Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Soy Sauce Market

- By Type Analysis

- By Process Analysis

- By Packaging Analysis

- By End-User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Top Key Players in the Market

- Recent Developments

- Report Scope

Report Overview

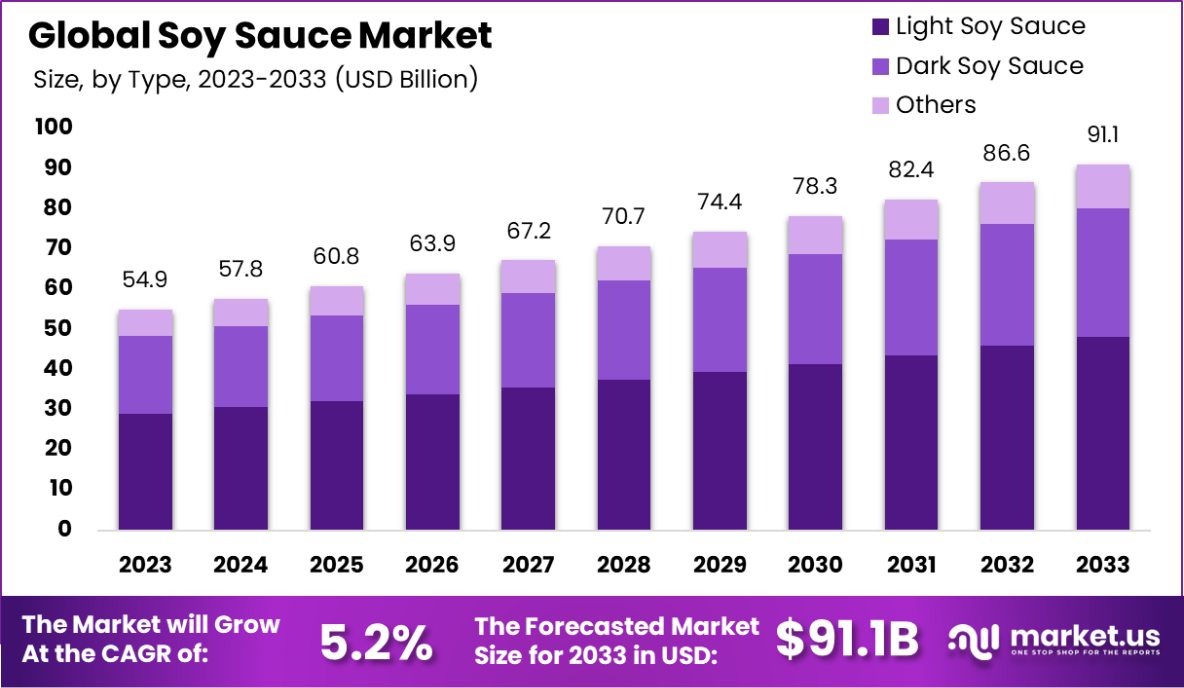

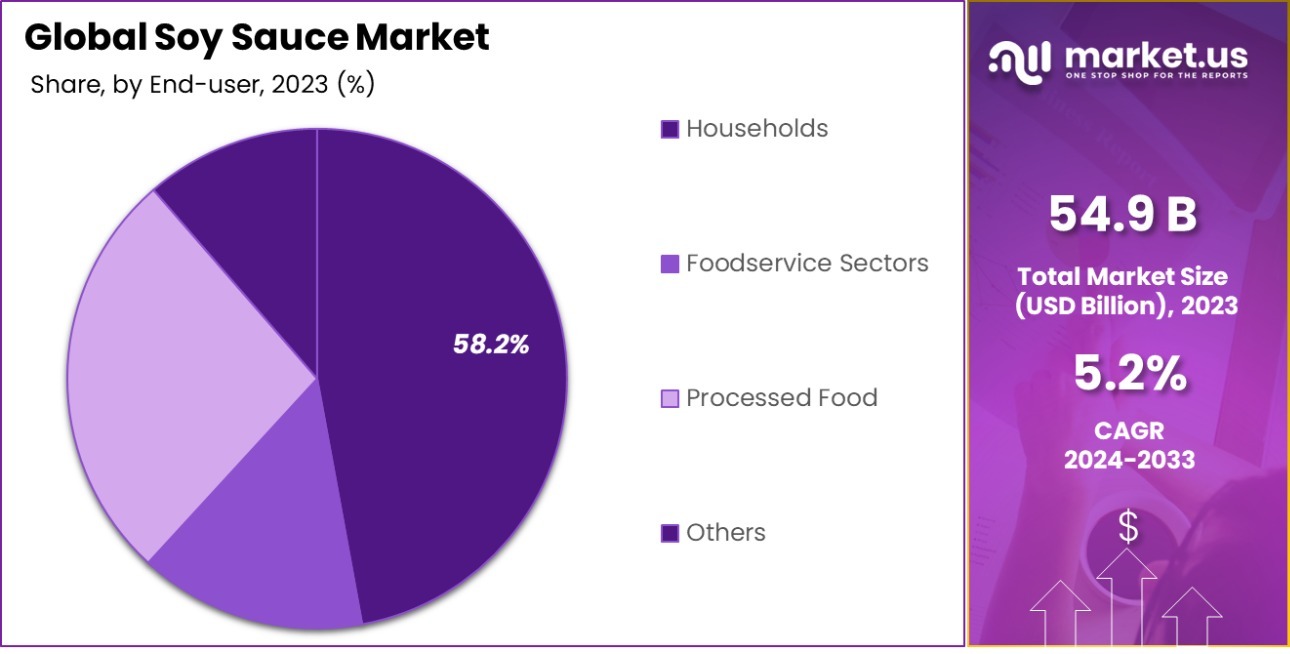

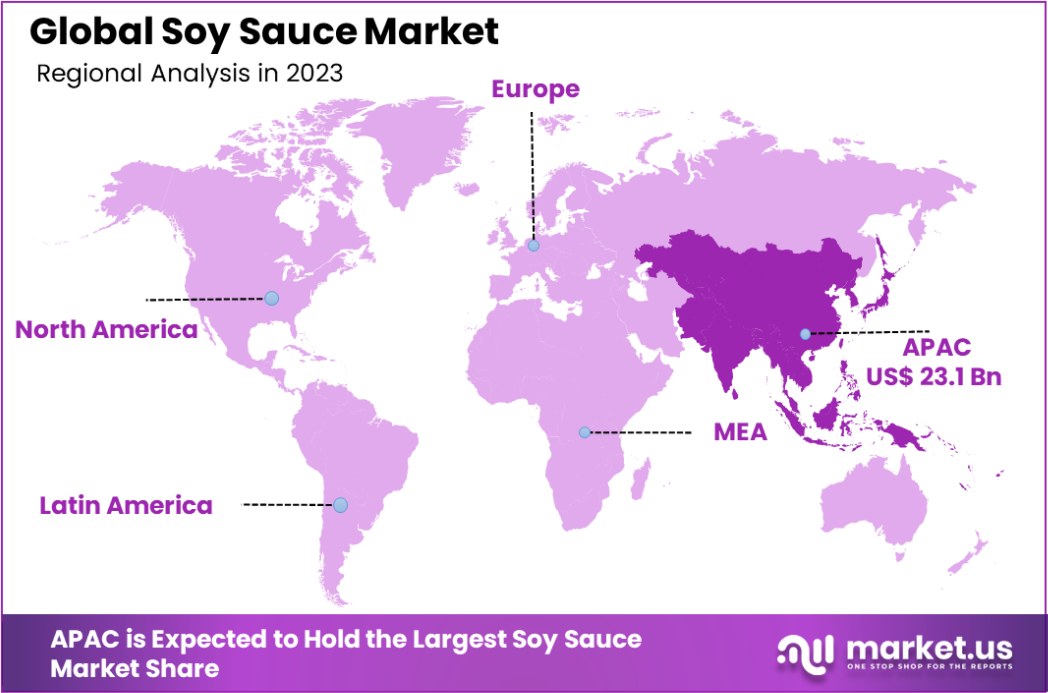

The Global Soy Sauce Market is expected to be worth around USD 91.1 Billion by 2033, up from USD 54.9 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033. Asia-Pacific holds 51.2%, valuing the soy sauce market at USD 23.1 billion.

Soy sauce, a traditional condiment integral to Asian cuisine, is produced through the fermentation or chemical hydrolysis of soybeans and wheat. The U.S. Department of Agriculture (USDA) classifies soy sauce into four types: Type I (Fermented), Type II (Non-fermented), Type III (Non-fermented, Light in sodium), and Type IV (Fermented, Reduced sodium).

The global demand for soy sauce has been influenced by various factors, including consumer preferences and regulatory standards. In the United States, the Food and Drug Administration (FDA) has established guidance levels for contaminants such as 3-chloro-1,2-propanediol (3-MCPD) in soy sauce, setting a threshold of 1 part per million (ppm) to ensure consumer safety.

This regulatory framework has prompted manufacturers to adopt improved production methods to minimize contaminant levels, thereby enhancing product quality and safety. Market trends indicate a growing consumer inclination towards low-sodium and gluten-free soy sauce variants, driven by increased health consciousness.

The FDA provides guidance on gluten-free labeling, allowing soy sauce made with wheat to be labeled as gluten-free if the gluten has been adequately removed and the product meets the established criteria. This has led to product innovation and diversification within the industry, catering to specific dietary needs and expanding consumer bases.

The U.S. soy sauce market is also influenced by international trade dynamics. For instance, the USDA reports that U.S. exports of condiments and sauces, including soy sauce, reached $2.27 billion in 2023, with key markets being Canada, Mexico, and the European Union. This underscores the significance of soy sauce within the broader category of condiment exports and highlights its role in the global food industry.

Looking ahead, the soy sauce market is poised for growth, supported by increasing consumer demand for diverse and health-oriented food products. Manufacturers are expected to continue innovating to meet regulatory standards and consumer preferences, particularly in developing low-sodium and allergen-free options.

The Soy Sauce Market is experiencing notable changes driven by various economic and regulatory interventions in key producing regions. The financial year-wise allocation under India’s Price Stabilization Fund (PSF) showcases a significant shift in government priorities and economic strategy.

For the fiscal year 2024-25, the allocation is set at ₹10,000 crore, as opposed to no allocation in the previous year, 2023-24, and a minimal ₹0.01 crore in 2022-23. This substantial increase indicates a strong governmental focus on stabilizing commodity prices and supporting agricultural sectors critical to the economy.

Furthermore, the government’s proactive approach is underscored by its recent approval for the procurement of 1.56 million metric tons of soybeans under the Price Support Scheme (PSS) across key agricultural states such as Maharashtra, Karnataka, Telangana, and Madhya Pradesh.

This initiative aims to stabilize soybean prices and provide necessary support to farmers amidst fluctuating market conditions. Such strategic interventions not only help in stabilizing the soy sauce market by ensuring a steady supply of raw materials but also bolster the broader agricultural framework that sustains this industry.

Key Takeaways

- The Global Soy Sauce Market is expected to be worth around USD 91.1 Billion by 2033, up from USD 54.9 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033.

- Light soy sauce dominates with a market share of 53.4%, reflecting consumer preference worldwide.

- Brewed soy sauce, accounting for 64.3%, highlights the increasing demand for naturally fermented, authentic flavor options.

- Glass jars hold a 39.2% share, driven by their premium appeal and long-term preservation benefits.

- Households dominate at 58.2%, as soy sauce remains a staple ingredient for home-cooked meals.

- Supermarkets and hypermarkets lead at 46.2%, offering convenience and diverse soy sauce options to consumers.

- The Asia-Pacific region dominates the Soy Sauce Market with 51.2%, valued at USD 23.1 billion.

Business Benefits of Soy Sauce Market

The soy sauce market offers significant business benefits, particularly in India, where soybean cultivation is substantial. Soy sauce, a fermented condiment derived from soybeans, is integral to various cuisines and is gaining popularity due to its distinctive flavor and potential health advantages.

One of the primary benefits is the opportunity for product diversification. Manufacturers can develop multiple soy-based products, including soy sauce, to cater to diverse consumer preferences. This diversification can enhance market reach and profitability.

The increasing health consciousness among consumers has led to a rise in demand for soy products. Soy sauce, being low in calories and containing beneficial compounds, appeals to health-conscious individuals. This shift in consumer behavior presents a lucrative opportunity for businesses to expand their product lines to include soy-based offerings.

Furthermore, the Indian government’s support for soybean processing and utilization encourages entrepreneurship in this sector. Initiatives aimed at promoting soy-based food products can lead to increased production and consumption, thereby boosting the soy sauce market.

By Type Analysis

Light soy sauce dominates with a substantial 53.4% market share.

In 2023, Light Soy Sauce held a dominant market position in the “By Type” segment of the Soy Sauce Market, with a 49.2% share. Its lighter color, subtle flavor, and thinner consistency make it preferred for marinating and as a dipping sauce, which significantly contributed to its leading status.

On the other hand, Dark Soy Sauce captured a substantial portion of the market as well. Known for its thicker consistency, darker color, and richer flavor due to a longer aging process, it is essential in cooking, adding both color and depth to dishes.

These two types cater to distinct culinary needs: Light Soy Sauce is primarily used to enhance flavors without overwhelming dishes, making it ideal for seafood and poultry, while Dark Soy Sauce is favored in hearty meals like stews and red meat dishes.

This segmentation addresses diverse consumer preferences and cooking styles, reflecting cultural and regional culinary traditions. The distinct market positions of Light and Dark Soy Sauce underscore the versatility of soy sauce as a staple in various recipes and its integral role in global cuisine trends.

By Process Analysis

Naturally fermented brewed soy sauce accounts for 64.3% of preference globally.

In 2023, Brewed (Naturally Fermented) held a dominant market position in the “By Process” segment of the Soy Sauce Market, with a 49.2% share. This traditional brewing process, involving natural fermentation, appeals to consumers seeking authentic flavors and artisanal food products.

Brewed soy sauce is characterized by a complex flavor profile and a longer fermentation period, which enhances its taste and quality. This method typically attracts a premium price point, reflecting its superior flavor and alignment with health-conscious and gourmet food trends.

Conversely, Blended soy sauce, which combines chemical hydrolysis and some degree of natural fermentation, accounted for a significant share of the market as well. This type of soy sauce is favored for its consistency in flavor and color, quicker production times, and lower cost. It caters to price-sensitive markets and is commonly used in food service industries where cost efficiency is crucial.

The contrasting consumer preferences for Brewed and Blended soy sauces highlight the market’s segmentation based on the production process and perceived quality. This division not only caters to different economic segments but also reflects a broader consumer trend towards both authentic culinary experiences and economical food solutions.

By Packaging Analysis

Glass jars remain popular, holding 39.2% of the packaging segment.

In 2023, Glass Jars held a dominant market position in the “By Packaging” segment of the Soy Sauce Market, with a 49.2% share. Glass jars are highly favored due to their ability to preserve the authentic taste, aroma, and quality of soy sauce over extended periods.

Their non-reactive nature ensures that the product remains free from contamination, appealing to premium product segments and health-conscious consumers. Additionally, glass jars are perceived as environmentally friendly due to their recyclability, aligning with growing sustainability trends in consumer preferences.

Flexible Packs, offering convenience, portability, and cost efficiency, captured a notable share of the market. These lightweight, resealable packaging options cater to on-the-go lifestyles and are particularly popular in retail and food service sectors where ease of handling and reduced storage space are critical.

Plastic Jars also contributed to the segment’s performance, driven by their durability, affordability, and resistance to breakage. These jars are commonly used in high-volume markets and industrial applications where cost-effectiveness and practicality are prioritized.

The diverse demand across packaging types highlights the importance of convenience, sustainability, and product preservation in influencing consumer choices, demonstrating the market’s adaptability to varying consumer and industrial needs.

By End-User Analysis

Households drive demand, contributing to 58.2% of total soy sauce consumption.

In 2023, Households held a dominant market position in the “By End-User” segment of the Soy Sauce Market, with a 49.2% share. The widespread use of soy sauce in home cooking, driven by its versatility and essential role in a variety of cuisines, positioned this segment at the forefront.

Increasing trends toward home cooking, influenced by growing health consciousness and the popularity of global culinary experimentation, further fueled demand within the household sector. Soy sauce’s long shelf life and multipurpose use as a condiment, marinade, and cooking ingredient make it a staple in kitchens worldwide.

The Processed Food segment also garnered a significant share of the market, as soy sauce is widely used in the production of snacks, ready-to-eat meals, and frozen foods. Its ability to enhance flavor and serve as a natural preservative makes it indispensable in food processing applications, particularly for savory product lines.

The service sectors accounted for a substantial portion of demand, driven by the rising popularity of Asian cuisines globally. Restaurants, fast-food chains, and catering services rely heavily on soy sauce for preparing authentic dishes, flavor enhancement, and cost-effective bulk purchasing.

The segmentation reflects varied usage patterns, emphasizing the importance of soy sauce in both household and industrial applications.

By Distribution Channel Analysis

Supermarkets and hypermarkets dominate sales, capturing 46.2% market penetration worldwide.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Soy Sauce Market, with a 49.2% share. These retail giants are preferred due to their extensive product variety, competitive pricing, and convenient shopping experience.

The availability of both premium and budget-friendly soy sauce brands under one roof attracts a broad consumer base. Additionally, the strategic placement of soy sauce in high-traffic aisles and promotional campaigns further drives sales in this channel.

The HoReCa (Hotels, Restaurants, and Catering) segment also captured a significant share, as these establishments rely heavily on soy sauce for bulk cooking needs and flavor enhancement. The continued growth of the food service industry, especially with the global popularity of Asian cuisines, has sustained demand within this segment.

Quick-Service Restaurants (QSRs) contributed notably, driven by their requirement for consistent and cost-effective ingredients, with soy sauce being a key flavoring agent in sauces, marinades, and dressings.

Convenience Stores cater to on-the-go consumers, offering smaller packaging options for immediate needs, while Online Sales are gaining traction due to increasing digital adoption and the convenience of home delivery, especially for niche or premium soy sauce products.

Key Market Segments

Ву Туре

- Light Soy Sauce

- Dark Soy Sauce

- Others

By Process

- Brewed

- Blended

By Packaging

- Glass Jars

- Flexible Packs

- Plastic Jars

- Others

By End-user

- Processed Food

- Foodservice Sectors

- Households

- Others

By Distribution Channel

- HoReCa

- QSR

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Sales

- Others

Driving Factors

Growing Popularity of Asian Cuisines Across the Globe

The increasing demand for Asian cuisines is driving the soy sauce market. Global consumers are exploring diverse flavors, boosting the adoption of soy sauce as a key ingredient. Its versatility in marinades, dips, and seasonings makes it indispensable in Asian recipes.

Rising tourism and globalization further amplify this trend, as consumers acquire a taste for traditional Asian dishes. Restaurants and food chains are incorporating soy sauce-based offerings to cater to this demand, contributing to steady market growth.

Rising Demand for Healthy and Natural Products

Consumers are leaning toward healthier and natural food products, driving the demand for soy sauce. The introduction of low-sodium and organic soy sauce variants aligns with health-conscious trends. These options cater to dietary preferences and the increasing awareness of reducing salt intake.

Additionally, natural soy sauces free from artificial additives are preferred by consumers seeking clean-label products. This shift in consumer preferences is pushing manufacturers to innovate, ensuring the soy sauce market continues to expand.

Increasing Use of Soy Sauce in Processed Foods

Soy sauce is increasingly used in processed and ready-to-eat foods, boosting its market growth. Its savory, umami flavor enhances the taste of snacks, instant noodles, and frozen meals. Manufacturers are incorporating soy sauce into packaged foods to cater to busy lifestyles and growing convenience food preferences.

The global rise in urbanization and dual-income households further fuels this trend, as consumers opt for quick yet flavorful meals. This widespread application strengthens the soy sauce market’s position in the food industry.

Restraining Factors

High Sodium Content is Restraining the Market

The high sodium content in soy sauce is a major concern, limiting its consumption. Health-conscious consumers are increasingly avoiding products with excessive salt due to risks such as hypertension and heart disease. Despite the availability of low-sodium variants, the perception of soy sauce as unhealthy persists among many.

This trend is particularly pronounced in markets with strict health regulations and growing awareness of lifestyle diseases, restraining the overall growth potential of the soy sauce market.

Rising Competition from Alternative Seasonings is Restraining

The soy sauce market faces challenges from alternative seasonings such as tamari, liquid aminos, and other plant-based sauces. These substitutes appeal to health-conscious and gluten-sensitive consumers, reducing the reliance on traditional soy sauce.

Additionally, the rise of regional seasonings in global markets offers more options for consumers seeking unique flavors. This increasing competition diverts consumer preferences and impacts the demand for soy sauce, creating a significant barrier to the market’s growth.

Fluctuating Soybean Prices are Restraining the Market

The volatility in soybean prices is a critical factor impacting the soysauce market. Soybeans are the primary raw material for soy sauce, and fluctuations in their cost directly affect production expenses. Price hikes due to adverse weather conditions, trade restrictions, or supply chain disruptions increase production costs, reducing profitability for manufacturers.

These challenges make it difficult for producers to maintain competitive pricing, restraining the market’s growth and creating uncertainty in future supply.

Growth Opportunity

Expanding Plant-Based Diets Present Growth Opportunities

The growing adoption of plant-based diets globally creates significant opportunities for the soy sauce market. Soy sauce, being plant-based, aligns with the preferences of vegetarians and vegans seeking flavorful, natural seasonings. As plant-based food products gain traction, soy sauce can further integrate into plant-based meal kits, snacks, and ready-to-eat offerings.

This trend is driven by increasing environmental awareness and a shift toward sustainable eating habits. Manufacturers can capitalize on this by promoting soy sauce as a versatile, plant-friendly condiment.

Innovative Flavors and Products Drive Market Growth

The development of innovative soy sauce flavors and products offers immense growth potential. Consumers are increasingly seeking unique and bold tastes, encouraging manufacturers to introduce flavored variants such as garlic, ginger, and truffle-infused soy sauce.

Additionally, low-sodium and gluten-free versions cater to health-conscious and allergen-sensitive buyers. Enhanced packaging and convenient formats like spray bottles or single-use sachets further attract modern consumers. These innovations meet diverse demands, helping soy sauce brands penetrate new markets and expand their consumer base.

Rising Demand in Emerging Markets Fuels Growth

Emerging markets in Asia, Africa, and Latin America present lucrative opportunities for the soy sauce market. Increasing urbanization, rising disposable incomes, and growing interest in international cuisines drive soy sauce adoption in these regions.

The expansion of retail channels, including supermarkets and online platforms, enhances accessibility. Additionally, local food producers incorporating soy sauce into traditional recipes further bolsters its demand. Targeted marketing strategies and culturally adapted products can help manufacturers tap into these untapped regions, accelerating market growth.

Latest Trends

Growing Popularity of Premium and Artisanal Soy Sauces

Consumers are increasingly seeking premium and artisanal soy sauces, reflecting a trend toward high-quality and authentic flavors. These products often feature traditional brewing methods, organic ingredients, and unique regional profiles. As culinary enthusiasts and foodies demand specialty condiments, manufacturers are introducing limited-edition and craft soy sauce variants.

This trend is particularly strong in gourmet and health-conscious segments, where consumers value flavor complexity and natural processes, driving innovation and growth in the soy sauce market.

Sustainability in Soy Sauce Production Gains Momentum

Sustainability is emerging as a key trend in the soy sauce market. Consumers are showing greater concern for environmentally friendly production practices, prompting manufacturers to adopt sustainable sourcing and packaging methods. Initiatives such as using non-GMO soybeans, reducing water usage, and implementing recyclable packaging appeal to eco-conscious buyers.

This trend aligns with broader global efforts toward sustainability and positions soy sauce brands as responsible and forward-thinking, enhancing their market appeal and long-term competitiveness.

E-Commerce Channels Transforming Soy Sauce Sales Landscape

The rise of e-commerce is reshaping the soy sauce market, providing greater access and convenience to consumers. Online platforms enable the sale of diverse soy sauce varieties, catering to global audiences and niche preferences. Subscription services and direct-to-consumer models further enhance customer engagement.

Additionally, digital marketing and social media influence are driving product awareness and trial. This trend is accelerating market growth, particularly among younger, tech-savvy demographics who prioritize convenience and product discovery through online channels.

Regional Analysis

The Asia-Pacific region dominates the Soy Sauce Market, holding 51.2%, valued at USD 23.1 billion.

The global soy sauce market exhibits varying regional dynamics, with Asia-Pacific leading the market, accounting for 51.2% of the total share, valued at approximately USD 23.1 billion. This dominance is driven by the region’s cultural affinity for soy sauce as a staple ingredient in traditional and modern cuisines. Countries such as China, Japan, and South Korea significantly contribute to this demand due to their large populations and culinary practices.

In North America, the growing popularity of Asian cuisine and the increasing availability of low-sodium and gluten-free soy sauce options have fueled market growth. The region is expected to exhibit steady growth, supported by a rising health-conscious consumer base.

Europe showcases a moderate share, driven by the growing inclination toward international cuisines and plant-based diets. The demand for organic and artisanal soy sauce in countries like Germany and the UK is contributing to this trend.

The Middle East & Africa and Latin America regions hold smaller shares but show growth potential. In these regions, increasing urbanization, exposure to global culinary trends, and expanding retail distribution channels are key growth drivers. The market’s expansion in these areas highlights opportunities for manufacturers to penetrate untapped segments and diversify their regional presence.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global soy sauce market in 2023 exhibited strong growth driven by increasing consumer demand for traditional condiments and innovative product variants. Key players such as Kikkoman Corporation, Lee Kum Kee, and YAMASA Corporation retained their dominance due to their global brand equity, consistent quality, and diversified product portfolios catering to various culinary applications.

Regional giants like Foshan Haitian Flavouring & Food Co. Ltd and Guangdong Meiweixian Flavoring Foods Co., Ltd. capitalized on the robust growth in the Asia-Pacific region, particularly in China, where rising disposable income and evolving food preferences boosted demand. Their ability to scale production and introduce modernized manufacturing technologies further strengthened their position.

Kraft Heinz Company and Nestlé S.A., known for their expansive distribution networks, tapped into the growing preference for soy sauce in Western markets by incorporating health-focused variants, such as low-sodium and organic options, to cater to evolving consumer trends.

Niche producers, including Bourbon Barrel Foods and Marunaka Shouyu, differentiated themselves with artisanal and traditional brewing techniques, appealing to the premium segment. Meanwhile, McCormick & Company Inc. and Masan Group leveraged their diversified product lines to penetrate new geographic markets.

Sustainability and innovation played critical roles, with companies like Shoda Shoyu Co. Ltd. and Okonomi focusing on eco-friendly packaging and plant-based production processes. In a competitive market, key players are expected to prioritize investments in R&D and regional expansions to maintain their market share amidst evolving consumer preferences and intensifying competition.

Top Key Players in the Market

- BOURBON BARREL FOODS

- Foshan Haitian Flavouring & Food Co. Ltd

- Guangdong Meiweixian

- Flavoring Foods Co., Ltd.

- Jiajia Food Group Co., Ltd.

- Kikkoman Corporation

- Koon Chun Hing Kee Soy & Sauce Factory

- Kraft Heinz Company

- Lee Kum Kee

- Maggi

- Marunaka Shouyu

- Masan Group

- McCormick & Company Inc.

- Nestle S.A.

- Okonomi

- Shoda Shoyu Co. Ltd.

- YAMASA Corporation

Recent Developments

- In 2024, Kikkoman Corporation began constructing a $560 million facility in Wisconsin, USA, to boost soy sauce production. This aligns with its mission to meet rising global demand and enhance manufacturing capabilities, strengthening its market presence.

- In 2023, Kraft Heinz Company introduced Master 0 Added Preservatives Low Salt Soy Sauce in China, which is free from additives and contains 30% less sodium, removing 21 tons of salt annually while maintaining a rich flavor. Additionally, their ABC® brand reduced sugar by 10% in its SOTO sweet soy sauce.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 54.9 Billion |

| Forecast Revenue (2033) | USD 91.1 Billion |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Ву Туре (Light Soy Sauce, Dark Soy Sauce, Others), By Process (Brewed, Blended), By Packaging (Glass Jars, Flexible Packs, Plastic Jars, Others), By End-user (Processed Food, Foodservice Sectors, Households, Others), By Distribution Channel (HoReCa, QSR, Supermarkets and Hypermarkets, Convenience Stores, Online Sales, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | BOURBON BARREL FOODS, Foshan Haitian Flavouring & Food Co. Ltd, Guangdong Meiweixian, Flavoring Foods Co., Ltd., Jiajia Food Group Co., Ltd., Kikkoman Corporation, Koon Chun Hing Kee Soy & Sauce Factory, Kraft Heinz Company, Lee Kum Kee, Maggi, Marunaka Shouyu, Masan Group, McCormick & Company Inc., Nestle S.A., Okonomi, Shoda Shoyu Co. Ltd., YAMASA Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |