Quick Navigation

Report Overview

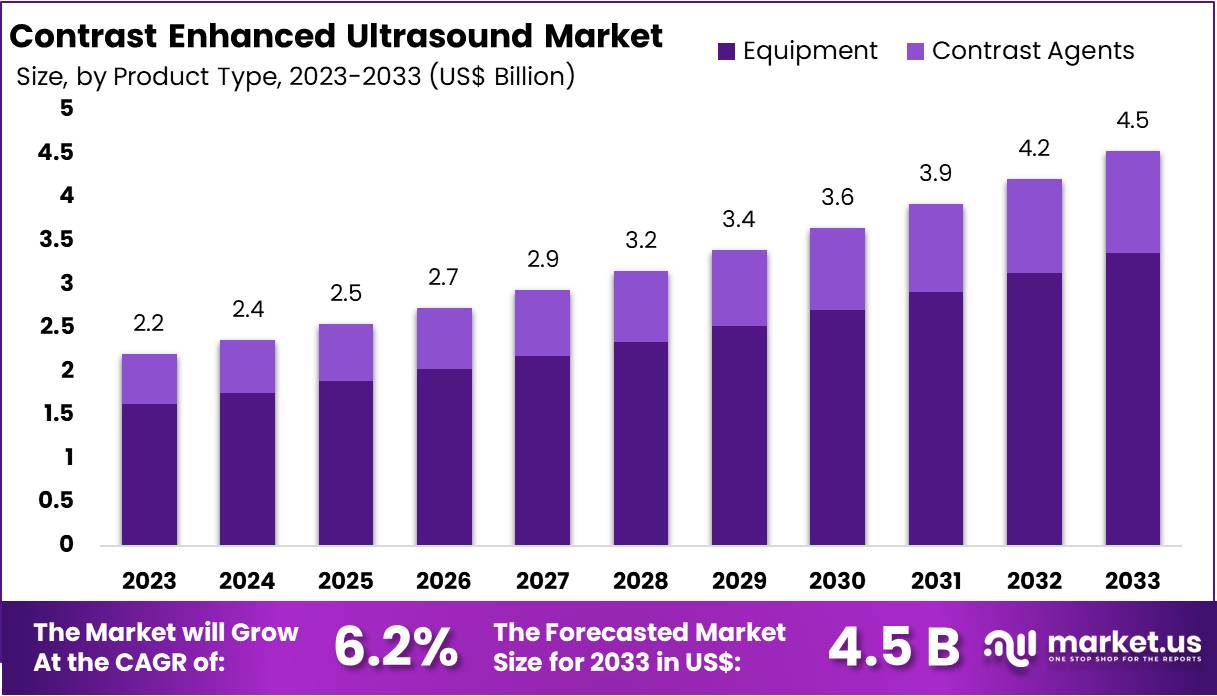

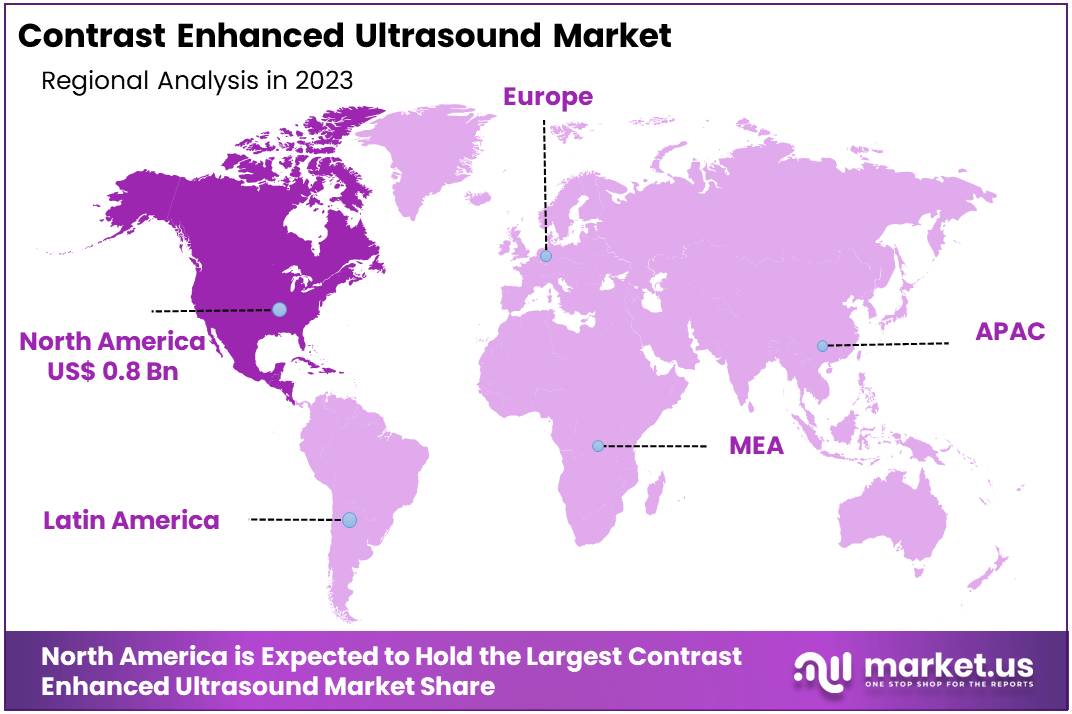

The Global Contrast Enhanced Ultrasound Market size is expected to be worth around US$ 4.5 Billion by 2033, from US$ 2.2 Billion in 2023, growing at a CAGR of 6.2% during the forecast period from 2024 to 2033. North America dominated the market with a 35.2% share. The region’s market value reached US$ 0.8 billion during the year.

Contrast-Enhanced Ultrasound (CEUS) is an advanced imaging technique enhancing traditional ultrasound with gas-filled microbubbles as contrast agents. These microbubbles improve ultrasound wave reflection, offering clearer images of blood flow and tissue vascularity.

CEUS is particularly effective in assessing organ perfusion and characterizing lesions in the liver, kidneys, and heart. For example, a Study by NLM found CEUS to be highly sensitive for detecting hepatobiliary lesions, with a sensitivity of 100.0%, specificity of 96.8%, and accuracy of 96.7% when correlated with pathological findings.

CEUS offers real-time blood flow evaluation without ionizing radiation, making it cost-effective and safer than other imaging techniques. Its applications are diverse. For instance, liver contrast ultrasound identifies tumors and evaluates cirrhosis, while cardiac CEUS assesses myocardial perfusion.

Additionally, CEUS is instrumental in vascular imaging, detecting blockages, and monitoring therapy effectiveness. According to the Mayo Clinic Proceedings, CEUS is pivotal in post-surgical monitoring, where 14.4% of surgical patients experience adverse events, such as prolonged hospital stays or disability. These advantages drive its adoption in clinical practices globally.

While CEUS excels in safety and cost, other imaging techniques also dominate interventional radiology. According to Health Imaging, 74 million CT procedures were performed in the U.S. in 2016, accounting for 18% of global usage. Additionally, 8.1 million interventional radiologic procedures were recorded in the same year, representing 34% globally. Nuclear medicine techniques, including PET and SPECT, are valuable in oncology. In 2016, 13.5 million nuclear medicine procedures were conducted in the U.S., also 34% globally. Despite these numbers, CEUS remains the preferred choice in scenarios prioritizing real-time evaluation and safety.

Postoperative complications occur in 17% of elective surgeries and increase to 27% for major surgeries, as reported by Anesthesiology. CEUS plays a crucial role in early detection of complications and ensuring proper healing. Emerging technologies like remote patient monitoring (RPM) complement CEUS. For example, a JAMA Network study revealed that RPM reduces unnecessary emergency visits by 22%. These tools collectively enhance post-surgical care and outcomes.

CEUS’s versatility extends to guiding interventional procedures like biopsies and monitoring chronic conditions like cirrhosis. For instance, CEUS aids in pediatric imaging by providing radiation-free diagnostic solutions for children with vascular issues.

Additionally, its use in fetal and placental assessment ensures safer pregnancies. Researchers are also exploring CEUS for drug delivery. Health Imaging highlights its ability to study organ perfusion and vascular changes, making it invaluable for conditions requiring precise blood flow visualization.

CEUS stands out as a versatile and essential imaging modality. Its ability to provide detailed, real-time images without radiation ensures patient safety while reducing healthcare costs. Although other techniques like CT and PET dominate in procedural numbers, CEUS remains invaluable for applications demanding precision and safety.

According to various studies, its integration with remote technologies like RPM enhances healthcare outcomes, particularly in postoperative and chronic disease management. CEUS’s widespread adoption across medical fields highlights its growing importance in modern diagnostics.

Key Takeaways

- The global Contrast Enhanced Ultrasound Market is projected to grow from US$ 2.2 billion in 2023 to US$ 4.5 billion by 2033.

- North America dominated the market with a 35.2% share in 2023, reaching a value of US$ 0.8 billion, driven by advanced healthcare infrastructure.

- The Equipment segment accounted for 74.2% of the market share in 2023, propelled by innovations improving imaging precision and diagnostic efficiency.

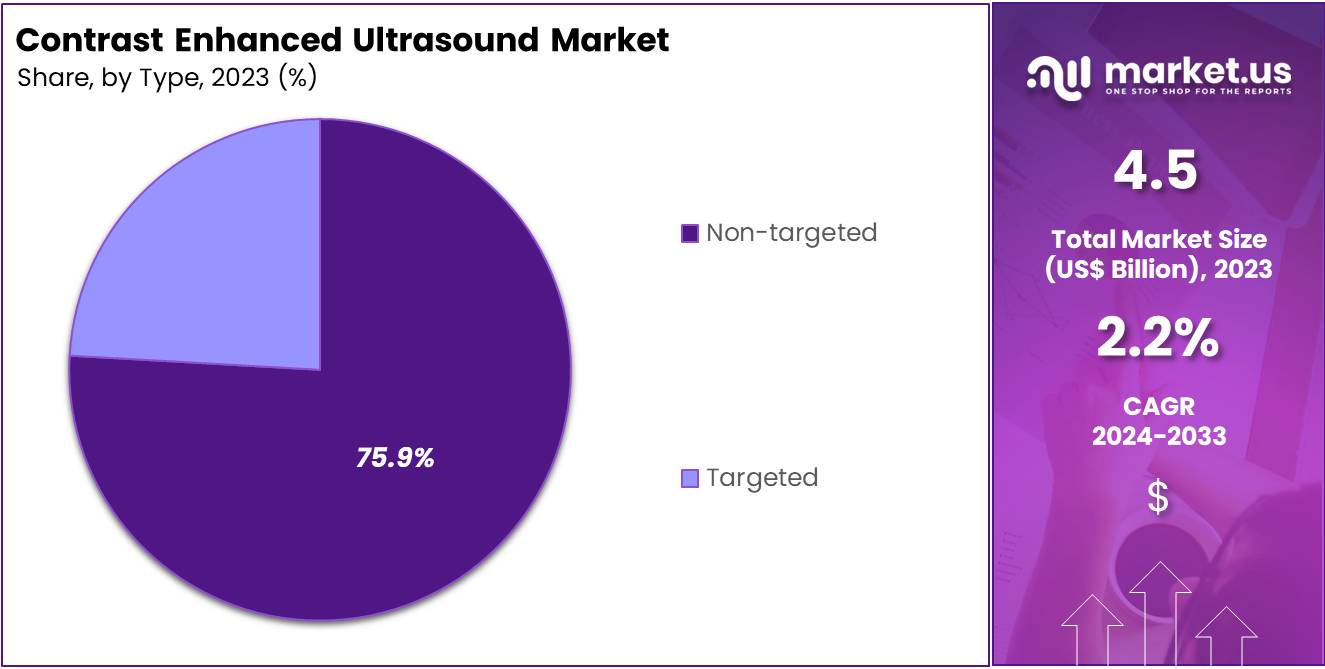

- Non-targeted contrast agents held 75.9% of the type segment share in 2023, favored for enhancing blood flow visibility in cardiology, oncology, and radiology.

- Hospitals dominated the end-use segment with a 75.9% market share in 2023, driven by their capacity to manage high patient volumes and advanced diagnostics.

- The growing adoption of non-invasive diagnostic tools supports the increasing use of contrast-enhanced ultrasound in ambulatory diagnostic centers and outpatient care.

- Lantheus’ DEFINITY gained FDA approval in March 2024 for pediatric echocardiograms, addressing critical diagnostic needs in children with 189 trial participants.

- Philips launched a super-resolution CEUS application in September 2023, achieving 200% better spatial resolution for enhanced cancer diagnostics.

- Bracco Diagnostics’ POSLUMA® injection achieved FDA approval in May 2023, with an 83% detection rate for prostate cancer lesions, enhancing clinical outcomes.

- The prevalence of chronic diseases like cardiovascular conditions and cancer is a key driver, boosting demand for real-time imaging solutions globally.

Product Type Analysis

In 2023, the Equipment segment held a dominant market position in the Product Type Segment of the Contrast Enhanced Ultrasound Market, capturing more than a 74.2% share. This substantial share underscores the segment’s critical role in the industry. The demand for advanced diagnostic tools is driven by the need for accuracy in medical imaging.

Technological advancements significantly contribute to this segment’s growth. Innovations in ultrasound equipment enhance imaging quality, facilitating better diagnosis and patient outcomes. These improvements are pivotal in settings that require high precision, such as hospitals and diagnostic centers.

The contrast agents segment, although smaller, is integral to the market. These agents help improve the visibility of internal organs and blood vessels during ultrasound examinations. They are particularly vital in procedures that assess vascular health and organ function.

Together, equipment and contrast agents form the backbone of the contrast-enhanced ultrasound market. Their combined utility is expanding the capabilities of ultrasound technology, meeting the growing demands for non-invasive and accurate diagnostic methods.

Type Analysis

In 2023, the Non-targeted segment held a dominant market position in the Type Segment of the Contrast Enhanced Ultrasound Market, capturing more than a 75.9% share. This segment primarily includes ultrasound contrast agents that distribute throughout the body without binding to specific molecular targets. These agents are favored for their ability to enhance the visibility of blood flow and the microvascular structure in real-time imaging. The significant share of this segment is driven by its broad application across various medical fields, including cardiology, radiology, and oncology.

Non-targeted contrast agents are preferred for their rapid diagnostic ability and effectiveness in routine clinical use. They provide essential enhancements in imaging that assist clinicians in making more accurate assessments of vascular diseases, tumors, and organ functions. Their widespread use is supported by advantages such as safety, cost-effectiveness, and the capability to provide real-time diagnostic results. These factors contribute to the high adoption rate of non-targeted contrast agents in the medical imaging field.

The segment’s dominance is also supported by ongoing advancements in ultrasound technology, which improve the efficacy and diagnostic capabilities of non-targeted contrast-enhanced ultrasound. As ultrasound techniques become more sophisticated, the role of non-targeted agents is expected to expand, potentially leading to further growth in their market share. Future developments are likely to focus on enhancing image quality and diagnostic accuracy, reinforcing the foundational role of non-targeted contrast agents in contrast-enhanced ultrasound procedures.

End-use Analysis

In 2023, the hospital segment held a dominant market position in the end-use segment of the Contrast Enhanced Ultrasound Market, capturing more than a 75.9% share. This significant market share is attributed to the extensive use of contrast-enhanced ultrasound techniques in hospitals for a variety of diagnostic procedures.

Hospitals often have the infrastructure and financial capacity to invest in advanced imaging technologies. This includes contrast agents and ultrasound machines that provide better visualization of vascular structures and organs.

Clinics, as a secondary segment, also utilize contrast-enhanced ultrasound but to a lesser extent compared to hospitals. The integration of these devices in clinics is driven by the need for precise diagnostic tools that support quick decision-making in medical care. However, the adoption rate in clinics is tempered by budget constraints and the smaller scale of operations.

Ambulatory diagnostic centers are emerging as a vital end-use segment. These centers cater to outpatient care, offering diagnostic services that require minimal to no recovery time. The use of contrast-enhanced ultrasound in these centers is increasing due to its safety profile, with fewer side effects and no ionizing radiation involved. This trend is expected to grow as patient preference shifts towards non-invasive procedures and rapid diagnostics.

Each of these segments contributes uniquely to the growth and evolution of the Contrast Enhanced Ultrasound Market. Hospitals remain at the forefront, largely due to their capacity to handle high patient volumes and complex cases. Meanwhile, clinics and ambulatory centers are adapting rapidly, focusing on specialized, patient-friendly approaches.

Key Market Segments

Product Type

- Equipment

- Contrast Agents

Type

- Non-targeted

- Targeted

End-use

- Hospitals

- Clinics

- Ambulatory Diagnostic Centers

Drivers

Technological Advancements in Ultrasound Systems

Advancements in ultrasound technology have significantly enhanced diagnostic precision. Modern systems, such as GE Healthcare’s LOGIQ E9, offer up to 99% improved spatial resolution and 22% more contrast, enabling clearer imaging of tissues and organs. These improvements assist healthcare professionals in detecting subtle abnormalities, leading to more accurate diagnoses and increased confidence in clinical evaluations.

The integration of artificial intelligence (AI) into ultrasound systems has further elevated their functionality. AI-driven enhancements have streamlined user interfaces, making them up to 80% more user-friendly. This ease of use allows clinicians to perform complex procedures more efficiently, reducing examination times and improving patient throughput. Additionally, AI algorithms aid in interpreting ultrasound data, minimizing human error and enhancing diagnostic reliability.

These technological advancements have contributed to the growing adoption of contrast-enhanced ultrasound (CEUS) procedures. Enhanced imaging capabilities and higher sensitivity make CEUS a more viable option for various diagnostic applications.

The global ultrasound systems market reflects this trend, with 2D ultrasound systems accounting for over 67% of the market share in 2020. As technology continues to evolve, the utilization of CEUS is expected to expand, offering safer and more effective diagnostic alternatives.

Restraints

High Cost of Devices and Procedures

The high costs associated with Contrast-Enhanced Ultrasound (CEUS) equipment and procedures present a significant barrier to their widespread adoption, especially in developing regions. This financial obstacle can deter healthcare facilities from investing in advanced imaging technologies. As a result, the accessibility of CEUS remains limited, impacting the overall growth of the market in these areas.

In regions where economic constraints are pronounced, the adoption of CEUS technology is notably slower. The expenses linked to acquiring the necessary equipment and the cost of conducting procedures make it a less viable option for many healthcare providers. This limitation not only affects the expansion of CEUS usage but also restricts the benefits it offers to a broader patient base.

Market growth for CEUS is consequently restrained by these high costs, which hinder the technology’s penetration into less affluent markets. Without adequate financial resources or support mechanisms, such as government funding or subsidies, the adoption of CEUS remains out of reach for many. Addressing these financial barriers is crucial for enhancing the global accessibility and utilization of CEUS technology.

Opportunities

Emerging Markets

Emerging markets in regions such as Asia-Pacific and Latin America hold immense growth potential for contrast-enhanced ultrasound technologies. These areas are experiencing rapid improvements in healthcare infrastructure. Governments and private sectors are investing more in healthcare systems. This has led to better access to advanced medical tools.

Additionally, rising awareness about the importance of early diagnosis is encouraging healthcare providers to adopt innovative imaging solutions. Contrast-enhanced ultrasound is increasingly recognized as a cost-effective and non-invasive diagnostic tool in these regions.

Healthcare spending in emerging economies is steadily increasing. This trend is driven by rising disposable incomes and a focus on improving public health outcomes. As a result, medical institutions are adopting advanced technologies like contrast-enhanced ultrasound.

The affordability and safety of this diagnostic tool make it a preferred choice. Its ability to provide accurate results without radiation exposure further supports its demand. These factors collectively create a promising environment for market growth in developing countries.

Growing awareness campaigns about advanced diagnostic techniques play a vital role in boosting the adoption of contrast-enhanced ultrasound. Both government initiatives and healthcare organizations are educating professionals and patients about its benefits.

The technique’s versatility across various medical fields adds to its appeal. Emerging markets are showing a shift towards more reliable diagnostic approaches. This shift highlights a significant opportunity for manufacturers and service providers to expand their presence in these regions. The potential for growth remains strong as demand continues to rise.

Trends

Technological Advancements

Technological advancements are driving improvements in ultrasound imaging. New developments include the integration of artificial intelligence (AI) and machine learning. These technologies enhance image processing and analysis, making ultrasound systems more efficient and accurate.

The focus on precision and speed in diagnostics has positioned AI as a valuable tool for clinicians. These innovations are transforming traditional ultrasound methods, enabling faster and more reliable results. Such advancements are creating new opportunities for improved diagnostic accuracy across a wide range of medical applications.

The use of AI and machine learning in contrast-enhanced ultrasound imaging is boosting diagnostic confidence. These technologies help provide clearer and more detailed imaging, aiding healthcare professionals in better decision-making. Improved image analysis ensures early and accurate detection of various medical conditions.

Additionally, the enhanced capabilities of contrast-enhanced ultrasound are positively impacting patient outcomes. With such advancements, the market for this technology is experiencing rapid growth, driven by its potential to revolutionize diagnostic imaging in healthcare.

Regional Analysis

In 2023, North America held a dominant market position in the Contrast Enhanced Ultrasound Market, capturing more than a 35.2% share with a market value of US$ 0.8 billion for the year. This leadership stems from a sophisticated healthcare infrastructure that integrates advanced imaging technologies into routine diagnostics.

The high incidence of chronic diseases like cardiovascular conditions and cancer also drives demand for these diagnostic solutions. Enhanced imaging is crucial for accurate diagnosis and monitoring, propelling the market forward.

Significant investments in research and development further solidify North America’s market dominance. Both public and private sectors contribute to technological advancements, improving patient outcomes and healthcare efficiency.

Additionally, the region benefits from a streamlined regulatory environment. Agencies like the FDA expedite the approval of innovative medical devices, including new contrast agents and ultrasound technologies. This regulatory support accelerates the introduction and adoption of advanced diagnostic methods.

Awareness and education about the benefits of early diagnosis through non-invasive methods are widespread among healthcare professionals and patients alike. Educational initiatives by health organizations promote the use of advanced imaging techniques such as contrast-enhanced ultrasound.

Moreover, North America’s strong economic standing supports substantial healthcare spending per capita. This financial capability enables the widespread adoption of costly but effective diagnostic techniques, maintaining the region’s leading position in the market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Contrast Enhanced Ultrasound Market is witnessing dynamic changes with key players such as Lantheus Medical Imaging, Inc. leading the way. Lantheus is noted for its pioneering diagnostic products that improve ultrasound accuracy.

The company’s financial growth is driven by strong sales in this segment. Lantheus’s portfolio features ultrasound contrast agents and equipment. Their primary strengths are robust R&D and a diverse product range, though they mainly depend on the U.S. market, posing a potential limitation.

GE Healthcare stands out as another major contributor in the market, providing a wide array of imaging solutions including advanced ultrasound technologies. The firm’s revenue benefits significantly from continuous innovation and its established global presence. Their ultrasound technology integrates cutting-edge digital enhancements like AI to boost diagnostic precision and operational efficiency. This strategy supports GE’s strong market positioning despite economic uncertainties.

Bracco Diagnostic specializes in contrast media essential for enhancing diagnostic imaging quality. The company enjoys a solid market position in Europe and North America. Bracco’s strategy focuses on improving product effectiveness and adhering to strict healthcare regulations, aiming to capitalize on opportunities in Asian markets. However, dependency on traditional markets and regulatory changes remain challenging factors.

Siemens Healthcare GmbH and other key players also significantly impact the market with high-end technology solutions and innovative products. Siemens is known for its sophisticated imaging technologies, which are supported by strong financial health and continuous market expansion efforts. Smaller companies in this sector push for market relevance through niche offerings and competitive strategies, collectively influencing market trends and encouraging larger entities to innovate continuously.

Market Key Players

- Lantheus Medical Imaging, Inc.

- GE Healthcare

- Bracco Diagnostic

- GE HealthCare

- Siemens Healthcare GmbH

- Koninklijke Philips N.V.

- CANON MEDICAL SYSTEMS CORPORATION

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Other Key Players

Recent Developments

- March 2024: The FDA approved a new application for Lantheus’ DEFINITY (Perflutren Lipid Microsphere), now authorized for pediatric use in echocardiograms where standard results are suboptimal. This decision followed the positive outcomes from three pediatric trials involving 189 participants, which confirmed DEFINITY’s safety and effectiveness in enhancing diagnostic clarity in pediatric cardiology. This approval marks a significant advancement in addressing the critical diagnostic needs of younger patients.

- September 2023: Philips launched a new super-resolution contrast-enhanced ultrasound (CEUS) application for its EPIQ Elite ultrasound system. This cutting-edge technology, designed primarily for cancer diagnostics, offers a spatial resolution up to 200% better than previous models. It employs micro-bubble contrast media that are exhaled through the lungs, thereby minimizing adverse effects and enhancing diagnostic accuracy without relying on ionizing radiation.

- May 2023: Bracco Diagnostics, through its subsidiary Blue Earth Diagnostics, gained FDA approval for POSLUMA® (flotufolastat F 18) injection. This innovative PET imaging agent is targeted at detecting prostate-specific membrane antigen (PSMA) positive lesions in men. With an impressive 83% detection rate, POSLUMA® is set to significantly impact the management of suspected biochemical recurrence of prostate cancer.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 2.2 Billion |

| Forecast Revenue (2033) | US$ 4.5 Billion |

| CAGR (2024-2033) | 6.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Equipment, Contrast Agents), By Type (Non-targeted, Targeted), By End-use (Hospitals, Clinics, Ambulatory Diagnostic Centers) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Lantheus Medical Imaging, Inc., GE Healthcare, Bracco Diagnostic, GE HealthCare, Siemens Healthcare GmbH, Koninklijke Philips N.V., CANON MEDICAL SYSTEMS CORPORATION, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |