Quick Navigation

Report Overview

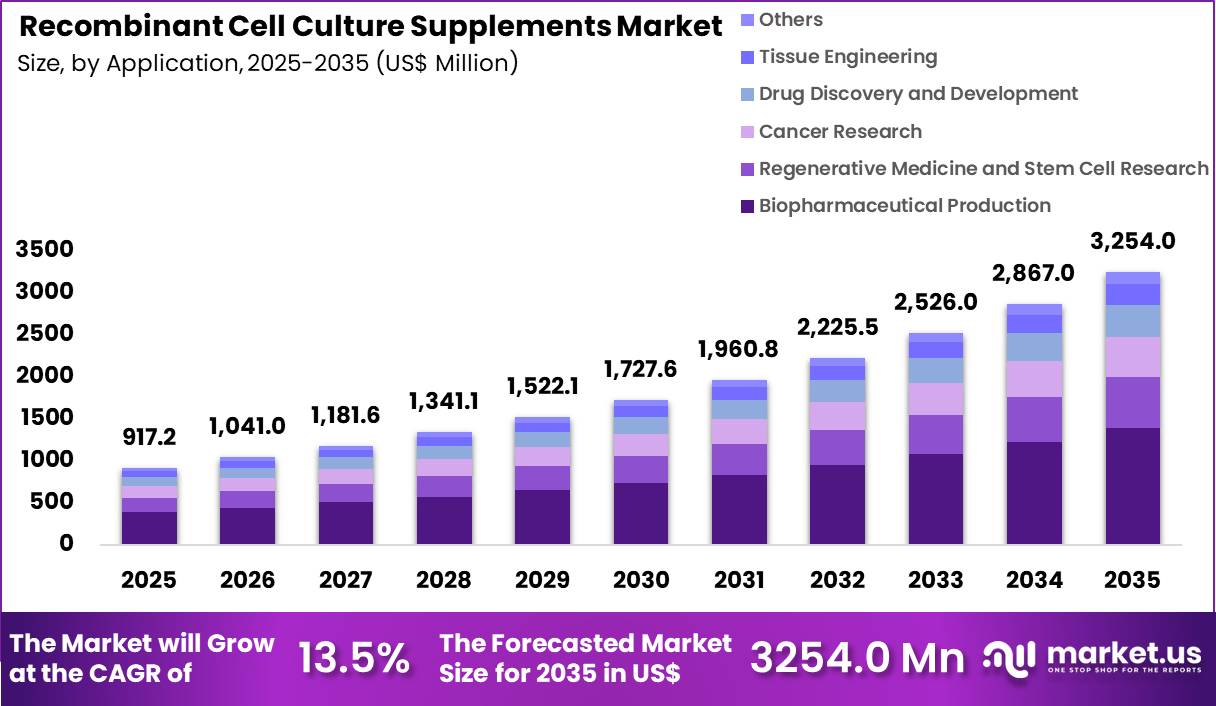

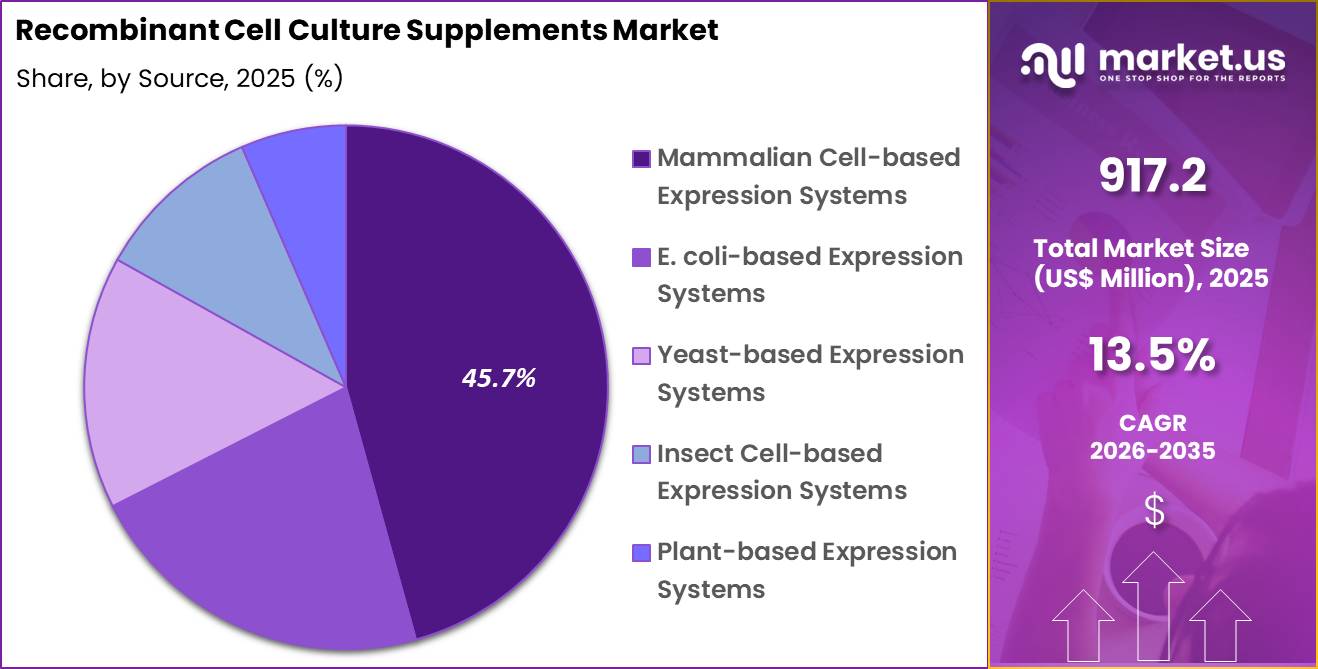

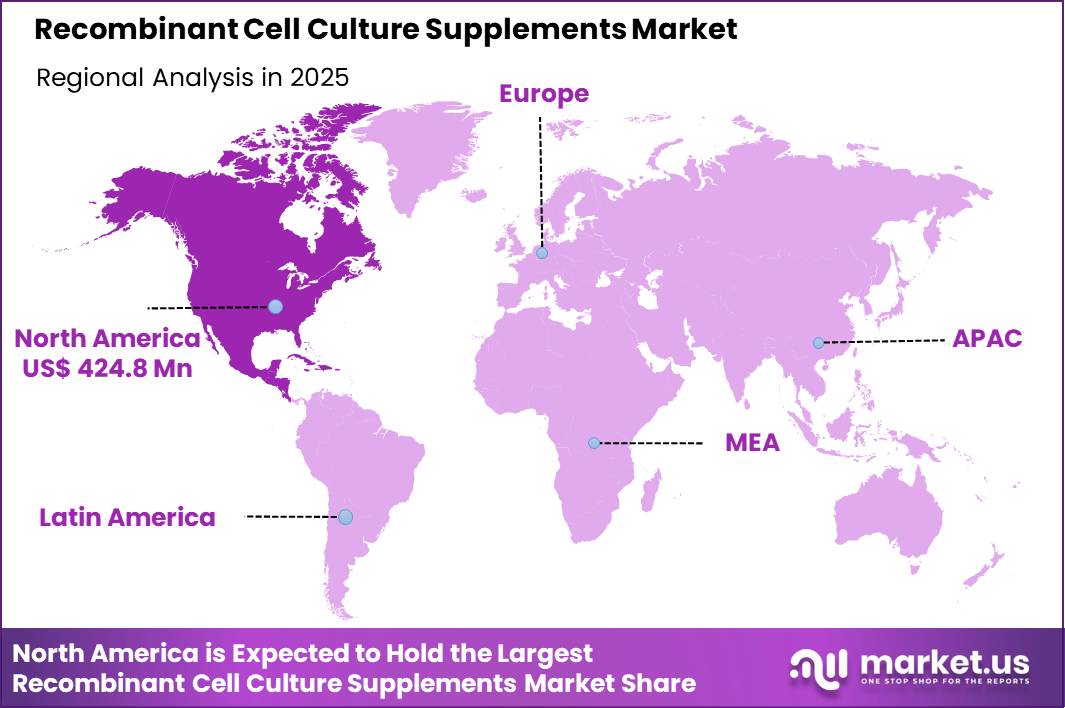

The Global Recombinant Cell Culture Supplements Market size is expected to be worth around US$ 3254.0 Million by 2035 from US$ 917.2 Million in 2025, growing at a CAGR of 13.5% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 46.3% share with a revenue of US$ 424.8 Million.

Increasing demand for consistent, regulatory-compliant, and animal-free raw materials accelerates the Recombinant Cell Culture Supplements market as biopharmaceutical manufacturers and researchers seek chemically defined solutions that enhance reproducibility and safety in cell-based production processes.

Bioprocess engineers increasingly incorporate recombinant growth factors, cytokines, and albumin into serum-free media formulations for mammalian cell lines, optimizing productivity and product quality in monoclonal antibody and recombinant protein manufacturing.

These supplements support stem cell expansion and differentiation protocols in regenerative medicine, providing precise signaling molecules that maintain pluripotency or direct lineage commitment without the variability associated with animal-derived components.

Vaccine developers utilize recombinant insulin and transferrin to sustain high-density cell cultures during viral vector production, ensuring robust yields and compliance with stringent safety standards for human-use products.

In cell therapy manufacturing, recombinant supplements enable controlled expansion of CAR-T cells and mesenchymal stem cells, delivering consistent growth conditions that preserve potency and minimize risk of adventitious agents.

Manufacturers pursue opportunities to develop fully defined, synthetic recombinant supplements that eliminate animal-origin risks and support xeno-free workflows, expanding applications in advanced therapy medicinal products where regulatory authorities prioritize traceability and safety.

These advancements facilitate transition from research-grade to clinical-grade manufacturing, streamlining scale-up for gene-modified cell therapies and organoid-based drug screening platforms.

In February 2026, Bio-Techne introduced a fully defined synthetic solution for 3D stem cell and organoid culture. This animal-free platform addresses growing regulatory expectations for xeno-free bioprocessing and is expected to accelerate adoption in regenerative medicine applications, where consistency and safety of culture conditions are critical.

Recent trends emphasize chemically defined, recombinant alternatives with enhanced stability and bioactivity, positioning the market for sustained growth in safe, scalable, and reproducible cell culture systems essential for next-generation biologics and regenerative therapies.

Key Takeaways

- In 2025, the market generated a revenue of US$ 917.2 Million, with a CAGR of 13.5%, and is expected to reach US$ 3254.0 Million by the year 2035.

- The product type segment is divided into recombinant growth factors, recombinant cytokines, recombinant hormones, recombinant transferrin, recombinant albumin, recombinant protease inhibitors and others, with recombinant growth factors taking the lead with a market share of 34.8%.

- Considering application, the market is divided into biopharmaceutical production, regenerative medicine & stem cell research, cancer research, drug discovery & development, tissue engineering and others. Among these, biopharmaceutical production held a significant share of 42.6%.

- Furthermore, concerning the end user segment, the market is segregated into pharmaceutical & biotechnology companies, CROs & CMOs, academic & research institutes and diagnostic laboratories. The pharmaceutical & biotechnology companies sector stands out as the dominant player, holding the largest revenue share of 58.4% in the market.

- The source segment is divided into E. coli-based expression systems, yeast-based expression systems, mammalian cell-based expression systems, insect cell-based expression systems and plant-based expression systems, with mammalian cell-based expression systems taking the lead with a market share of 45.7%.

- North America led the market by securing a market share of 46.3%.

Product Type Analysis

Recombinant growth factors accounted for 34.8% of growth within product type and dominate the recombinant cell culture supplements market due to their critical role in regulating cell proliferation, differentiation, and survival in culture systems.

Biopharmaceutical production relies heavily on growth factors to maintain optimal cell conditions for protein expression and biologic manufacturing. The segment is expected to expand as biologics and cell-based therapies continue to gain importance in modern medicine.

Growth factors are likely to remain preferred because they enhance yield, consistency, and scalability in production workflows. The segment benefits from increasing demand for serum-free and chemically defined media.

Advancements in recombinant protein engineering are projected to improve functionality and stability. As research shifts toward high-efficiency cell culture systems, recombinant growth factors are estimated to maintain their dominant position in this market.

Application Analysis

Biopharmaceutical production accounted for 42.6% of growth within application and dominates the recombinant cell culture supplements market due to the rapid expansion of biologics, vaccines, and monoclonal antibody manufacturing.

These processes require highly controlled culture environments supported by recombinant supplements to ensure product quality and yield. The segment is expected to grow as global demand for biologic therapies continues to rise across oncology, immunology, and rare diseases.

Pharmaceutical pipelines increasingly include complex biologics, which strengthens reliance on advanced cell culture systems. The segment is likely to benefit from increasing investment in biomanufacturing infrastructure.

As production scalability and efficiency remain critical, biopharmaceutical production is anticipated to retain its dominant position in this market.

End-User Analysis

Pharmaceutical and biotechnology companies accounted for 58.4% of growth within end user and dominate the recombinant cell culture supplements market due to their extensive involvement in drug development and biologics manufacturing. These companies require high-quality supplements to support large-scale cell culture processes and ensure regulatory compliance.

The segment is expected to expand as R&D pipelines grow and demand for biologics increases globally. Companies are likely to invest in advanced culture systems to improve productivity and reduce variability.

The segment benefits from strong funding in drug discovery and innovation. As competition intensifies in biologics development, pharmaceutical and biotechnology companies are estimated to remain the dominant end users in this market.

Source Analysis

Mammalian cell-based expression systems accounted for 45.7% of growth within source and dominate the recombinant cell culture supplements market due to their ability to produce complex proteins with proper folding and post-translational modifications.

Biopharmaceutical products such as monoclonal antibodies and therapeutic proteins depend on mammalian systems for functional accuracy. The segment is expected to grow as demand for high-quality biologics increases.

Mammalian systems are likely to remain preferred because they closely mimic human cellular environments. The segment benefits from advancements in cell line engineering and culture optimization.

As biologic production becomes more sophisticated, mammalian cell-based systems are anticipated to maintain their leading position in this market.

Key Market Segments

By Product Type

- Recombinant Growth Factors

- Recombinant Cytokines

- Recombinant Hormones

- Recombinant Transferrin

- Recombinant Albumin

- Recombinant Protease Inhibitors

- Others

By Application

- Biopharmaceutical Production

- Regenerative Medicine & Stem Cell Research

- Cancer Research

- Drug Discovery & Development

- Tissue Engineering

- Others

By End User

- Pharmaceutical & Biotechnology Companies

- CROs & CMOs

- Academic & Research Institutes

- Diagnostic Laboratories

By Source

- E. coli-Based Expression Systems

- Yeast-Based Expression Systems

- Mammalian Cell-Based Expression Systems

- Insect Cell-Based Expression Systems

- Plant-Based Expression Systems

Drivers

Expansion of biopharmaceutical manufacturing and demand for serum-free media are driving the Recombinant Cell Culture Supplements market.

The biopharmaceutical sector’s rapid growth has increased reliance on defined, animal-component-free supplements to support consistent and scalable cell culture processes. Recombinant supplements such as albumin, insulin, growth factors, and transferrin enable chemically defined media that minimize batch-to-batch variability and contamination risks.

Regulatory emphasis on xeno-free and chemically defined systems for therapeutic protein production further accelerates adoption. North America accounted for a substantial share of related cell culture activities in 2025, supported by robust investments in biologics development.

The recombinant segment within broader cell culture supplements demonstrated a projected CAGR of 11.27% in recent analyses covering the period. Rising production of monoclonal antibodies and recombinant proteins necessitates high-performance supplements that enhance cell viability and productivity.

Contract manufacturing organizations increasingly incorporate these supplements to meet sponsor requirements for reproducible processes. Advancements in recombinant technology have improved the purity and functionality of these components compared to animal-derived alternatives.

These factors collectively sustain elevated demand across research, development, and commercial manufacturing stages. Consequently, biomanufacturing expansion and quality imperatives establish a primary driver for market progression during the 2022–2025 period.

Restraints

Elevated costs of recombinant supplements and scalability challenges are restraining the Recombinant Cell Culture Supplements market.

Production of high-purity recombinant proteins involves complex expression systems, purification, and quality control measures that result in premium pricing relative to traditional supplements.

Many academic and smaller biotechnology entities face budgetary limitations when transitioning from serum-containing to fully defined media. Scale-up of recombinant manufacturing processes requires specialized facilities and expertise, which constrain supply availability during periods of surging demand.

Variability in performance across different cell lines or culture conditions necessitates additional optimization, increasing development timelines and expenses. Limited reimbursement or direct cost recovery for research applications further discourages widespread substitution in cost-sensitive environments.

These economic and technical hurdles slow the replacement rate of established supplements despite recognized advantages in consistency and safety. Resource constraints in emerging regions amplify barriers to adoption of advanced recombinant solutions.

Persistent gaps in cost-effective large-scale production moderate overall penetration rates. As a result, such cost and scalability factors impose measurable restraint on accelerated market growth throughout the 2022–2025 timeframe.

Opportunities

Advancements in chemically defined and animal-free formulations are creating growth opportunities in the Recombinant Cell Culture Supplements market.

Development of next-generation recombinant supplements supports fully chemically defined media that align with stringent regulatory expectations for therapeutic cell products. Opportunities emerge for customized formulations tailored to specific cell types, including stem cells and viral vector production systems.

Integration with automated bioprocessing platforms enables higher throughput and improved process control in commercial facilities. Expansion into regenerative medicine and cell therapy applications broadens the addressable market beyond traditional protein therapeutics.

Partnerships between supplement providers and biomanufacturers facilitate co-development of optimized media systems that enhance yield and reduce downstream processing burdens. Potential exists for modular supplement portfolios that allow flexible adaptation to diverse production scales and modalities.

Alignment with sustainability goals through animal-free sourcing strengthens value propositions for ethically conscious organizations. These innovations foster recurring revenue through consumable usage and support differentiation in competitive bioprocessing segments.

Overall, formulation advancements generate substantial prospects for diversified applications and sustained market development.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical conditions are actively shaping investment flow, cost structures, and supply reliability in the recombinant cell culture supplements market. Strong expansion in biologics, vaccine production, and cell-based therapies is driving consistent demand for high-quality, animal-free supplements that improve reproducibility and regulatory compliance in biomanufacturing.

At the same time, inflation is increasing the cost of recombinant proteins, growth factors, and specialized media inputs, which places financial pressure on research institutions and biopharmaceutical manufacturers.

Currency volatility and global trade uncertainty are complicating procurement of critical raw materials and bioprocessing components sourced across multiple regions. Geopolitical tensions are also affecting cross-border collaboration in biotechnology research and slowing the movement of sensitive biological materials and equipment.

Current US tariffs on imported laboratory equipment, electronic systems, and certain biochemical inputs are raising capital and operational expenditure for production facilities and R&D labs. These cost increases may delay capacity expansion and limit adoption among smaller biotech firms.

However, such trade dynamics are encouraging domestic manufacturing, localized supply chains, and investment in scalable, serum-free technologies. Overall, despite short-term cost and supply challenges, sustained demand for biologics and advanced therapies is expected to support a resilient and progressively expanding market outlook.

Latest Trends

Shift toward chemically defined recombinant supplements and integration with advanced bioprocessing platforms represents a recent trend in the Recombinant Cell Culture Supplements market.

In 2024 and 2025, the industry has observed accelerated transition from serum-containing or animal-derived components to fully recombinant and chemically defined alternatives in cell culture workflows. This progression supports enhanced batch consistency and compliance with quality-by-design principles in biologics manufacturing.

Manufacturers have introduced refined recombinant albumin and growth factor products designed for closed-system and high-density cultures. The trend aligns with broader biopharmaceutical strategies emphasizing risk mitigation and process intensification.

Implementations during this period demonstrate improved cell productivity and reduced variability in monoclonal antibody and vaccine production. Continued focus on scalable, animal-free solutions reflects regulatory and ethical priorities influencing media development.

Prominent activities observed in 2024–2025 underscore a maturing emphasis on defined supplements that facilitate efficient scale-up from research to commercial production. This evolution continues to reshape standards for reliable and reproducible cell culture practices within the sector.

Regional Analysis

North America is leading the Recombinant Cell Culture Supplements Market

North America accounted for 46.3% of the recombinant cell culture supplements market in 2025, supported by the region’s advanced bioprocessing infrastructure and strong demand for animal-free, chemically defined media components in biologics manufacturing.

Biopharmaceutical companies across the United States are transitioning toward recombinant supplements to enhance consistency, reduce contamination risk, and meet stringent regulatory expectations for cell-based production systems.

The U.S. Food and Drug Administration continues to emphasize quality and safety standards in biologic manufacturing, encouraging adoption of well-characterized recombinant inputs in upstream processes. Expansion of monoclonal antibody production, vaccine development, and cell and gene therapy pipelines has increased reliance on high-performance culture systems.

Manufacturers are investing in optimized formulations that improve cell growth, productivity, and scalability in bioreactor environments. Contract development and manufacturing organizations are also adopting recombinant supplements to align with global quality benchmarks and client requirements.

Advances in protein engineering and recombinant expression technologies are enabling development of highly specific growth factors and cytokines. Research institutions are incorporating defined culture systems in experimental models to improve reproducibility. These factors have collectively reinforced strong growth of recombinant cell culture inputs across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to expand steadily over the forecast period as regional biopharmaceutical production and biotechnology research capabilities continue to advance. Countries such as China, India, South Korea, and Singapore are investing in biologics manufacturing and cell-based research to strengthen their position in global pharmaceutical supply chains.

The World Health Organization underscores the importance of high-quality biologic production systems in ensuring safe and effective therapeutic availability worldwide, supporting the transition toward defined and recombinant culture components. Regional manufacturers are adopting advanced cell culture technologies to improve yield and meet international regulatory standards.

Governments are providing incentives and infrastructure support to attract investment in biotechnology and life sciences sectors. Academic and research institutions are expanding work in cell biology, regenerative medicine, and vaccine development.

Local suppliers are introducing cost-efficient recombinant supplements tailored to regional production needs. Partnerships between global and regional firms are facilitating technology transfer and process optimization. These developments are expected to drive sustained adoption of recombinant cell culture supplements across Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Recombinant Cell Culture Supplements Market expand growth by developing chemically defined, animal-free media components, strengthening collaborations with biopharmaceutical manufacturers, and enhancing consistency in large-scale cell culture processes.

Companies invest in recombinant proteins, growth factors, and cytokines that support high-yield cell expansion and improve reproducibility in biologics production. They also focus on regulatory compliance, scalable manufacturing, and supply chain reliability to meet rising demand from vaccine and monoclonal antibody development.

Thermo Fisher Scientific represents a prominent participant in the Recombinant Cell Culture Supplements Market and operates as a U.S.-based life sciences company that develops cell culture media, reagents, and laboratory solutions for research and bioproduction.

The company emphasizes innovation in serum-free and defined culture systems to support advanced cell-based manufacturing. Industry competitors continue to introduce high-purity supplements, expand production capabilities, and strengthen partnerships with biotechnology firms to accelerate adoption and sustain long-term market growth.

Top Key Players

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Danaher Corporation (Cytiva/Pall)

- Lonza Group AG

- Sartorius AG

- Corning Incorporated

- Bio-Techne Corporation

- FUJIFILM Irvine Scientific

- STEMCELL Technologies Inc.

- Akron Biotech

- Cytiva

- Novozymes A/S

Recent Developments

- In March 2026, Merck KGaA announced the acquisition of HUB Organoids, significantly expanding its capabilities in 3D cell culture technologies. This move enables Merck to combine its recombinant supplement portfolio with advanced organoid models, enhancing the predictive accuracy of preclinical drug development and supporting more reliable translational research outcomes.

- In March 2026, Lonza conducted an Outsourced Pharma Capabilities update, highlighting expanded production capacity for mRNA and viral vectors across its global GMP facilities. The company is increasingly leveraging specialized recombinant proteins to support the scalable manufacturing of both autologous and allogeneic cell therapies, reinforcing its role in next-generation biologics production.

- Throughout 2025 and into 2026, Sartorius has intensified its focus on promoting its Recombumin portfolio, a recombinant human albumin product line. Positioned as a high-purity, animal-origin-free stabilizer, it plays a key role in protecting sensitive cell types during cryopreservation and other advanced therapy processes, supporting improved viability and therapeutic outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 917.2 Million |

| Forecast Revenue (2035) | US$ 3254.0 Million |

| CAGR (2026-2035) | 13.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Recombinant Growth Factors, Recombinant Cytokines, Recombinant Hormones, Recombinant Transferrin, Recombinant Albumin, Recombinant Protease Inhibitors and Others), By Application (Biopharmaceutical Production, Regenerative Medicine & Stem Cell Research, Cancer Research, Drug Discovery & Development, Tissue Engineering and Others), By End User (Pharmaceutical & Biotechnology Companies, CROs & CMOs, Academic & Research Institutes and Diagnostic Laboratories), By Source (E. coli-Based Expression Systems, Yeast-Based Expression Systems, Mammalian Cell-Based Expression Systems, Insect Cell-Based Expression Systems and Plant-Based Expression Systems) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Thermo Fisher Scientific Inc., Merck KGaA, Danaher Corporation, Lonza Group AG, Sartorius AG, Corning Incorporated, Bio-Techne Corporation, FUJIFILM Irvine Scientific, STEMCELL Technologies Inc., Akron Biotech, Cytiva, Novozymes A/S. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |