Quick Navigation

Report Overview

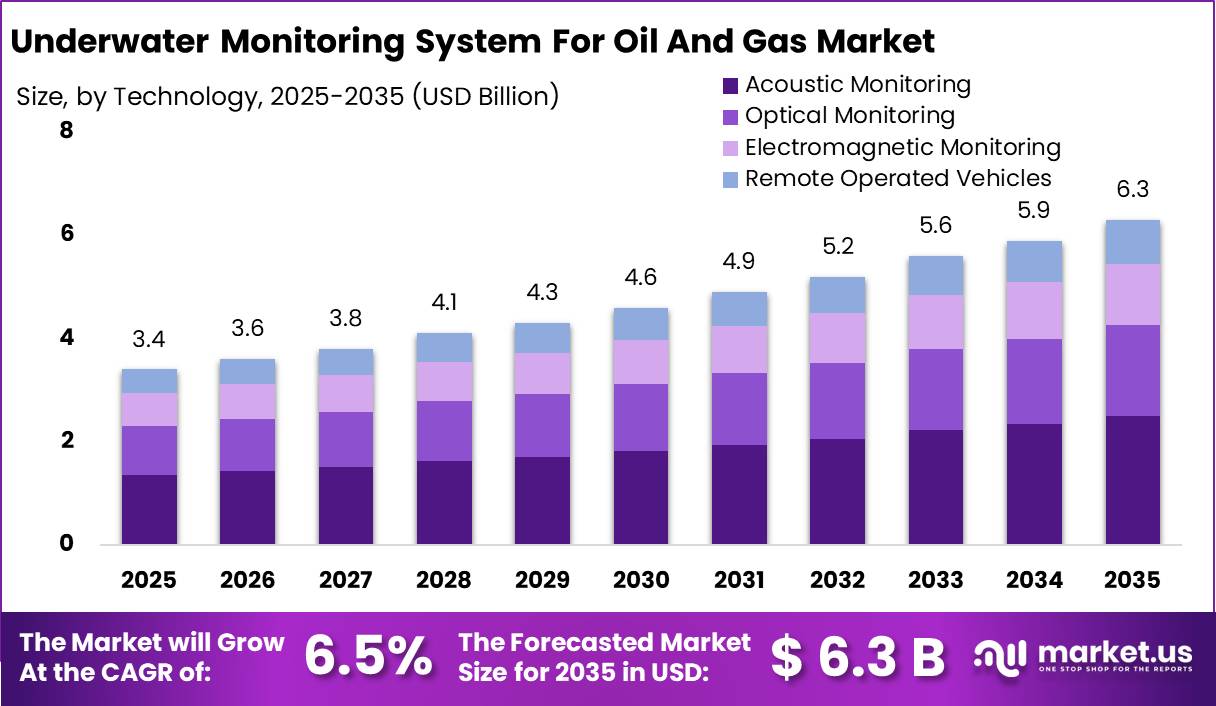

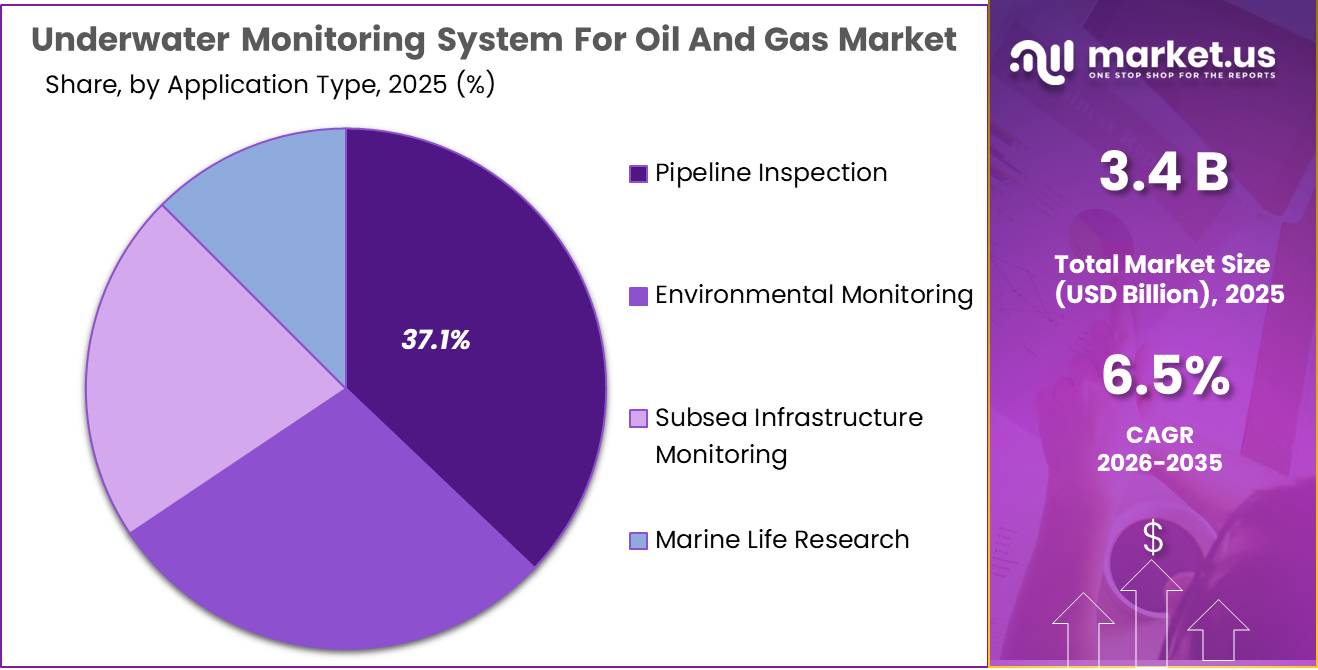

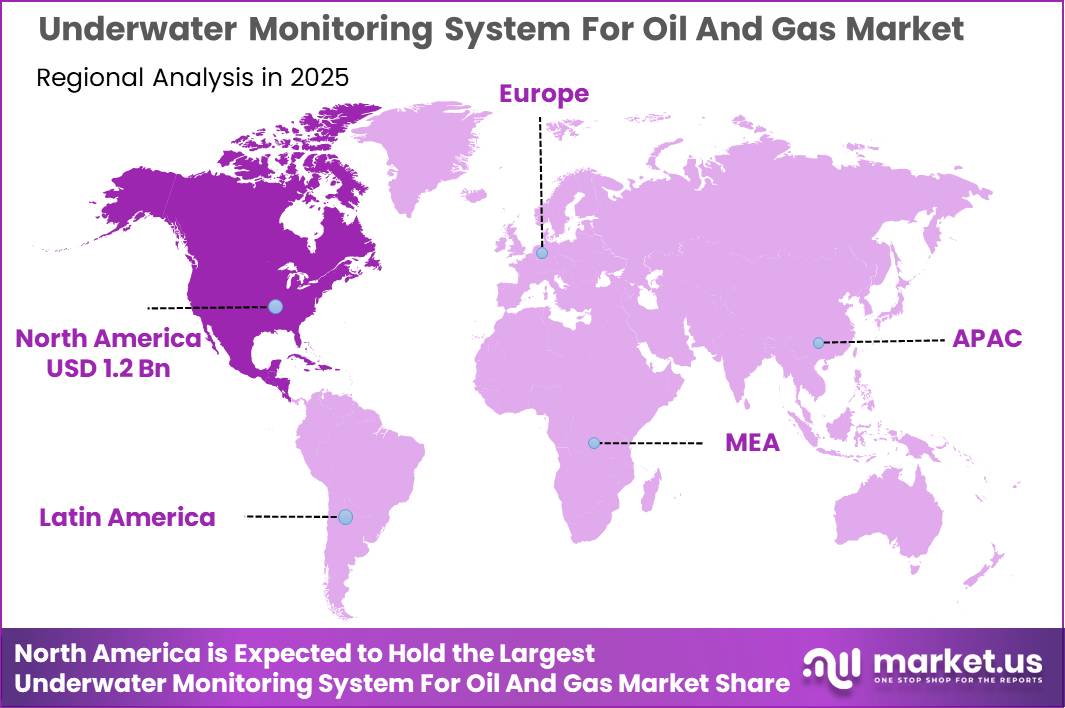

The Global Underwater Monitoring System For Oil And Gas Market size is expected to be worth around USD 6.3 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 6.5% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 36.2% share, holding USD 1.2 Billion revenue.

The underwater monitoring system for oil and gas industry is becoming a strategic subsea integrity, safety and emissions-control segment, supporting pipelines, risers, wellheads, manifolds and deepwater production assets through sensors, acoustic systems, ROV/AUV inspection, fiber-optic monitoring and digital analytics. Its relevance is rising as offshore operations remain material: the U.S. Federal Offshore Gulf of America supplied about 15% of U.S. crude oil and 2% of U.S. dry natural gas in 2022, with platforms operating in waters up to 6,000 feet and some beyond 10,000 feet.

- Demand is supported by offshore output scale: the U.S. EIA forecast Federal Offshore Gulf crude production at 1.80 million b/d in 2025 and 1.81 million b/d in 2026, with the region contributing about 13% of U.S. crude output.

Key Takeaways

- Underwater Monitoring System For Oil And Gas Market size is expected to be worth around USD 6.3 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 6.5%.

- Sensors held a dominant market position, capturing more than a 42.7% share in the Underwater Monitoring System for Oil and Gas market.

- Acoustic Monitoring held a dominant market position, capturing more than a 39.6% share in the Underwater Monitoring System for Oil and Gas market.

- Pipeline Inspection held a dominant market position, capturing more than a 37.1% share.

- North America emerged as the leading regional market in the Underwater Monitoring System for Oil and Gas industry, holding a dominant 36.2% market share and reaching a value of USD 1.2 Billion.

The industrial scenario is supported by new offshore activity. EIA reported that new Gulf fields are expected to add 85,000 barrels/day of crude oil in 2025 and 308,000 barrels/day in 2026, while associated gas additions are expected at 0.09 Bcf/day in 2025 and 0.27 Bcf/day in 2026. This creates direct demand for subsea sensors, AUV/ROV inspection tools, pipeline tracking, and continuous monitoring networks.

EIA noted that 12 new Gulf fields were expected to start production during 2024–2025, including seven using subsea tiebacks, indicating continued reliance on underwater extensions and monitoring-intensive infrastructure. At the global level, the IEA forecast oil production capacity rising by 5.1 million b/d to 114.7 million b/d by 2030, creating continued need for safe offshore asset integrity management.

Driving factors include methane-control rules, real-time leak detection and digitalized offshore operations. The European Commission states that methane rules focus on measurement, reporting and verification, with stronger leak detection and repair requirements, while EPA/DOE announced about USD 850 million across 43 projects to reduce methane pollution from the oil and gas sector.

BSEE states that it conducts about 20,000 component inspections annually across more than 2,000 offshore facilities in U.S. waters, reinforcing demand for monitoring, compliance and inspection technologies. The IEA also reported that upstream oil and gas costs are set to rise by about 3% in 2025, making predictive maintenance and remote monitoring more attractive for operators seeking fewer shutdowns and lower vessel/ROV intervention costs.

- Government initiatives are reinforcing the outlook. The U.S. Department of the Interior directed BOEM to hold a Gulf lease sale in 2025 and cited technically recoverable Gulf resources of 29.59 billion barrels of oil and 54.84 trillion cubic feet of gas. BOEM’s lease schedule also listed Gulf of America BBG1 for December 10, 2025.

In 2025, SLB strengthened its subsea and monitoring-relevant portfolio through multiple agreements and acquisitions. SLB OneSubsea signed an agreement with Vår Energi in February 2025 for standardized subsea production systems on the Norwegian Continental Shelf. SLB also completed the ChampionX acquisition in July 2025 and expected about $400 million in annual pretax synergies within three years. In September 2025, SLB agreed to acquire RESMAN Energy Technology, a wireless reservoir surveillance company.

By Component Type Analysis

Sensors dominates with 42.7% share due to its critical role in continuous underwater data collection and operational reliability.

In 2025, Sensors held a dominant market position, capturing more than a 42.7% share in the Underwater Monitoring System for Oil and Gas market by component type. This leadership was mainly supported by the growing need for accurate and real-time monitoring of underwater operations across offshore oil and gas facilities. Sensors are considered one of the most important components in underwater monitoring systems because they provide direct measurement and detection of environmental and operational conditions below the sea surface.

By Technology Analysis

Acoustic Monitoring dominates with 39.6% share due to its strong capability in long-range underwater detection and real-time operational monitoring.

In 2025, Acoustic Monitoring held a dominant market position, capturing more than a 39.6% share in the Underwater Monitoring System for Oil and Gas market by technology. Its leading position was supported by the growing requirement for continuous underwater observation and reliable communication across offshore oil and gas operations. Acoustic monitoring became widely preferred because it performs effectively in deepwater environments where visibility is limited and traditional monitoring methods face operational challenges.

By Application Type Analysis

Pipeline Inspection dominates with 37.1% share due to rising focus on subsea asset integrity and uninterrupted offshore operations.

In 2025, Pipeline Inspection held a dominant market position, capturing more than a 37.1% share in the Underwater Monitoring System for Oil and Gas market by application type. This strong position was mainly driven by the increasing importance of maintaining safe and efficient underwater pipeline networks across offshore oil and gas operations. As subsea pipelines continue to transport large volumes of oil and gas over long distances, regular inspection became a critical requirement to avoid leaks, corrosion, and unexpected operational disruptions.

Key Market Segments

By Component Type

- Sensors

- Cameras

- Monitoring Software

- Data Analysis Tools

By Technology

- Acoustic Monitoring

- Optical Monitoring

- Electromagnetic Monitoring

- Remote Operated Vehicles

By Application Type

- Pipeline Inspection

- Environmental Monitoring

- Subsea Infrastructure Monitoring

- Marine Life Research

Emerging Trends

Digital and Autonomous Underwater Monitoring Is Becoming the New Standard Across Offshore Oil and Gas Operations

One of the most important latest trends in the Underwater Monitoring System for Oil and Gas market is the growing shift toward digital and autonomous monitoring technologies. Offshore operators are increasingly moving away from periodic inspections and adopting continuous underwater observation supported by sensors, remote communications, data analytics, and intelligent monitoring platforms. This transition is helping companies improve asset visibility and respond faster to operational changes.

According to the International Energy Agency (IEA), digitalisation is improving the productivity, safety, and operational performance of energy systems globally. Across offshore environments, digital monitoring technologies are being integrated to reduce manual intervention and support real-time decision making. At the same time, recent underwater technology studies highlight growing interest in underwater internet-of-things (UIoT) frameworks that combine sensing, communication, and data processing capabilities for subsea environments.

Offshore Platform Monitoring Is Moving Toward AI-Based and Continuous Observation Models

Another major trend shaping the market is the increasing use of automated monitoring and data-driven offshore infrastructure management. Offshore assets are becoming more distributed and dynamic, creating demand for monitoring systems that can operate continuously with limited physical intervention.

A recent offshore infrastructure study identified approximately 3,728 offshore oil and gas platforms operating across major production regions in 2025. The study also found that more than 2,700 platforms had been installed, relocated, or decommissioned over time, highlighting how rapidly offshore environments are changing. This level of infrastructure movement is encouraging operators to adopt smarter underwater monitoring approaches that combine remote sensing, automated inspection, and predictive analysis.

Drivers

Growing Offshore Oil and Gas Investments Are Increasing the Need for Underwater Monitoring Systems

One of the major factors driving the Underwater Monitoring System for Oil and Gas market is the continued investment in offshore oil and gas production and the growing need to protect underwater infrastructure. Offshore operations are becoming more complex as companies move into deeper waters and expand subsea production networks. This creates a stronger requirement for continuous monitoring to maintain safe and stable operations.

- According to the International Energy Agency (IEA), the Middle East alone is expected to invest around USD 130 billion in oil and gas supply activities in 2025, representing nearly 15% of global oil and gas investment.

At the same time, Middle Eastern and Asian national oil companies account for about 40% of upstream investment globally, compared with 25% in 2015. These large investment flows continue to increase the number of underwater assets such as subsea pipelines, wells, and offshore production facilities that require real-time monitoring and inspection.

Expansion of Offshore Infrastructure and Asset Protection Requirements Is Supporting Market Growth

Another key growth driver is the increasing scale and operational movement of offshore infrastructure worldwide. As offshore platforms and subsea installations grow in number, energy operators are investing more in monitoring technologies to maintain visibility and improve operational control across underwater environments.

Recent offshore infrastructure observations identified approximately 3,728 offshore oil and gas platforms operating across major producing regions in 2025. Among these, around 1,731 platforms were located in the Persian Gulf, 1,641 in the Gulf of Mexico, and 356 in the North Sea. The study also highlighted that more than 2,700 platforms were installed, relocated, or decommissioned over time, showing how dynamic offshore operations have become.

Restraints

High Installation and Maintenance Costs Continue to Limit Wider Adoption of Underwater Monitoring Systems

One of the major restraining factors for the Underwater Monitoring System for Oil and Gas market is the high cost involved in deploying and maintaining underwater monitoring infrastructure. Offshore environments are technically demanding, and installing monitoring equipment below sea level requires specialized vessels, underwater communication systems, inspection tools, and long-term servicing support. These costs become more challenging for operators managing older offshore assets or projects with tighter investment budgets.

- According to the International Energy Agency (IEA), upstream oil and gas costs are expected to increase by around 3% in 2025 due to ongoing inflation and pressure across large engineering and industrial projects.

Rising project expenses directly affect investment decisions related to supporting technologies, including underwater monitoring systems. When offshore operators face increasing capital requirements, spending is often prioritized toward core production assets rather than additional monitoring upgrades.

Increasing Capital Allocation Pressure Reduces Spending Flexibility for Monitoring Technologies

Another important challenge for the market is the growing pressure on oil and gas companies to allocate investment toward maintaining production levels rather than expanding support technologies. Offshore operators increasingly face decisions on where available capital should be directed, especially as production assets become more expensive to sustain.

- According to IEA analysis, nearly 90% of annual upstream investment is currently being used to offset production decline from existing oil and gas fields rather than meeting new demand growth. The agency also noted that oil and gas fields are experiencing average annual post-peak decline rates of 5.6% for conventional oil and 6.8% for natural gas.

Opportunity

Expansion of Deepwater and Subsea Oil Projects Creates Long-Term Opportunity for Underwater Monitoring Systems

One of the biggest growth opportunities for the Underwater Monitoring System for Oil and Gas market comes from the continued expansion of deepwater and subsea oil and gas developments. As offshore energy projects move into deeper and more technically challenging environments, operators are increasing investment in technologies that provide continuous underwater visibility and operational control.

- According to the International Energy Agency (IEA), upstream oil and gas investment is expected to reach around USD 570 billion in 2025.

At the same time, oil supply from non-OPEC+ producers is projected to increase by 3.1 million barrels per day by 2030, supported by new offshore developments and long-term production planning. These investments create a larger installed base of subsea infrastructure including wells, pipelines, production systems, and underwater assets that require constant monitoring and inspection.

Growth in Offshore Infrastructure Monitoring Opens New Revenue Potential

Another major opportunity comes from the increasing number of offshore platforms and the need to manage them more efficiently over time. Offshore infrastructure continues to expand, creating greater demand for technologies that support inspection, maintenance, and operational safety.

Regional Insights

North America dominated the Underwater Monitoring System for Oil and Gas Market with a 36.2% share, accounting for USD 1.2 Billion.

North America emerged as the leading regional market in the Underwater Monitoring System for Oil and Gas industry, holding a dominant 36.2% market share and reaching a value of USD 1.2 Billion. The region’s strong position is supported by its well-developed offshore oil and gas infrastructure, continued investment in subsea production activities, and increasing focus on maintaining aging offshore assets through advanced monitoring technologies.

The United States remains the major contributor within the region due to extensive offshore operations in the Gulf of Mexico, which continues to be one of the world’s most active offshore production zones. According to government energy statistics, offshore areas in the U.S. Gulf of Mexico contribute a significant portion of domestic crude oil production and support large-scale subsea infrastructure networks including pipelines, wells, and production platforms.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Schlumberger Limited continues to hold a strong position in the Underwater Monitoring System for Oil and Gas market through its offshore digital solutions, subsea monitoring capabilities, and integrated field services. The company operates in more than 100 countries and supports offshore energy developments through advanced sensing, data acquisition, and asset performance technologies.

Nexans S.A. is a major supplier of subsea cable and offshore connectivity solutions supporting underwater monitoring applications in oil and gas operations. The company operates in more than 40 countries and reported annual revenue of over EUR 8 billion in recent financial periods. Nexans has delivered thousands of kilometers of subsea cable infrastructure supporting offshore communication and monitoring systems.

Nexans S.A. is a major supplier of subsea cable and offshore connectivity solutions supporting underwater monitoring applications in oil and gas operations. The company operates in more than 40 countries and reported annual revenue of over EUR 8 billion in recent financial periods. Nexans has delivered thousands of kilometers of subsea cable infrastructure supporting offshore communication and monitoring systems.

Top Key Players Outlook

- Schlumberger Limited

- Innovatum, Inc.

- Nexans S.A.

- Kongsberg Gruppen ASA

- Fugro N.V.

- Saab AB

- Halliburton Company

- Baker Hughes Company

- Subsea 7 S.A.

- TechnipFMC plc

- Rowe Technologies, Inc.

- Sonar Products Limited

- Sonardyne International Ltd.

- Oceaneering International, Inc.

- Teledyne Technologies Incorporated

Recent Industry Developments

In 2025, Fugro N.V. reported EUR 1,848.1 million revenue in 2025, with EUR 267.9 million EBITDA, a 14.5% EBITDA margin, and a 12-month backlog of EUR 1,395.9 million. In Partnership & Agreement, Fugro won 4 multi-year Petrobras contracts in June 2025 for inspection and monitoring of critical subsea infrastructure in Brazil, valued at about USD 340 million, running for 4 years with possible 1-year extensions.

In 2025, Saab AB reported SEK 79 billion in sales, SEK 275 billion order backlog, 9.8% operating margin, and around 28,000 employees in 2025, showing strong financial capacity to support underwater technology growth. For Partnership & Agreement, Saab was selected in 2025 to lead NATO’s underwater battlespace project under the MANGROVE consortium, which began on 1 September 2025 and focuses on better use of maritime uncrewed systems. For Merger & Acquisition, Saab acquired Swedish company Deform AB in August 2025, strengthening its submarine production supply chain.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.4 Bn |

| Forecast Revenue (2035) | USD 6.3 Bn |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component Type (Sensors, Cameras, Monitoring Software, Data Analysis Tools), By Technology (Acoustic Monitoring, Optical Monitoring, Electromagnetic Monitoring, Remote Operated Vehicles), By Application Type (Pipeline Inspection, Environmental Monitoring, Subsea Infrastructure Monitoring, Marine Life Research) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Schlumberger Limited, Innovatum, Inc., Nexans S.A., Kongsberg Gruppen ASA, Fugro N.V., Saab AB, Halliburton Company, Baker Hughes Company, Subsea 7 S.A., TechnipFMC plc, Rowe Technologies, Inc., Sonar Products Limited, Sonardyne International Ltd., Oceaneering International, Inc., Teledyne Technologies Incorporated |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |