yield passenger segments view supersonic capability as a differentiation tool, not just an engineering milestone.

Aerospace companies have directed substantial capital toward supersonic propulsion and low-boom aerodynamics. New engine architectures and fuselage designs are solving problems that grounded the Concorde in 2003 — namely operating costs, noise, and fuel efficiency. These technical advances now make commercial viability a near-term possibility rather than a long-horizon ambition.

Government programs and regulatory bodies are actively reshaping the certification landscape for supersonic flight. The FAA and ICAO are reviewing noise and emissions standards specifically for supersonic aircraft, creating a clearer path for manufacturers seeking commercial certification. This regulatory attention signals that overland supersonic routes may open within this decade.

According to NASA, its X-59 aircraft is engineered to reduce the sonic boom from over 100 perceived loudness decibels (PLdB) — the level produced by Concorde — to approximately 75 PLdB. This 25+ PLdB reduction is commercially decisive: it is the technical threshold that could unlock overland supersonic routes currently banned across most jurisdictions, directly expanding the addressable route network for supersonic operators.

The 4.8% CAGR from 2025 to 2035 reflects a market where capital is accumulating ahead of commercial entry, not one where products are already scaling. Investors entering now face technology and certification risk, but position ahead of the consolidation phase that will follow first commercial service launches expected in the late 2020s.

Key Takeaways

- The Global Commercial Supersonic Aircraft Market was valued at USD 45.3 Billion in 2025 and is forecast to reach USD 72.4 Billion by 2035.

- The market advances at a CAGR of 4.8% during the forecast period 2026 to 2035.

- By Aircraft Type, Commercial Supersonic Aircraft leads with a 73.8% market share in 2025.

- By Engine Type, Turbojet Engines dominate with 67.2% share, reflecting the propulsion architecture preferred for high-speed cruise performance.

- By End-Use, Commercial Airlines Agencies hold the largest share at 54.1% in 2025.

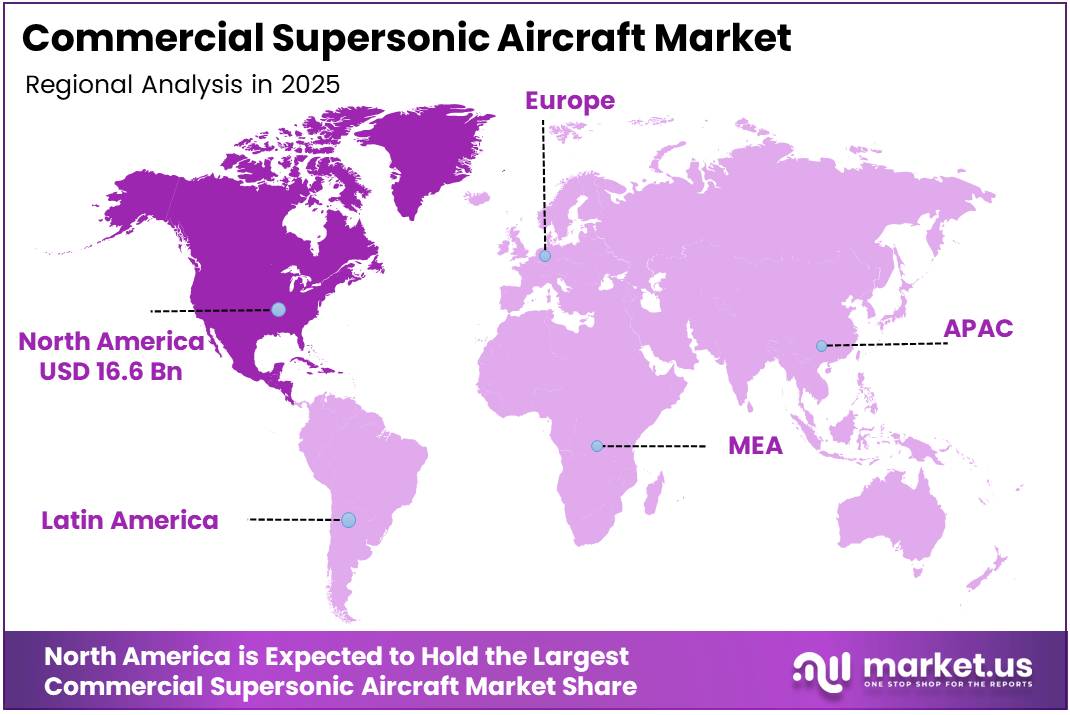

- North America leads all regions with a 36.80% share, valued at approximately USD 16.6 Billion in 2025.

Aircraft Type Analysis

Commercial Supersonic Aircraft dominates with 73.8% due to airline-scale procurement and route economics.

In 2025, Commercial Supersonic Aircraft held a dominant market position in the By Aircraft Type segment of the Commercial Supersonic Aircraft Market, with a 73.8% share. Airlines pursuing transatlantic and transpacific time savings drive procurement at a scale that business jet programs cannot match. Consequently, manufacturer R&D investment and certification timelines concentrate heavily on this sub-segment.

Business Jet Supersonic Aircraft serves the ultra-high-net-worth traveler segment, where cabin exclusivity and point-to-point speed justify premium pricing. However, smaller fleet sizes and niche route structures limit its revenue contribution relative to commercial aviation. Moreover, certification challenges for supersonic overland flight compress the viable route map for private operators until noise regulations evolve.

Engine Type Analysis

Turbojet Engines dominate with 67.2% due to superior thrust efficiency at supersonic cruise speeds.

In 2025, Turbojet Engines held a dominant market position in the By Engine Type segment of the Commercial Supersonic Aircraft Market, with a 67.2% share. Turbojet architecture delivers the high-pressure, high-velocity exhaust necessary to sustain Mach 1+ cruise without the bypass air losses that reduce turbofan efficiency at supersonic speeds. Therefore, existing supersonic programs continue to anchor their propulsion strategies around turbojet-derived designs.

Turbofan Engines carry strong appeal for next-generation supersonic programs because they offer meaningfully better fuel efficiency at lower supersonic speeds, particularly in the Mach 1.1–1.4 range. Additionally, turbofan architecture aligns more readily with sustainable aviation fuel compatibility mandates. Boom Supersonic’s Symphony engine program reflects this shift, targeting turbofan-based propulsion specifically to address fuel burn and emissions concerns that constrained earlier supersonic platforms.

End-Use Analysis

Commercial Airlines Agencies dominates with 54.1% due to high-volume procurement and scheduled route deployment.

In 2025, Commercial Airlines Agencies held a dominant market position in the By End-Use segment of the Commercial Supersonic Aircraft Market, with a 54.1% share. Scheduled carriers operating premium transatlantic routes represent the largest and most bankable buyer class, with fleet procurement decisions that anchor manufacturer production planning. Their financial commitment validates market demand in ways that smaller operators cannot replicate.

Private Aerospace Companies occupy the development and early deployment layer of this market, investing in supersonic platforms ahead of airline adoption at scale. Their role is structural: without private aerospace investment in demonstrators, propulsion systems, and manufacturing infrastructure, commercial airline deployment timelines would extend significantly. Therefore, private aerospace activity functions as a market-building force rather than a competing demand source.

Luxury Travel Operators differentiate through curated high-speed travel experiences, packaging supersonic transit with premium ground services and exclusive itineraries. This segment targets a clientele for whom time is the scarcest commodity. However, its market share remains constrained by fleet availability limitations — a condition expected to ease as first-generation commercial supersonic aircraft enter service later this decade.

Key Market Segments

By Aircraft Type

- Commercial Supersonic Aircraft

- Business Jet Supersonic Aircraft

By Engine Type

- Turbojet Engines

- Turbofan Engines

By End-Use

- Commercial Airlines Agencies

- Private Aerospace Companies

- Luxury Travel Operators

Drivers

Premium Traveler Demand and Aerospace Investment Accelerate the Commercial Supersonic Market

Business and premium travelers on long-haul routes treat flight time as a direct cost. A transatlantic crossing reduced from seven hours to three hours and thirty minutes translates into recoverable workdays for executive travelers. This economic logic converts travel time savings into a quantifiable value proposition, making supersonic service pricing power structurally stronger than standard business class upgrades.

Aerospace manufacturers have responded by directing capital toward the aerodynamic and propulsion advances needed to make supersonic flight commercially viable. New engine architectures address the fuel burn and noise deficiencies that ended the Concorde era. According to Boom Supersonic, XB-1 — its demonstrator aircraft — broke the sound barrier six times across two flights in January and February 2025, confirming that privately developed supersonic jets can achieve consistent supersonic performance without producing a ground-audible sonic boom.

The combination of private investment and measurable flight demonstration results narrows the gap between current aircraft certification standards and supersonic commercial entry requirements. Consequently, airlines that have placed pre-orders for supersonic aircraft gain strategic positioning in premium route markets before fleet availability becomes the binding constraint. The competitive window for early procurement commitments is compressing as program milestones advance.

Restraints

Noise Regulations and High Development Costs Constrain Supersonic Market Entry

International noise regulations prohibit supersonic flight over land across most major jurisdictions, restricting viable commercial routes to transoceanic corridors. This constraint directly limits the addressable route network for supersonic operators. Until regulatory bodies revise overland supersonic standards — a process tied to acoustic validation programs like NASA’s X-59 — market expansion remains geographically bounded.

Development costs for supersonic aircraft programs run significantly higher than equivalent subsonic programs due to the materials, propulsion systems, and structural requirements that sustained Mach 1+ cruise demands. High operational costs compound this — supersonic jets burn substantially more fuel per seat-mile than modern wide-body aircraft. These economics make supersonic service viable only in premium cabin configurations, narrowing the passenger market to the highest yield tier.

For new market entrants, the capital intensity of supersonic development creates a high barrier that filters out all but the best-funded programs. Established aerospace manufacturers hold a structural advantage through existing supply chains, regulatory relationships, and engineering depth. Therefore, smaller entrants must secure continuous funding cycles to sustain development timelines — a condition that introduces execution risk in a market where program delays are historically common.

Growth Factors

Sustainable Fuels, Low-Boom Technology, and Airline Partnerships Open New Revenue Paths

Sustainable aviation fuel (SAF) compatibility gives next-generation supersonic programs a credible answer to the emissions criticism that constrained Concorde-era aircraft. Supersonic jets designed to run on SAF can meet emissions targets that would otherwise exclude them from future regulatory frameworks. This compatibility shifts the emissions conversation from a market barrier to a manageable engineering specification.

Low-boom technology directly expands the geographic scope of viable supersonic routes. According to NASA, CarpetDIEM III testing in 2026 recorded an acoustic signature as low as 67 PLdB using an F-18 maneuver that simulated a quiet sonic boom — validating the measurement systems developed for X-59 evaluation. If commercial aircraft achieve comparable acoustic profiles, overland routes across North America, Europe, and Asia become regulatory candidates, multiplying the addressable market well beyond transoceanic corridors.

Strategic collaborations between supersonic manufacturers and major airlines convert technology programs into commercially funded development roadmaps. Airline pre-orders provide manufacturers with forward revenue visibility that attracts additional investment. Moreover, collaboration agreements transfer market intelligence on route economics, cabin configuration preferences, and passenger yield expectations — data that improves aircraft design decisions and reduces commercial risk for both parties.

Emerging Trends

Next-Generation Propulsion and Startup Activity Reshape the Competitive Landscape

Advanced propulsion development now sits at the center of supersonic program differentiation. Boom Supersonic’s Symphony engine — engineered specifically for the Overture aircraft — targets the fuel burn and thermal performance limitations of legacy turbojet designs. In December 2025, Boom launched a 42-megawatt Superpower turbine variant derived from the Symphony core, with Crusoe as launch customer for 29 units representing 1.21 gigawatts of capacity valued at USD 1.25 Billion — demonstrating that supersonic propulsion technology generates revenue applications beyond aviation.

New aerospace startups are entering the supersonic segment with focused programs targeting specific performance or market gaps rather than full commercial aircraft development. This startup activity compresses innovation cycles and introduces propulsion, materials, and avionics advances that established primes then evaluate for integration. According to Boom Supersonic, Boomless Cruise physics enable Overture to fly at speeds up to Mach 1.3 over land without an audible boom, cutting U.S. coast-to-coast flight time by up to 90 minutes versus current subsonic jets.

Certification testing activity is advancing across multiple programs simultaneously, creating a body of regulatory precedent that will define the commercial supersonic operating framework. Early test results from NASA and private programs establish acoustic and emissions benchmarks that regulators can reference when writing formal certification standards. Manufacturers that participate actively in this testing phase gain procedural familiarity and technical credibility that translates directly into faster regulatory approval timelines.

Regional Analysis

North America Dominates the Commercial Supersonic Aircraft Market with a Market Share of 36.80%, Valued at USD 16.6 Billion

North America holds a 36.80% share valued at USD 16.6 Billion, anchored by the presence of NASA’s active X-59 low-boom program, the FAA’s ongoing supersonic certification rulemaking, and the highest concentration of funded supersonic developers globally. This regulatory and R&D infrastructure creates a self-reinforcing advantage that other regions have not yet replicated.

Europe Commercial Supersonic Aircraft Market Trends

Europe’s supersonic market interest connects directly to transatlantic route economics, where carriers on London, Paris, and Frankfurt corridors serve the highest-yield business traveler volumes. However, European environmental and noise regulations impose stricter constraints than the current U.S. framework, meaning that European route clearance will likely follow North American regulatory approvals rather than lead them.

Asia Pacific Commercial Supersonic Aircraft Market Trends

Asia Pacific represents a structurally large opportunity for supersonic aviation given the volume of ultra-long-haul routes connecting major financial centers — Tokyo, Singapore, Sydney, and Hong Kong. National aerospace programs in Japan, including JAXA’s research contributions, add a domestic technology development dimension. However, route distances and airport infrastructure complexity create adoption timelines that trail North America and Europe.

Middle East and Africa Commercial Supersonic Aircraft Market Trends

The Middle East’s position as a global aviation hub — led by carriers operating some of the world’s highest premium cabin seat densities — creates a logical fit for supersonic service on Europe and Asia routes. Gulf carriers’ demonstrated willingness to invest in premium fleet differentiation positions the region as an early adoption candidate once commercial supersonic aircraft achieve certification and fleet availability.

Latin America Commercial Supersonic Aircraft Market Trends

Latin America’s supersonic market development remains early-stage, constrained by lower premium travel volumes and limited domestic aerospace manufacturing capability. However, transoceanic routes from São Paulo and Mexico City to European hubs align well with supersonic’s time-savings value proposition. Regional adoption will depend on global fleet availability and the unit economics that first-generation commercial supersonic operators establish on primary routes.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lockheed Martin Corporation brings decades of high-speed aircraft development — including its work on classified hypersonic programs — into the commercial supersonic space. Its engineering depth in low-observable aerodynamics and advanced propulsion integration positions it to address the noise reduction and structural performance challenges that define next-generation supersonic design. This foundation gives Lockheed a credibility advantage when engaging with defense-adjacent supersonic programs.

Northrop Grumman Corporation applies its advanced systems integration capabilities to supersonic aircraft programs, drawing on experience across high-speed platforms and aerospace structures. The company’s supply chain depth and manufacturing scale allow it to participate across multiple supersonic program tiers — from component supply to systems integration. This positions Northrop Grumman as a structural enabler of the broader ecosystem rather than solely a prime developer.

Hermeus Corporation focuses specifically on hypersonic and high-supersonic aircraft development, targeting Mach 5 point-to-point passenger transport as its long-term objective. Its accelerated hardware development methodology — building and testing rapidly rather than following traditional aerospace program timelines — distinguishes its approach from legacy primes. This positions Hermeus as the market’s clearest signal of where supersonic aviation’s technology frontier is moving post-2030.

United Aircraft Corporation contributes supersonic development capability from Russia’s established aerospace manufacturing base, with historical design experience in high-speed commercial aviation. Its participation reflects the global distribution of supersonic engineering expertise, though geopolitical considerations increasingly shape its ability to access Western supply chains, certification bodies, and airline customers in key commercial markets.

Key Players

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Hermeus Corporation

- United Aircraft Corporation

- Japan Aerospace Exploration Agency

- National Aeronautics and Space Administration

- Boom Technology Inc.

- Aerion Corporation

- Baykar Technology

- Dawn Aerospace Limited

- Reaction Engines Ltd.

- Spike Aerospace Inc.

- Exosonic Inc.

- Hypersonix Launch Systems Ltd.

- Virgin Galactic

- EON Aerospace Inc.

Recent Developments

- December 2025 — Boom Supersonic closed a $300 million funding round led by Darsana Capital Partners, with participation from Altimeter Capital, ARK Invest, Bessemer Venture Partners, Robinhood Ventures, and Y Combinator, valuing the company at approximately $1.5 billion post-money. Total funding since inception now exceeds $700 million, with Symphony core testing at Colorado Air and Space Port targeted for mid-2026.

- October 2025 — NASA’s X-59 quiet supersonic aircraft completed its first test flight over the California desert, cruising at Mach 1.42 at 55,000 ft altitude. The flight advances NASA’s mission to validate low-boom acoustic technology, with data from this program intended to support FAA rulemaking on overland supersonic flight.

- 2026 — During CarpetDIEM III testing, an F-18 inverted dive maneuver simulating a quiet sonic boom produced an acoustic signature as low as 67 PLdB on the ground, validating measurement systems developed for X-59 evaluation. This result confirms that ground-level acoustic measurement infrastructure can reliably capture the quiet boom signatures required for regulatory certification evidence.

- 2024 — Boom Supersonic completed construction of the Overture Superfactory in Greensboro, North Carolina — a LEED-certified manufacturing facility designed to scale production to 66 Overture aircraft per year. The facility represents a $6 billion investment expected to generate 2,400 jobs by 2040, establishing the physical manufacturing base needed for commercial-scale supersonic aircraft production.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 45.3 Billion |

| Forecast Revenue (2035) | USD 72.4 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Aircraft Type (Commercial Supersonic Aircraft, Business Jet Supersonic Aircraft), By Engine Type (Turbojet Engines, Turbofan Engines), By End-Use (Commercial Airlines Agencies, Private Aerospace Companies, Luxury Travel Operators) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Lockheed Martin Corporation, Northrop Grumman Corporation, Hermeus Corporation, United Aircraft Corporation, Japan Aerospace Exploration Agency, National Aeronautics and Space Administration, Boom Technology Inc., Aerion Corporation, Baykar Technology, Dawn Aerospace Limited, Reaction Engines Ltd., Spike Aerospace Inc., Exosonic Inc., Hypersonix Launch Systems Ltd., Virgin Galactic, EON Aerospace Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |