Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Pregelatinized Starch

- By Source Analysis

- By Form Analysis

- By Type Analysis

- By Application Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

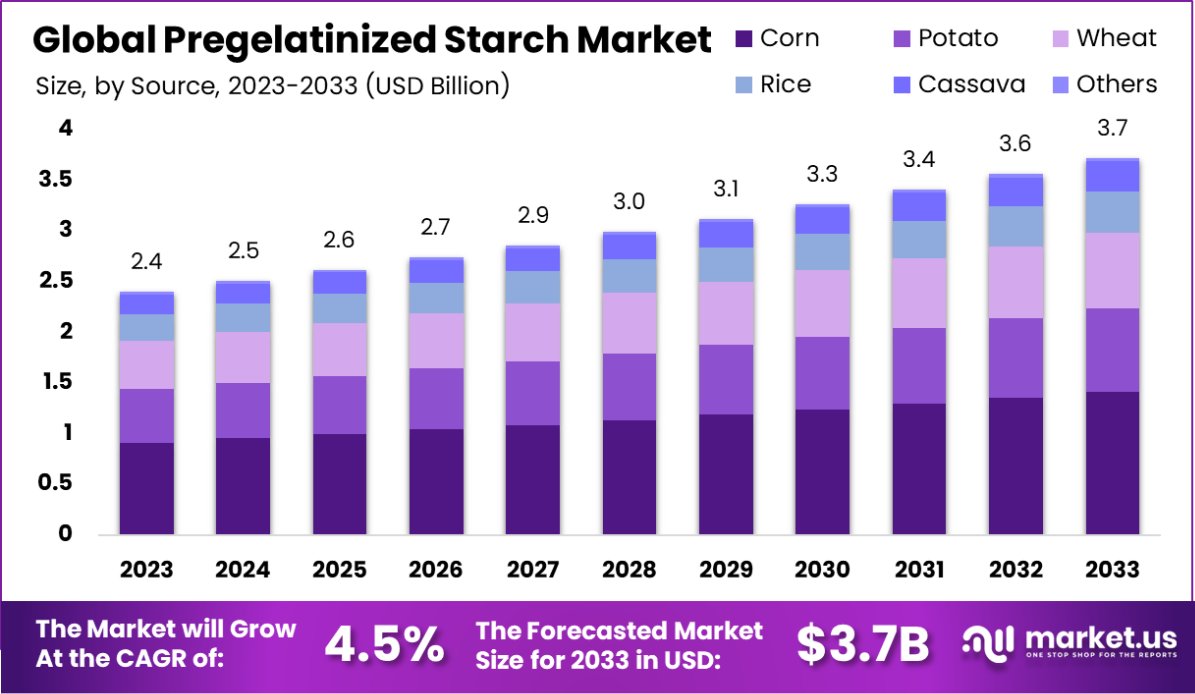

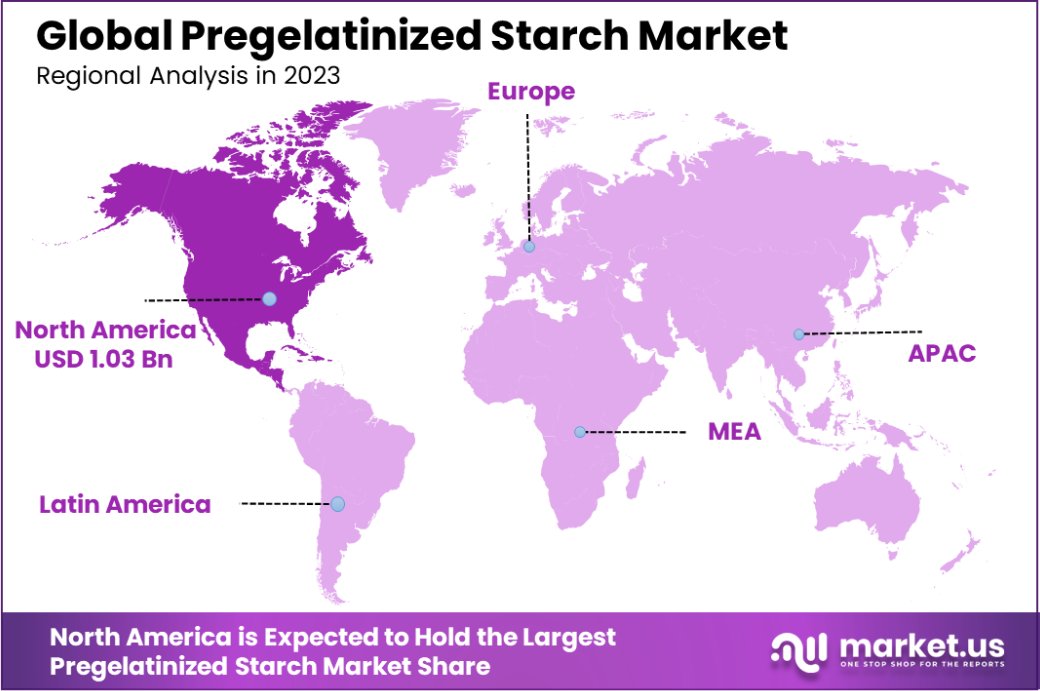

The Global Pregelatinized Starch Market is expected to be worth around USD 3.7 Billion by 2033, up from USD 2.4 Billion in 2023, and grow at a CAGR of 4.5% from 2024 to 2033. In North America, the Pregelatinized Starch Market reached USD 1.03 billion, a 41.6% share.

Pregelatinized starch is a modified starch that has been cooked and then dried, making it soluble in cold water without requiring further heating. This starch is used as a thickening agent in various applications, such as in the food, pharmaceutical, and cosmetic industries.

It is derived from natural sources like corn, potato, or tapioca. Pregelatinized starch is commonly used in ready-to-eat foods, instant soups, sauces, and gravies because it provides convenience by eliminating the need for additional cooking processes.

The pregelatinized starch market is expanding due to its increasing application in the food and beverage sector, where there is a rising demand for convenience foods. As consumers opt for ready-to-eat meals and processed food products, the demand for pregelatinized starch as a thickener and stabilizer has surged.

The pharmaceutical and cosmetics industries are also contributing to market growth due to their use in drug formulations and personal care products.

The growth of the pregelatinized starch market is driven by the increasing demand for processed and convenience foods. Its ability to enhance texture and improve shelf life has boosted its popularity, especially in instant food applications.

Rising consumer preference for convenience foods and ready-to-eat meals, particularly in emerging economies, has increased the demand for pregelatinized starch in food production.

Opportunities lie in expanding applications across pharmaceuticals, where pregelatinized starch is used in tablets and capsules, as well as in the cosmetic sector for lotions and creams, where its thickening properties are valued.

The Pregelatinized Starch Market is poised for steady growth, driven by increasing demand across diverse industries such as food, pharmaceuticals, and cosmetics. As an essential ingredient, pregelatinized starch is valued for its ability to enhance product texture, improve digestibility, and act as a binder and filler in tablet formulations.

With growing applications in pharmaceutical products, where it serves as a filler at concentrations ranging from 5% to 75%, the market is expanding. The increased use of pregelatinized starch in tablet formulations is further supported by its compressibility index, which ranges from 5.9950% to 7.9941%, making it a versatile option for manufacturers.

Key properties, such as a low glass transition temperature of around 39.90°C—significantly lower than the 78.65°C for cross-linked starch—ensure that pregelatinized starch offers superior processing characteristics in temperature-sensitive applications.

Moreover, its higher content of low-branched amylose chains (37.55%) compared to natural starch (27.43%) further enhances its functional properties, making it an attractive choice for formulators seeking improved stability and quality in end products.

As global demand for clean-label and plant-based ingredients continues to rise, the market for pregelatinized starch is expected to benefit from these trends. However, the market will face challenges related to cost fluctuations and supply chain disruptions.

Overall, with its diverse applications and growing adoption, pregelatinized starch is set to remain a key ingredient across various sectors, providing substantial growth opportunities for stakeholders.

Key Takeaways

- The Global Pregelatinized Starch Market is expected to be worth around USD 3.7 Billion by 2033, up from USD 2.4 Billion in 2023, and grow at a CAGR of 4.5% from 2024 to 2033.

- The pregelatinized starch market is dominated by corn, which accounts for 38.2% of the market share.

- The powder form of pregelatinized starch leads the market, holding a significant 59.1% share.

- Modified starch type is the leading category in the market, representing 46.1% of total demand.

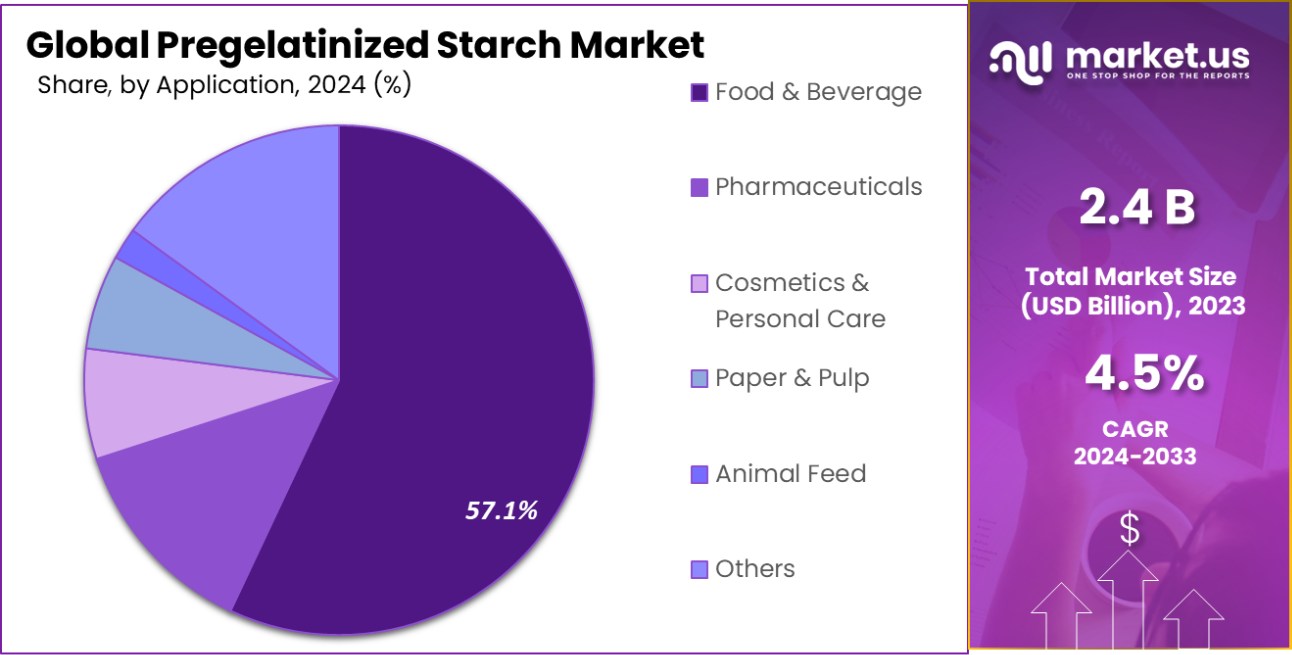

- The food and beverage industry holds the largest share in the pregelatinized starch market, 57.1%.

- Direct sales are the primary distribution channel for pregelatinized starch, contributing 65.1% of total sales.

- In 2023, North America held 41.6% of the Pregelatinized Starch Market, valued at USD 1.03 billion.

Business Benefits of Pregelatinized Starch

Pregelatinized starch offers significant benefits in various applications, contributing to its business appeal, particularly in the pharmaceutical and food industries. As an excipient in drug formulations, pregelatinized starch is utilized for its stability and efficiency-enhancing properties.

It serves as a disintegrant, binder, and filler, which aids in the ease of drug processing and ensures consistent quality and performance in drug delivery. Specifically, it can be included in up to 200 mg in drug formulations under certain regulatory frameworks, indicating its substantial utility in pharmaceutical products.

In food products, pregelatinized starch acts as a stabilizer and thickener, improving the texture and consistency of foods. This adaptation is especially valued for its instant thickening capabilities, which are crucial in products that require cold or minimal preparation times. The versatility of pregelatinized starch under various processing conditions makes it a valuable ingredient in the food industry, enhancing product quality and consumer satisfaction.

Moreover, its role in manufacturing processes, where it simplifies operations and reduces costs, demonstrates its broad utility. The ability to produce pregelatinized starch by cooking and drying methods makes it a critical component in the industrial preparation of food and pharmaceutical products, optimizing texture and solubility which are essential for consumer acceptance and regulatory compliance.

By Source Analysis

The Pregelatinized Starch Market is largely driven by corn, contributing 38.2% of the total market share.

In 2023, Corn held a dominant market position in the “By Source” segment of the Pregelatinized Starch Market, with a 38.2% share. This substantial share underscores corn’s pivotal role in the industry, primarily due to its wide availability and cost-effectiveness as a raw material. Following Corn, Potato captured the second-largest share at 24.5%, appreciated for its functional properties that contribute to food texture and consistency.

Wheat, with a market share of 18.6%, is favored for its gluten content that offers unique viscoelastic properties, essential in bakery applications and meat products. Rice starch, which holds a 10.4% share, is noted for its hypoallergenic qualities and is increasingly preferred in baby food and pharmaceuticals. Lastly, Cassava contributed 8.3% to the market.

Its growth is driven by its use of gluten-free and clean-label products, tapping into the rising consumer demand for healthier and more natural ingredients. Collectively, these sources are shaping the dynamics of the Pregelatinized Starch Market, each offering distinct advantages that cater to diverse industry needs and consumer preferences.

By Form Analysis

Powdered pregelatinized starch holds a dominant position in the market, representing 59.1% of the total form.

In 2023, Powder held a dominant market position in the “By Form” segment of the Pregelatinized Starch Market, with a 59.1% share. This form of pregelatinized starch is highly preferred due to its ease of dispersion and solubility in cold water, which significantly enhances its application in a wide range of products, including instant foods, soups, and sauces. Its ability to provide immediate thickening properties upon contact with water is a key driver behind its substantial market share.

Conversely, Flake form accounted for the remaining 40.9% of the market. Flakes are favored in specific applications where gradual hydration and texturization are required, such as in baked goods and meat products. The flake form’s unique characteristics lend a desirable texture and consistency that powder cannot achieve, making it indispensable in certain culinary and industrial applications.

The pregelatinized starch market, segmented by form into powder and flake, reflects diverse consumer and manufacturing preferences that influence product formulation and innovation. Manufacturers continue to explore these forms to cater to the evolving demands of the food processing industry, where ease of use and functional properties are key determinants of consumer preference.

By Type Analysis

Modified starch accounts for 46.1% of the market share, driving significant demand in various applications.

In 2023, Modified Starch held a dominant market position in the “By Type” segment of the Pregelatinized Starch Market, with a 46.1% share. This leading position is attributed to the enhanced functionality of modified starches, including improved stability under high heat, acid, and shear conditions, making them highly suitable for processed foods that require extended shelf life and stability during cooking.

Modified starches are extensively used in products ranging from bakery goods to sauces and beverages, where texture and viscosity are crucial.

Native Starch followed with a 29.4% share, valued for its minimal processing and natural origin, which appeals to consumers seeking clean-label products. Cross-linked starch, accounting for 14.8% of the market, is preferred in applications requiring high processing tolerance, such as canned foods and frozen food products.

Lastly, Thermally Modified Starch captured a 9.7% market share. This type is increasingly popular in ready-to-eat meals and snack foods due to its ability to enhance texture and water retention without the use of chemicals.

The diversity within the Pregelatinized Starch Market by type showcases the varied applications and preferences in the food industry, driving innovation and adaptation in starch functionalities to meet specific industrial and consumer demands.

By Application Analysis

Food and beverage applications make up 57.1% of the pregelatinized starch market, showing strong consumer demand.

In 2023, Food and Beverage held a dominant market position in the “By Application” segment of the Pregelatinized Starch Market, with a 57.1% share. This sector’s significant market share is driven by the widespread use of pregelatinized starch in various food applications, such as ready-to-eat meals, snacks, and bakery products, where it acts as a thickener, binder, and stabilizer.

Its ability to dissolve quickly in cold water makes it particularly useful in instant food products, enhancing texture and consistency while also reducing preparation time.

Pharmaceuticals accounted for 20.2% of the market, utilizing pregelatinized starch primarily as a disintegrant and binder in tablet formulations. Cosmetics and Personal Care followed with 10.3%, where these starches are used for their absorbency and smooth textures in products like powders and lotions.

Paper and Pulp industries held a 7.4% share, employing starches to improve paper strength and printability. Finally, Animal Feed rounded out the segment with 5%, where pregelatinized starch helps enhance feed quality and palatability for livestock.

Overall, the diverse applications of pregelatinized starch across these sectors underscore its critical role in improving product performance and meeting consumer expectations in multiple industries.

By Distribution Channel Analysis

Direct sales through distribution channels dominate, contributing to 65.1% of the total sales in this market.

In 2023, Direct Sales held a dominant market position in the “By Distribution Channel” segment of the Pregelatinized Starch Market, with a 65.1% share. This distribution channel’s predominance is largely attributed to the bulk purchase behaviors of major industrial buyers, including large food and beverage manufacturers and pharmaceutical companies, who prefer direct transactions to streamline procurement and reduce costs.

Direct sales offer these companies not only cost advantages but also enhanced supply chain control, ensuring product quality and timely delivery.

Indirect Sales accounted for 22.4% of the market. This channel typically involves third-party distributors and wholesalers who cater to smaller manufacturers and regional markets, providing accessibility to pregelatinized starch without the necessity for direct partnerships with producers.

Online Sales, while still developing in this sector, captured 12.5% of the market. The growth in online sales reflects a broader trend towards digitalization, with more companies adopting e-commerce to reach a wider audience, including small to medium enterprises and end-users seeking convenience and competitive pricing.

The segmentation of the pregelatinized starch market by distribution channel highlights the diverse purchasing preferences across different end-user industries, with direct sales leading due to the scale and efficiency demands of large-scale manufacturers.

Key Market Segments

By Source

- Corn

- Potato

- Wheat

- Rice

- Cassava

- Others

By Form

- Flake

- Powder

By Type

- Modified Starch

- Native Starch

- Cross-Linked Starch

- Thermally Modified Starch

By Application

- Food & Beverage

- Pharmaceuticals

- Cosmetics & Personal Care

- Paper & Pulp

- Animal Feed

- Others

By Distribution Channel

- Direct Sales

- Indirect Sales

- Online Sales

Driving Factors

Expanding Convenience Food Sector Fuels Starch Demand

The escalating demand for convenience foods is a primary driver of the pregelatinized starch market. As lifestyles become busier globally, consumers increasingly seek quick and easy meal solutions, such as instant soups, sauces, and ready-to-eat meals, where pregelatinized starch plays a crucial role in texture and stability.

The starch’s ability to dissolve easily and provide immediate thickening is highly valued in these applications, supporting swift preparation without sacrificing quality, which directly influences the growth of this market segment.

Rise in Clean Label and Gluten-Free Products

Consumer preference for clean-label and gluten-free products is significantly impacting the pregelatinized starch market. As awareness of health and wellness grows, more consumers are choosing products with recognizable and natural ingredients.

Pregelatinized starch, especially from sources like corn and potato, is increasingly used as a gluten-free thickening and binding agent in various food products. This shift towards healthier eating habits is propelling the demand for starches that align with consumer desires for both health benefits and transparency in food sourcing and processing.

Technological Advancements in Food Processing

Technological advancements in food processing technology are crucial in driving the growth of the pregelatinized starch market. Innovations in starch modification techniques allow for the development of starches with specific properties tailored to diverse industrial needs, ranging from freeze-thaw stability in frozen foods to high shear resistance in beverages.

These tailored solutions enable manufacturers to improve product performance and meet specific consumer demands, thereby boosting the use of pregelatinized starch across a wide array of applications.

Restraining Factors

Volatility in Raw Material Prices Impacts Production Costs

Fluctuations in raw material prices represent a significant restraining factor for the pregelatinized starch market. Starch is derived from agricultural commodities such as corn, wheat, and potatoes, whose prices can vary due to factors like weather conditions, crop yields, and economic policies.

These fluctuations can lead to inconsistent production costs for manufacturers of pregelatinized starch, making budgeting and pricing strategies more challenging and potentially affecting the profitability and price stability of starch products in the market.

Stringent Regulatory Standards Limit Market Expansion

The pregelatinized starch industry faces stringent regulatory standards that can hinder market growth. These regulations, which vary by region and country, often involve rigorous approval processes for food additives, including starches, to ensure they meet safety and quality standards.

Complying with these regulations can be costly and time-consuming for manufacturers, potentially delaying product launches and limiting the availability of innovative starch solutions in the market, thus restraining market growth.

Competition from Alternative Thickeners and Stabilizers

The availability of alternative thickeners and stabilizers poses a challenge to the pregelatinized starch market. Ingredients such as gum arabic, xanthan gum, and cellulose derivatives are also used for their thickening and stabilizing properties in various food products.

These alternatives, often promoted as having superior or additional functionalities compared to starches, can divert market share from pregelatinized starch, especially in industries that continuously seek innovative and cost-effective ingredient solutions to improve product texture and stability.

Growth Opportunity

Emerging Markets Propel Demand for Processed Food Products

Emerging markets present significant growth opportunities for the pregelatinized starch market. As economies in regions like Asia, Africa, and South America develop, increasing urbanization and rising disposable incomes are driving demand for processed and convenience food products.

This trend creates a robust market for pregelatinized starch, which is essential in enhancing the texture and shelf life of these products. Targeting these growing markets with tailored food solutions that cater to local tastes and preferences can significantly boost market penetration and revenue for starch manufacturers.

Expansion in Pharmaceutical Applications Enhances Market Scope

The pharmaceutical sector offers a lucrative growth avenue for the pregelatinized starch market. As a binder and disintegrant in tablet manufacturing, pregelatinized starch is crucial for ensuring the integrity and controlled release of active pharmaceutical ingredients.

The ongoing expansion of the pharmaceutical industry, driven by increasing healthcare spending and the continuous development of new medications, presents a growing market for specialized starch products designed to meet strict pharmaceutical standards, thereby expanding the market scope for pregelatinized starch.

Technological Innovations in Starch Modification Open New Avenues

Technological innovations in starch modification techniques represent a major growth opportunity for the pregelatinized starch market. By enhancing the functional properties of starch, such as improving its stability under various processing conditions and enhancing its compatibility with different food systems, these innovations allow starch manufacturers to cater to a broader range of applications.

This not only includes traditional food and beverage sectors but also expands into novel uses in nutraceuticals and functional foods, offering manufacturers new markets and increased revenue potential.

Latest Trends

Increasing Use of Organic Sources in Starch Production

One of the latest trends in the pregelatinized starch market is the increasing use of organic sources for starch production. As consumer demand for organic and natural products continues to rise, manufacturers are shifting towards organic corn, potatoes, and other starch-rich crops to meet these preferences.

This shift not only aligns with the global trend towards healthier and more sustainable food production but also allows companies to differentiate their products in a competitive market, catering to the health-conscious consumer who values transparency and sustainability in their food choices.

Growth in Clean Label Starches for Food Transparency

The clean label movement is significantly influencing the pregelatinized starch market, with an increasing number of manufacturers producing clean label starches that are free from artificial chemicals and additives. This trend is driven by consumers’ growing awareness of food ingredients and their health implications, leading to a demand for simpler, more natural ingredient lists. Pregelatinized starches that are marketed as “clean label” can leverage this trend to gain preference among health-conscious consumers, enhancing brand loyalty and market share.

Technological Advancements in Cold Water Swelling Starches

Technological advancements leading to the development of cold water swelling (CWS) pregelatinized starches are a key trend shaping the market. These starches offer enhanced convenience and functionality, as they thicken without the need for heat, which is particularly advantageous in instant food applications such as instant desserts, salad dressings, and ready-to-mix beverages.

The ability of CWS starches to deliver improved textural qualities and process tolerance makes them highly attractive for food manufacturers looking to simplify production processes and meet consumer demands for quick-prep food solutions.

Regional Analysis

In 2023, North America held 41.6% of the Pregelatinized Starch Market, valued at USD 1.03 billion.

The Pregelatinized Starch Market exhibits varied growth dynamics across global regions, with North America leading at a dominating 41.6% market share, translating to USD 1.03 billion. This significant stake is fueled by advanced food processing industries and a robust demand for convenience foods.

Europe follows closely, driven by stringent food safety regulations that encourage the use of clean and modified starches in the food and pharmaceutical industries. The market in Europe is bolstered by its matured food sector and a shift towards gluten-free products.

In Asia Pacific, rapid urbanization and increasing disposable incomes are catalyzing the market’s growth, with expanding applications in processed foods and pharmaceuticals. This region is expected to witness the fastest growth due to its burgeoning middle class and increasing investment in food processing technologies.

The Middle East & Africa, and Latin America are emerging as potential growth areas, driven by evolving food habits and industrial growth. These regions are incorporating more processed foods into diets, boosting demand for functional ingredients like pregelatinized starch.

Overall, the market’s expansion is influenced by regional shifts towards convenient dietary solutions and technological innovations in food processing and formulations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global Pregelatinized Starch market in 2023, a diverse range of key players is driving innovation and competition. Companies like Agrana Beteiligungs-AG, Archer Daniels Midland Company, and Cargill Incorporated lead with substantial market influence due to their expansive geographic footprint and robust product portfolios.

These companies have leveraged their extensive R&D capabilities to introduce innovative and differentiated products that cater to the specific needs of food, pharmaceutical, and industrial applications, maintaining a competitive edge.

Another notable contributor is BENEO GmbH, which specializes in producing high-quality functional ingredients, including pregelatinized starches that align with the growing consumer demand for clean-label and gluten-free products. Their focus on health and nutritional benefits, combined with sustainable practices, positions them favorably in European and global markets.

Emerging players like Coöperatie Koninklijke Avebe U.A. and Emsland Group are also pivotal, with a focus on specialty starches that offer unique properties such as high freeze-thaw stability and excellent texturizing characteristics. Their innovations are particularly aligned with the needs of the frozen food and convenience food sectors, which are experiencing rapid growth.

The Asia-Pacific region, represented by companies like SMS Corporation Co. Ltd. and Manildra Group, is witnessing significant growth due to increasing urbanization and changes in consumer eating habits. These companies are capitalizing on local market dynamics and increasing their investment in production capacity and technological advancements to meet regional demands.

Overall, the competition among these key players is intense, with each striving to enhance its market position through strategic expansions, collaborations, and innovations. This competitive environment is expected to drive further advancements in product functionalities and applications, broadening the market scope and introducing more tailored solutions to meet the evolving demands of end-users across various industries.

Top Key Players in the Market

- Agrana Beteiligungs-AG

- Anil Products Ltd.

- Archr Daniels Midland Company

- Asahi Kasei Corporation

- Banpong Tapioca Flour Industrial Co Ltd.

- BENEO GmbH

- Cargill Incorporated

- Colorchem Industries Limited

- Coöperatie Koninklijke Avebe U.A.

- Crest Cellulose

- DezhouGaoFeng Starch Co. Ltd.

- DFE Pharma

- Emsland Group

- Galam Ltd.

- Grain Processing Corporation

- Ingredion Incorporated

- Interstarch GmbH

- Karandikars Cashell Private Limited

- Kartoffelmelcentralen (KMC) A.m.b.a

- Manildra Group

- Roquette Freres SA

- S A Pharmachem Pvt Ltd.

- Safal Biopolymers Private Limited

- SMS Corporation Co. Ltd.

- Sudzucker Group

- Tate & Lyle PLC

- Tereos Group

- Universal Starch-Chem Allied Ltd

Recent Developments

- In 2023, Coöperatie Koninklijke Avebe U.A. expanded its distribution through a partnership with Brenntag Specialties, starting in Turkey and extending to the Benelux and Nordic regions, aligning with its market expansion strategy in the pregelatinized starch sector.

- In 2023, Coöperatie Koninklijke Avebe U.A. initiated a partnership with Brenntag Specialties to distribute pregelatinized starch, expanding into Turkey, Benelux, and by 2024, into Nordic and Baltic regions. This broadened Avebe’s market presence and streamlined its supply chain.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.4 Billion |

| Forecast Revenue (2033) | USD 3.7 Billion |

| CAGR (2024-2033) | 4.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Corn, Potato, Wheat, Rice, Cassava, Others), By Form (Flake, Powder), By Type (Modified Starch, Native Starch, Cross-Linked Starch, Thermally Modified Starch), By Application (Food and Beverage, Pharmaceuticals, Cosmetics and Personal Care, Paper and Pulp, Animal Feed, Others), By Distribution Channel (Direct Sales, Indirect Sales, Online Sales) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Agrana Beteiligungs-AG, Anil Products Ltd., Archr Daniels Midland Company, Asahi Kasei Corporation, Banpong Tapioca Flour Industrial Co Ltd., BENEO GmbH, Cargill Incorporated, Colorchem Industries Limited, Coöperatie Koninklijke Avebe U.A., Crest Cellulose, DezhouGaoFeng Starch Co. Ltd., DFE Pharma, Emsland Group, Galam Ltd., Grain Processing Corporation, Ingredion Incorporated, Interstarch GmbH, Karandikars Cashell Private Limited, Kartoffelmelcentralen (KMC) A.m.b.a, Manildra Group, Roquette Freres SA, S A Pharmachem Pvt Ltd., Safal Biopolymers Private Limited, SMS Corporation Co. Ltd., Sudzucker Group, Tate & Lyle PLC, Tereos Group, Universal Starch-Chem Allied Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |