Quick Navigation

Report Overview

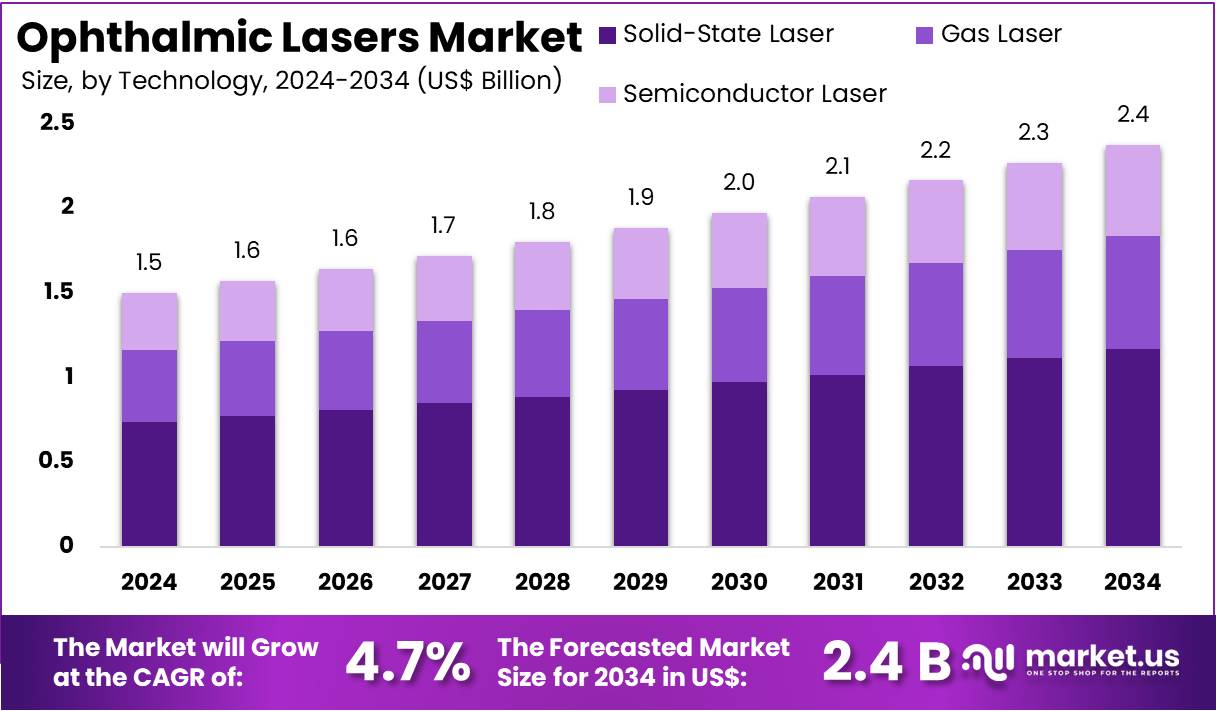

The Ophthalmic Lasers Market size is expected to be worth around US$ 2.4 billion by 2034 from US$ 1.5 billion in 2024, growing at a CAGR of 4.7% during the forecast period 2025 to 2034.

Increasing adoption of ophthalmic lasers for treating conditions such as cataracts, glaucoma, and refractive errors is driving the growth of the ophthalmic lasers market. The advancements in laser technology, such as femtosecond lasers and excimer lasers, have led to more precise treatments with faster recovery times, encouraging both patients and healthcare professionals to opt for these procedures. The shift toward minimally invasive surgeries further boosts the demand for laser-assisted treatments.

Innovations in laser-based diagnostics and treatments, along with rising awareness of eye diseases, offer considerable growth opportunities. A growing elderly population, who are more prone to conditions like cataracts and glaucoma, will likely increase the market’s scope. Additionally, the introduction of combination therapies and increasing use of lasers in aesthetic procedures such as laser vision correction are expected to contribute to market expansion. According to the World Health Organization, over 2.2 billion people suffer from vision impairment globally, with cataracts being a leading cause, contributing to the increasing demand for ophthalmic lasers.

Key Takeaways

- In 2024, the market for ophthalmic lasers generated a revenue of US$ 1.5 billion, with a CAGR of 4.7%, and is expected to reach US$ 2.4 billion by the year 2034.

- The product type segment is divided into YAG laser, femtosecond laser, diode laser, and argon laser, with femtosecond laser taking the lead in 2024 with a market share of 41.9%.

- Considering technology, the market is divided into gas laser, solid-state laser, and semiconductor laser. Among these, solid-state laser held a significant share of 49.2%.

- Furthermore, concerning the application segment, the market is segregated into laser eye surgery, cataract surgery, retinal procedures, and glaucoma treatment. The cataract surgery sector stands out as the dominant player, holding the largest revenue share of 46.4% in the ophthalmic lasers market.

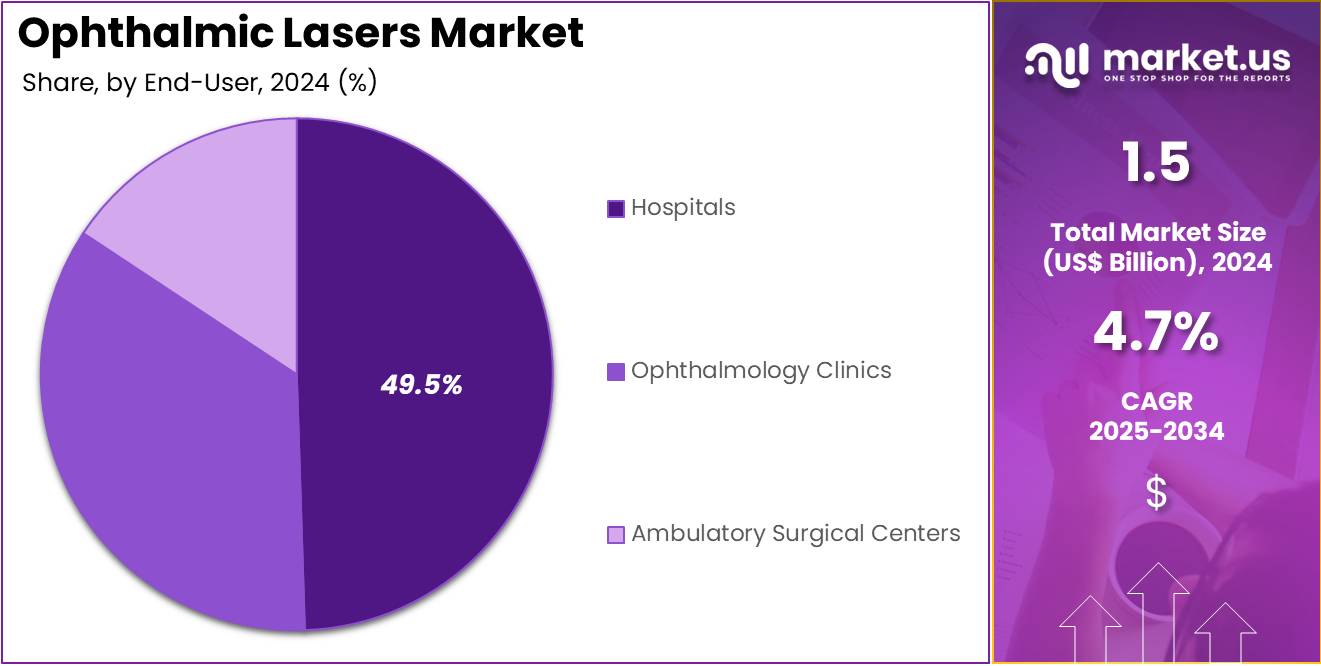

- The end-user segment is segregated into ophthalmology clinics, hospitals, and ambulatory surgical centers, with the hospitals segment leading the market, holding a revenue share of 49.5%.

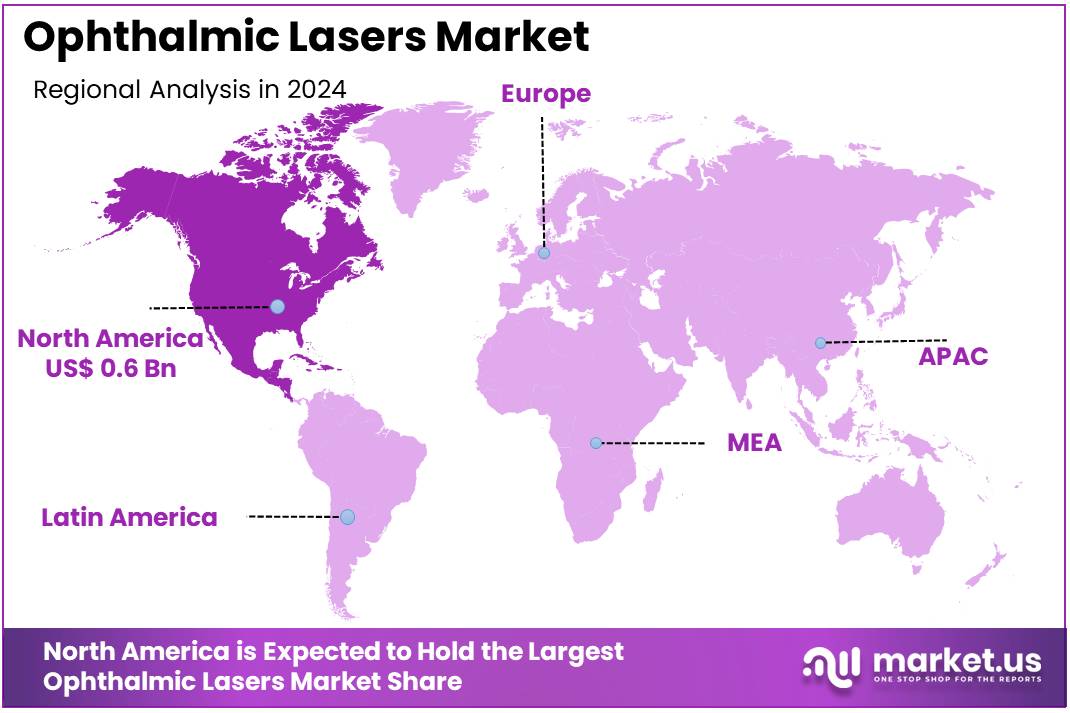

- North America led the market by securing a market share of 39.1% in 2024.

Product Type Analysis

The femtosecond laser segment led in 2024, claiming a market share of 41.9% owing to its advanced capabilities in precision and minimally invasive procedures. This segment is anticipated to expand as femtosecond lasers offer superior accuracy and reduced recovery times compared to traditional methods, especially in cataract surgeries and refractive procedures.

The growing demand for safer and more effective treatments is likely to drive the adoption of femtosecond lasers, particularly in surgeries that require delicate tissue manipulation. Additionally, the increased popularity of laser-assisted surgeries and advancements in femtosecond laser technology, which allow for more customized treatments, are projected to contribute to this segment’s growth. As patients and healthcare providers seek cutting-edge surgical options, the femtosecond laser market is likely to see continued expansion.

Technology Analysis

The solid-state laser held a significant share of 49.2% due to its numerous advantages, including high efficiency, reliability, and durability. Solid-state lasers are expected to become more popular in ophthalmic procedures due to their compact size, ease of use, and precision. These lasers are anticipated to be increasingly favored for their ability to provide high-quality results in treatments like retinal surgeries and glaucoma management.

The growing focus on minimally invasive procedures and the rise in laser technology integration into various ophthalmic treatments are projected to further boost the adoption of solid-state lasers. With ongoing advancements in solid-state laser technology, including improved beam quality and power efficiency, the segment is likely to continue expanding, meeting the rising demand for advanced eye care solutions.

Application Analysis

The cataract surgery segment had a tremendous growth rate, with a revenue share of 46.4% as cataract surgery continues to be one of the most common eye procedures worldwide. The demand for laser-assisted cataract surgeries is anticipated to increase as patients seek more precise, faster, and safer treatment options. Laser technology, particularly femtosecond lasers, has revolutionized cataract surgery by enhancing surgical outcomes and reducing recovery times.

As the global aging population rises and cataract cases increase, the need for innovative solutions in cataract surgery is projected to grow. Additionally, the growing preference for outpatient cataract surgeries and the increased adoption of laser-based systems are expected to fuel the expansion of this segment. The rising awareness of the benefits of laser cataract surgery is likely to contribute to its widespread acceptance.

End-user Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 49.5% due to the increasing number of patients seeking advanced eye care treatments. Hospitals are projected to remain the primary settings for complex and high-volume ophthalmic procedures, such as cataract surgeries and glaucoma treatments, which require advanced laser technologies. The growing prevalence of eye diseases, coupled with the adoption of advanced ophthalmic laser systems for more accurate and effective procedures, is likely to drive the demand for lasers in hospitals.

Additionally, hospitals’ ability to offer a wide range of surgical services, including emergency and elective procedures, is anticipated to support the growth of this segment. As hospitals continue to invest in state-of-the-art equipment and specialized ophthalmic care, this segment is expected to see consistent expansion in the coming years.

Key Market Segments

By Product Type

- YAG Laser

- Femtosecond Laser

- Diode Laser

- Argon Laser

By Technology

- Gas Laser

- Solid-State Laser

- Semiconductor Laser

By Application

- Laser Eye Surgery

- Cataract Surgery

- Retinal Procedures

- Glaucoma Treatment

By End-user

- Ophthalmology Clinics

- Hospitals

- Ambulatory Surgical Centers

Drivers

Advancements in Laser Technology are Driving the Market

The ophthalmic lasers market is experiencing significant growth due to continuous technological advancements. Innovations such as femtosecond lasers have revolutionized procedures like cataract surgery, offering increased precision and reduced recovery times. For instance, Alcon, a leading company in the ophthalmic sector, has developed advanced femtosecond laser systems designed for cataract surgeries, enhancing surgical outcomes and patient safety.

These technological strides not only improve patient experiences but also expand the capabilities of ophthalmologists, thereby driving market expansion. As companies like Alcon continue to invest in research and development, the market is poised for further growth, meeting the evolving needs of eye care professionals and patients alike.

Restraints

High Costs of Laser Equipment are Restraining the Market

The high costs of ophthalmic laser equipment create a major barrier to market growth. Advanced laser systems require significant investment, making them difficult for smaller clinics and healthcare facilities to afford. This issue is more severe in developing regions, where financial constraints limit access to cutting-edge medical technologies. Many healthcare providers struggle to invest in these systems due to the high upfront costs and ongoing maintenance expenses. As a result, patients in underserved areas may not receive the latest ophthalmic treatments, reducing market expansion potential.

To overcome this challenge, cost-effective solutions and flexible financial models are essential. Leasing options, government subsidies, and technological advancements can help lower costs. Manufacturers should focus on developing affordable laser systems without compromising quality. Partnerships between medical institutions and financial organizations can also improve accessibility. By making ophthalmic lasers more affordable, healthcare providers can expand their treatment offerings. This shift would enhance patient care while driving market growth, particularly in regions with limited healthcare funding.

Opportunities

Emerging Markets are Creating Growth Opportunities

Emerging markets in the Asia-Pacific region offer strong growth opportunities for the ophthalmic lasers market. Countries like China and India are witnessing rising demand due to improving healthcare infrastructure and growing awareness of advanced ophthalmic treatments. As more patients seek modern eye care solutions, the market is expected to expand. Companies are recognizing these trends and investing in these regions to build a strong presence. Strategic collaborations with local healthcare providers can help businesses navigate regulatory challenges and increase adoption of advanced laser treatments.

Tailored product offerings designed for regional needs can further drive market penetration. Many companies are focusing on affordability and accessibility to cater to a diverse patient base. As these economies continue to develop, disposable incomes are rising, making premium healthcare services more accessible. The demand for ophthalmic laser treatments is expected to grow significantly in the coming years. This trend creates a favorable environment for companies looking to expand in Asia-Pacific’s ophthalmic lasers market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a crucial role in shaping the ophthalmic lasers market. Economic downturns often lead to lower healthcare spending, reducing investments in advanced medical equipment. Geopolitical tensions can disrupt global supply chains, affecting the availability of essential components for laser systems.

Trade restrictions and tariffs may further increase production costs, impacting pricing strategies. These challenges can slow market growth and limit technological advancements. However, companies that diversify supply sources and optimize manufacturing processes can reduce risks and maintain steady operations.

Despite these challenges, supportive government policies can drive market growth. Investments in healthcare infrastructure encourage the adoption of advanced ophthalmic technologies. In regions prioritizing healthcare, increased funding can boost demand for innovative laser systems.

Additionally, international collaborations foster research and technological advancements, expanding market opportunities. Strategic partnerships can help companies navigate uncertainties and enhance their market presence. Overall, while obstacles exist, proactive planning and strong policies can ensure steady growth in the ophthalmic lasers market.

Trends

Integration of Artificial Intelligence is a Recent Trend

The integration of artificial intelligence (AI) into ophthalmic laser systems is an emerging trend enhancing diagnostic and therapeutic precision. AI algorithms can analyze complex ocular data, assisting in the early detection of conditions like glaucoma and diabetic retinopathy. This technological synergy enables personalized treatment plans, improving patient outcomes.

Leading companies are investing in AI-driven platforms to augment their laser systems’ capabilities. This trend reflects the industry’s commitment to leveraging advanced technologies to meet evolving healthcare needs. As AI continues to evolve, its integration into ophthalmic practices is poised to set new standards in patient care.

Regional Analysis

North America is leading the Ophthalmic Lasers Market

North America dominated the market with the highest revenue share of 39.1% owing to increasing demand for advanced laser technologies for treating various eye conditions such as glaucoma, cataracts, and diabetic retinopathy. The aging population in the region, which has a higher risk of eye-related diseases, contributed to the rising need for efficient and minimally invasive treatment options.

Additionally, the growing awareness of the benefits of laser therapies, including faster recovery times and reduced risk of complications, further fueled market expansion. Technological advancements, such as the integration of precision and AI-powered lasers, improved treatment outcomes and patient satisfaction. In March 2021, Lumenis Ltd. collaborated with the Advent Health Nicholson Center to establish an advanced medical training facility.

This initiative provided physicians with hands-on experience in a controlled setting, ensuring continuous education and skill development during the pandemic. These efforts have contributed to the growing adoption of ophthalmic lasers in clinical practices across North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness the fastest growth in the ophthalmic lasers market due to rising healthcare investments and increasing awareness of advanced treatments. The region has a growing elderly population prone to ocular diseases like cataracts and glaucoma. This rising prevalence is driving demand for laser-based treatment solutions.

Additionally, improving healthcare infrastructure and government initiatives focused on healthcare access and affordability are key factors supporting market expansion. These developments are expected to fuel rapid growth in the adoption of ophthalmic laser technologies across the region.

In June 2022, Iridex Corporation received regulatory approval from China’s National Medical Products Administration (NMPA) for its Cyclo G6 system. This non-invasive glaucoma treatment platform marked a significant milestone in expanding access to advanced eye care solutions in the region. With continuous advancements in laser technology and rising healthcare expenditures, the Asia Pacific ophthalmic lasers market is projected to grow at a strong pace. Increasing investments in ophthalmic care will further drive the adoption of laser-based treatments in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the ophthalmic lasers market focus on advancing laser technologies, such as femtosecond and excimer lasers, to improve precision in eye surgeries like cataract removal and refractive corrections. Companies invest in research and development to enhance laser safety, reduce procedure times, and improve patient outcomes.

Strategic partnerships with ophthalmology clinics and hospitals help expand product adoption and increase access to advanced treatments. Many players also emphasize the development of user-friendly, portable devices to cater to smaller practices and global markets. Geographic expansion into emerging markets with growing healthcare infrastructure supports further growth.

Top Key Players in the Ophthalmic Lasers Market

- Valon Lasers

- Topcon

- QIAGEN

- Optos

- IRIDEX Corporation

- Eurofins Scientific

- Ellex Medical Lasers

- Ampath

Recent Developments

- In April 2022, Lumibird Group launched a newly developed ophthalmic laser system, designed to improve the precision of capsulotomy and iridotomy procedures. The advanced laser technology provides ophthalmologists with a more efficient and accurate treatment tool, enhancing patient outcomes in vision correction.

- In March 2021, Iridex Corporation entered a strategic partnership with Topcon Corporation to enhance its global distribution network. By integrating Iridex’s laser-based ophthalmic treatments with Topcon’s diagnostic solutions, the partnership aimed to expand access to innovative glaucoma and retina care technologies in key international markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.5 billion |

| Forecast Revenue (2034) | US$ 2.4 billion |

| CAGR (2025-2034) | 4.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (YAG Laser, Femtosecond Laser, Diode Laser, and Argon Laser), By Technology (Gas Laser, Solid-State Laser, and Semiconductor Laser), By Application (Laser Eye Surgery, Cataract Surgery, Retinal Procedures, and Glaucoma Treatment), By End-user (Ophthalmology Clinics, Hospitals, and Ambulatory Surgical Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Valon Lasers, Lumibird Group, QIAGEN, Optos, IRIDEX Corporation, Eurofins Scientific, Ellex Medical Lasers, and Ampath. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |