Quick Navigation

Report Overview

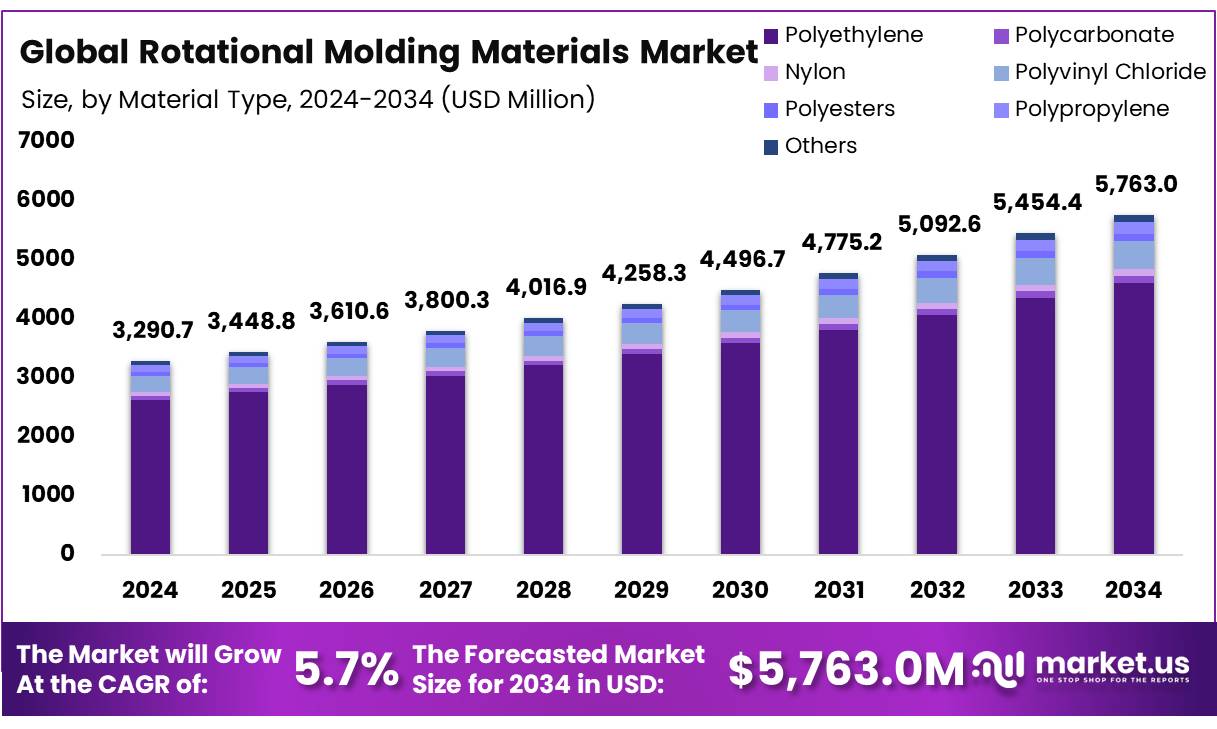

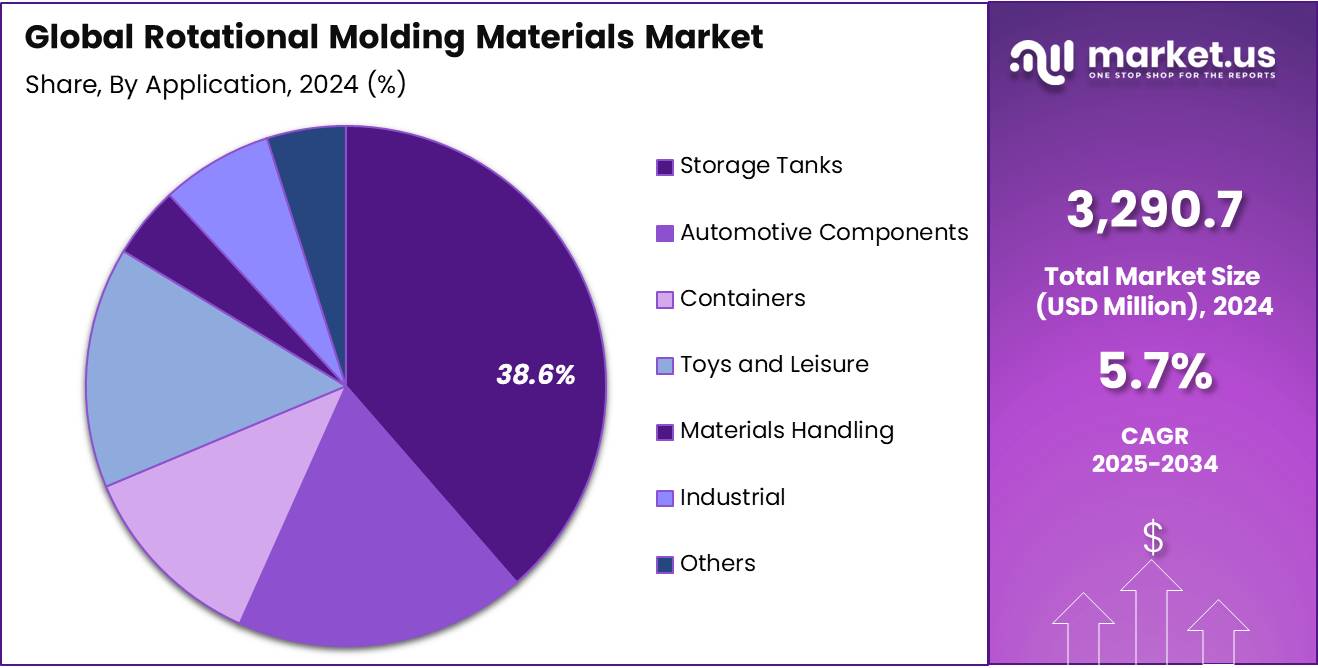

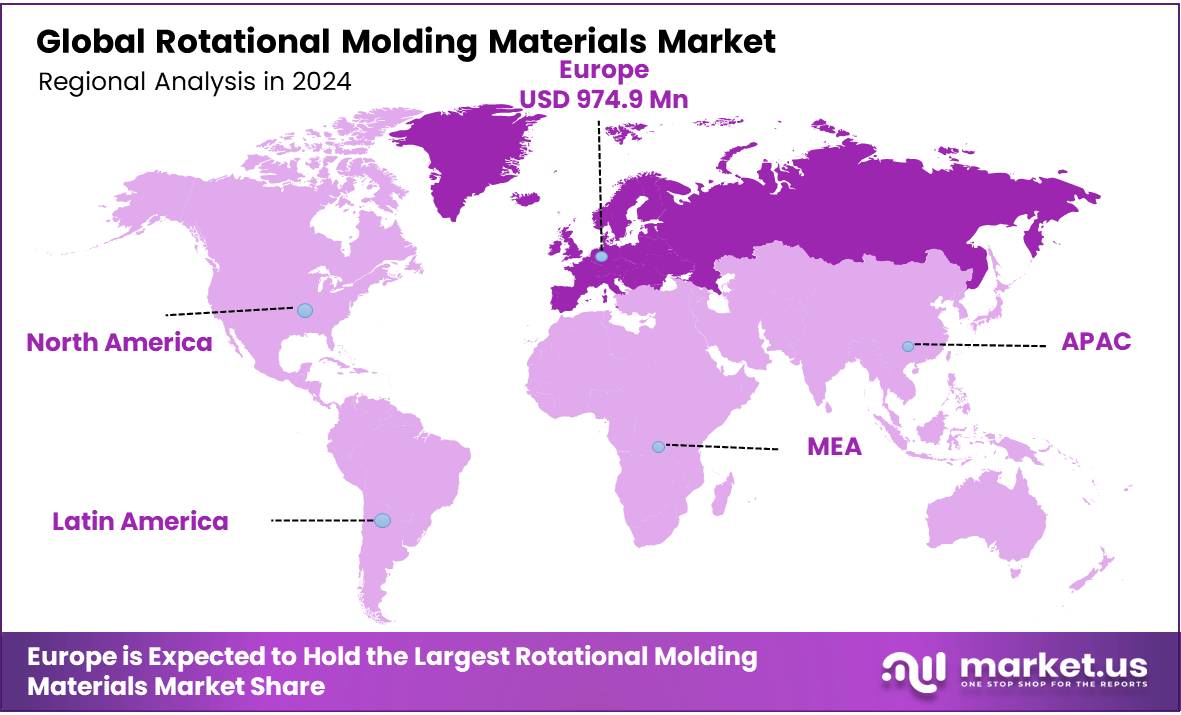

The Global Rotational Molding Materials Market size is expected to be worth around USD 5,763.0 Million by 2034, from USD 3,290.7 Million in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034. In 2024, Europe dominated the market with a 29.6% share, generating USD 855.5 Million in revenue.

The global rotational molding materials market is experiencing significant growth, driven by increasing demand for lightweight, durable, and cost-effective plastic products across various industries such as automotive, packaging, construction, and agriculture. Rotational molding (rotomolding) is a manufacturing process that produces seamless, hollow plastic components with uniform wall thickness, making it ideal for tanks, containers, playground equipment, and industrial storage solutions.

North America and Europe remain key markets due to technological advancements and high industrial applications, while Asia-Pacific is emerging as a high-growth region due to rapid industrialization and infrastructure development. As sustainability and material innovation continue to shape the industry, the rotational molding materials market is expected to witness steady expansion in the coming years.

Key Takeaways

- The global rotational molding materials market was valued at US$ 3,290.7 million in 2024.

- The global rotational molding materials market is projected to grow at a CAGR of 5.7% and is estimated to reach US$ 5,763.0 million by 2034.

- Among material types, polyethylene accounted for the largest market share of 80.0%.

- Among types, virgin accounted for the majority of the market share at 82.0%.

- Based on forms, powder held the majority of the revenue share at 80.4%.

- Among applications, storage tanks accounted for the largest revenue share of 38.6%.

- Based on end-use, construction held the majority of the revenue share at 24.3%.

- Europe is estimated as the largest market for rotational molding materials with a share of 29.6% of the market share.

Material Type Analysis

Polyethylene Materials Dominated the Market, Owing to Their Widespread Application Across Various Industries

The rotational molding materials market is segmented based on polyethylene, polycarbonate, nylon, polyvinyl chloride, polyesters, polypropylene, others. In 2024, the polyethylene segment held a significant revenue share of 80.0%.

Global Rotational Molding Materials Market, By Material Type, 2020-2024 (USD Mn)

| Material Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Polyethylene | 2,246.6 | 2,325.5 | 2,415.8 | 2,513.6 | 2,631.9 |

| Polycarbonate | 57.8 | 59.7 | 61.7 | 63.7 | 65.5 |

| Nylon | 59.8 | 62.1 | 64.6 | 67.0 | 69.3 |

| Polyvinyl Chloride | 235.7 | 243.3 | 252.0 | 261.4 | 272.9 |

| Polyesters | 61.1 | 62.4 | 63.8 | 65.4 | 67.4 |

| Polypropylene | 96.6 | 100.6 | 105.2 | 110.1 | 116.0 |

| Others | 58.2 | 60.2 | 62.4 | 64.9 | 67.8 |

Type Analysis

The Rotational Molding Materials Market Was Dominated By the Personal Care & Cosmetics Industry.

Based on types, the market is further divided into virgin and recycled. The predominance of the virgin materials, commanding a substantial 82.0% market share in 2024 primarily due to its superior quality, durability, and consistency compared to recycled materials. Virgin resins, particularly polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC), are widely preferred in high-performance applications where strength, chemical resistance, and long service life are critical. Industries such as automotive, industrial storage, agriculture, and medical equipment rely heavily on virgin materials to ensure structural integrity and compliance with stringent safety regulations.

Additionally, technological advancements in resin formulation have enhanced the properties of virgin plastics, making them more suitable for customized, precision-molded applications. While sustainability initiatives and circular economy efforts are promoting the use of recycled plastics, challenges such as inconsistent material properties, contamination risks, and limited availability of high-quality recycled resins continue to favor the dominance of virgin materials.

Global Rotational Molding Materials Market, By Type, 2020-2024 (USD Mn)

| Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Virgin | 2,319.4 | 2,397.7 | 2,487.0 | 2,583.4 | 2,699.3 |

| Recycled | 496.4 | 516.1 | 538.4 | 562.6 | 591.5 |

Form Analysis

Based on forms, the market is further divided into powder and granules. The powder form of rotational molding materials dominated the market in 2024, commanding a substantial 80.4% market share, primarily due to its superior processing efficiency, uniformity, and cost-effectiveness. Powdered resins offer better flowability, faster melting, and enhanced dispersion, making them the preferred choice for manufacturers seeking high-quality, consistent, and durable molded products. The fine particle size of powder materials ensures even heat distribution during the rotational molding process, resulting in seamless, structurally strong components with uniform wall thickness.

Additionally, powders allow for greater design flexibility, enabling the production of complex, custom-molded plastic products used across industries such as automotive, packaging, agriculture, and construction. The increasing demand for lightweight, high-performance plastic solutions has further boosted the adoption of powder-based materials, as they offer improved mechanical properties, chemical resistance, and recyclability compared to granules.

Global Rotational Molding Materials Market, By Form, 2020-2024 (USD Mn)

| Form | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Powder | 2,246.1 | 2,328.9 | 2,423.5 | 2,525.5 | 2,647.1 |

| Granules | 569.7 | 584.9 | 602.0 | 620.5 | 643.7 |

Application Analysis

Based on applications, the market is further divided into storage tanks, automotive components, containers, toys and leisure, materials handling, industrial & others. The storage tanks emerged as the dominant application in the rotational molding materials market, commanding a 38.6% market share due to their extensive use in industrial, agricultural, and residential sectors. Rotationally molded storage tanks are widely preferred for their seamless design, high durability, chemical resistance, and cost-effectiveness, making them ideal for storing water, chemicals, fuel, and agricultural liquids.

The increasing demand for water storage solutions in developing regions, coupled with stringent regulations on chemical storage and handling, has further fueled market growth. Additionally, polyethylene-based rotational molding materials, known for their corrosion resistance and lightweight properties, are widely used in large-capacity tanks, making them a preferred choice over traditional metal tanks. The rising adoption of rainwater harvesting systems, wastewater treatment infrastructure, and sustainable agriculture practices has also contributed to the market’s expansion. As industries continue to seek cost-effective, long-lasting storage solutions, the storage tanks segment is expected to maintain its leading position in the coming years.

Global Rotational Molding Materials Market, By Application, 2020-2024 (USD Mn)

| Application | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Storage Tanks | 701.2 | 730.4 | 764.3 | 801.9 | 845.0 |

| Automotive Components | 363.3 | 369.6 | 377.0 | 385.5 | 395.9 |

| Containers | 237.3 | 242.1 | 247.9 | 254.6 | 262.5 |

| Toys and Leisure | 300.6 | 306.1 | 312.3 | 319.5 | 328.3 |

| Materials Handling | 92.8 | 93.5 | 94.5 | 95.8 | 97.5 |

| Industrial | 136.8 | 140.8 | 144.8 | 148.6 | 152.2 |

| Others | 103.5 | 104.0 | 104.9 | 106.0 | 107.5 |

End-Use Analysis

Based on end-uses, the market is further divided into construction, automotive, agriculture, consumer goods, chemical, food & beverage & others. The construction of rotational molding materials dominated the market in 2024, commanding a substantial 24.3% market share primarily due to the increasing demand for durable, lightweight, and cost-effective plastic components in infrastructure and building projects. The growing adoption of polyethylene-based rotationally molded products for applications such as water tanks, septic tanks, pipelines, road barriers, and roofing solutions has significantly contributed to market growth.

These materials offer high strength, corrosion resistance, and weather durability, making them ideal for harsh environmental conditions in construction settings. Additionally, the rise in smart city projects, urbanization, and government investments in sustainable infrastructure has fueled the demand for rotomolded construction materials. The energy efficiency and recyclability of these materials align with green building initiatives, further driving market expansion. With continued advancements in material innovation and customization, the construction sector is expected to maintain its leadership in the rotational molding materials market.

Global Rotational Molding Materials Market, By End-Use, 2020-2024 (USD Mn)

| End-Use | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Construction | 625.5 | 662.2 | 703.7 | 748.0 | 798.3 |

| Automotive | 528.6 | 542.4 | 557.9 | 574.7 | 595.8 |

| Agriculture | 578.2 | 604.4 | 634.0 | 666.0 | 703.9 |

| Consumer Goods | 437.3 | 448.8 | 461.7 | 475.7 | 493.1 |

| Chemical | 321.4 | 326.8 | 333.5 | 340.8 | 350.4 |

| Food & Beverage | 174.3 | 176.7 | 179.7 | 183.1 | 187.7 |

| Others | 150.5 | 152.5 | 155.0 | 157.8 | 161.6 |

Key Market Segments

By Material Type

- Polyethylene

- LLDPE

- HDPE

- XLPE

- MDPE

- LDPE

- Polycarbonate

- Nylon

- Polyvinyl Chloride

- Polyesters

- Polypropylene

- Others

By Type

- Virgin

- Recycled

By Form

- Powder

- Granules

By Application

- Storage Tanks

- Automotive Components

- Containers

- Toys and Leisure

- Materials Handling

- Industrial

- Others

By End-Use

- Construction

- Automotive

- Agriculture

- Consumer Goods

- Chemical

- Food & Beverage

- Others

Drivers

Growing Demand for Lightweight and Durable Plastic Products is Estimated to Boost The Rotational Molding Materials Market.

The growing demand for lightweight and durable plastic products is driven by various factors across industries, including automotive, aerospace, consumer goods, and packaging. This demand is fuelled by the need to improve fuel efficiency, reduce carbon emissions, enhance performance, and lower manufacturing costs. Rotational molding, utilizing both granules and powders, plays a significant role in meeting this demand by offering lightweight yet robust solutions for a wide range of applications.

In the automotive industry, for instance, lightweight plastics are increasingly used to replace heavier materials like metal in vehicle components. Rotomolded plastic fuel tanks, made from polyethylene granules, provide a lightweight alternative that contributes to overall vehicle weight reduction, improving fuel efficiency and reducing emissions without compromising safety or performance. Additionally, rotomolded interior components, such as door panels and storage bins, offer durable and lightweight solutions that enhance comfort and functionality while reducing vehicle weight.

- As per the data from OECD, between 2019 and 2060, the world’s plastics consumption is expected to triple, from 460 million tonnes (Mt) to 1,321 Mt, primarily due to economic expansion.

Restraints

Fluctuating Raw Material Prices May Hinder The Growth Of The Market to a Certain Extent

Fluctuating raw material prices present a significant restraint for the global rotational molding materials market. The market heavily relies on polymer resins such as polyethylene (PE) and polypropylene (PP), which are derived from crude oil and natural gas feedstock. As a result, fluctuations in the prices of crude oil and natural gas directly impact the cost of raw materials for rotational molding.

The volatility of raw material prices can be attributed to various factors, including geopolitical tensions, supply chain disruptions, and shifts in global demand. For instance, geopolitical conflicts in major oil-producing regions, such as the Middle East, can lead to sudden spikes in crude oil prices, causing raw material costs to soar. Similarly, disruptions in the supply chain, such as natural disasters or transportation bottlenecks, can disrupt the availability of raw materials and drive prices higher.

Opportunity

Rising Adoption Of Recycled Rotational Molding Materials

The rising adoption of recycled rotational molding materials presents a significant opportunity for the global market. As sustainability concerns continue to gain prominence across industries, there is growing interest in utilizing recycled materials to reduce environmental impact and promote circular economy principles. Rotational molding, known for its versatility and ability to produce complex shapes, is well-suited for incorporating recycled content into end products.

One of the key drivers behind the adoption of recycled rotational molding materials is the increasing emphasis on environmental responsibility among consumers, businesses, and governments. With growing awareness of plastic pollution and the need to minimize waste, there is a strong demand for eco-friendly alternatives that leverage recycled materials. Rotational molding offers a sustainable solution by repurposing post-consumer and post-industrial plastics into new products, thereby reducing reliance on virgin resins and diverting waste from landfills.

Trends

Growth Strategies Such as Partnership and Acquisition

Partnerships and acquisitions have emerged as a key growth trend in the rotational molding materials market, enabling companies to expand product portfolios, enhance manufacturing capabilities, and strengthen market presence. Leading manufacturers are forming strategic alliances with material suppliers, research institutions, and technology providers to develop high-performance and sustainable polymers, addressing the increasing demand for eco-friendly and recyclable materials. Acquisitions are also reshaping the market, as large corporations acquire smaller, specialized firms to gain access to innovative materials, advanced production technologies, and new customer bases.

For instance, mergers between polymer manufacturers and rotational molders allow for streamlined supply chains and reduced production costs, boosting overall efficiency. Additionally, collaborations with automotive, packaging, and industrial sectors are driving the adoption of custom-engineered resins tailored to industry-specific needs. As competition intensifies, companies leveraging partnerships and acquisitions are better positioned to stay ahead, capitalize on emerging opportunities, and drive long-term market growth.

Geopolitical Impact Analysis

Geopolitical Pressures and Disturbances In The Worldwide Supply Chain Have A Adverse Impact On The Growth Of The Rotational Molding Materials Market.

Geopolitical tensions and disruptions in the global supply chain have significantly impacted the growth of the rotational molding materials market by causing supply shortages, rising material costs, and production delays. Trade wars, tariffs, and political instability can lead to uncertainty in sourcing raw materials, as companies become dependent on specific regions for key resources like polyethylene, polypropylene, and other polymers. These disruptions can cause delays in material procurement, impacting manufacturing timelines and increasing costs for companies.

Additionally, logistical challenges, such as port congestion, transportation bottlenecks, and labor shortages, have further hindered the efficient flow of materials across borders. The resulting cost escalations and inability to meet demand can harm profit margins and strain relationships with customers. Overall, geopolitical tensions and supply chain disruptions create market volatility, making it difficult for companies in the rotational molding materials sector to maintain consistent production, pricing stability, and market competitiveness.

Regional Analysis

Europe Held the Largest Share of the Global Rotational Molding Materials Market

In 2024, Europe dominated the global rotational molding materials market, accounting for 29.6% due to several key factors, including rapid industrialization, infrastructure development, and growing demand for plastic products. The region’s emerging economies, particularly China, India, and Southeast Asia, have seen significant growth in sectors such as automotive, construction, and consumer goods, all of which rely heavily on rotationally molded products.

The availability of low-cost labor and affordable raw materials in Asia-Pacific also provides a competitive advantage, making it a hub for manufacturing and cost-efficient production. The region’s strong manufacturing base and advancements in rotomolding technologies have driven increased adoption of rotational molding in industries like packaging, agriculture, and material handling.

Additionally, government initiatives to boost infrastructure and manufacturing sectors, alongside rising demand for sustainable and eco-friendly products, have spurred the growth of rotational molding materials in the region. Asia-Pacific’s strategic location, with access to major global shipping routes, enhances supply chain efficiencies, ensuring timely delivery of materials at competitive prices. As industries in Asia-Pacific continue to expand and modernize, coupled with rising consumer demand for innovative plastic products, the region is expected to maintain a dominant position in the global rotational molding materials market.

Global Rotational Molding Materials Market, By Region, 2020-2024 (USD Mn)

| Region | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| North America | 691.4 | 718.7 | 749.7 | 783.0 | 822.7 |

| Europe | 855.5 | 879.6 | 907.6 | 937.8 | 974.9 |

| Asia Pacific | 649.0 | 679.5 | 713.7 | 750.4 | 793.5 |

| Middle East & Africa | 382.5 | 392.7 | 404.4 | 417.2 | 432.8 |

| Latin America | 237.3 | 243.2 | 250.1 | 257.6 | 266.8 |

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

To Maintain a Competitive Edge, Major Companies In The Rotational Molding Materials Market Focus On Product Innovation and Research & Development (R&D)

To maintain a competitive edge in the rotational molding materials market, major companies focus heavily on product innovation and research & development (R&D). By continuously developing new materials with enhanced performance characteristics such as strength, flexibility, and sustainability, companies can meet the evolving demands of industries like automotive, packaging, and construction.

Investments in R&D allow firms to create eco-friendly, recyclable materials and improve manufacturing processes for greater efficiency and cost-effectiveness. Furthermore, companies are leveraging advanced technologies like 3D printing and automation to enhance product design, reduce material waste, and deliver customized solutions, ensuring they remain competitive in a rapidly growing market.

The following are some of the major players in the industry

- SCG Chemicals

- LyondellBasell Industries Holdings B.V.

- ExxonMobil

- Reliance Industries Limited

- SABIC

- Matrix Polymers Limited

- Rototech Industries

- GreenAge Industries

- Prisma Colour Limited

- Petrotech Group

- PTT Global Chemical Public Company Limited.

- DOMO Chemicals

- Broadway Colours

- Roto Polymers

- OSWAL HITECH PVT. LTD.

- Mabaplast

- Kalpataru Polymer Private Limited

- Pinaxis Polymer

- Xiamen Keyuan Plastic Co., Ltd

- Other Key Players

Key Development

January 23, 2024: LyondellBasell introduces Petrothene T3XL7420, a groundbreaking polymer compound engineered to revolutionize manufacturing processes. This innovative product not only enhances the quality of end products but also caters to the specific requirements of wire producers in automotive and appliance industries. Developed in response to customer demands and industry trends, Petrothene T3XL7420 is meticulously designed to streamline production line speeds and improve overall manufacturing efficiency.

July 2023, GC has introduced Matrix Polymers Thai, a move aimed at expanding its production capacity in Asia to achieve full integration.

April 2022, DOMO Chemicals, a renowned global leader in engineered materials, has revealed a long-term investment strategy in China aimed at further enhancing its production capacity of TECHNYL® high-performance polyamides.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3,290.7 Mn |

| Market Volume (2024) | XX Ton |

| Forecast Revenue (2034) | US$ 5,763.0 Mn |

| CAGR (2025-2034) | 5.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Polyethylene, Polycarbonate, Nylon, Polyvinyl Chloride, Polyesters, Polypropylene, and Others), By Type (Virgin, and Recycled), By Form (Powder, and Granules) By Application (Storage Tanks, Automotive Components, Containers, Toys and Leisure, Materials Handling, Industrial, and Others) By End-use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | SCG Chemicals, LyondellBasell Industries Holdings B.V., ExxonMobil, Reliance Industries Limited, SABIC, Matrix Polymers Limited, Rototech Industries, GreenAge Industries, Prisma Colour Limited, Petrotech Group, PTT Global Chemical Public Company Limited., DOMO Chemicals, Broadway Colours, Roto Polymers, OSWAL HITECH PVT. LTD., Mabaplast, Kalpataru Polymer Private Limited, Pinaxis Polymer, Xiamen Keyuan Plastic Co.,Ltd, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |