Quick Navigation

Report Overview

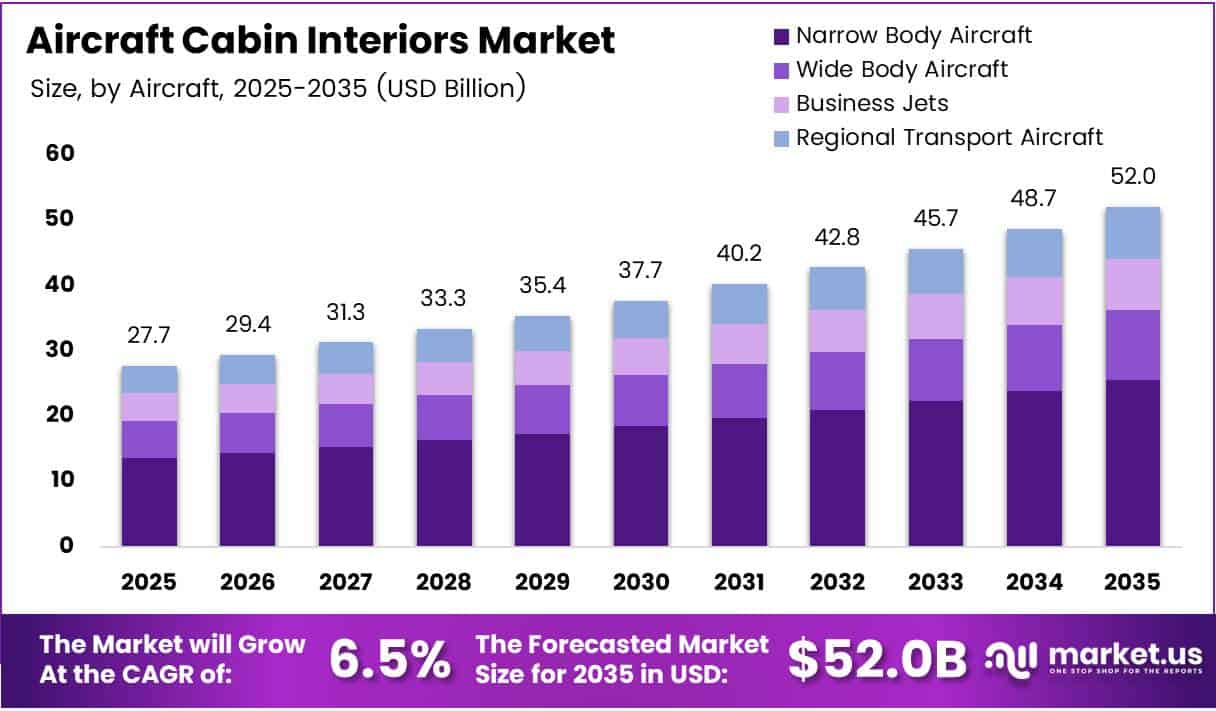

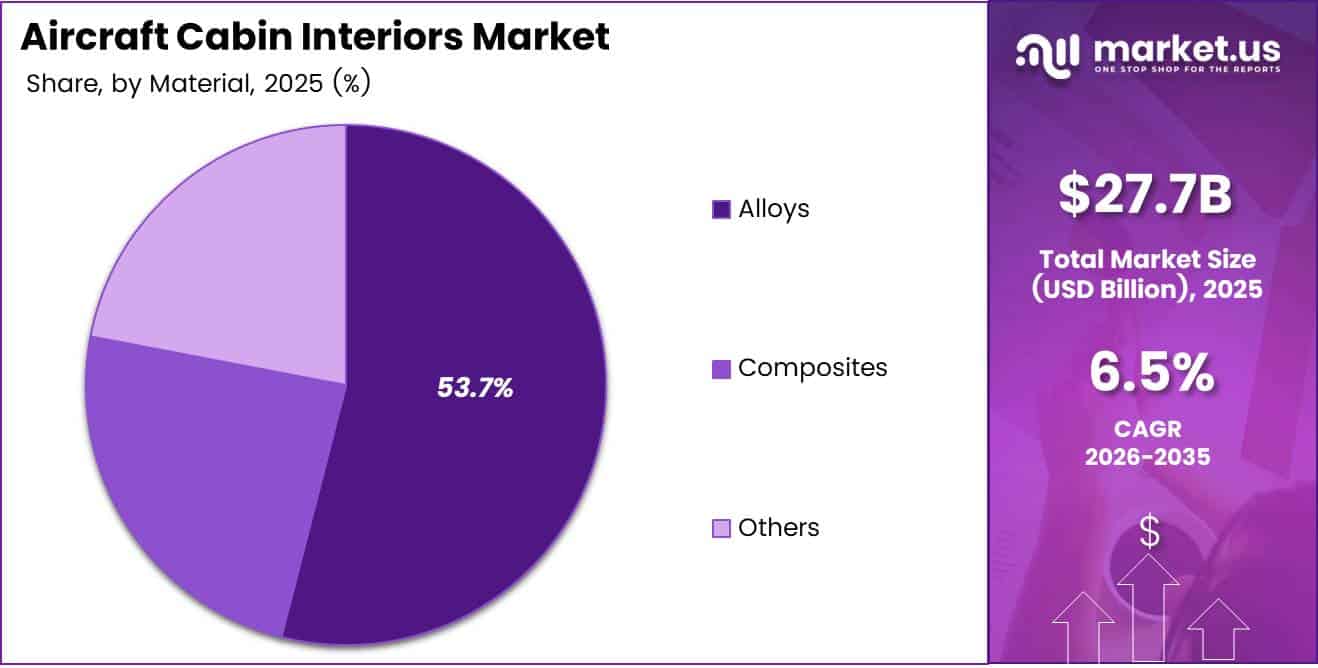

The global Aircraft Cabin Interiors Market size is expected to be worth around USD 52.0 billion by 2035 from USD 27.7 billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

Aircraft cabin interiors encompass every structural and experiential element inside a commercial or business aircraft — from seating and lighting to galleys, lavatories, stowage, and in-flight entertainment systems. Airlines treat cabin interiors as both a cost management lever and a brand asset, making them central to fleet strategy decisions.

The aftermarket segment commands majority spending, as airlines continuously retrofit existing fleets rather than wait for new aircraft deliveries. This retrofit cycle — driven by aging interiors, passenger expectation shifts, and fuel efficiency targets — creates a durable, recurring revenue base that insulates the market from new aircraft order fluctuations.

Fleet modernization programmes are accelerating across both legacy and low-cost carriers. In September 2024, Air India commenced a $400 million interior retrofit programme covering 67 legacy aircraft, beginning with 27 A320neos — signaling how large carriers now treat cabin upgrades as investment-grade fleet decisions rather than routine maintenance.

Material choice sits at the core of cabin economics. Alloys — particularly aluminum — dominate because they balance structural strength with weight control at a cost that composites cannot yet match at scale. However, composite adoption is rising as unit costs fall and fuel savings justify the premium.

According to simpliflying.com, 97% of an aircraft seat’s total environmental footprint occurs during its operational use phase, driven by the fuel required to carry its weight in service. This figure reframes cabin weight reduction from an engineering preference into a financial and regulatory imperative — airlines that ignore seat weight carry measurable cost penalties on every flight cycle.

According to eplaneai.com, Southwest Airlines’ cabin interior retrofit saved 6 million gallons of fuel in a single year — equivalent to approximately $36 million in annual fuel cost savings. This outcome demonstrates that cabin investment delivers compounding returns, making the financial case for retrofit programmes far stronger than upfront cost analysis alone suggests.

Key Takeaways

- The global Aircraft Cabin Interiors Market was valued at USD 27.7 billion in 2025 and is forecast to reach USD 52.0 billion by 2035.

- The market grows at a CAGR of 6.5% over the forecast period 2026 to 2035.

- By Material, Alloys hold the dominant share at 53.7%, led by aluminum and steel alloy applications.

- By Type, Aircraft Seating leads with 32.8% share, reflecting continued investment in passenger-facing cabin upgrades.

- By Aircraft, Narrow Body Aircraft accounts for 48.3% share, driven by high fleet volumes among low-cost and regional carriers.

- By End-use, the Aftermarket segment holds the largest share at 67.2%, underpinned by active fleet retrofit and cabin refurbishment programmes.

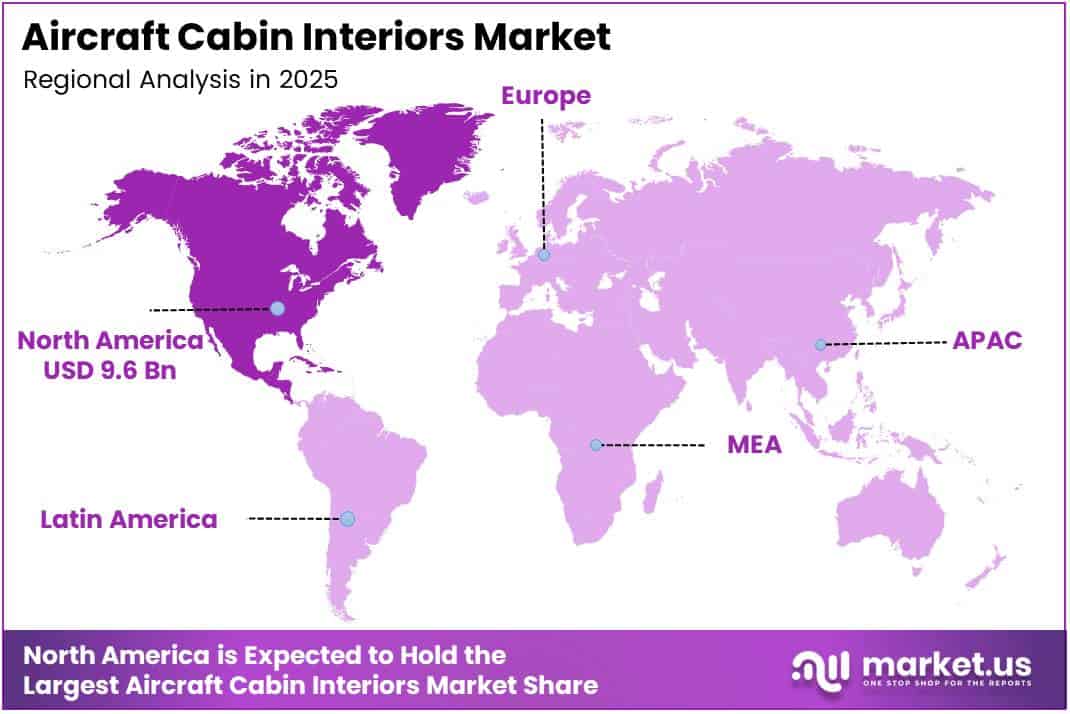

- North America leads regional markets with a 34.90% share, valued at USD 9.6 billion.

Type Analysis

Aircraft Seating dominates with 32.8% due to direct passenger experience and brand visibility.

In 2025, Aircraft Seating held a dominant market position in the By Type segment of the Aircraft Cabin Interiors Market, with a 32.8% share. Seating is the single largest cost item in any cabin interior upgrade, and airlines treat it as the primary differentiator between cabin classes — driving consistent capital allocation toward seat design, weight reduction, and comfort features.

Entertainment and Connectivity differentiates through recurring software and content revenue rather than one-time hardware sales. Airlines increasingly evaluate IFE systems on total lifecycle cost — including connectivity bandwidth, content refresh cycles, and passenger engagement metrics — rather than upfront installation price alone.

Cabin Lighting drives passenger perception of cabin quality at lower cost-per-seat than seating upgrades. LED lighting systems deliver dual returns — reducing electrical load relative to older fluorescent systems while enabling circadian-rhythm programming on long-haul flights that directly addresses passenger fatigue and jet lag.

Galley systems directly determine catering operational efficiency and aircraft weight allocation on every sector. The shift toward electric galley equipment reflects both weight reduction goals and the electrification roadmap that narrow-body platforms are following as next-generation propulsion systems enter service.

Material Analysis

Alloys dominate with 53.7% due to proven structural performance and cost scalability.

In 2025, Alloys held a dominant market position in the By Material segment of the Aircraft Cabin Interiors Market, with a 53.7% share. Aluminum and steel alloys remain the default structural material because their performance characteristics are fully certified across existing aircraft platforms — eliminating the recertification cost and timeline that composite substitutions require.

Aluminum Alloy serves as the backbone of cabin interior structures across both narrow-body and widebody platforms, valued for its high strength-to-weight ratio and machinability. Airlines and OEMs alike default to aluminum alloy specifications because the material’s supply chain depth keeps unit costs stable even at high production volumes.

Steel Alloy carries the highest load-bearing applications within cabin interiors, particularly in seat tracks, attachment fittings, and structural junction points. Despite its weight disadvantage versus aluminum, steel alloy retains structural positions where tensile strength requirements exceed what lighter alternatives can certify.

Composites differentiates through weight reduction performance that alloys cannot match at equivalent structural thickness. As fuel cost pressure and emissions targets intensify, composite adoption in interior panels and seating structures is increasing — but certification timelines and higher unit costs continue to slow the pace of substitution.

Carbon fiber composites deliver the highest stiffness-to-weight ratio available for interior structural applications, making them the preferred material for premium seating shells and structural panels on long-haul platforms. Their adoption is concentrated in widebody interiors where weight savings per kilogram carry the highest fuel cost return.

Glass fiber composites occupy the mid-tier of the composite category — heavier than carbon but significantly cheaper to produce and process. Glass composites dominate interior panel applications where structural loads are moderate and cost per kilogram matters more than ultimate weight performance.

ARAMID (Kevlar) provides impact resistance and ballistic properties that neither carbon nor glass composites replicate, making it the specification choice for floor panels and partition structures where impact and abrasion loads are highest. Its niche but non-substitutable role protects ARAMID suppliers from direct competition on the applications they serve.

Aircraft Analysis

Narrow Body Aircraft dominates with 48.3% due to high fleet volume and short-haul retrofit frequency.

In 2025, Narrow Body Aircraft held a dominant market position in the By Aircraft segment of the Aircraft Cabin Interiors Market, with a 48.3% share. The narrow-body segment’s dominance reflects the global low-cost carrier expansion — airlines that operate high daily cycle counts on single-aisle aircraft refresh interiors more frequently than any other fleet category.

Wide Body Aircraft carries the highest per-aircraft interior investment value, as cabin configurations span multiple classes with premium seating, dedicated crew rest zones, and full IFE infrastructure. A single widebody cabin retrofit programme can generate more revenue per contract than a narrow-body fleet-wide upgrade, concentrating supplier competition at the top end of the market.

Business Jets serve as the highest-margin sub-segment per aircraft, where full cabin customization and bespoke material specifications are standard. Business jet interior suppliers operate in a fundamentally different competitive environment — one where design differentiation and lead time matter more than unit cost — insulating this segment from the commodity pricing pressure that affects commercial aviation interiors.

Regional Transport Aircraft represents the most cost-constrained segment, where interior specifications are driven by weight limits and tight per-seat economics rather than passenger experience ambitions. However, regional aircraft operators face the same cabin wear cycles as mainline carriers, creating steady aftermarket demand for replacement panels, seating components, and lighting systems.

End-Use Analysis

Aftermarket dominates with 67.2% due to active retrofit cycles across aging global fleets.

In 2025, Aftermarket held a dominant market position in the By End-use segment of the Aircraft Cabin Interiors Market, with a 67.2% share. The aftermarket’s structural dominance reflects the ten-to-fifteen-year gap between new aircraft deliveries and the average aircraft retirement age — a window during which airlines actively invest in cabin upgrades to maintain competitive positioning and meet updated regulatory standards.

Original Equipment Manufacturer (OEM) demand tracks directly with new aircraft delivery rates from Airbus and Boeing, making it the more volatile of the two end-use channels. While OEM specifications set the long-term design benchmark for cabin interiors, production rate constraints at both major OEMs have kept OEM revenue growth below aftermarket pace in recent years, reinforcing the aftermarket’s dominant share position.

Key Market Segments

By Material

- Alloys

- Aluminum Alloy

- Steel Alloy

- Others

- Composites

- Carbon

- Glass

- ARAMID (Kevlar)

- Others

- Others

By Type

- Aircraft Seating

- Passenger Seating

- Crew Rest Seating

- Entertainment & Connectivity

- Hardware

- Connectivity

- Content

- Cabin Lighting

- Signage Lights

- Ceiling & Wall Lights

- Floor Path Lighting Strips

- Reading Lights

- Lavatory Lights

- Galley

- Electric

- Non-electric

- Lavatory

- Reusable Liquid Flush

- Vacuum Flush Type

- Windows & Windshields

- Cabin Windows

- Windshields

- Stowage Bins

- Shelf Bins

- Pivot Bins

- Translating Bins

- Interior Panels

- Floor Panels

- Ceiling Panels

- Side Panels

- Cabin Dividers

By Aircraft

- Narrow Body Aircraft

- Wide Body Aircraft

- Business Jets

- Regional Transport Aircraft

By End-use

- Aftermarket

- Original Equipment Manufacturer (OEM)

Drivers

Fleet Retrofit Programmes and Passenger Experience Investment Accelerate Cabin Interior Spending

Airlines worldwide are treating cabin refurbishment as a capital investment rather than a maintenance cost. In October 2025, Air India completed the first phase of its $400 million retrofit programme — installing 3,564 new Economy seats, 648 Premium Economy seats, and 216 Business Class seats across 27 legacy A320neos within twelve months. This execution pace signals that large carriers now commit multi-year capital specifically to interior upgrades.

Passenger experience has become a measurable revenue variable rather than a soft brand consideration. Airlines adding Premium Economy cabins within existing narrowbody configurations report yield improvements that justify retrofit costs within three to five years. This return profile makes cabin investment attractive even under tight capacity constraints, as airlines extract higher per-seat revenue from the same physical aircraft.

According to emeoutlookmag.com, easyJet’s next-generation Mirus Kestrel economy seat is more than 20% lighter than current models — delivering weight savings of up to 500 kg per aircraft and projected annual fuel savings of 12,936 tonnes, reducing CO2 by over 40,513 tonnes. This data demonstrates that seat selection is now a fuel strategy decision, connecting cabin procurement directly to an airline’s operating cost structure and emissions compliance position.

Restraints

High Upgrade Costs and Certification Complexity Slow Cabin Modernization Across Mid-Tier Carriers

Major cabin upgrade programmes require capital commitments that smaller and mid-tier airlines cannot absorb within standard maintenance budgets. A full widebody cabin retrofit — including seats, panels, lighting, and IFE — can run tens of millions of dollars per aircraft, with aircraft out-of-service time adding indirect revenue losses that compound the headline investment figure.

Aviation safety regulations require that every new cabin interior component achieve full certification before installation. Design changes that appear incremental from an engineering standpoint — new seat structures, revised panel materials, updated lighting systems — each trigger independent regulatory review processes that extend project timelines by months and add non-recoverable compliance costs to every cabin programme.

According to simpliflying.com, saving a single kilogram of weight on an A320 operating 2,800 flight hours annually avoids 350 kg of CO2 emissions per passenger per year. This figure illustrates the economic and environmental stakes of cabin material selection — but it also highlights why compliance processes must be rigorous. Each kilogram of weight change alters an aircraft’s certified performance envelope, making regulatory caution structurally embedded in the cabin upgrade process.

Growth Factors

Lightweight Material Innovation and Sustainability Mandates Open New Revenue Streams for Cabin Suppliers

Airline sustainability commitments are converting cabin weight reduction from an engineering preference into a procurement mandate. According to eplaneai.com, American Airlines’ lightweight cabin programme — combining lighter seats, new brake systems, and reduced paint weight — saves 12.4 million gallons of fuel annually and eliminates 117,800 metric tons of CO2. These figures give procurement teams a precise financial and regulatory justification for upgrading cabin specifications ahead of normal refurbishment cycles.

In April 2026, Air India unveiled its first retrofitted Boeing 787-8 Dreamliner — the lead aircraft in a $400 million widebody upgrade covering 26 aircraft — replacing a two-class layout with 20 Business Class suites with sliding doors, 25 Premium Economy seats, and 205 Economy seats. This widebody programme demonstrates that premium cabin densification — adding Business and Premium Economy seats — delivers revenue growth per aircraft that justifies capital-intensive retrofit investments.

The integration of smart cabin technologies — including adaptive lighting, connected IFE platforms, and modular galley systems — is creating a recurring technology refresh cycle that did not exist in traditional cabin interior markets. Airlines that adopt connected cabin architectures create ongoing software and content revenue streams for suppliers, transforming what was a hardware replacement market into a services-augmented revenue model.

Emerging Trends

Touchless Interfaces, Modular Design, and In-Flight Connectivity Redefine the Cabin Experience Roadmap

Passenger touchpoints inside aircraft cabins are shifting toward contactless and hygienic configurations across all cabin classes. Touchless reading lights, gesture-controlled IFE interfaces, and antimicrobial surface materials entered business class specifications first — but airlines are now extending these specifications into economy class on new-build and retrofit programmes, expanding the addressable market for hygiene-focused cabin components.

Modular cabin design is emerging as an operational efficiency tool rather than purely a design trend. Airlines that specify modular seat and partition systems can reconfigure cabin class ratios within a single aircraft type without structural modification — allowing rapid commercial response to demand shifts between economy, premium economy, and business class without triggering full recertification of the aircraft interior.

According to eplaneai.com, ANA replaced metal beverage service carts with lightweight alternatives up to 10 kg lighter each — achieving total weight savings of approximately 580 kg per Boeing 777-300ER aircraft and cutting 5,700 tonnes of fuel use and 11.4 million gallons annually. This outcome illustrates that weight optimization is now extending beyond primary structures and seating into every cabin element — creating a broad addressable market for lightweight component suppliers across the full cabin interior stack.

Regional Analysis

North America Dominates the Aircraft Cabin Interiors Market with a Market Share of 34.90%, Valued at USD 9.6 Billion

North America holds a 34.90% share of the global Aircraft Cabin Interiors Market, valued at USD 9.6 billion. This position reflects the region’s combination of the world’s largest commercial aviation network, mature MRO infrastructure, and a high concentration of aftermarket service operators. US carriers run some of the most active fleet retrofit programmes globally, sustaining consistent domestic demand for cabin interior upgrades.

Europe Aircraft Cabin Interiors Market Trends

Europe supports a dense network of low-cost carriers and legacy airlines operating high-frequency narrow-body routes — a configuration that drives steady aftermarket demand for seating, panels, and lighting upgrades. The region also hosts major Tier 1 interior suppliers and MRO facilities, giving European airlines shorter supply chains and faster cabin turnaround times compared to other regions.

Asia Pacific Aircraft Cabin Interiors Market Trends

Asia Pacific represents the fastest-expanding geography for new aircraft deliveries, with Indian and Southeast Asian carriers adding significant fleet capacity. In November 2024, Singapore Airlines announced a SGD 1.1 billion (~$814 million) investment to upgrade cabin products across 41 Airbus A350-900 aircraft — illustrating the scale of premium cabin investment that Asia Pacific carriers are now committing as long-haul competition intensifies.

Middle East and Africa Aircraft Cabin Interiors Market Trends

Middle East carriers operate some of the world’s largest widebody fleets on ultra-long-haul routes, making them disproportionately large buyers of premium cabin interior systems. Gulf carriers’ consistent investment in Business and First Class product differentiation sustains above-average per-aircraft interior spending, supporting a concentrated but high-value regional market for premium cabin component suppliers.

Latin America Aircraft Cabin Interiors Market Trends

Latin America’s cabin interior market is driven primarily by a growing low-cost carrier segment and the modernization of legacy airline fleets. Budget constraints limit full cabin refurbishment programmes for most operators, but demand for seating replacements, lighting upgrades, and IFE installations on aging narrow-body fleets creates a sustained aftermarket revenue base across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Astronics Corporation builds its competitive position around the intersection of cabin power systems and lighting — two components that are becoming central to the connected cabin architecture that airlines are standardizing across new-build and retrofit programmes. Its focus on power delivery for passenger devices and LED lighting systems places it at a high-value, recurring-upgrade point in the cabin interior stack, where replacement cycles are shortening as digital cabin standards evolve.

Cobham PLC concentrates its cabin interior relevance on in-flight connectivity hardware and antenna systems — a sub-segment where demand is structurally non-discretionary as airlines respond to passenger expectations for broadband access at altitude. Cobham’s positioning in the connectivity infrastructure layer gives it exposure to both new aircraft installations and the active retrofit market, where legacy aircraft require connectivity hardware upgrades to remain commercially competitive.

Collins Aerospace operates as one of the broadest-scope cabin interior suppliers globally, covering seating, lighting, IFE, galley systems, and interior structures. This breadth gives Collins significant leverage in large airline procurement processes, where carriers prefer to consolidate cabin supply relationships. In July 2025, Safran completed the acquisition of Collins Aerospace’s flight control and actuation business for approximately $1.8 billion, signaling active portfolio restructuring among the market’s largest players.

Gogo, Inc. occupies a structurally critical position in the business aviation connectivity segment — a market where bandwidth performance and uptime reliability determine customer retention more directly than price. Gogo’s established install base across business jet fleets creates high switching costs, and its software-defined connectivity platform positions it to capture recurring revenue through service upgrades as satellite bandwidth availability improves over the forecast period.

Key Players

- Astronics Corporation

- Cobham PLC

- Collins Aerospace

- Gogo, Inc.

- Honeywell International Inc.

- Hong Kong Aircraft Engineering Company Limited

- JCB Aero

- Panasonic Corporation

- Thales Group

- The Boeing Company

Recent Developments

- November 2024 — Singapore Airlines announced a SGD 1.1 billion (~$814 million) investment to upgrade cabin products across 41 Airbus A350-900 long-haul and ultra-long-range aircraft, targeting a premium travel experience enhancement across its widebody fleet.

- July 2025 — Safran completed the acquisition of Collins Aerospace’s flight control and actuation business — integrated into 180 aircraft platforms and generating approximately $1.55 billion in revenue in 2024 — for approximately $1.8 billion, expanding Safran’s position in commercial, helicopter, and defense actuation systems.

- September 2025 — Safran announced it was considering the sale of its aircraft interiors assets — including overhead bins, kitchen galleys, and interior fittings — valued at up to $1.76 billion, as part of a strategic refocus toward higher-margin propulsion and flight control systems.

- April 2025 — Insperial announced the acquisition of the MGR Foamtex and Airline Graphics brands at Aircraft Interiors Expo 2025, expanding its interior materials and graphics portfolio to serve a broader range of airline interior programme requirements.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 27.7 Billion |

| Forecast Revenue (2035) | USD 52.0 Billion |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Alloys: Aluminum Alloy, Steel Alloy, Others; Composites: Carbon, Glass, ARAMID/Kevlar, Others; Others), By Type (Aircraft Seating: Passenger Seating, Crew Rest Seating; Entertainment & Connectivity: Hardware, Connectivity, Content; Cabin Lighting; Galley; Lavatory; Windows & Windshields; Stowage Bins; Interior Panels), By Aircraft (Narrow Body, Wide Body, Business Jets, Regional Transport), By End-use (Aftermarket, OEM) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Astronics Corporation, Cobham PLC, Collins Aerospace, Gogo Inc., Honeywell International Inc., Hong Kong Aircraft Engineering Company Limited, JCB Aero, Panasonic Corporation, Thales Group, The Boeing Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |