Quick Navigation

Report Overview

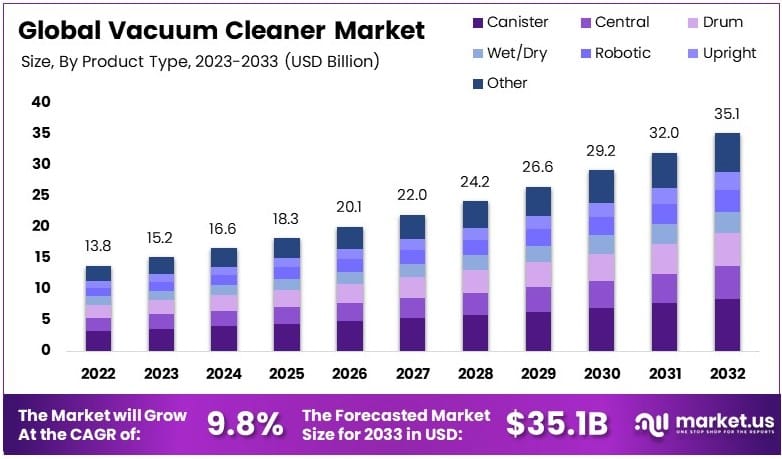

The Global Vacuum Cleaner Market size is expected to be worth around USD 35.1 Billion by 2033, from USD 13.8 Billion in 2023, growing at a CAGR of 9.8% during the forecast period from 2024 to 2033.

A vacuum cleaner is a household or industrial device designed to remove dust, dirt, and debris from surfaces. It operates using suction and often includes various attachments for specific cleaning tasks. Vacuum cleaners are widely used for maintaining cleanliness in homes, offices, and commercial spaces.

The vacuum cleaner market involves the production, distribution, and sale of vacuum cleaning devices. It includes various models, such as upright, canister, and robotic vacuums, catering to different user needs. This market serves households, businesses, and institutions focused on efficient and effective cleaning solutions.

The vacuum cleaner market remains robust, supported by high household penetration rates and steady commercial demand. According to the Vacuum Cleaner Manufacturers Association, 98% of American households own a vacuum cleaner, underlining strong market saturation domestically.

Commercial use is also substantial, as vacuum cleaners serve as essential tools in the commercial cleaning industry, which employs over 2 million workers across offices, hotels, and industrial facilities. This widespread adoption highlights the product’s critical role in both residential and commercial spaces, where efficient cleaning solutions are a priority.

The vacuum cleaner industry benefits from consistent demand driven by both household and commercial sectors. Growth opportunities are tied to technological advancements, particularly in smart, automated and robotic vacuum cleaners that cater to convenience-oriented consumers.

Market saturation is high in developed regions, including North America and Europe, where ownership rates are near maximum levels. However, emerging markets present new growth opportunities as urbanization and rising disposable incomes increase demand. Market competitiveness is notable, with global brands and regional players competing on price, technology, and features.

Import-export trends are significant within this industry. According to the OEC, China led global exports of vacuum cleaners with a total export value of $11.6 billion in 2022. The United States, as a major importer, recorded imports totaling $6.26 billion in the same year, reflecting strong demand and a reliance on foreign manufacturers for supply.

Government regulations around energy efficiency and sustainable materials are expected to shape the future of the market, prompting manufacturers to invest in eco-friendly technologies and meet evolving consumer and regulatory expectations.

Key Takeaways

- The Vacuum Cleaner Market was valued at USD 13.8 Billion in 2023 and is expected to reach USD 35.1 Billion by 2033, with a CAGR of 9.8%.

- In 2023, Canister type dominates the product segment with 24%, attributed to its versatility in cleaning.

- In 2023, Online leads the distribution channel with 58%, aligning with consumer preference for e-commerce platforms.

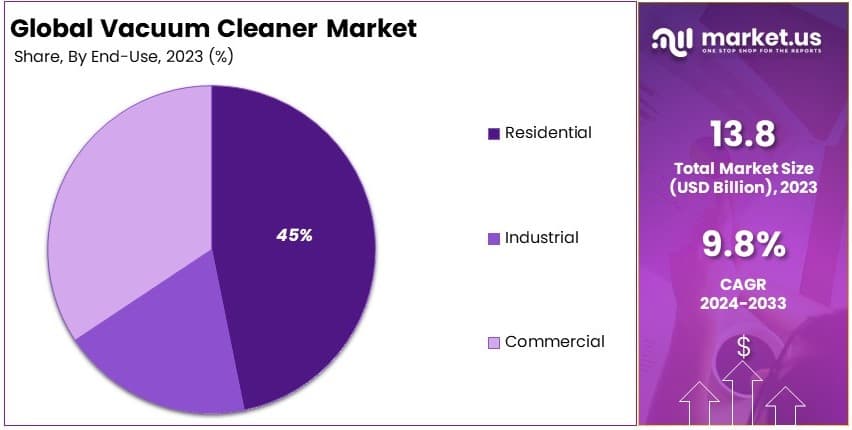

- In 2023, Residential use holds the end-user segment with 45%, reflecting household reliance on vacuum cleaners.

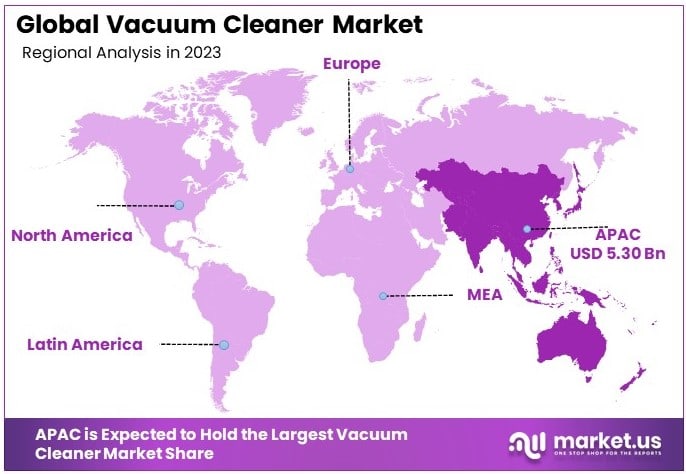

- In 2023, the Asia Pacific region dominates with 38.4% of the market, driven by rising urbanization and disposable incomes.

Product Type Analysis

Canister vacuums dominate with 24% due to their versatility and ease of use.

The Vacuum Cleaner Market, segmented by product type, includes Canister, Central, Drum, Wet/Dry, Robotic, Upright, and Other vacuum cleaners. Canister vacuums hold the largest market share at 24%. Their dominance is attributed to their flexibility and efficiency in cleaning a variety of surfaces.

Canister vacuums are particularly favored in residential settings for their powerful suction and maneuverability, which make them ideal for cleaning hard-to-reach areas and delicate surfaces without causing damage.

Canister vacuums typically come with a range of attachments that cater to different cleaning needs, enhancing their versatility. Additionally, their design, which separates the motor and the vacuum bag from the vacuum head, allows for a lighter handle, reducing fatigue during cleaning tasks.

Other segments like Upright and Robotic vacuums also play significant roles in the market. Upright vacuums are preferred for their ease of storage and effective cleaning of large carpeted areas, making them popular in markets like the United States.

Robotic vacuums, on the other hand, offer convenience and autonomous operation, appealing to tech-savvy consumers and those with busy lifestyles. Their increasing popularity is bolstered by advancements in technology such as smart home integration and improved cleaning efficiency. Wet/Dry vacuums are valued for their ability to handle liquid spills and dry dirt, making them essential in both residential and commercial settings.

Distribution Channel Analysis

Online sales dominate with 58% due to convenience and the availability of a wide range of products.

The Vacuum Cleaner Market segmented by distribution channel includes Online and Offline channels. Online sales lead the market with a 58% share, driven by the convenience and wide selection that online shopping offers. Consumers appreciate the ability to compare prices, read reviews, and check the broad array of features from the comfort of their homes, which has significantly influenced the growth of online sales.

The online platform also offers opportunities for manufacturers to reach a broader audience, including international markets, without the need for physical retail infrastructure. This accessibility has been crucial in expanding the customer base for vacuum cleaners and introducing innovative products quickly to the market.

Despite the dominance of online sales, offline channels remain relevant, especially in regions where consumers prefer in-person shopping experiences to assess the product firsthand.

Retail stores, including specialty appliance stores, department stores and big box retailers, play a critical role in the distribution of vacuum cleaners. These stores provide immediate product availability and in-person customer service, which are important factors for many consumers, particularly those purchasing higher-end models.

End-Use Analysis

Residential use dominates with 45% due to the high demand for home cleaning solutions.

The Vacuum Cleaner Market segmented by end-use includes Industrial, Residential, and Commercial sectors. The Residential sector is the dominant segment, accounting for 45% of the market.

This predominance is largely due to the increasing demand for efficient, easy-to-use home cleaning solutions. The growth in residential usage is driven by rising global living standards and the growing awareness of the health benefits of maintaining a clean home environment.

Within the residential sector, there is a significant demand for products that offer convenience and innovation, such as robotic and cordless vacuums. These products appeal to busy households where ease of use and time-saving are highly valued.

The Commercial sector, including hospitals, retail stores, and hospitality, also relies heavily on vacuum cleaners to maintain public spaces and meet hygiene standards, especially in high-traffic environments. Industrial vacuum cleaners are essential in sectors like manufacturing and construction, where heavy-duty cleaning capability is required.

These sectors demand vacuum cleaners that are durable and can handle large volumes of waste, often under harsh conditions. The Food & Beverages and Pharmaceuticals sectors emphasize hygiene and contamination prevention, making vacuum cleaners integral to their operations.

Key Market Segments

By Product Type

- Canister

- Central

- Drum

- Wet/Dry

- Robotic

- Upright

- Other

By Distribution Channel

- Online

- Offline

By End-Use

- Industrial

- Manufacturing

- Food & Beverages

- Pharmaceuticals

- Construction

- Others

- Residential

- Commercial

- Hospitals

- Retail Stores

- Hospitality

- Shopping Malls

- Others

Drivers

Rising Demand for Smart Home Appliances Drives Market Growth

The increasing demand for smart home appliances contributes significantly to the Vacuum Cleaner Market. Consumers are seeking more automated and connected cleaning robots and solutions, making smart vacuum cleaners highly popular.

Additionally, a heightened focus on hygiene and cleanliness, especially after global health events, boosts vacuum cleaner sales. Households now prioritize efficient cleaning tools that ensure a hygienic environment, further driving market growth.

Growing urbanization leads to smaller living spaces, making compact and efficient vacuum cleaners essential. This shift supports the demand for easy-to-store, space-saving vacuum cleaner models in urban households.

Technological advancements enhance vacuum cleaner features, making them more user-friendly and effective. Innovations like smart sensors, voice commands, and automated scheduling have made vacuum cleaners more appealing to a wider audience.

Restraints

High Cost of Advanced Models Restraints Market Growth

The high cost of advanced vacuum cleaner models limits their adoption among cost-sensitive consumers. Premium models often feature smart technologies and additional functionalities, making them expensive.

Limited awareness in rural areas also restrains market growth. Consumers in these regions may lack information about modern vacuum cleaners, impacting sales in these markets.

High maintenance and repair costs add to the overall expenses, making vacuum cleaners less attractive for budget-conscious buyers. Regular servicing or part replacements can increase operational costs, affecting purchasing decisions.

Limited battery life of cordless models is another restraint. While convenient, frequent recharging requirements reduce the overall efficiency and user satisfaction of cordless vacuum cleaners, limiting their wider adoption.

Opportunity

Expansion in Emerging Markets Provides Opportunities

Emerging markets present substantial growth opportunities for the Vacuum Cleaner Market. Rapid urbanization in regions like Asia-Pacific and Latin America boosts demand for cleaning solutions, increasing sales.

Development of eco-friendly vacuum cleaners caters to the rising consumer preference for sustainable products. Green technologies and energy-efficient designs enhance market appeal and align with global sustainability trends.

Integration with IoT and AI technologies creates growth avenues. Smart vacuum cleaners that connect with home automation systems offer convenience, making them attractive to tech-savvy consumers.

Increased demand for robotic vacuum cleaners further fuels growth. These models provide automated cleaning solutions, reducing manual labor and attracting busy households, leading to higher adoption rates globally.

Challenges

Intense Market Competition Challenges Market Growth

Intense competition is a significant challenge in the Vacuum Cleaner Market. Numerous brands compete for market share, leading to aggressive pricing strategies that affect profit margins.

Frequent technological changes also pose challenges. Manufacturers must continuously innovate to keep up with new features, which can be costly and time-consuming.

Economic fluctuations in key markets impact consumer spending on non-essential products like vacuum cleaners. During economic downturns, households may delay purchases, affecting overall sales.

Supply chain disruptions can limit the availability of vacuum cleaner components, delaying production and deliveries. These disruptions can result from global events or logistical challenges, impacting market stability.

Growth Factors

Government Support for Smart Cities Is Growth Factors

Government support for smart city projects drives demand for smart appliances, including vacuum cleaners. Initiatives aimed at creating tech-enabled urban infrastructure enhance market prospects.

Increasing household disposable income supports growth. Higher income levels enable more consumers to invest in advanced cleaning solutions, boosting vacuum cleaner sales.

Innovations in battery and suction technology contribute to market expansion. Improved battery life and stronger suction make vacuum cleaners more efficient, leading to increased consumer satisfaction.

Expanding e-commerce distribution channels also supports growth. Online platforms provide easy access to a variety of vacuum cleaner models, making it easier for consumers to compare and purchase, driving overall market growth.

Emerging Trends

Adoption of Robotic Vacuum Cleaners Is Latest Trending Factor

Robotic vacuum cleaners have become a major trend in the market. Their convenience and ability to operate autonomously make them highly desirable in modern households.

The growing preference for cordless models is another trend. Consumers appreciate the mobility and flexibility of cordless vacuum cleaners, making them a popular choice.

Use of HEPA filters is on the rise, as they improve air quality by capturing fine particles. This feature is particularly appealing to consumers with allergies or respiratory issues.

Increased demand for wet-dry vacuum cleaners is also noticeable. These versatile models offer both dry and wet cleaning, making them suitable for various cleaning tasks in homes and offices.

Regional Analysis

Asia Pacific Dominates with 38.4% Market Share

Asia Pacific (APAC) leads the Vacuum Cleaner Market with a 38.4% share, amounting to USD 5.30 billion. The region’s dominance is driven by rapid urbanization, increased household income, and rising awareness of hygiene. Demand is particularly strong in countries like China, India, and Japan, where cleaning automation is gaining popularity.

Market performance in APAC benefits from cost-effective production, a strong distribution network, and growing adoption of smart appliances. Additionally, government initiatives promoting urban infrastructure and modern living further enhance market demand for vacuum cleaners. The rise of e-commerce has also expanded product availability across the region.

Asia Pacific’s influence in the vacuum cleaner market is expected to grow. Ongoing technological advancements and rising consumer preference for automated cleaning solutions will strengthen the region’s position in the global market.

Regional Mentions:

- North America: North America maintains a strong market presence, driven by high demand for advanced vacuum technologies, including robotic models. High disposable income supports consumer spending on premium cleaning appliances.

- Europe: Europe’s market benefits from strict regulations on indoor air quality and a strong emphasis on sustainable living. Demand for eco-friendly and energy-efficient vacuum cleaners drives market growth.

- Middle East & Africa: The region experiences growth due to increasing urbanization and improving living standards. The adoption of vacuum cleaners is rising in residential and commercial sectors, supporting steady market expansion.

- Latin America: Latin America shows growth potential, driven by rising awareness of home hygiene and expanding retail channels. The region’s growing middle class supports increased spending on modern cleaning solutions.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The vacuum cleaner market is competitive, driven by innovation and evolving consumer preferences. The top four companies in this sector are Alfred Karcher SE & Co., Dyson Ltd., Emerson Electric Co., and iRobot Corporation. They maintain strong positions due to their innovative products, global presence, and focus on consumer needs.

Dyson Ltd. is a leader in innovation, offering powerful and energy-efficient vacuum cleaners. Its focus on cordless technology and advanced filtration systems supports its dominance in the premium segment.

Emerson Electric Co. provides a wide range of vacuum cleaners, emphasizing performance and durability. It caters to both residential and commercial sectors, expanding its market reach.

iRobot Corporation stands out with robotic vacuum cleaners. Its focus on AI-driven cleaning solutions positions it as a leader in the smart home segment, appealing to tech-savvy consumers.

These key players drive growth through continuous innovation, strategic partnerships, and expanding product lines, making them leaders in the vacuum cleaner market.

Top Key Players in the Market

- Alfred Karcher SE & Co.

- Dyson Ltd.

- Emerson Electric Co.

- Haier Group Corp

- iRobot Corporation

- Neato Robotics, Inc.

- Nilfisk Group

- Panasonic Holdings Corporation

- Snow Joe LLC

- Panasonic Corporation

- Koninklijke Philips N.V.

- LG Electronics

- Samsung Electronics Co., Ltd.

- Other key Players

Recent Developments

- Dyson: In April 2024, Dyson launched the 360 Vis Nav robot vacuum, featuring double the suction power of comparable models and an extending side duct for thorough edge-to-edge cleaning. The device, controllable via the MyDyson app, includes a wide brush bar designed to capture hair and dirt across different surfaces.

- Dyson Financial Performance: In 2022, Dyson reported a revenue increase to £6.5 billion from £6.0 billion in 2021, despite global challenges like chip shortages and supply chain issues. The company credited this growth to continuous investment in R&D, focusing on innovative products such as advanced vacuum cleaners and air purifiers.

- Shark Navigator Deluxe: In November 2024, the Shark Navigator Deluxe Upright Vacuum Cleaner was recognized by PEOPLE magazine as a top-performing model. Praised for powerful suction, quiet operation, and ease of use on both hard floors and carpets, it gained popularity among consumers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 13.8 Billion |

| Forecast Revenue (2033) | USD 35.1 Billion |

| CAGR (2024-2033) | 9.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Canister, Central, Drum, Wet and Dry, Robotic, Upright, Other), By Distribution Channel (Online, Offline), By End-Use (Industrial: Manufacturing, Food and Beverages, Pharmaceuticals, Construction, Others; Residential; Commercial: Hospitals, Retail Stores, Hospitality, Shopping Malls, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alfred Karcher SE & Co., Dyson Ltd., Emerson Electric Co., Haier Group Corp, iRobot Corporation, Neato Robotics, Inc., Nilfisk Group, Panasonic Holdings Corporation, Snow Joe LLC, Panasonic Corporation, Koninklijke Philips N.V., LG Electronics, Samsung Electronics Co., Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |