Quick Navigation

Report Overview

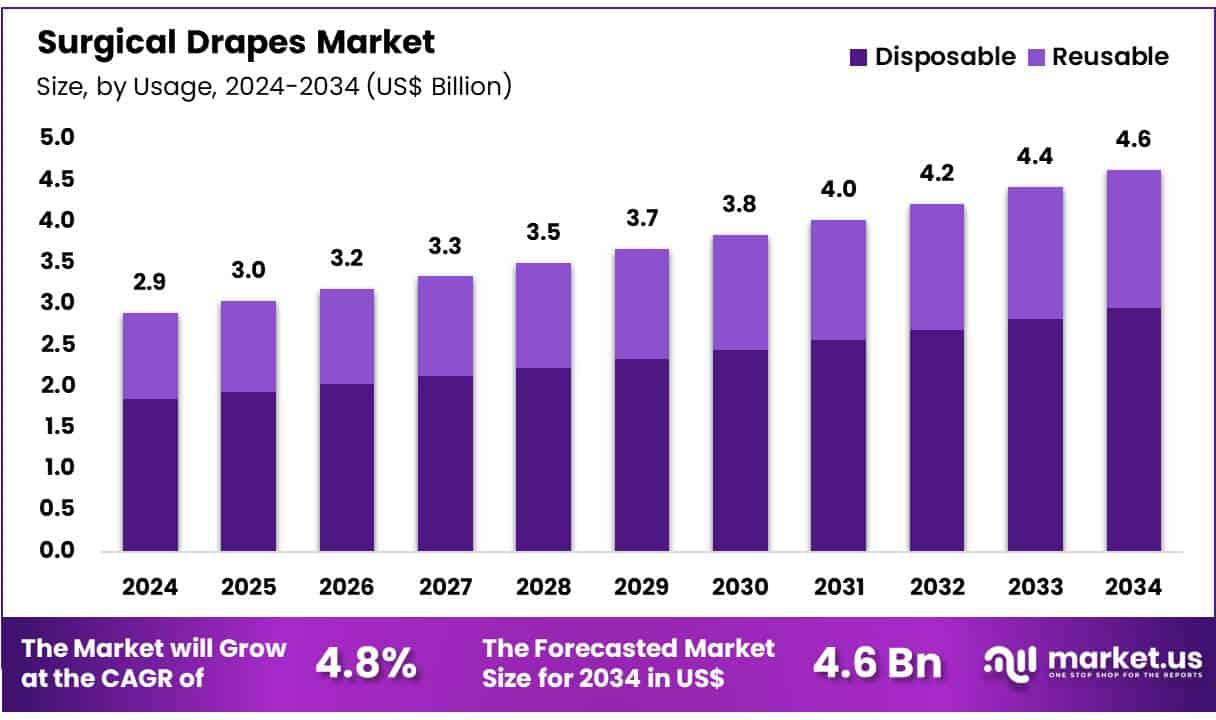

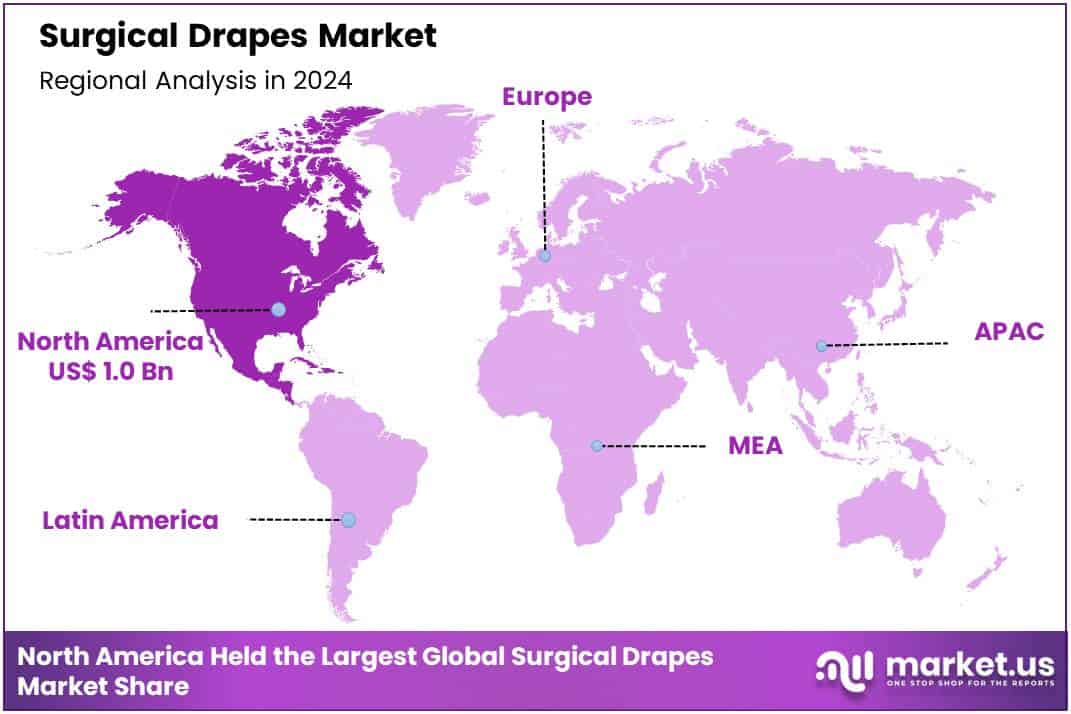

Global Surgical Drapes Market size is expected to be worth around US$ 4.6 Billion by 2034 from US$ 2.9 Billion in 2024, growing at a CAGR of 4.8% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 35.2% share with a revenue of US$ 1.0 Billion.

The global surgical drapes sector is experiencing steady expansion, supported by several structural trends across the healthcare system. The rise in surgical procedures worldwide remains one of the strongest drivers. WHO-supported research indicates that surgical operations increased from 226.4 million in 2004 to 312.9 million in 2012, reflecting growth of more than 30% within eight years.

Current estimates suggest that about 310 million major surgeries are performed each year, and this number is expected to rise further as populations age and access to surgical care improves. Every procedure requires sterile draping, which directly strengthens demand for high-quality surgical drapes across all regions.

The burden of healthcare-associated infections (HAIs) adds strong momentum to this market. WHO states that 1 in 10 patients globally experiences at least one HAI. In the United States, CDC data show approximately 687,000 HAIs in acute care hospitals in 2015, leading to about 72,000 deaths. These infections cost hospitals tens of billions of dollars annually. Surgical site infections are among the most common HAIs in Europe, according to ECDC. This high clinical and economic burden reinforces strict infection-prevention practices, where surgical drapes serve as essential barriers that limit contamination between patients, staff, and equipment.

Stronger infection-prevention and control (IPC) guidelines further support market growth. WHO reports that effective IPC programmes can reduce HAIs by up to 70%. Global guidelines permit the use of sterile disposable non-woven or reusable woven drapes, provided they deliver effective protection. National frameworks, such as the NHS IPC manual, encourage single-use items and standardized sterile environments. As hospitals work to comply with these requirements, they increasingly replace basic textiles with advanced draping systems.

Demographic changes contribute to additional demand. Ageing populations in high- and middle-income countries drive higher volumes of surgeries for chronic diseases. OECD data show average hip and knee replacement rates of 172 and 119 procedures per 100,000 population, respectively. Over 2 million hip and knee replacements occur each year worldwide. Each procedure requires extensive sterile draping, supporting market growth in orthopaedic, cardiac, and oncology surgery segments.

Low- and middle-income countries are expanding surgical capacity to close the global care gap, with WHO estimating the need for 143 million additional surgical procedures annually. As new facilities open, baseline demand for cost-effective, compliant draping products rises. At the same time, concerns over antimicrobial resistance, regulatory pressure, and sustainability targets are shifting hospitals toward high-performance, environmentally responsible drape systems. Together, these factors create a strong long-term outlook for the surgical drapes market.

Key Takeaways

- Market Size: Global Surgical Drapes Market size is expected to be worth around US$ 4.6 Billion by 2034 from US$ 2.9 Billion in 2024.

- Market Growth: The market growing at a CAGR of 4.8% during the forecast period from 2025 to 2034.

- Usage Analysis: The dominance of disposable drapes has been reinforced in 2024, as this segment accounted for 63.7% of the total market share.

- Product Analysis: In 2024, fenestrated drapes accounted for 28.5% of the global market share, establishing this segment as the leading product category.

- Material/Fabric Analysis: The SMS (Spunbonded + Meltblown + Spunbonded) non-woven fabric segment accounted for 37.7% of the global market share in 2024.

- Risk/Barrier Protection Level Analysis: Moderate protection (AAMI Level 3) accounts for an estimated 39.0% of the global market in 2024.

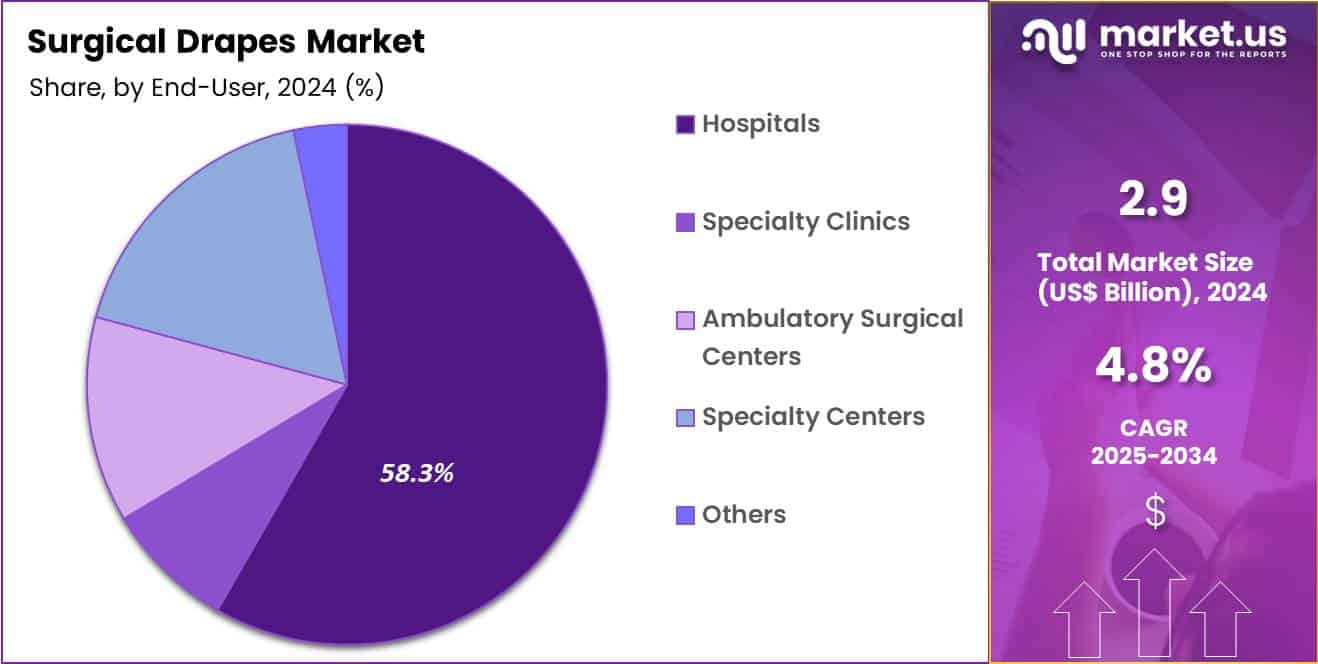

End-Use Analysis: Hospitals account for an estimated 58.3% share of the global market in 2024.

- Regional Analysis: In 2024, North America led the market, achieving over 35.2% share with a revenue of US$ 1.0 Billion.

Usage Analysis

The global market for surgical drapes has been segmented based on usage into disposable and reusable categories. The dominance of disposable drapes has been reinforced in 2024, as this segment accounted for 63.7% of the total market share. The growth of this segment can be attributed to the rising emphasis on infection prevention, strict regulatory standards, and increased procedural volumes in hospitals and ambulatory surgical centers. Single-use drapes are widely adopted because they reduce the risk of cross-contamination and eliminate the need for sterilization cycles, which supports operational efficiency.

Reusable drapes continue to represent a smaller but steady segment of the market. Their adoption is supported by long-term cost benefits and sustainability initiatives in certain healthcare systems. However, the reliance on complex reprocessing workflows and concerns about fabric integrity after repeated laundering have limited their expansion. Overall, disposable drapes are expected to maintain a leading position due to strong compliance and hygiene advantages.

Product Analysis

The product portfolio of the surgical drapes market has been categorized into fenestrated drapes, incise drapes, non-fenestrated drapes, fluid-resistant drapes, specialty drapes, split drapes, extremity drapes, and other ancillary drape products. In 2024, fenestrated drapes accounted for 28.5% of the global market share, establishing this segment as the leading product category.

The dominance of fenestrated drapes can be attributed to their extensive utilization in procedures requiring controlled access to the surgical site, as well as their compatibility with a wide range of general and specialty surgeries. Their design facilitates efficient workflow, maintains a sterile field, and minimizes contamination risks, which supports their continued market strength.

Incise drapes represent a notable share due to their adhesive properties that secure the surgical area and enhance aseptic conditions. Non-fenestrated drapes continue to serve as essential protective coverings across various clinical settings. Fluid-resistant drapes have experienced increased demand as operating rooms emphasize fluid management and enhanced barrier protection.

Specialty drapes, split drapes, and extremity drapes address specific procedural requirements, thereby contributing to diversified adoption across surgical departments. Although these segments remain smaller individually, their cumulative contribution reflects the market’s preference for application-specific draping solutions that meet evolving surgical standards.

Material/Fabric Analysis

The material composition of surgical drapes has been shaped by the increasing demand for barrier efficiency, cost-effectiveness, and compliance with stringent infection-control protocols. The SMS (Spunbonded + Meltblown + Spunbonded) non-woven fabric segment accounted for 37.7% of the global market share in 2024, and its dominance has been linked to the balanced combination of strength, filtration efficiency, and fluid resistance achieved through multilayer construction. The segment has also benefited from the rising preference for disposable, sterile solutions in operating rooms, where consistent quality and reduced contamination risk are required.

Woven textile fabrics continue to hold a notable position due to their durability and reusability. Their adoption has been sustained in cost-sensitive healthcare environments where laundering and sterilization infrastructure is available. However, growth has remained comparatively moderate, as the shift toward single-use drapes has accelerated.

Long-fiber polyester fiber fabrics have gained traction in high-performance surgical settings. Their dimensional stability, tear resistance, and favourable breathability have supported adoption in advanced operating theatres. The “Others” category, which includes composite materials and specialty laminates, represents a smaller share but is expected to expand gradually as innovation in antimicrobial coatings and bio-based materials continues.

Risk/Barrier Protection Level Analysis

The surgical drapes market is segmented by Risk/Barrier Protection Level, and the demand distribution reflects the increasing emphasis on infection control and fluid-resistant materials across operating environments. Moderate protection (AAMI Level 3) accounts for an estimated 39.0% of the global market in 2024, and this segment has been supported by rising adoption in general surgeries where a balance between comfort, breathability, and barrier efficiency is required. Its dominance can be attributed to its ability to provide reliable protection against moderate fluid exposure, making it suitable for a broad set of procedures across high-volume healthcare facilities.

Minimal protection (AAMI Level 1) and Minimal to Low protection (AAMI Level 2) categories continue to serve routine, low-risk procedures. Their usage has been sustained by cost-efficiency requirements in outpatient settings, although their overall market share remains comparatively lower due to limited resistance to fluid penetration. The Highest protection category (AAMI Level 4) is utilized in complex and invasive surgeries where maximum fluid and pathogen barrier performance is required. Growth in this segment has been supported by the increasing number of high-acuity surgical cases, although adoption remains concentrated in specialized clinical environments.

By End-User Analysis

By end user, and demand patterns are shaped by procedure volumes, infection-prevention protocols, and procurement capabilities across healthcare facilities. Hospitals account for an estimated 58.3% share of the global market in 2024, and this dominance is driven by the high concentration of complex, high-acuity surgical procedures performed in these settings.

The presence of advanced operating rooms, stringent sterilization standards, and large patient inflows has supported continuous consumption of high-quality draping systems. Centralized purchasing departments in hospitals have also enabled consistent adoption of premium single-use sterile drapes to reduce cross-contamination risks.

Specialty clinics represent a growing segment, supported by the expansion of dermatology, ophthalmology, orthopedics, and obstetrics procedures that require focused sterile fields. Although their share remains smaller, demand has been increasing due to the rise in minimally invasive treatments. Ambulatory surgical centers have continued to gain traction as outpatient procedures expand, and their preference for cost-effective, disposable drapes has reinforced steady market uptake.

Specialty centers, including cardiac and cancer institutes, contribute additional demand where advanced barrier protection is required. The “other” category includes smaller healthcare facilities and academic institutions, where usage is moderate but consistent due to training and minor procedural needs.

Key Market Segments

By Usage

- Disposable

- Reusable

By Product

- Incise drapes

- Fenestrated drapes

- Non-Fenestrated Drapes

- Fluid-Resistant Drapes

- Specialty Drapes

- Split drapes

- Extremity drapes

- Other

By Material/Fabric

- SMS (Spunbonded + Meltblown + Spunbonded) non-woven fabric

- Woven textile fabric

- Long-fiber polyester fiber fabric

- Others

By Risk/Barrier Protection Level

- Minimal (AAMI Level 1)

- Minimal to Low (AAMI Level 2)

- Moderate (AAMI Level 3)

- Highest (AAMI Level 4)

By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Specialty Centers

- Others

Market Driver

The growth of the surgical drapes market is primarily driven by the rising global surgical volume and the persistent burden of healthcare-associated infections (HAIs). The World Health Organization (WHO) estimates that over 300 million surgical procedures are performed each year worldwide, and surgery accounts for around 13% of total disability-adjusted life years (DALYs).

HAIs affect on average 1 in 10 patients globally, with higher rates in low- and middle-income countries. In the United States, the CDC reported an estimated 687,000 HAIs in acute care hospitals in 2015, with about 72,000 related deaths, and 3% of hospitalized patients having at least one HAI.

Surgical site infections (SSIs) account for a substantial share of these events, with about 110,800 SSIs linked to inpatient surgeries in 2015. As infection-prevention protocols increasingly emphasize sterile barriers, demand for high-performance surgical drapes is being reinforced across hospitals and ambulatory surgical centers.

Market Trend

The global number of surgical interventions has grown substantially, thereby underpinning increased demand for surgical drapes. According to World Health Organization (WHO), in low- and middle-income countries approximately 11 % of patients undergoing surgery develop a surgical-site infection (SSI) — indicating both high volume and high stake for sterile drape usage.

For example, in Europe 2021-22 data show 10,193 SSIs from 662,309 monitored procedures across 11 member states, implying an infection incidence up to 9.6 % in certain surgery types. Because surgical drapes form a fundamental barrier in sterile fields, increasing surgery volume directly correlates with higher drape consumption. This trend is further reinforced by growth in ambulatory surgical centres, minimally invasive surgical approaches, and expanding surgical access in emerging markets. The implication is sustained upward pressure on drape demand, while the need for higher performance barrier materials also increases.

Market Restraint

Despite favourable infection-control drivers, the surgical drapes market is constrained by cost pressures and structural gaps in infection surveillance, particularly in low- and middle-income countries (LMICs). WHO and partner analyses indicate that 7 out of every 100 hospitalized patients develop an HAI in high-income countries, rising to 15 per 100 patients in LMICs. However, only about 16% of LMICs had national or sub-national HAI surveillance systems in place around 2010, limiting systematic procurement of higher-specification disposable drapes.

Budget-constrained facilities may continue to use lower-cost textiles or reuse protocols, even where guidelines recommend sterile, single-use barriers. Environmental concerns around the volume of non-woven medical waste generated by disposable drapes also lead some health systems to adopt conservative usage policies. In addition, variability in clinical practice and adherence to IPC bundles can restrict the full infection-reduction benefit that premium drapes are designed to deliver.

Market Opportunity

Significant opportunity exists in aligning surgical drape innovation with global IPC and antimicrobial resistance (AMR) agendas. A recent WHO-supported analysis indicates that antibiotic-resistant HAIs account for over 130 million cases annually, with the majority occurring in middle-income countries, underscoring the need for stronger prevention at the surgical field.

Surgical drapes with enhanced barrier properties, fluid control and antimicrobial features can be positioned as key components of national IPC strategies and SSI-reduction bundles. ECDC and CDC documents emphasize SSIs as among the most common HAIs, linked to prolonged length of stay and higher costs, providing a strong clinical and economic case for higher-performance draping solutions.

Emerging markets, where surgical volumes are rising rapidly and IPC programmes are being formalized, represent a substantial untapped segment. Targeted education, government tenders and value-based procurement models can unlock incremental adoption of premium drapes in these regions.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 35.2% share and holding a market value of about US$ 1.0 billion for the year. The strong position of the region can be attributed to the high volume of surgical procedures performed across the United States and Canada. A well-established hospital network and a strong presence of advanced healthcare facilities have supported sustained demand. Adoption of disposable and protective surgical drapes has increased as strict infection-prevention standards have been reinforced in clinical settings. This has further strengthened regional consumption patterns.

Growth in outpatient surgeries and a rising focus on sterile environments have also contributed. Ambulatory surgical centers have expanded their procedural capacity, and this expansion has generated consistent demand for barrier-protective drapes. The presence of clear regulatory guidelines has supported the use of high-quality surgical draping materials. This environment has created stable procurement cycles among healthcare providers.

Technological improvements in nonwoven fabrics and fluid-resistant materials have enhanced product performance. These improvements have encouraged providers to shift from reusable to disposable drapes. The shift has been supported by an increased emphasis on minimizing cross-contamination risks. As a result, the region has maintained its leadership position.

Overall, steady healthcare spending, advanced clinical practices, and a strong regulatory framework have reinforced North America’s dominance in the surgical drapes market. The region is expected to maintain a leading share as safety protocols and surgical procedure volumes continue to rise.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

A competitive landscape has been characterized by the presence of several global and regional manufacturers that emphasize product innovation, sterilization standards, and cost efficiency. Market growth has been supported by continuous advancements in disposable nonwoven materials, improved barrier performance, and infection-control technologies. Leading participants have focused on expanding product portfolios, enhancing resistance to fluid penetration, and developing eco-friendly draping solutions.

Strategic activities have included capacity expansion, regulatory compliance improvements, and collaborations with healthcare facilities to strengthen procurement channels. Premium-grade solutions have been positioned toward high-acuity procedures, while value-based offerings have targeted cost-sensitive settings. The competitive environment has remained moderately consolidated, and differentiation has been achieved through material quality, customization capabilities, global distribution networks, and consistent adherence to surgical safety protocols.

Market Key Players

- 3M Company

- Mölnlycke Health Care

- Amaryllis Healthcare Pvt Ltd

- AdvaCare Pharma

- Medline Industries, Inc.

- Cardinal Health, Inc.

- Steris plc

- Paul Hartmann AG

- Standard Textile Co.

- Priontex

- OneMed

- Medic

- Lohmann & Rauscher GmbH & Co. KG

- Ahlstrom‑Munksjö Oyj

- Sterimed Group

- Medica Europe BV

- Winner Medical Co. Ltd.

Recent Developments

- 3M Company (Jun 2023): 3M introduced its Steri-Drape™ Surgical Specialty Drapes incorporating Ioban™ 2 Incise Film, offering a fluid-resistant barrier and antimicrobial properties to help reduce surgical-site infection risk.

- Mölnlycke Health Care (May 2025): Mölnlycke’s joint-venture in Saudi Arabia with Tamer Mölnlycke Care commenced manufacture of customised surgical trays and surgical drapes locally, enabling regional supply and production scalability.

- Medline Industries, Inc. (Aug 2024): Medline closed acquisition of the global surgical-solutions business of Ecolab Inc., including the Microtek™ sterile-drape lines, enhancing its operating-room drape portfolio.

- Paul Hartmann AG 2024: The company introduced more cost-effective sterile drapes with enhanced fluid-resistance and hygiene performance in Europe, responding to market demand for high-barrier infection-control products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 2.9 Billion |

| Forecast Revenue (2034) | US$ 4.6 Billion |

| CAGR (2025-2034) | 4.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Usage (Disposable, Reusable) By Product (Incise drapes, Fenestrated drapes, Non-Fenestrated Drapes, Fluid-Resistant Drapes, Specialty Drapes, Split drapes, Extremity drapes, Other) By Material/Fabric (SMS (Spunbonded + Meltblown + Spunbonded) non-woven fabric, Woven textile fabric, Long-fiber polyester fiber fabric, Others) By Risk/Barrier Protection Level (Minimal (AAMI Level 1), Minimal to Low (AAMI Level 2), Moderate (AAMI Level 3), Highest (AAMI Level 4)) By End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Specialty Centers, Others) |

| Regional Analysis | North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA |

| Competitive Landscape | 3M Company, Mölnlycke Health Care, Amaryllis Healthcare Pvt Ltd, AdvaCare Pharma, Medline Industries, Inc., Cardinal Health, Inc., Steris plc, Paul Hartmann AG, Standard Textile Co., Priontex, OneMed, Medic, Lohmann & Rauscher GmbH & Co. KG, Ahlstrom‑Munksjö Oyj, Sterimed Group, Medica Europe BV, Winner Medical Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |