Quick Navigation

Report Overview

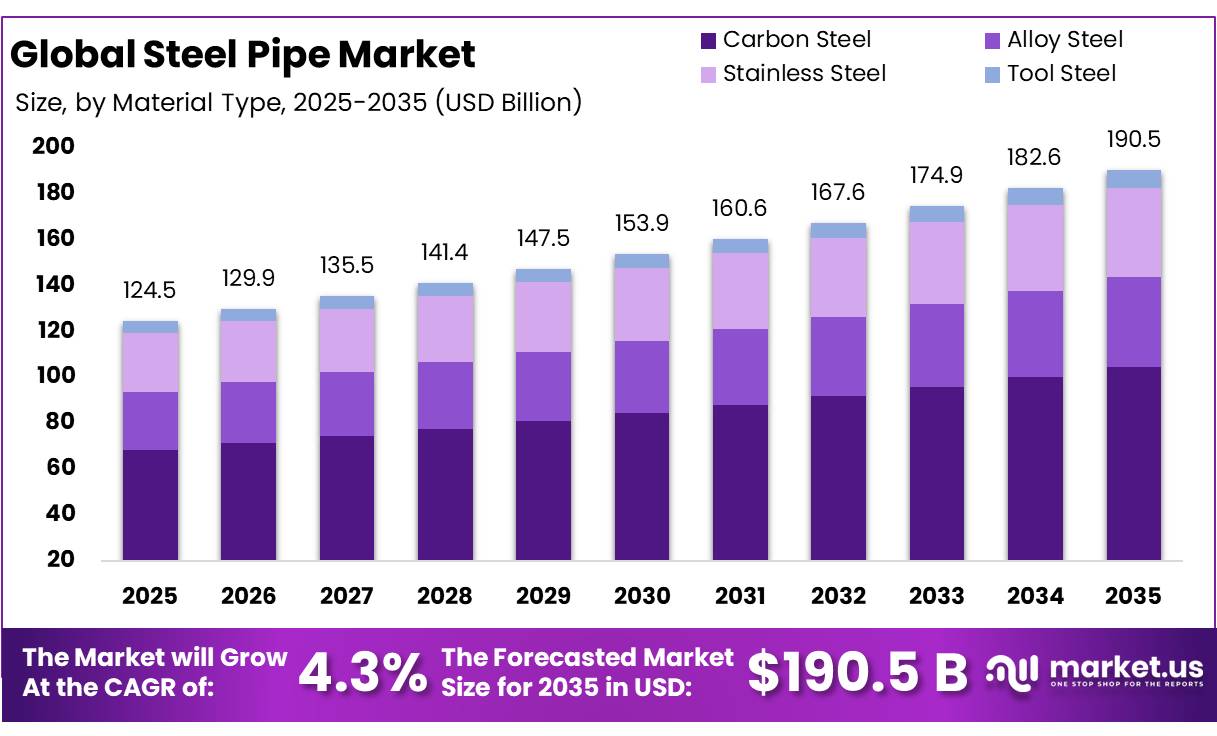

The Global Steel Pipe Market size is expected to be worth around USD 190.5 Billion by 2035, from USD 124.5 Billion in 2025, growing at a CAGR of 4.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 47.5% share, holding USD 0.4 Billion revenue.

- According to the World Steel Association, global crude steel production reached 1,882.6 million tonnes in 2024, while apparent finished steel consumption stood at approximately 1.75 billion tonnes. Demand remains closely linked to key end-use sectors such as construction, energy, manufacturing, and mechanical engineering.

Key Takeaways

- The Steel Pipe Market was valued at USD 124.5 billion in 2025.

- The market is expected to reach USD 190.5 billion by 2035.

- The market is projected to grow at a CAGR of 4.3% from 2026 to 2035.

- Carbon Steel remained the leading material type, holding 54.8% of the total market share.

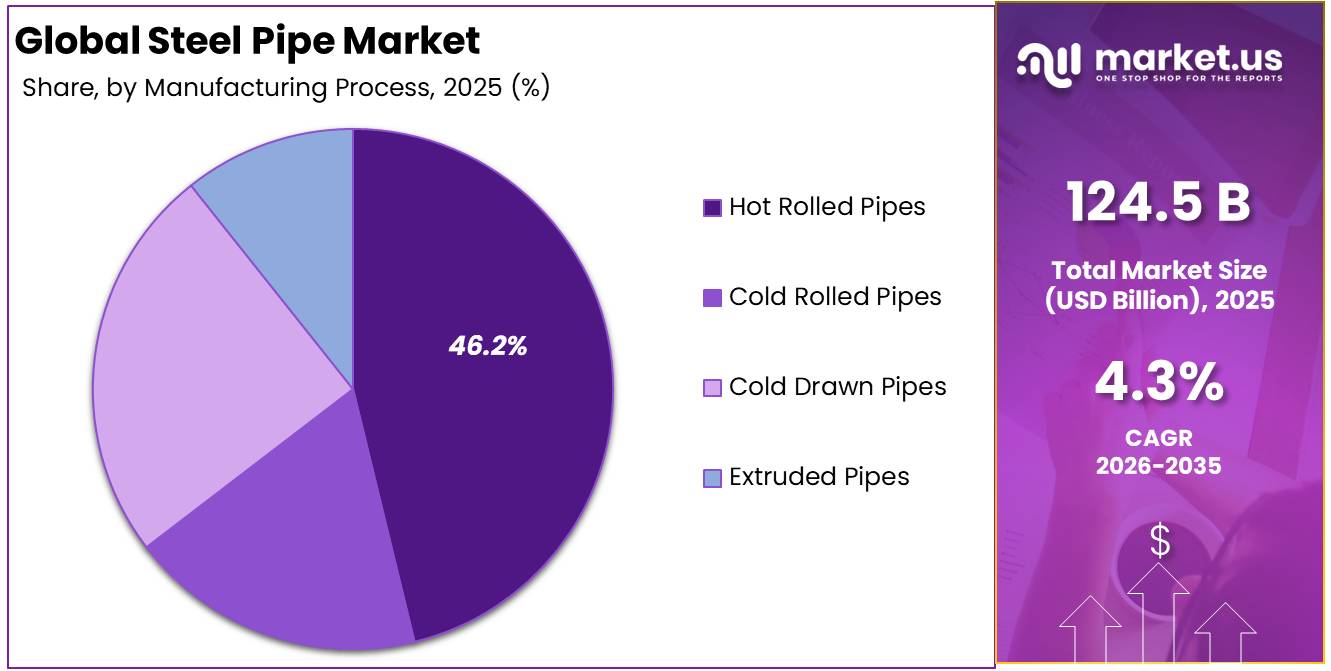

- Hot Rolled Pipes led the manufacturing process segment, accounting for 46.2% of total revenue.

- Oil & Gas Transportation was the top application segment, with a 28.9% revenue share.

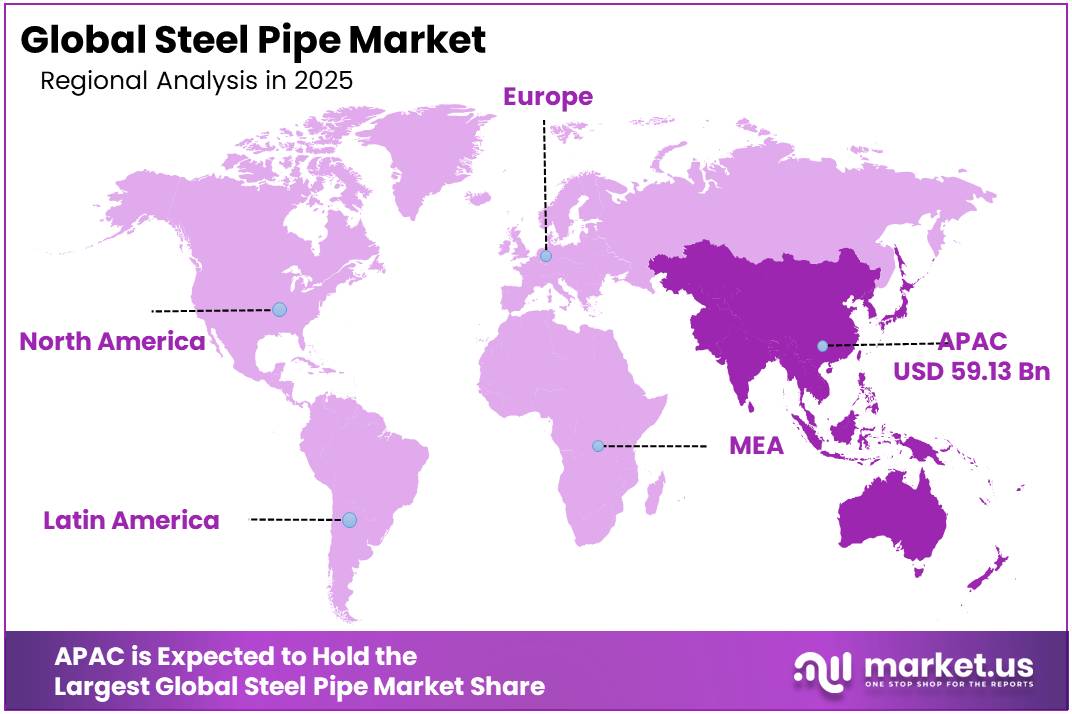

- Asia Pacific dominated the regional market, capturing 47.5% of global revenue.

- North America and Europe were the second and third largest markets. Growth in these regions was supported by oil and gas pipeline modernization and infrastructure renewal projects.

- Middle East and Africa was the fastest-growing region. This growth was driven by rising investments in water transmission systems and oil and gas pipeline projects.

- Market growth is mainly supported by higher energy infrastructure spending, rapid urbanization, and the expansion of water transmission networks across the world.

Globally, more than 1.18 million km of oil and gas pipelines are currently operating across 162 countries, with an additional 212,000 km+ of pipelines either under construction or planned. These projects represent nearly US$ 1 trillion in future investments. Since each kilometer of large-diameter pipeline requires hundreds of tonnes of API-grade carbon steel pipe, even modest expansion in pipeline infrastructure creates significant additional demand for steel pipes worldwide.

Asia Pacific accounted for 47.5% of global market revenue, supported by its position as both the largest steel-producing and steel-consuming region. According to worldsteel, China produced approximately 1.0 billion tonnes of crude steel in 2024, representing more than 50% of global output, while India produced around 150 million tonnes, recording 6.3% year-on-year growth. India has also remained the world’s fastest-growing steel demand market for the past three years, with steel consumption expected to increase by about 8% annually during 2024 and 2025, driven by investments in highways, metro rail systems, industrial parks, and urban housing projects.

Long-term urbanization trends further strengthen demand prospects. The United Nations estimates that the global urban population will increase from 4.2 billion in 2018 to 6.7 billion by 2050, with nearly 90% of this growth occurring in Asia and Africa. Together, India and China are expected to add more than 670 million new urban residents. Rapid urban expansion requires extensive water distribution networks, district heating systems, fire protection infrastructure, and structural construction materials, all of which rely heavily on steel pipes due to their superior pressure resistance, durability, temperature tolerance, and structural strength.

- For instance, ArcelorMittal stated that in 2024, its steel pipes and tubes business segment produced revenue exceeding $4.2 billion, while oil and gas industry customers were the single largest end-users of their products, contributing to 34% of the total volume of sales made by this segment due to pipeline construction projects in the Middle East, North America, and Latin America.

Steel Pipe Market Segmentation

Material Type Analysis

Carbon steel pipes lead the market due to cost efficiency, strength, and wide industrial applications.

Carbon Steel is the market leader among the material type category with an overwhelming 54.8% revenue share. Carbon steel pipes dominate the global steel pipe market due to their critical role in high-volume infrastructure and energy transportation systems, where cost efficiency and mechanical strength are essential.

According to the World Steel Association, global crude steel production exceeded 1.88 billion tonnes in 2024, with carbon steel accounting for the vast majority, ensuring abundant and cost-effective raw material availability. Their widespread use is directly tied to energy demand: the International Energy Agency (IEA) reports that global oil demand reached over 102 million barrels per day in 2024, necessitating extensive pipeline networks constructed primarily from carbon steel compliant with API and ASTM standards. Global energy procurement mandates require compliance with API 5L, ASTM A53, and ISO 3183 standards, compelling EPC contractors to default to carbon steel for major midstream transmission networks.

- For instance, Tenaris stated that its revenue from the carbon steel OCTG products amounted to US$ 7.8 billion for the year 2024, and the most voluminous category of buyers was North American shale oil and gas companies due to their increasing drilling programs in the Permian and Eagle Ford shale plays, necessitating constant purchases of carbon steel casing and tubing in huge volumes.

The market shares of Alloy steel and Stainless steel are equal to 20.6%. The Alloy steel is used for power generation and chemical process industries where mechanical strength becomes more important. The Stainless steel is growing rapidly due to rising demand for corrosion resistant pipes in the chemical, pharmaceuticals, food processing, and marine industries. The Tool steel caters to the specialty mechanical engineering industries.

Manufacturing Process Analysis

Hot rolled pipes lead the manufacturing segment due to scale, cost efficiency, and large diameter capability.

Hot-rolled pipes command the largest share of the steel pipe manufacturing market, accounting for 46.2% of total revenue, because they uniquely align high-volume steel output with the heavy-duty demand profile of energy, water, and construction infrastructure. World crude steel production reached about 1.89 billion tonnes in 2023, with China alone accounting for roughly 54% of output, underpinning massive hot-rolling capacity across integrated mills operated by groups such as Baowu, Nippon Steel, and ArcelorMittal.

Global oil transmission pipeline projects under construction total around 9,100 km, with a further 21,900 km proposed, and nearly half of this length located in Africa and the Middle East—regions that heavily favor large-diameter steel lines for export and interconnector schemes. This sustained pipeline build-out directly pulls demand for hot-rolled pipe rather than smaller, cold-formed alternatives. Because hot rolling offers the lowest unit cost at scale and can process a wide range of carbon and alloy grades into everything from mechanical tubing to pipe above 60 inches, it remains the core, default route for steel pipe manufacture worldwide.

- For instance, JFE Steel Corporation announced that it successfully expanded its production capacity for hot-rolled large diameter steel pipes through Q3 2024 at its Fukuyama Works plant. This led to an additional annual production capacity of 180,000 tons, as there is rising demand for the product by off-shore oil and gas pipeline projects located in the Southeast Asian and Middle Eastern regions.

Cold Drawn Pipes with a share of 24.7% constitute the second-biggest production process in terms of manufacture of high-tolerance pipes used in automotive, mechanical engineering, and hydraulic cylinder applications. Cold Rolled Pipes at 18.4% cater to thin wall applications, whereas Extruded Pipes at 10.7% are the fastest growing production process owing to rising demand for seamless pipes made from stainless steel and alloy steel used in high pressure applications.

Application Analysis

Oil and gas transportation leads steel pipe applications due to strong infrastructure demand and strict pipeline requirements.

Oil & Gas Transportation accounted for 28.9% of the market, maintaining its position as the leading application segment due to the extensive use of steel pipes in global oil and natural gas transmission infrastructure. According to the International Energy Agency (IEA), global oil demand exceeded 102 million barrels per day in 2024, while natural gas consumption surpassed 4 trillion cubic meters, creating sustained demand for high-capacity pipeline networks. Steel pipes remain the preferred solution because they can withstand operating pressures of more than 1,000–1,500 psi and extreme temperatures ranging from -60°C to 150°C, conditions that alternative materials cannot reliably support.

- For instance, Welspun Corp reported that its large-diameter API-grade steel pipe division secured orders totaling over US$ 1.1 billion from oil and gas pipeline operators across the United States, Middle East, and Australia in 2024 — with pipeline operators increasingly specifying higher-grade X70 and X80 steel pipe for new projects to reduce wall thickness requirements and lower total installed pipeline weight and cost.

The dominance of this segment is further reinforced by the scale of existing and expanding pipeline infrastructure worldwide. The United States Energy Information Administration (EIA) reports that the U.S. operates more than 3 million miles of natural gas pipelines, while the International Gas Union estimates that global cross-border gas pipeline networks exceed 1.2 million kilometers. These large-scale systems rely on high-strength API-grade steel pipes, including X70 and X80, due to their superior durability, corrosion resistance, and operational lifespan of 25–50 years.

Key Market Segments

By Material Type

- Carbon Steel

- Alloy Steel

- Stainless Steel

- Tool Steel

By Manufacturing Process

- Hot Rolled Pipes

- Cold Rolled Pipes

- Cold Drawn Pipes

- Extruded Pipes

By Application

- Oil & Gas Transportation

- Water & Wastewater Transmission

- Construction & Infrastructure

- Power Generation

- Chemical & Petrochemical

- Automotive

- Mechanical & Engineering

- Agriculture & Irrigation

- Mining

- Marine

- Others

Drivers

Water transmission and lead-line replacement cycle

Government-backed water infrastructure upgrades are creating steady demand for steel pipes, particularly in municipal water transmission and distribution networks. The U.S. Infrastructure Investment and Jobs Act allocated USD 15 billion for lead service line replacement, distributed at USD 3 billion annually from 2022 to 2026. Following the October 16, 2024 inventory deadline and upcoming compliance requirements extending beyond 2027, utilities are increasingly investing in broader network modernization projects.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy security pipeline buildout and OCTG restocking | 1.40% | North America core, MENA, India, selected LATAM basins | Short term (≤ 2 years) |

| Water transmission and lead-line replacement cycle | 1.10% | U.S. core, Canada selective, urban APAC spill-over | Medium term (2-4 years) |

| Infrastructure steel demand rebound outside China | 0.90% | India core, ASEAN, MENA, EU recovery pockets, U.S. | Short term (≤ 2 years) |

| CBAM and emissions-traceable procurement shift | 0.70% | EU core, Turkey, India, East Asia exporters | Medium term (2-4 years) |

| Premium grades for hydrogen, corrosion, and high-pressure service | 0.80% | EU corridors, North America, GCC, offshore projects | Long term (≥ 4 years) |

| Mill automation and higher-yield domestic substitution | 0.60% | China, India, U.S., EU, Japan/Korea | Medium term (2-4 years) |

Restraints

Tariffs and trade remedies

Trade restrictions have become a significant challenge for the steel pipe industry as rising tariffs increase the cost of cross-border steel procurement. Under the revised U.S. Section 232 framework effective April 6, 2026, many steel products are subject to a 50% tariff, while several steel derivative products face a 25% tariff. These duties substantially increase landed costs for imported pipes, tubing, and fabricated steel products, reducing their competitiveness.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material cost swings | -1.30% | APAC core, EU, North America | Short term (≤ 2 years) |

| Tariffs and trade remedies | -1.10% | U.S. core, EU, UK, export Asia | Short term (≤ 2 years) |

| China demand drag and export glut | -1.00% | China core, ASEAN, MENA, EU spill-over | Medium term (2-4 years) |

| Carbon-compliance cost burden | -0.80% | EU core, Turkey, India, East Asia exporters | Medium term (2-4 years) |

| Project delays in energy and water | -0.70% | North America, EU, LATAM, GCC | Medium term (2-4 years) |

| High rates and weak private capex | -0.60% | EU, North America, developed APAC | Short term (≤ 2 years) |

Opportunity

Hydrogen-ready pipe platforms

Hydrogen pipeline infrastructure represents a major future opportunity for the steel pipe industry, although large-scale demand is still in the planning and early procurement stages. The European Hydrogen Backbone initiative targets an initial 11,600 km hydrogen network by 2030, expanding to 39,700 km by 2040, with estimated investments of EUR 27–64 billion.

Approximately 75% of the planned network could be created by repurposing existing natural gas pipelines, creating demand for both new hydrogen-ready steel pipes and retrofit solutions. Manufacturers that develop hydrogen-certified products early can benefit from higher-value specification packages, with potential pricing premiums of 12%–20% above conventional line pipes while strengthening long-term customer relationships.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Hydrogen-ready pipe platforms | 1.60% | EU core, North America, GCC | Medium term (2-4 years) |

| Desalination transmission buildouts | 1.30% | MENA core, India, North Africa | Medium term (2-4 years) |

| Low-carbon traceable export pipe | 1.10% | EU core, Turkey, India, East Asia | Short term (≤ 2 years) |

| Pipe-plus-services monetization | 0.90% | North America, EU, APAC industrial hubs | Short term (≤ 2 years) |

| M&A in coating and threading | 0.80% | U.S., India, GCC, Southeast Asia | Medium term (2-4 years) |

| Circular pipe and reuse channels | 0.70% | EU, North America, developed APAC | Long term (≥ 4 years) |

Challenge

CBAM data traceability

CBAM compliance is becoming a significant operational challenge for steel pipe manufacturers exporting to Europe. From 2026 onward, companies must provide verified plant-level emissions data, with reporting reviewed by accredited third parties. The framework sets a 5% materiality threshold for embedded emissions per tonne, requires mandatory site visits during the first year, and mandates the first annual declaration by September 2027. Many mid-sized producers lack integrated systems for carbon tracking, creating additional compliance burdens.

Challenges Impact Analysis

| Challenge | (~) % Potential CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| CBAM data traceability | -1.00% | EU regulatory hubs, India, Turkey, East Asia exporters | Medium term (2-4 years) |

| Skilled welding gap | -0.90% | North America core, EU, GCC, India | Long term (≥ 4 years) |

| Project timing volatility | -0.80% | North America, LATAM, MENA, EU | Medium term (2-4 years) |

| Logistics lead-time swings | -0.70% | APAC corridors, EU, North America import hubs | Short term (≤ 2 years) |

| Energy-intensity exposure | -0.70% | EU, India, East Asia, Turkey | Medium term (2-4 years) |

| Product-mix yield instability | -0.60% | Global premium-grade mills | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade policies, steel tariffs, and energy security strategies reshaping global steel pipe supply chains.

A convergence of strict carbon border taxes, restructured tariff regimes, and energy market volatility is permanently altering global steel pipe trade flows. This fractured geopolitical landscape is forcing EPC contractors and distributors to prioritize supply security over lean inventory models, fundamentally reshaping procurement economics for OCTG and line pipe.

- The United States continues to enforce the Section 232 tariff framework. Under the revised 2026 structure, selected steel and derivative products are subject to tariff rates of 50%, 25%, and 15%, which are now calculated on the full customs value rather than only the metal content. This significantly increases costs for higher-value products such as API-grade welded and seamless steel pipes used in the oil & gas and construction sectors.

Europe is also introducing severe cost pressures through environmental regulations. The European Union’s Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase in 2026, requiring importers to purchase CBAM certificates that reflect the embedded carbon emissions of imported steel products. With the European Commission setting the initial 2026 CBAM certificate price at €75.36 per tonne of CO2, highly emissive steel imports—such as blast-furnace hot-rolled coil used in pipe manufacturing—can face added carbon penalties of roughly €254 per tonne. As a result, steel pipe exports from countries such as India, Turkey, and China face massive cost disadvantages when supplying EU pipeline, district heating, and construction projects.

Energy security concerns are also reshaping steel pipe demand and supply chains. According to the World Bank’s April 2026 Commodity Markets Outlook, Brent crude oil prices are projected to remain elevated, averaging $86 per barrel in 2026 before easing toward $70 per barrel in 2027. This volatility directly impacts drilling activity, steel pipe procurement budgets, and project planning for oil and gas operators, which represent a major share of global OCTG demand.

Supply chain risks remain elevated as conflicts disrupt global trade routes. The International Energy Agency (IEA) has highlighted tightening oil availability and declining inventories, increasing freight and fuel cost volatility on key shipping routes between Asia, Europe, and the Middle East. Combined with U.S. tariffs and EU CBAM regulations, global trade is increasingly shifting toward “friendly” sourcing countries. This market fragmentation has extended average delivery times by 5 to 10 days compared to historical trade patterns.

Regional Analysis

Asia Pacific Dominates the Global Steel Pipe Market, Accounting for 47.5% Revenue Share in 2025.

The Asia Pacific region occupies the leading position among the steel pipe producers worldwide in 2025 owing to its 47.5% share in revenue, due largely to China being the world’s biggest producer and consumer of steel pipes, together with the substantial contribution from India, Japan, and South Korea as secondary key players.

This dominance can be attributed to the region having the highest concentration of steel production capacity in the world with China alone accounting for more than 50% of global steel production capacity together with its growing infrastructure spending pipeline. This includes government-sponsored mega-infrastructure projects like the Chinese Belt and Road Project, India’s National Infrastructure Pipeline valued at US$ 1.4 trillion till 2025 and other ASEAN urbanization programs.

- For instance, Baowu Steel Group – the largest manufacturer of steel in the world – posted segment revenue in excess of US$ 12 billion in 2024 from its steel pipe and tubes business line, with the majority share (over 70%) coming from domestic Chinese end users in the construction, energy, and water infrastructures sectors.

The North American region is the second largest market in terms of investment in pipelines, shale wells drilling operations, and municipal water works system upgrades. The European market is another important market that is based on the applications of industry, chemicals, and offshore energy. The Middle East and Africa regions is the fastest growing market due to large scale investments in oil and gas infrastructures and water security projects among the GCC countries. Latin America is another growing market where there are developments in oil and gas pipelines and agricultural irrigation infrastructures in Brazil and Mexico.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Competitive strengths for suppliers operating in the international steel pipe industry involve integrated steel making capability alongside pipe manufacturing, diversified range of grades from carbon, alloy, to stainless steel categories, and distribution facilities across multiple geographic regions catering to energy sector users, construction sector consumers, and industrial application clients.

Key strategy areas for suppliers are development of high-grade API and OCTG pipe grades for oil & gas use; production of highly precise tolerance cold drawn pipes for automotive and machinery engineering sectors; and manufacture of environmentally friendly steel pipes by using electric arc furnace techniques. Expansion and improvement in production capacity, digital quality assurance, and certification according to API, ASTM, ISO, and EN standards remain ongoing initiatives for capturing higher price levels at institutions.

Vertical integration within the process chain from steel manufacturing to pipe manufacturing and coating provides economies of scale in terms of costs and specifications within high volume contracts for energy and infrastructure sectors. Framework supply agreements with national oil companies, EPC contractors, and municipal infrastructure agencies help ensure financial stability and buyer retention until 2035.

Market Key Players

- Tenaris

- Nippon Steel

- JFE Steel Corporation

- United States Steel Corporation

- ArcelorMittal

- TMK

- Vallourec

- ChelPipe Group

- SeAH Steel

- Hyundai Steel

- Maharashtra Seamless

- APL Apollo Tubes

- Tata Steel

- Welspun Corp

- EVRAZ

- Borusan Mannesmann

- Baowu Steel Group

- Youfa Steel Pipe Group

- Zekelman Industries

- Northwest Pipe Company

- Other Key Players

Key Development

- In February 2026, Nippon Steel secured a large-diameter API-grade steel pipe supply contract for a major LNG export terminal pipeline project in Southeast Asia, covering over 85,000 tonnes of high-grade carbon steel line pipe delivery through 2027.

- In March 2026, APL Apollo Tubes commissioned a new structural steel hollow section manufacturing facility in India, adding 600,000 tonnes of annual production capacity to serve surging domestic construction and infrastructure sector procurement demand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 124.5 Billion |

| Forecast Revenue (2035) | USD 190.5 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Carbon Steel, Alloy Steel, Stainless Steel, Tool Steel), By Manufacturing Process (Hot Rolled Pipes, Cold Rolled Pipes, Cold Drawn Pipes, Extruded Pipes), By Application (Oil & Gas Transportation, Water & Wastewater Transmission, Construction & Infrastructure, Power Generation, Chemical & Petrochemical, Automotive, Mechanical & Engineering, Agriculture & Irrigation, Mining, Marine, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Tenaris, Nippon Steel, JFE Steel Corporation, United States Steel Corporation, ArcelorMittal, TMK, Vallourec, ChelPipe Group, SeAH Steel, Hyundai Steel, Maharashtra Seamless, APL Apollo Tubes, Tata Steel, Welspun Corp, EVRAZ, Borusan Mannesmann, Baowu Steel Group, Youfa Steel Pipe Group, Zekelman Industries, Northwest Pipe Company, and Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |