Quick Navigation

Report Overview

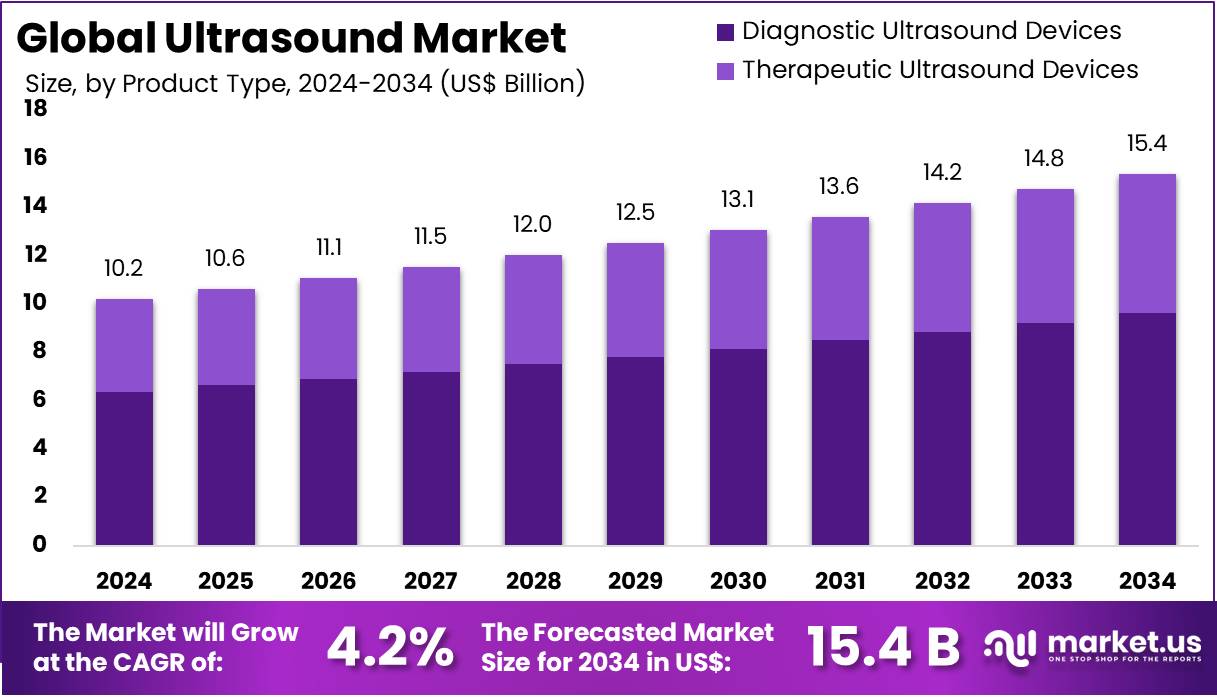

The Ultrasound Market size is expected to be worth around US$ 15.4 billion by 2034 from US$ 10.2 billion in 2024, growing at a CAGR of 4.2% during the forecast period 2025 to 2034.

Increasing adoption of ultrasound technology in medical diagnostics, along with continuous advancements in imaging capabilities, is driving the growth of the ultrasound market. Ultrasound devices play a crucial role in a wide range of applications, including obstetrics and gynecology, cardiology, musculoskeletal imaging, and abdominal imaging.

Rising demand for non-invasive diagnostic procedures and the preference for cost-effective, portable imaging devices are further boosting market expansion. Technological innovations, such as the integration of artificial intelligence (AI) and cloud-based solutions, are enhancing the precision and efficiency of ultrasound imaging, making it an indispensable tool in both routine and emergency healthcare settings.

Growing awareness of early disease detection, particularly in pregnancy and chronic conditions like cardiovascular diseases, contributes to the increasing use of ultrasound. Moreover, the shift towards point-of-care diagnostics, supported by portable and handheld ultrasound devices, is opening new opportunities in home healthcare and emergency care settings. According to the US Food and Drug Administration (FDA), the number of ultrasound procedures in the US has risen significantly, with more than 20 million ultrasound procedures performed annually, highlighting the widespread adoption of ultrasound as a diagnostic tool.

Key Takeaways

- In 2024, the market for ultrasound generated a revenue of US$ 10.2 billion, with a CAGR of 4.2%, and is expected to reach US$ 15.4 billion by the year 2034.

- The product type segment is divided into diagnostic ultrasound devices and therapeutic ultrasound devices, with diagnostic ultrasound devices taking the lead in 2024 with a market share of 62.4%.

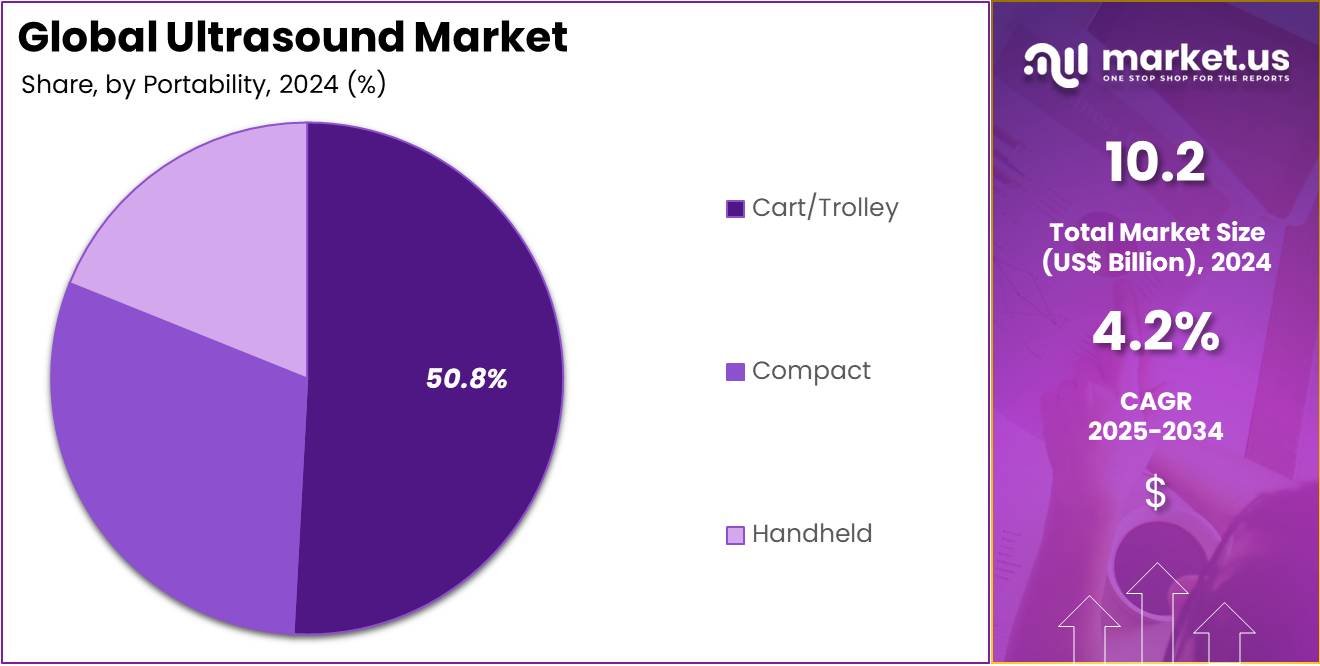

- Considering portability, the market is divided into cart/trolley, compact, and handheld. Among these, cart/trolley held a significant share of 50.8%.

- Furthermore, concerning the application segment, the market is segregated into cardiology, obstetrics/gynecology, orthopedic, radiology, and others. The radiology sector stands out as the dominant player, holding the largest revenue share of 48.9% in the ultrasound market.

- The end-user segment is segregated into hospitals, research centers, and imaging centers, with the hospitals segment leading the market, holding a revenue share of 54.3%.

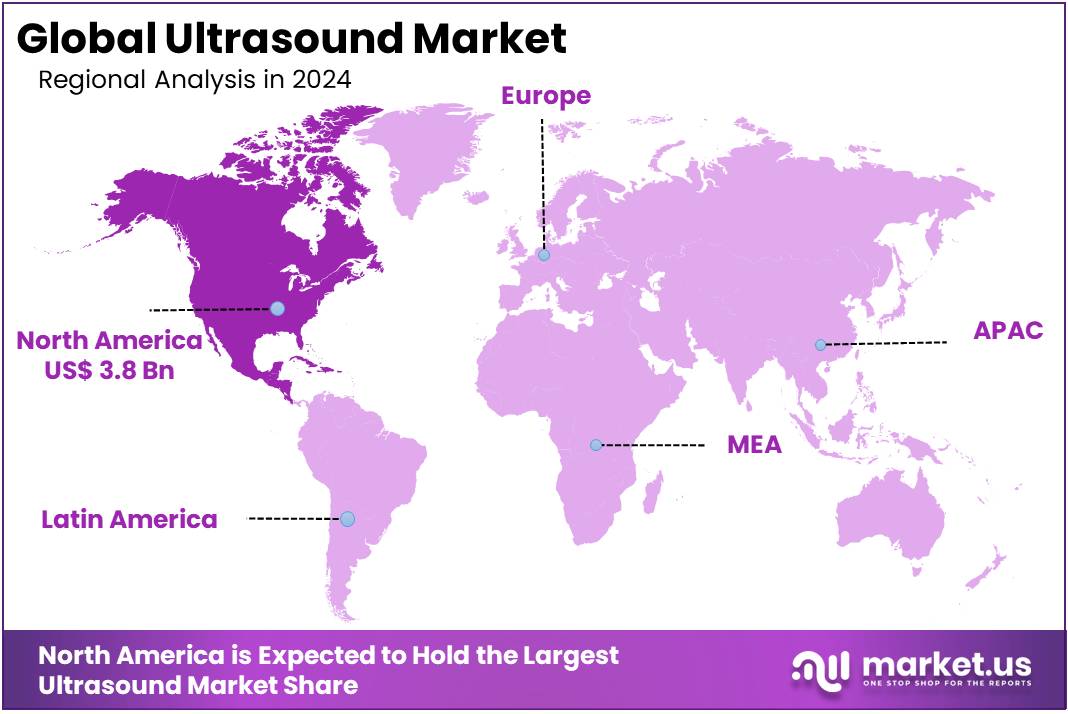

- North America led the market by securing a market share of 37.4% in 2024.

Product Type Analysis

The diagnostic ultrasound devices segment led in 2024, claiming a market share of 62.4% owing to the increasing demand for non-invasive imaging technologies that offer high accuracy and versatility. Diagnostic ultrasound devices, such as 2D, 3D/4D, and Doppler systems, are projected to see widespread adoption in both clinical and outpatient settings, driven by the need for improved diagnostic precision in various medical fields, including cardiology, obstetrics, and orthopedics.

The rising prevalence of chronic diseases, coupled with the growing preference for non-invasive diagnostic tools, is likely to drive the adoption of these ultrasound devices. Additionally, the advancements in ultrasound technology, such as improved imaging capabilities and portability, are expected to further boost the growth of this segment. As healthcare systems prioritize early disease detection and patient comfort, the demand for diagnostic ultrasound systems is projected to rise steadily.

Portability Analysis

The cart/trolley held a significant share of 50.8% due to the increasing demand for flexible, mobile imaging solutions in healthcare settings. Cart/trolley-based ultrasound systems are expected to see wide adoption in hospitals, outpatient clinics, and emergency care settings, as they provide a convenient means of transporting ultrasound equipment to various departments or patient rooms.

The growing preference for diagnostic tools that can be easily moved and accessed in multiple settings is likely to drive demand for ultrasound devices mounted on carts or trolleys. Additionally, the increasing need for rapid, on-site diagnostics in emergency care and intensive care units is expected to further fuel the growth of this segment. As hospitals and healthcare facilities prioritize accessibility and convenience, cart/trolley-based ultrasound systems are projected to see continued demand in the coming years.

Application Analysis

The radiology segment experienced significant growth, capturing a revenue share of 48.9%. This rise is due to the increasing adoption of ultrasound technology in radiology departments. The demand for high-resolution imaging solutions for detecting tumors, internal bleeding, and organ abnormalities is driving this trend. Healthcare providers prefer ultrasound because it offers quick diagnostic results. The shift toward non-invasive procedures and personalized medicine is further fueling market expansion. These factors make ultrasound a valuable tool for improving diagnostic accuracy and patient outcomes.

Ultrasound’s real-time imaging capabilities and ability to evaluate tissue and blood flow enhance its use in radiology. It provides cost-effective and efficient diagnostic solutions, making it a preferred choice for healthcare providers. As hospitals and clinics focus on accurate and non-invasive diagnostics, the ultrasound market is set for steady growth. Advancements in ultrasound technology, including improved image clarity and AI integration, will further boost adoption in radiology. The demand for efficient, safe, and precise imaging is expected to rise.

End-user Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 54.3% due to the increasing number of diagnostic procedures performed in these settings. Hospitals, as major healthcare providers, are expected to remain key users of ultrasound technology for a wide range of applications, including obstetrics, cardiology, and emergency care. The rise in chronic diseases, the growing demand for non-invasive diagnostic procedures, and the need for rapid, accurate imaging in hospitals are projected to drive the expansion of the ultrasound market in this segment.

Furthermore, hospitals’ ongoing investment in advanced imaging technologies and the increasing adoption of point-of-care ultrasound devices for quicker diagnoses are expected to boost demand. As hospitals strive to improve patient care and reduce healthcare costs, the ultrasound segment in this sector is projected to continue its growth trajectory.

Key Market Segments

By Product Type

- Diagnostic Ultrasound Devices

- 2D

- 3D/4D

- Doppler

- Therapeutic Ultrasound Devices

- High-intensity Focused Ultrasound

- Extracorporeal Shockwave Lithotripsy

By Portability

- Cart/Trolley

- Compact

- Handheld

By Application

- Cardiology

- Obstetrics/Gynecology

- Orthopedic

- Radiology

- Others

By End-user

- Hospitals

- Research Centers

- Imaging Centers

Drivers

Rising Prevalence of Chronic Diseases is Driving the Market

The rising prevalence of chronic diseases, including cardiovascular conditions and cancer, is driving the demand for ultrasound diagnostics. This technology provides a non-invasive, real-time imaging solution crucial for early detection and disease management. According to the World Health Organization (WHO), cardiovascular diseases are the leading global cause of death, responsible for approximately 17.9 million fatalities annually. Early diagnosis using imaging techniques like ultrasound helps in effective disease management. The ability to detect conditions at an early stage makes ultrasound an essential tool in modern healthcare.

Similarly, cancer remains a major global health challenge, causing around 10 million deaths in 2020, as reported by the WHO. Timely diagnosis is key to improving patient outcomes, and ultrasound plays a vital role in detecting tumors and monitoring disease progression. Its versatility and safety make it a preferred diagnostic tool for chronic diseases. The growing adoption of ultrasound technology in hospitals and diagnostic centers is significantly fueling market expansion worldwide.

Restraints

Economic Constraints in Healthcare Systems are Restraining the Market

Despite the benefits, economic challenges within healthcare systems, especially in developing regions, hinder the widespread adoption of advanced ultrasound equipment. The high initial investment and maintenance costs associated with state-of-the-art ultrasound devices can be prohibitive for facilities operating under tight budgets.

For example, a report by the World Bank highlights that healthcare expenditure in low-income countries remains significantly lower compared to high-income nations, limiting the capacity to acquire advanced medical technologies. Additionally, the allocation of limited resources often prioritizes immediate healthcare needs over the procurement of new diagnostic equipment. This financial strain restricts the expansion of ultrasound services, particularly in rural and underserved areas, thereby restraining market growth.

Opportunities

Technological Innovations are Creating Growth Opportunities

Advancements in ultrasound technology, such as the development of portable and handheld devices, are opening new avenues for market expansion. These innovations enhance accessibility and convenience, allowing healthcare providers to deliver diagnostic services in diverse settings, including remote and underserved areas.

For instance, the introduction of compact ultrasound devices has enabled point-of-care diagnostics, reducing the need for patients to travel to specialized facilities. This shift not only improves patient outcomes but also expands the market reach of ultrasound technology. Moreover, the integration of artificial intelligence into ultrasound systems enhances image analysis and diagnostic accuracy, further boosting their adoption across various medical disciplines. As these technological advancements continue to evolve, they present significant growth opportunities within the ultrasound market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a pivotal role in shaping the ultrasound market. Economic downturns can lead to reduced healthcare budgets, limiting investments in new medical technologies, including ultrasound equipment. For instance, the global economic impact of the COVID-19 pandemic strained healthcare resources, causing delays in equipment procurement and upgrades. Geopolitical tensions and trade disputes can disrupt supply chains, leading to shortages of critical components and increased manufacturing costs.

However, government initiatives aimed at strengthening healthcare infrastructure can mitigate these challenges. For example, stimulus packages and funding programs focused on healthcare improvements can facilitate the acquisition of advanced diagnostic tools. International collaborations and agreements also play a positive role, ensuring the steady supply of medical equipment across borders. Overall, while economic and political challenges exist, strategic policies and cooperative efforts can foster resilience and growth in the ultrasound market.

Trends

Integration of Artificial Intelligence is a Recent Trend

The incorporation of artificial intelligence (AI) into ultrasound systems represents a significant trend, enhancing diagnostic precision and workflow efficiency. AI algorithms can assist in real-time image interpretation, reducing variability and aiding in the early detection of abnormalities. For example, AI-enhanced ultrasound has shown promise in improving the accuracy of breast cancer detection, as noted by the US Food and Drug Administration (FDA). This technology aids radiologists by highlighting areas of concern, thereby expediting the diagnostic process.

Additionally, AI integration facilitates automated measurements and reporting, streamlining clinical workflows and reducing the burden on healthcare professionals. As AI technology continues to advance, its application within ultrasound diagnostics is expected to become more prevalent, setting new standards in medical imaging.

Regional Analysis

North America is leading the Ultrasound Market

North America dominated the market with the highest revenue share of 37.4% owing to several key factors. The increasing prevalence of chronic diseases, such as cardiovascular conditions, cancer, and musculoskeletal disorders, has heightened the demand for advanced diagnostic tools like ultrasound. According to the Centers for Disease Control and Prevention (CDC), heart disease remains the leading cause of death in the United States, underscoring the need for effective diagnostic imaging.

Technological advancements have led to the development of more sophisticated and user-friendly ultrasound devices, enhancing their adoption in both clinical and home settings. The rising preference for non-invasive diagnostic procedures has further boosted the market, as ultrasound offers a safer and more comfortable alternative to traditional imaging methods. Additionally, the presence of a well-established healthcare infrastructure and high healthcare spending in North America have facilitated the widespread availability and utilization of ultrasound devices. These factors collectively contributed to the robust growth of the ultrasound market in North America in 2023.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to several key factors. The region’s aging population is anticipated to increase the demand for healthcare services, including diagnostic imaging. For instance, the United Nations projects that by 2050, the number of older persons in Asia and the Pacific will reach 1.3 billion, up from 600 million in 2020.

Additionally, rising air pollution levels in countries like China and India are expected to contribute to respiratory issues, further driving the need for diagnostic imaging. Government initiatives aimed at improving healthcare access and combating chronic diseases are likely to support market growth. The increasing awareness of the importance of early diagnosis and preventive healthcare is expected to drive demand for ultrasound devices. These factors collectively contribute to the anticipated growth of the ultrasound market in Asia Pacific during the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the ultrasound market focus on advancing imaging technologies, such as 3D and 4D imaging, to improve diagnostic accuracy and patient outcomes. Companies invest in portable and handheld devices to enhance accessibility, especially in emergency and point-of-care settings. Strategic partnerships with hospitals and healthcare providers help expand market reach and promote the adoption of innovative systems. Many players emphasize artificial intelligence integration to improve image processing and automate routine tasks, increasing efficiency.

Geographic expansion into emerging markets with growing healthcare infrastructure supports further market growth. GE Healthcare is a leading company in this market, offering advanced ultrasound systems like the LOGIQ and Venue series for various clinical applications. The company focuses on innovation, integrating AI-driven diagnostics, and enhancing the portability of devices. GE Healthcare’s commitment to improving diagnostic imaging and global accessibility establishes it as a key player in the market.

Top Key Players in the Ultrasound Market

- Siemens Healthineers

- Mindray Medical International Limited

- Konica Minolta Inc

- GE Healthcare

- FUJIFILM SonoSite, Inc

- Esaote

- Canon Medical Systems

- Boston Imaging

Recent Developments

- In March 2023, Siemens Healthineers introduced the latest advancements in its Acuson Sequoia ultrasound series at the European Congress of Radiology in Vienna. The upgraded system incorporates cutting-edge imaging technology to improve diagnostic precision and workflow efficiency.

- In February 2023, Boston Imaging unveiled the Hera W10 Elite, a premium addition to its Hera platform designed for obstetrics and gynecology. Equipped with advanced AI-driven features, the system enhances diagnostic accuracy and streamlines clinical assessments for healthcare professionals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 10.2 billion |

| Forecast Revenue (2034) | US$ 15.4 billion |

| CAGR (2025-2034) | 4.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Diagnostic Ultrasound Devices (2D, 3D/4D, and Doppler), Therapeutic Ultrasound Devices (High-intensity Focused Ultrasound and Extracorporeal Shockwave Lithotripsy)), By Portability (Cart/Trolley, Compact, and Handheld), By Application (Cardiology, Obstetrics/Gynecology, Orthopedic, Radiology, and Others), By End-user (Hospitals, Research Centers, and Imaging Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens Healthineers, Mindray Medical International Limited, Konica Minolta Inc, GE Healthcare, FUJIFILM SonoSite, Inc, Esaote, Canon Medical Systems, and Boston Imaging. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |