Quick Navigation

Report Overview

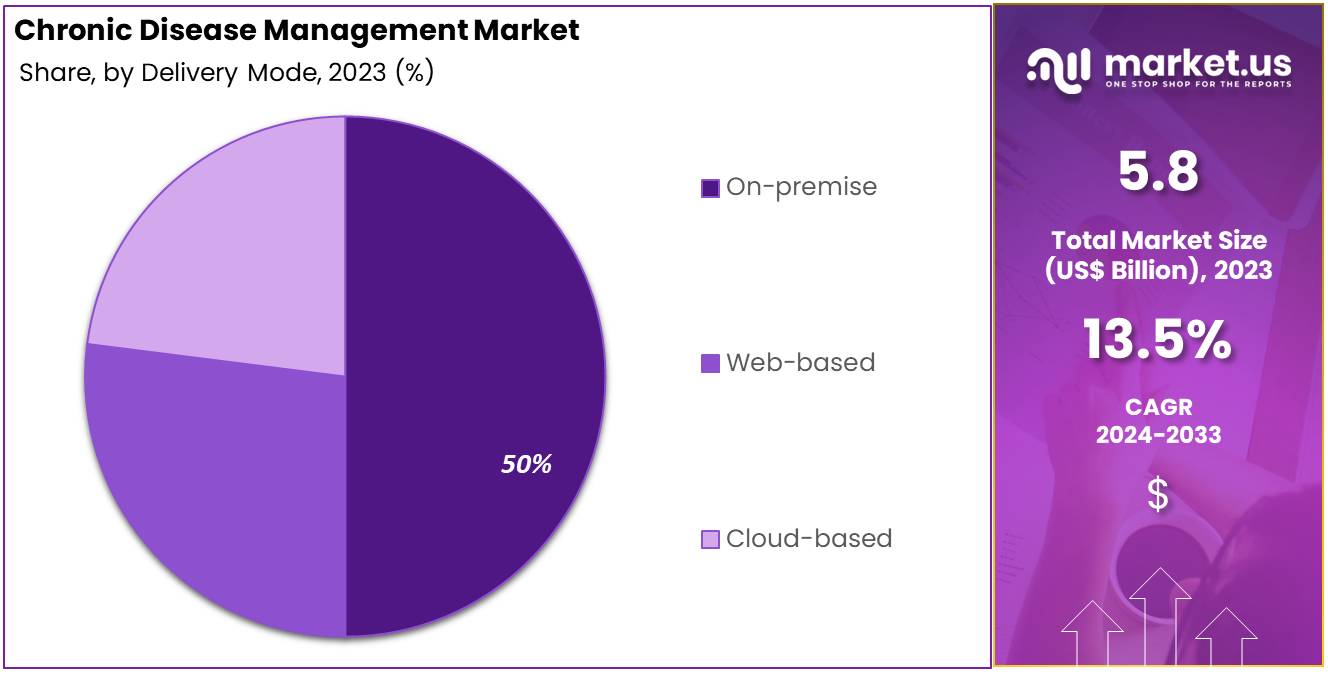

The Global Chronic Disease Management Market size is expected to be worth around US$ 20.6 Billion by 2033, from US$ 5.8 Billion in 2023, growing at a CAGR of 13.5% during the forecast period from 2024 to 2033.

The chronic disease management market is driven by the increasing global burden of chronic diseases such as diabetes, cardiovascular disorders, cancer, and respiratory illnesses. The rising ageing population, with its higher susceptibility to chronic conditions, further boosts market growth. Advancements in digital health technologies, including telemedicine, mobile health (mHealth) applications, and artificial intelligence (AI)-enabled solutions, are transforming chronic disease management by enabling remote monitoring and personalized care.

Governments and healthcare organizations are increasingly investing in preventive care and chronic disease programs, fostering innovation and adoption of management tools. However, the market faces challenges such as high implementation costs, particularly in low-income regions, and limited healthcare infrastructure. Data privacy concerns and the lack of interoperability between health systems also hinder widespread adoption.

Chronic diseases are a significant global health challenge, accounting for about 71% of all deaths worldwide, according to the World Health Organization (WHO). Each year, these non-communicable diseases (NCDs) are responsible for the deaths of approximately 41 million people. Alarmingly, 17 million of these deaths occur prematurely, affecting individuals under the age of 70.

A striking 77% of all NCD-related deaths occur in low- and middle-income countries. This disparity is even more pronounced for premature deaths, where 86% occur in these regions. Such statistics highlight the urgent need for targeted health interventions and support in these areas.

Among the various types of chronic diseases, cardiovascular diseases claim the most lives annually, with 17.9 million deaths. This is followed by cancers, which cause approximately 9.3 million deaths. Respiratory diseases and diabetes also contribute significantly to global mortality, with 4.1 million and 1.5 million deaths respectively. These figures underline the critical need for effective disease management and prevention strategies globally.

Key Takeaways

- The global chronic disease management market was valued at US$ 5.8 billion in 2023 and is anticipated to register substantial growth of US$ 20.6 billion by 2033, with a 13.5% CAGR.

- In 2023, the cardiovascular disease segment took the lead in the global market, securing 31% of the total revenue share.

- Among end-user segments, hospitals emerged as the dominant segment, capturing 46% of the total revenue.

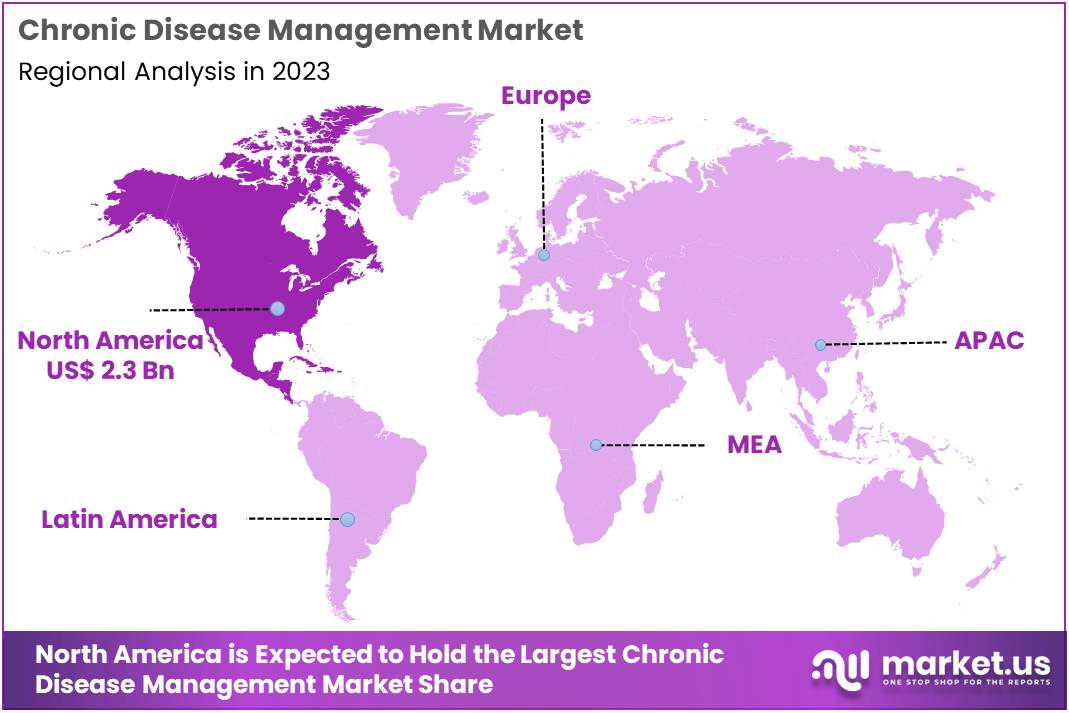

- North America maintained its leading position in the global market with a share of over 40% of the total revenue.

Disease Type Analysis

Based on disease type the market is fragmented into respiratory disease, cardiovascular disease, cancer, diabetes, and others. Amongst these, cardiovascular disease dominated the global chronic disease management market capturing a significant market share of 31% in 2023. Cardiovascular diseases (CVDs) dominated the global chronic disease management market due to their high prevalence and significant impact on public health.

CVDs, which include conditions like coronary artery disease, heart failure, and stroke, are responsible for the largest number of deaths worldwide. The rise in CVD cases is largely driven by aging populations, unhealthy lifestyles, and increasing rates of risk factors such as hypertension, diabetes, obesity, and high cholesterol. This growing burden has led to an increasing demand for effective management solutions, including early diagnosis, remote monitoring, and personalized treatment plans.

- For instance, the World Health Organization (WHO) estimated 9 million fatalities annually. This accounts for nearly 32% of all global deaths, making cardiovascular health a top priority in chronic disease management.

Service Type Analysis

The market is fragmented by service type into consulting services, implementation services, educational services, and others. Implementation services dominated the global chronic disease management market. The segment held a noteworthy market share of 40% in 2023. Implementation service dominated the global chronic disease management (CDM) market due to their crucial role in the effective integration and optimization of disease management programs.

These services encompass a range of activities, including system design, software installation, training, data migration, and ongoing technical support, all of which are essential for the successful adoption of CDM solutions. As healthcare organizations increasingly adopt digital health tools such as electronic health records (EHR), telemedicine platforms, and remote monitoring devices, the need for expert guidance in implementing these technologies becomes paramount.

In addition, effective implementation ensures that chronic disease management solutions are seamlessly integrated into existing healthcare systems, allowing for better data exchange, improved care coordination, and enhanced patient outcomes. The complexity of chronic diseases, which often require multi-faceted, long-term care, demands a well-structured implementation process that addresses various healthcare workflows.

Delivery Mode Analysis

Based on delivery mode the market is fragmented into on-premise, web-based, and cloud-based. Amongst these, on-premise dominated the global chronic disease management market capturing a significant market share of 50% in 2023. The on-premise segment dominated the global chronic disease management (CDM) market due to several key factors.

On-premise solutions refer to software and tools installed and operated locally on a healthcare provider’s infrastructure, offering greater control over data security and customization. Healthcare organizations prefer on-premise models for chronic disease management because they can integrate the solution more seamlessly with existing systems like electronic health records (EHR) and patient management platforms.

This integration is critical for tracking long-term patient data, managing multiple conditions, and ensuring continuous care for chronic disease patients. Furthermore, on-premise systems are perceived to provide more robust data privacy and security controls, which is a priority in healthcare settings where patient confidentiality is vital. The healthcare industry’s regulatory requirements, such as HIPAA in the U.S., also make on-premise solutions attractive, as they offer a higher level of compliance and governance.

End-user Analysis

Based on the end-user, the market fractionates into hospitals, speciality clinics, home care settings, and others. An indispensable role is performed by the hospitals segment apprehending a large market revenue share of 46% in the year 2023. The hospital segment has dominated the global chronic disease management (CDM) market due to the central role hospitals play in the diagnosis, treatment, and long-term care of chronic diseases.

Chronic conditions such as diabetes, heart disease, and respiratory disorders often require continuous monitoring and comprehensive care, which hospitals are uniquely equipped to provide. Hospitals have a multidisciplinary approach, involving specialized doctors, nurses, dietitians, and other healthcare professionals, which makes them ideal settings for managing complex chronic diseases.

Hospitals also have access to advanced diagnostic tools, technologies, and infrastructure needed to monitor patients’ conditions closely and intervene as necessary. With growing patient numbers, especially in ageing populations, hospitals are increasingly adopting CDM programs to manage chronic diseases effectively, reduce readmissions, and improve patient outcomes.

- In the United States, the Census Bureau provides comprehensive data on the ageing population. According to their 2020 Census report, individuals aged 65 and older accounted for 16.8% of the total U.S. population, and this proportion is projected to rise significantly in the coming decades.

Key Segments Analysis

By Services

- Cardiovascular Disease

- Respiratory Disease

- Cancer

- Diabetes

- Others

By Service Type

- Consulting Services

- Implementation Services

- Educational Services

- Other

By Delivery Mode

- On-premise

- Web-based

- Cloud-based

By End-user

- Hospitals

- Speciality Clinics

- Home Care Setting

- Others

Drivers

Increasing Patient with Chronic Disease

The growing global prevalence of chronic diseases has significantly increased the demand for Chronic Disease Management (CDM) services and solutions. According to the World Health Organization, chronic diseases account for 71% of all deaths worldwide, highlighting the urgent need for effective management strategies.

CDM plays a crucial role in improving medication adherence and overall patient care by offering personalized resources, educational materials, and support systems. This comprehensive approach helps individuals better understand their conditions, promoting improved self-management and better health outcomes. As chronic disease rates continue to rise, the demand for robust CDM solutions is expected to grow, driving market expansion and fostering innovation in healthcare delivery systems.

Restraints

Data Privacy and Security Concerns

Data privacy and security concerns present major challenges for the chronic disease management (CDM) market, especially with the increasing use of digital tools and telehealth platforms. As healthcare providers incorporate these technologies to improve patient care, the risk of data breaches and unauthorized access to sensitive patient information rises. For example, a 2021 survey reported that more than 45 million patient medical records were impacted by cyber threats, marking a significant increase compared to 2020.

Compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA) adds another layer of complexity, as healthcare organizations must enforce strict security measures to safeguard patient data. Non-compliance with these regulations can lead to hefty fines and legal consequences, which may discourage healthcare providers from fully adopting digital solutions for chronic disease management.

Opportunities

Increasing Healthcare Expenditure

Rising global healthcare expenditure presents a significant opportunity for the chronic disease management market, as both governments and private sectors increase funding to improve healthcare services and technologies. Higher healthcare spending typically leads to greater financial support for CDM solutions that improve the management of chronic diseases.

For example, the adoption of innovative telehealth platforms enables healthcare providers to remotely monitor patients, reducing hospital visits and improving access to care. As healthcare budgets continue to grow, investments in CDM technologies are expected to rise, creating a more dynamic market focused on improving patient outcomes and effectively managing chronic conditions.

- For instance, According to the World Bank, global health expenditure accounted for about 9.8% of the world’s GDP in 2020, reflecting a growing investment in health infrastructure and services.

Impact of macroeconomic factors / Geopolitical factors

Macroeconomic and geopolitical factors can significantly influence the chronic disease management (CDM) market. Economic conditions, such as inflation, recessions, or shifts in healthcare funding, affect government spending and private sector investments in healthcare services and technologies. Economic downturns may lead to budget cuts in healthcare, slowing the adoption of CDM solutions.

Conversely, periods of economic growth can increase investment in innovative healthcare technologies, including telehealth and digital health platforms. Geopolitical factors, such as international trade policies, conflicts, and global health crises, also impact the CDM market. For instance, disruptions in the global supply chain, exacerbated by geopolitical tensions, can delay the production and distribution of medical devices or software used in CDM.

Trends

The chronic disease management (CDM) market is seeing several transformative trends. Telehealth and remote monitoring are at the forefront, enabling real-time tracking of patient health through digital platforms, reducing hospital visits, and expanding access to care. Post-pandemic, virtual consultations have become mainstream, enhancing convenience and efficiency.

Personalized medicine is gaining traction, with CDM solutions increasingly focused on individualized treatment plans based on genetic, lifestyle, and environmental factors, leading to more targeted and effective care. Artificial intelligence (AI) and machine learning (ML) are playing a pivotal role by providing predictive analytics, early detection, and decision support, which optimize treatment and outcomes.

Additionally, wearable devices, such as fitness trackers and smart medical devices, are becoming integral, offering continuous monitoring of vital health metrics like glucose levels, heart rate, and blood pressure. These trends collectively reflect a shift towards more proactive, data-driven, and patient-centered approaches in managing chronic conditions.

Regional Analysis

North America held a large share of 40% of the global chronic disease management market driven by advanced healthcare infrastructure, high healthcare spending, and increasing prevalence of chronic diseases. The region, particularly the United States, has a well-established healthcare system that actively integrates digital health technologies such as telemedicine, remote monitoring, and wearable devices, making it a key adopter of CDM solutions.

The growing demand for innovative healthcare services, driven by an aging population and the rise of lifestyle-related diseases like diabetes, hypertension, and obesity, further fuels the market. Additionally, North American governments and private sector investments are pushing for more effective chronic disease management through funding and policy initiatives.

Strong regulatory frameworks, including the Health Insurance Portability and Accountability Act (HIPAA), ensure data security and encourage the adoption of digital health solutions. As a result, North America remains a dominant player in the global CDM market, both in terms of market size and innovation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The chronic disease management market is consolidated in nature with a strong presence of established players. In addition, key players in the market are leading innovation with technologies like telehealth services, wearable devices, and AI-driven predictive analytics, aimed at improving patient outcomes and optimizing care management.

Additionally, emerging players such as Omron Healthcare and Fitbit are gaining traction by providing consumer-oriented devices and apps that empower patients in self-management. The market is also witnessing partnerships and collaborations between healthcare providers, technology companies, and pharmaceutical firms, further expanding the reach of CDM solutions globally. This competitive landscape underscores the growing demand for comprehensive, patient-centric care models.

Top Key Players in the Chronic Disease Management Market

- Health Catalyst

- Cedar Gate Technologies

- Cognizant

- Epic Systems Corporation

- NXGN Management, LLC

- MINES & Associates, Inc.

- Zyter

- ExlServings Holdings, Inc.

- Veradigm LLC

- Infosys Limited

- Medecision

- IBM

- Health Plan Alliance

- TATA Consultancy Services Limited

Recent Developments

- In January 2024: Eli Lilly and Company rolled out LillyDirect™, a digital healthcare initiative in the U.S., aimed at aiding patients with obesity, migraine, and diabetes. The platform offers resources for disease management, including connections to independent healthcare providers, tailored support, and direct delivery of certain Lilly medications to patients’ homes via third-party pharmacy services.

- In May 2024: WELL Health Technologies Corp., along with its affiliate, HEALWELL AI, launched the second generation of WELL AI Decision Support. This updated tool enhances chronic disease screening capabilities, building on its predecessor’s focus on rare disease detection from six months earlier.

- In March 2023: Royal Philips introduced Philips Virtual Care Management. This service provides a broad array of solutions and services tailored to improve engagement and connectivity between health systems, providers, payers, employer groups, and patients, regardless of their geographical location.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 5.8 billion |

| Forecast Revenue (2033) | US$ 20.6 billion |

| CAGR (2024-2033) | 13.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Disease Type (Respiratory Disease, Cardiovascular Disease, Cancer, Diabetes, and Others), By Service Type (Consulting Services, Implementation Services, Educational Services, and Other), By Delivery Mode (On-premise, Web-based, and Cloud-based), By End User (Hospitals, Speciality Clinics, Home Care Setting, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Health Catalyst, Cedar Gate Technologies, Cognizant, Epic Systems Corporation, NXGN Management, LLC, MINES & Associates, Inc., Zyter, ExlServings Holdings, Inc., Veradigm LLC, Infosys Limited, Medecision, IBM, Health Plan Alliance, and TATA Consultancy Services Limited. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |