Quick Navigation

- Report Overview

- Key Takeaways

- By Product Analysis

- By Production Process Analysis

- By Components Analysis

- By Installation Type Analysis

- By Application Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

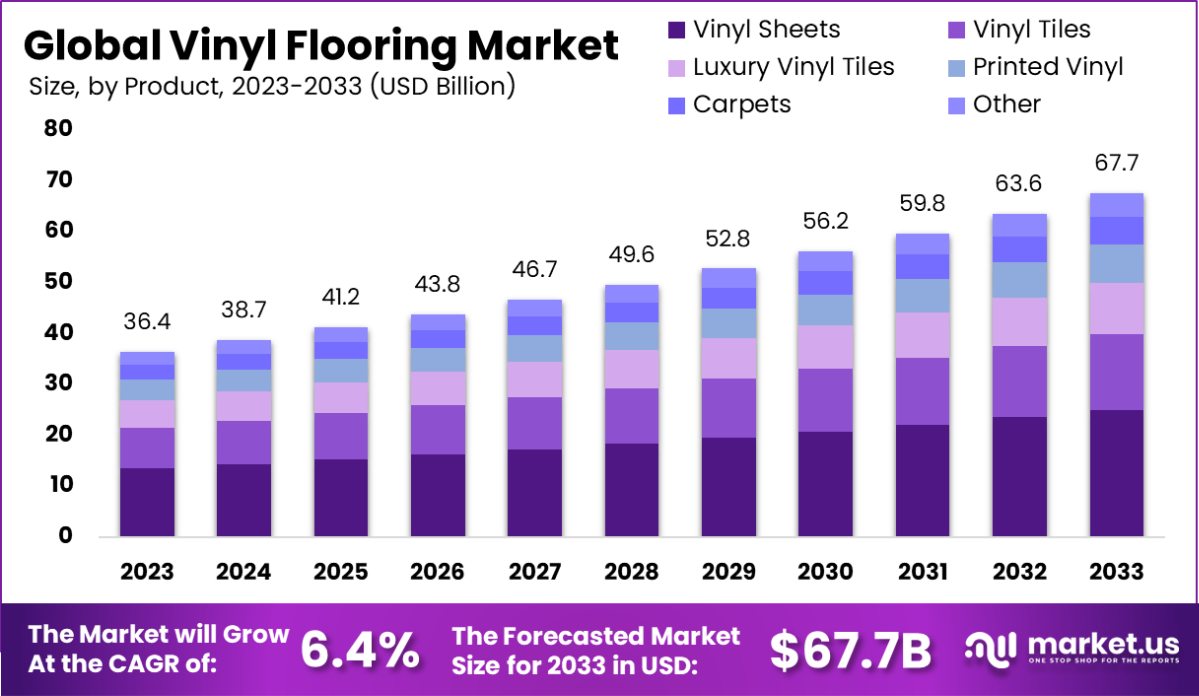

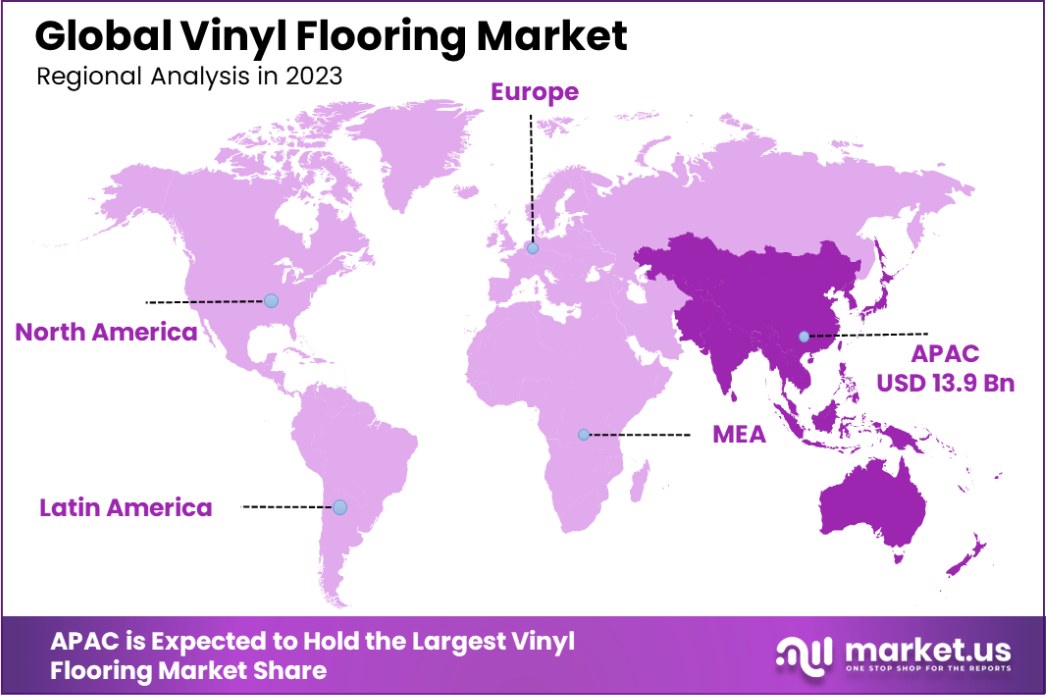

The Global Vinyl Flooring Market is expected to be worth around USD 67.7 Billion by 2033, up from USD 36.4 Billion in 2023, and grow at a CAGR of 6.4% from 2024 to 2033. Asia-Pacific vinyl flooring market 38% share, USD 13.9 billion.

Vinyl flooring is a popular synthetic flooring material made from polyvinyl chloride (PVC) and other compounds. It is known for its durability, versatility, and resistance to water, making it ideal for both residential and commercial spaces. The vinyl flooring market encompasses the global distribution and sale of these materials, driven by trends in home improvement and commercial construction.

The growth of the vinyl flooring market is primarily fueled by the increasing demand for cost-effective, durable, and low-maintenance flooring solutions. The versatility of designs that mimic natural materials like hardwood and stone also broadens its appeal.

The rising trend of home renovations and the expansion of commercial sectors such as healthcare and retail contribute significantly to its demand. Opportunities in the vinyl flooring market are expanding with technological advancements in eco-friendly production processes and the development of phthalate-free vinyl flooring, catering to the growing consumer preference for sustainable building materials.

The vinyl flooring market presents a complex landscape influenced by several factors, including environmental health concerns, safety performance, material composition, and sustainability practices.

Notably, a study referenced by the National Institutes of Health highlighted that 56% of monitored rooms with vinyl or linoleum flooring exhibited significantly higher concentrations of benzyl butyl phthalate (BBzP), measuring at 23.9 ng/m3 compared to 10.6 ng/m3 in rooms with wood flooring or carpet flooring. This data suggests a potential public health concern due to the emission of volatile organic compounds associated with vinyl materials.

However, from a safety perspective, vinyl flooring demonstrates comparable performance to other flooring types. A hospital study cited by Pubmed.ncbi.nlm showed almost identical fall rates between carpet tiles and vinyl flooring, with 19.5 and 19.6 falls per 1000 bed days, respectively.

This indicates that vinyl flooring does not necessarily increase the risk of falls compared to other flooring options, which could maintain its attractiveness in settings where fall risks are a priority, such as in healthcare facilities.

The composition of vinyl flooring products also plays a crucial role in market dynamics. Certain vinyl flooring products contain up to 32% by weight of ortho-phthalates, which are known for their potential health impacts. Conversely, the inclusion of up to 75% pre-and post-consumer recycled materials in these products underscores a move towards greater sustainability within the industry.

Moreover, as per ws680, limestone constitutes 84% of the mass fraction in typical vinyl composition tile, with vinyl resins accounting for 12%, highlighting a significant use of natural resources in production.

This data-driven analysis suggests that while vinyl flooring faces challenges related to health and environmental concerns, its safety record and efforts to incorporate recycled materials may help sustain its market position. The industry must continue to innovate in materials science and recycling practices to address these concerns and enhance its market appeal.

Key Takeaways

- The Global Vinyl Flooring Market is expected to be worth around USD 67.7 Billion by 2033, up from USD 36.4 Billion in 2023, and grow at a CAGR of 6.4% from 2024 to 2033.

- Luxury Vinyl Tiles dominate the Vinyl Flooring Market, holding a 37.5% share by product.

The Printed production process is the most popular, capturing 65.4% of the Vinyl Flooring Market. - Polyvinyl Chloride Resins are essential, comprising 54.5% of components in the Vinyl Flooring Market.

- Glue-Down installation types are preferred by 47.8% of consumers in the Vinyl Flooring Market.

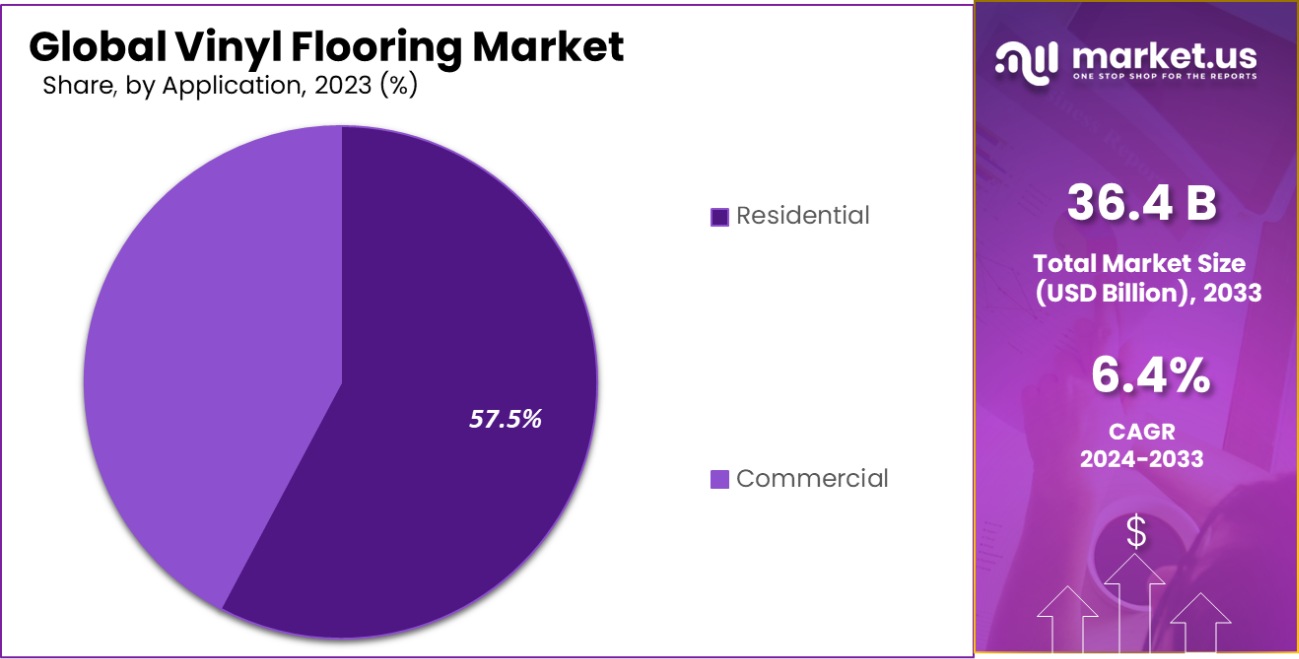

- The Residential application leads, with a significant 57.5% share in the Vinyl Flooring Market.

- The vinyl flooring market in Asia-Pacific is valued at USD 13.9 billion, comprising 38%.

By Product Analysis

The Vinyl Flooring Market sees Luxury Vinyl Tiles dominating, with a substantial 37.5% market share.

In 2023, Luxury Vinyl Tiles held a dominant market position in the By Product segment of the Vinyl Flooring Market, capturing a 37.5% share. This segment outperformed other categories such as Vinyl Sheets, Vinyl Tiles, Printed Vinyl, and Carpets, highlighting its growing popularity and adoption in both residential and commercial settings.

The appeal of Luxury Vinyl Tiles can be attributed to their superior aesthetics, durability, and ease of maintenance, which make them a preferred choice among consumers seeking cost-effective yet stylish flooring solutions.

Vinyl Sheets and Vinyl Tiles also held significant positions, securing market shares of 21% and 19.5%, respectively. These products are valued for their affordability and versatility, offering a range of patterns and designs that cater to varying consumer preferences.

Printed Vinyl, accounting for a 12% market share, continues to attract customers with its customizable options and vibrant designs, suitable for unique and expressive interior decors.

Carpets, although holding a smaller share of 10%, still play a crucial role in the market, favored for their comfort and warmth. The overall distribution of market shares among these product categories indicates a diverse consumer preference landscape, where functionality and aesthetic appeal dictate purchasing decisions.

By Production Process Analysis

Printed production processes are favored significantly, accounting for 65.4% of the Vinyl Flooring Market.

In 2023, Printed held a dominant market position in the “By Production Process” segment of the Vinyl Flooring Market, boasting a 65.4% share. This prominent placement is contrasted with the Inlaid production process, which occupied the remaining market share. The significant preference for Printed vinyl flooring can be attributed to its cost-effectiveness and versatility in design.

Unlike Inlaid vinyl, which embeds color granules into the vinyl sheet for a richer and more durable finish, Printed vinyl flooring allows for a wider range of aesthetic options through digital or print technology, making it more appealing to budget-conscious consumers seeking variety in design.

The extensive adoption of Printed vinyl flooring is also driven by its application across various sectors, including residential, commercial, and industrial markets. It is particularly favored in commercial settings where rapid installation and aesthetic flexibility are highly valued.

The ease of customization and quicker production times of Printed methods align well with the fast-paced development demands of commercial projects. This method’s capability to swiftly adapt to market trends and consumer preferences reinforces its dominant position within the vinyl flooring industry.

By Components Analysis

Polyvinyl Chloride Resins constitute a major component, comprising 54.5% of materials used in the market.

In 2023, Polyvinyl Chloride Resins held a dominant market position in the By Components segment of the Vinyl Flooring Market, commanding a 54.5% share. This was followed by Plasticizers, Trace Stabilizers, and Pigments, which collectively contributed to enhancing the performance and aesthetic appeal of vinyl flooring products.

The robust demand for Polyvinyl Chloride Resins is primarily due to their essential role in providing durability, flexibility, and resistance to environmental factors in vinyl flooring solutions.

Plasticizers, the second most significant component, accounted for a considerable market portion by improving the pliability and workability of vinyl flooring. These additives are vital for tailoring the physical properties of vinyl products to diverse application requirements.

Meanwhile, Trace Stabilizers played a critical role in enhancing the longevity and color stability of the flooring, safeguarding it against degradation from UV light and heat. Lastly, Pigments was instrumental in offering a wide range of aesthetic options, meeting the rising consumer demand for customized and visually appealing flooring solutions.

Together, these components form the backbone of the vinyl flooring industry, driving innovation and meeting evolving consumer preferences for high-performance and aesthetically pleasing flooring options. Their combined functionalities ensure vinyl flooring remains a preferred choice in both residential and commercial sectors.

By Installation Type Analysis

In terms of installation, the Glue-Down method is prevalent, being preferred in 47.8% of cases.

In 2023, Glue-Down held a dominant market position in the “By Installation Type” segment of the Vinyl Flooring Market, with a 47.8% share. This method, known for its strong adhesion and durability, continues to be a preferred choice in commercial settings where heavy foot traffic demands robust flooring solutions. Following Glue-Down, the Floating installation type captured a significant portion of the market, accounting for 34.5%.

Floating vinyl floors are favored for their ease of installation and versatility, making them ideal for residential and light commercial applications. Meanwhile, Loose Lay, an innovative approach known for its simplicity and flexibility, held a 17.7% market share. The Loose Lay method allows for easy repairs and replacements, appealing to those seeking convenient yet reliable flooring options.

This distribution reflects broader trends in consumer preferences and technological advancements in the vinyl flooring industry. The data underscores the importance of installation efficiency and product longevity, driving manufacturers to innovate within these key areas. As the market evolves, these segments are expected to shift, influenced by changing consumer demands and emerging installation technologies.

By Application Analysis

The residential segment prominently utilizes vinyl flooring, representing 57.5% of the market’s applications.

In 2023, Residential held a dominant market position in the “By Application” segment of the Vinyl Flooring Market, with a 57.5% share. This segment outperformed Commercial, which accounted for the remaining 42.5%.

The Residential sector’s strong performance can be attributed to the growing demand for durable and cost-effective flooring solutions in private homes. As homeowners increasingly seek materials that offer both aesthetic appeal and longevity, vinyl flooring has become a popular choice due to its resistance to wear and ease of maintenance.

On the other hand, the Commercial sector also showed significant usage of vinyl flooring, driven by its application in various industries including healthcare, retail, and education. The versatility and robustness of vinyl flooring make it suitable for high-traffic areas commonly found in commercial settings.

Moreover, advancements in vinyl flooring technologies, such as the development of luxury vinyl tiles (LVT) that offer enhanced design capabilities, have made it an attractive option for commercial interiors.

Overall, the Vinyl Flooring Market continues to expand, with both Residential and Commercial segments benefiting from technological innovations and shifting consumer preferences towards more sustainable and stylish flooring solutions.

Key Market Segments

By Product

- Vinyl Sheets

- Vinyl Tiles

- Luxury Vinyl Tiles

- Printed Vinyl

- Carpets

- Other

By Production Process

- Inlaid

- Printed

By Components

- Polyvinyl Chloride Resins

- Plasticizers

- Trace Stabilizers Pigments

- Others

By Installation Type

- Glue-Down

- Floating

- Loose Lay

By Application

- Residential

- Commercial

Driving Factors

Increasing Demand for Durable and Low-Maintenance Flooring

The vinyl flooring market is growing primarily due to the increasing consumer demand for durable and easy-to-maintain flooring solutions. Vinyl flooring offers superior resistance to scratches, stains, and moisture compared to traditional materials like hardwood and tile.

This makes it an ideal choice for high-traffic areas in both residential and commercial settings. The material’s versatility in design and color also caters to a wide range of aesthetic preferences, further boosting its popularity among homeowners and businesses seeking practical yet stylish flooring options.

Rise of Eco-Friendly and Sustainable Building Materials

In recent years, there has been a significant shift towards sustainable and eco-friendly building practices, which has directly influenced the vinyl flooring market. Manufacturers are increasingly focusing on producing low-VOC (volatile organic compounds) and recyclable vinyl products to meet stringent environmental regulations and cater to the green building trend.

This evolution in product offerings is not only attracting environmentally conscious consumers but also aligning with global sustainability goals, thereby positioning vinyl flooring as a forward-thinking choice in the construction and renovation industries.

Technological Advancements in Flooring Production Techniques

Technological advancements in production processes have transformed the vinyl flooring market by enhancing the quality and efficiency of the final product. Modern techniques allow for more detailed and authentic textures, mimicking materials like wood and stone with remarkable accuracy.

These innovations extend the life span and improve the visual appeal of vinyl flooring, making it a competitive alternative to more expensive materials. Additionally, the integration of digital printing and 3D imaging has enabled customized flooring solutions, appealing to a broader consumer base and opening up new market opportunities.

Restraining Factors

High Installation and Maintenance Costs Deter Potential Buyers

Vinyl flooring, while durable and versatile, comes with significant upfront installation costs, especially for higher-quality or luxury vinyl tiles. These costs can be a deterrent for homeowners and businesses operating on tighter budgets.

Additionally, despite its reputation for durability, vinyl flooring requires regular maintenance to prevent scratches and dents. This need for upkeep, coupled with the initial investment, can make vinyl less appealing compared to more low-maintenance flooring options like laminate or ceramic tiles, which offer similar aesthetic benefits without the high ongoing care.

Environmental Concerns Limit Market Acceptance

The production of vinyl flooring often involves the use of PVC (polyvinyl chloride), which releases harmful chemicals during manufacturing and disposal. These environmental and health concerns are becoming more significant for consumers and businesses aiming for sustainability.

As the market grows more environmentally conscious, the demand for eco-friendly materials increases, putting vinyl at a disadvantage. This shift is prompting manufacturers to explore and invest in alternative materials that are less harmful, thereby impacting the traditional vinyl flooring market’s growth.

Competition from Substitute Products Restrains Growth

Vinyl flooring faces stiff competition from a variety of other flooring materials, such as hardwood, ceramic, and stone, which offer both aesthetic and functional benefits. These alternatives are often perceived as more natural and sustainable, which appeals to a segment of the market that values environmental impact and long-term durability.

Additionally, innovations in other flooring types, like improved water resistance in laminate flooring, challenge vinyl’s unique selling points. This competitive pressure forces vinyl manufacturers to continually innovate, sometimes at increased costs, limiting their market share growth.

Growth Opportunity

Expansion into Emerging Markets for Increased Reach

Vinyl flooring manufacturers have significant growth opportunities in emerging markets where urbanization and construction are on the rise. As countries like India, Brazil, and China continue to develop economically, the demand for affordable, durable, and easy-to-install flooring options such as vinyl increases.

Companies can capitalize on this trend by establishing local production facilities or partnerships to reduce shipping costs and tariffs, tailor designs to local tastes, and navigate regulatory environments more effectively.

Eco-Friendly Products to Meet Consumer Sustainability Demands

As environmental awareness increases, consumers are more inclined to choose sustainable building materials, presenting a ripe opportunity for innovation in the vinyl flooring market. Manufacturers can explore the development of eco-friendly vinyl products that utilize recycled materials, reduce VOC emissions, and offer end-of-life recyclability.

Marketing these green alternatives not only meets consumer demand but also helps companies stand out in a competitive market, potentially attracting a new segment of environmentally conscious buyers.

Technological Advancements in Product and Installation Techniques

Investing in technology that enhances the aesthetic appeal and functionality of vinyl flooring could significantly boost market share. This includes innovations like 3D printing technologies for intricate patterns, improved wear layers for enhanced durability, and easier click-lock installation systems that appeal to the DIY market.

These advancements could transform consumer perceptions of vinyl flooring from a budget-friendly option to a desirable, cutting-edge choice for modern interiors.

Latest Trends

Rapid Adoption of Eco-Friendly Vinyl Flooring Solutions

The vinyl flooring market is witnessing a significant shift towards sustainable and eco-friendly products. Consumers are increasingly aware of environmental impacts and are opting for flooring options that are both durable and made from recycled materials.

Manufacturers are responding by offering vinyl flooring that meets stringent environmental standards, utilizing phthalate-free plasticizers and recycled content. This trend not only caters to environmentally conscious buyers but also aligns with global sustainability regulations, enhancing the market’s growth prospects.

Growing Popularity of Luxury Vinyl Tiles (LVT) in Residential Spaces

Luxury Vinyl Tiles (LVT) are gaining traction, especially in residential areas, due to their aesthetic appeal and practical benefits. LVT offers the appearance of natural materials like wood and stone at a lower cost and with easier maintenance.

Its water-resistant properties and durability make it ideal for kitchens, bathrooms, and high-traffic living areas. The versatility in designs and textures, coupled with technological advancements in embossing techniques, is making LVT a preferred choice among homeowners seeking both style and functionality.

Technological Advancements in Vinyl Flooring Production

Technological advancements are revolutionizing the vinyl flooring industry. Modern manufacturing techniques have enabled the production of vinyl floors that are remarkably resilient and offer extended lifespans. These technologies include improved digital graphic layers that enhance the aesthetic realism of vinyl products and innovations in wear layers that increase scratch and stain resistance.

Additionally, advancements in installation techniques, such as click-lock systems, are simplifying the installation process, reducing costs, and making it feasible for DIY projects, further boosting the market’s growth.

Regional Analysis

The Asia-Pacific vinyl flooring market holds a 38% share, valued at USD 13.9 billion.

The global vinyl flooring market showcases distinct characteristics across different regions, reflecting varying consumer preferences, economic dynamics, and construction activities.

In North America, the market is driven by robust investments in residential and commercial construction sectors, with a significant uptrend in renovation and retrofitting activities across the United States and Canada.

Europe, while mature, exhibits steady demand due to the high emphasis on sustainable and low-maintenance building materials, particularly in Germany, France, and the UK.

Asia-Pacific stands out as the dominant region, holding approximately 38% of the market share and generating revenues close to USD 13.9 billion. This prominence is fueled by rapid urbanization, industrialization, and the expansion of residential sectors in China, India, and Southeast Asia. Manufacturers are capitalizing on the rising demand for cost-effective, durable, and aesthetically pleasing flooring options.

The Middle East & Africa region, though smaller in scale, is experiencing growth driven by the increasing number of infrastructure projects and economic diversification efforts, particularly in the Gulf Cooperation Council (GCC) countries. Latin America, on the other hand, shows potential for growth with improving economic conditions and increasing consumer spending on home decor.

These regional dynamics highlight the varied growth trajectories within the global vinyl flooring market, with Asia-Pacific not only leading in terms of percentage but also in revenue generation, setting the pace for market trends and consumer preferences globally.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global vinyl flooring market of 2023, key companies have exhibited strategic behaviors and market positioning that underline the industry’s growth and evolution. Companies like Armstrong Flooring, Inc., Mannington Mills, Inc., and Mohawk Industries, Inc. are longstanding players with a robust presence in North America, showcasing a strong focus on sustainability and technological innovation in flooring solutions.

European manufacturers such as Forbo Flooring Systems, Tarkett S.A., and Gerflor are leveraging their expertise in design and eco-friendly materials, pushing the boundaries of vinyl flooring’s aesthetic and functional appeal. These companies have been pivotal in advancing low-VOC (Volatile Organic Compounds) emitting products that meet stringent environmental regulations prevalent in European markets.

Asian firms such as LG Hausys and Beaulieu International Group are capitalizing on the rising demand in the Asia-Pacific region, driven by rapid urbanization and increased construction activities. Their strategic advantage lies in scalable operations and advanced R&D capabilities, which allow for competitive pricing and innovation in durable and decorative vinyl flooring options.

Interface, Inc., and Shaw Industries Group, Inc., have particularly emphasized their commitment to circular economy principles, making significant strides in recycling and reusing materials. This approach not only appeals to environmentally conscious consumers but also aligns with global regulatory trends favoring sustainable building materials.

The smaller players like Fatra A.S. and Polyflor Ltd. focus on niche markets, offering specialized products that cater to specific needs such as slip resistance and acoustic properties, thus maintaining a competitive edge in a crowded marketplace.

Overall, the vinyl flooring market in 2023 is characterized by intense competition and innovation, with key players focusing on sustainability, technological advancements, and expanding their geographical footprint to harness growth opportunities in emerging markets.

Top Key Players in the Market

- Armstrong Flooring, Inc.

- Beaulieu International Group

- Fatra A.S.

- Forbo Flooring Systems

- Gerflor

- Interface, Inc.

- LG Hausys

- Mannington Mills, Inc.

- Mohawk Industries, Inc.

- Polyflor Ltd.

- Shaw Industries Group, Inc.

- Tarkett S.A.

Recent Developments

- In 2023, Armstrong Flooring expanded its product range with enhanced designs and sustainable materials. Recent developments include launching eco-friendly vinyl flooring and upgrading manufacturing processes to reduce environmental impact, aligning with the rising consumer demand for sustainable products.

- In 2023, Beaulieu International Group enhanced its vinyl flooring portfolio with innovative designs and sustainable solutions. Recent developments include investing in new manufacturing technologies, expanding globally, and launching eco-friendly flooring options to meet the growing demand for sustainability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 36.4 Billion |

| Forecast Revenue (2033) | USD 67.7 Billion |

| CAGR (2024-2033) | 6.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Vinyl Sheets, Vinyl Tiles, Luxury Vinyl Tiles, Printed Vinyl, Carpets, Other), By Production Process (Inlaid, Printed), By Components (Polyvinyl Chloride Resins, Plasticizers, Trace Stabilizers Pigments, Others), By Installation Type (Glue-Down, Floating, Loose Lay), By Application (Residential, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Armstrong Flooring, Inc., Beaulieu International Group, Fatra A.S., Forbo Flooring Systems, Gerflor, Interface, Inc., LG Hausys, Mannington Mills, Inc., Mohawk Industries, Inc., Polyflor Ltd., Shaw Industries Group, Inc. , Tarkett S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |