Quick Navigation

Report Overview

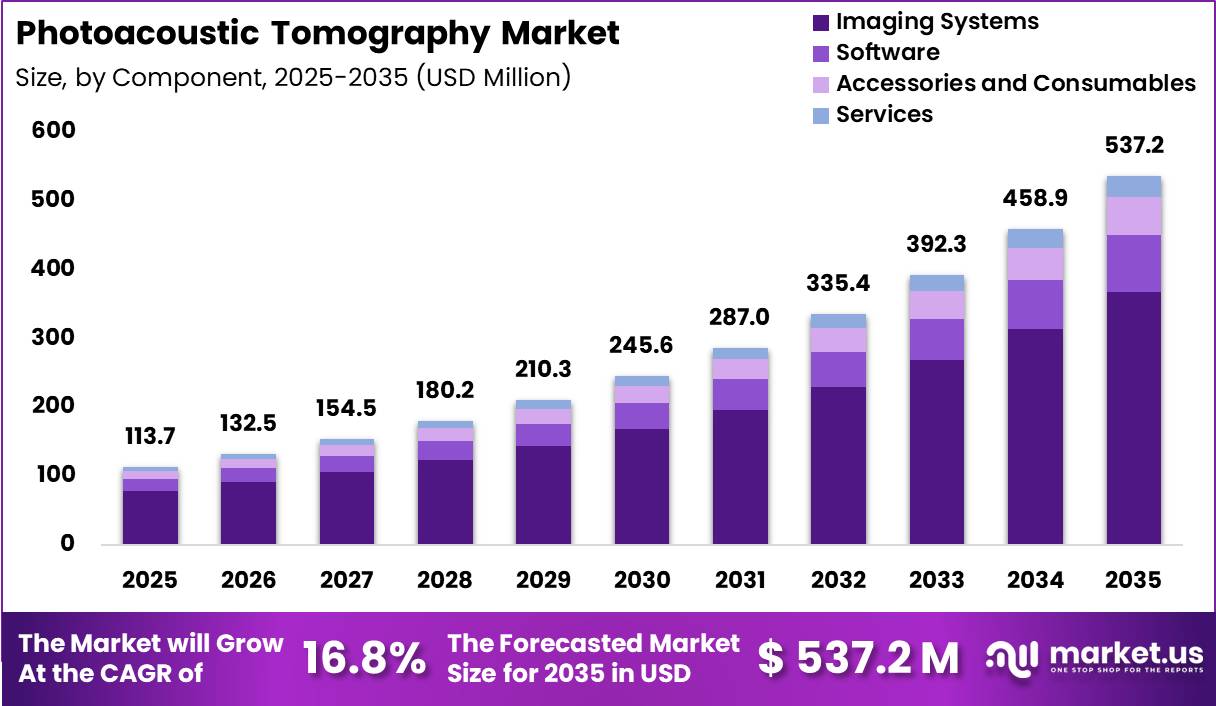

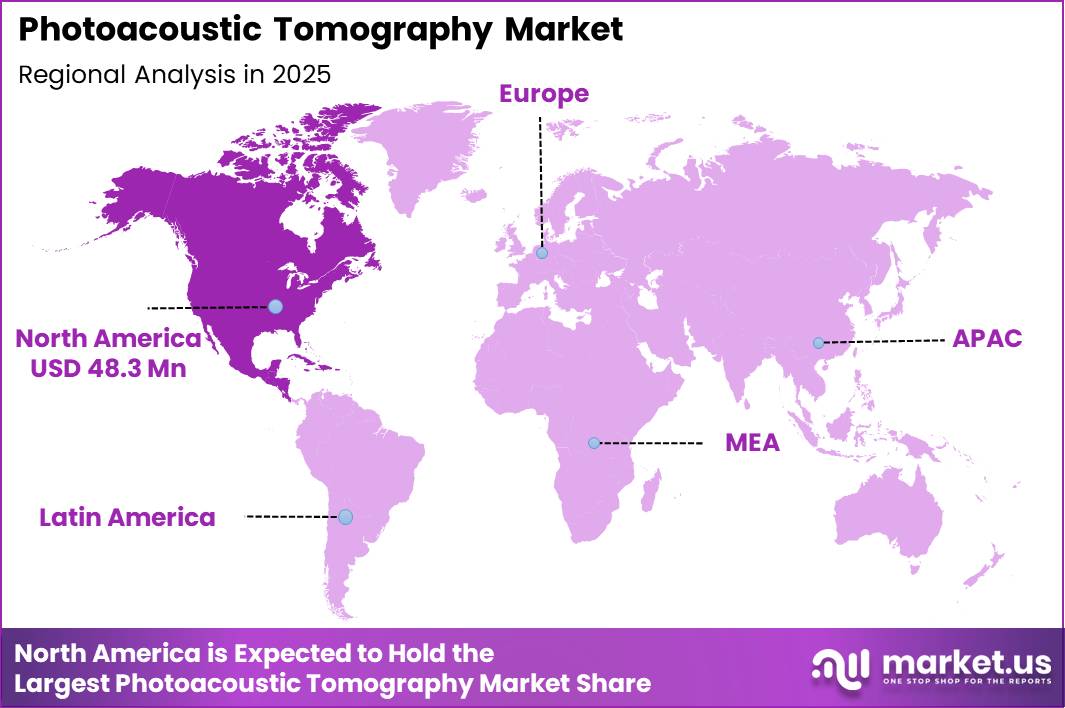

Global Photoacoustic Tomography Market size is expected to be worth around US$ 537.2 Million by 2035 from US$ 113.7 Million in 2025, growing at a CAGR of 16.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 48.3 Million.

Photoacoustic tomography (PAT) is an advanced biomedical imaging technology that combines optical laser excitation with ultrasound detection to generate high-resolution images of biological tissues. The technology enables visualization of tissue composition, blood oxygenation, and vascular structures with greater depth penetration than traditional optical imaging methods.

PAT has emerged as a promising non-invasive diagnostic approach for oncology, cardiology, neurology, and dermatology applications due to its ability to provide both structural and functional imaging without ionizing radiation. According to the U.S. Food and Drug Administration (FDA), ultrasound-based imaging technologies are widely recognized for their safety profile compared with X-ray-based systems, supporting growing clinical interest in photoacoustic imaging platforms.

The increasing burden of chronic diseases is creating demand for advanced diagnostic imaging technologies. According to the World Health Organization (WHO), cancer accounted for approximately 9.7 million deaths globally in 2022, while nearly 20 million new cancer cases were reported worldwide. Breast cancer alone represented 2.3 million new cases in 2022, highlighting the need for early and accurate imaging solutions. PAT is increasingly being evaluated for early tumor detection because it can image blood vessel growth and oxygen saturation associated with malignant tissues.

Research studies supported by the U.S. National Institutes of Health (NIH) indicate that photoacoustic tomography systems can achieve imaging depths of approximately 5–7 centimeters with spatial resolution below 500 micrometers, making them suitable for clinical imaging applications involving soft tissues and vascular networks. Additionally, NIH-funded research has demonstrated the use of PAT in breast cancer screening, melanoma detection, rheumatoid arthritis imaging, and brain functional imaging.

Government healthcare investments are also supporting technology adoption. The National Institutes of Health allocated more than USD 47 billion toward medical research funding in fiscal year 2023, supporting innovation in biomedical imaging technologies and translational diagnostics. Continuous advancements in laser technology, ultrasound transducers, and artificial intelligence-based image reconstruction are expected to further enhance the clinical utility of photoacoustic tomography systems across hospitals and research institutions globally.

Key Takeaways

- Market Size: Global Photoacoustic Tomography Market size is expected to be worth around US$ 537.2 Million by 2035 from US$ 113.7 Million in 2025.

- Market Share: The market growing at a CAGR of 16.8% during the forecast period from 2026 to 2035.

- Component Analysis: Imaging Systems accounted for the largest market share of 68.5% in 2025.

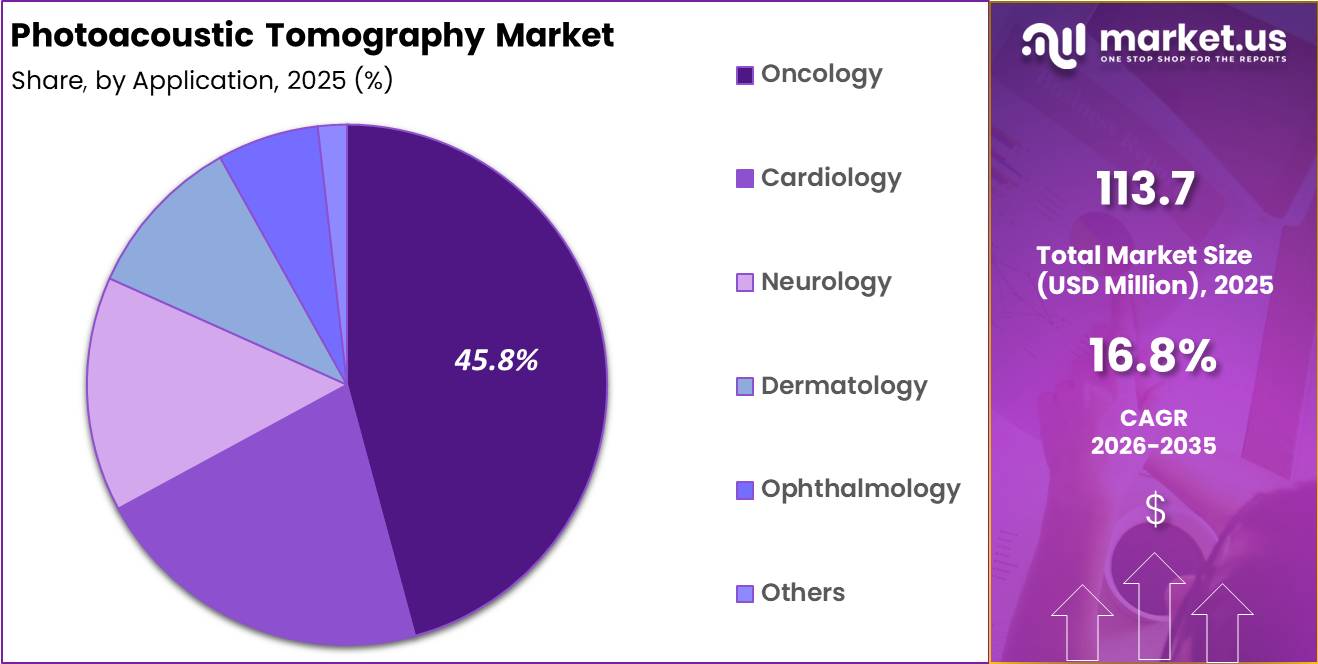

- Application Analysis: Oncology emerged as the leading application segment, accounting for 45.8% of the global market share in 2025.

- End User Analysis: Hospitals and Clinics dominated the market with a 38.6% share in 2025

- Regional Analysis: In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 48.3 Million.

Component Analysis

The component segment of the Photoacoustic Tomography market is categorized into Imaging Systems, Software, Accessories and Consumables, and Services. Among these, Imaging Systems accounted for the largest market share of 68.5% in 2025, primarily driven by the increasing adoption of advanced hybrid imaging technologies in clinical diagnostics and preclinical research.

The dominance of this segment can be attributed to continuous technological advancements in laser-based imaging devices, enhanced image resolution capabilities, and rising demand for non-invasive diagnostic solutions across oncology and cardiovascular applications. In addition, growing investments by healthcare institutions and research organizations in high-performance imaging infrastructure are further supporting segment expansion.

The Software segment is witnessing notable growth due to the increasing integration of artificial intelligence, image reconstruction tools, and data analytics platforms that improve diagnostic accuracy and workflow efficiency. Accessories and Consumables, including transducers, contrast agents, and laser components, continue to generate stable demand owing to repeated usage requirements in imaging procedures.

Meanwhile, the Services segment is expanding steadily, supported by rising demand for equipment maintenance, installation, training, and system upgrades across healthcare and research facilities globally.

Application Analysis

Based on application, the Photoacoustic Tomography market is segmented into Oncology, Cardiology, Neurology, Dermatology, Ophthalmology, and Others. Oncology emerged as the leading application segment, accounting for 45.8% of the global market share in 2025.

The segment’s dominance is primarily attributed to the increasing prevalence of cancer worldwide and the growing demand for early-stage tumor detection and real-time monitoring technologies. Photoacoustic tomography offers superior visualization of tumor vascularity, oxygen saturation, and tissue composition, making it highly suitable for precision oncology and personalized treatment planning.

Cardiology represents a significant growth area due to rising cardiovascular disease incidence and increasing use of photoacoustic imaging for vascular assessment and plaque characterization. In Neurology, the technology is gaining traction for brain imaging and neurovascular mapping applications, particularly in research settings.

Dermatology applications are expanding steadily owing to increasing demand for non-invasive skin imaging and melanoma detection. Ophthalmology is also witnessing growing adoption for retinal and ocular vascular imaging. The Others segment includes applications in immunology, drug discovery, and regenerative medicine, supported by ongoing advancements in biomedical imaging technologies and translational research activities.

End User Analysis

Based on end user, the Photoacoustic Tomography market is segmented into Hospitals and Clinics, Diagnostic Imaging Centers, Research and Academic Institutes, Pharmaceutical and Biotechnology Companies, and Others.

Hospitals and Clinics dominated the market with a 38.6% share in 2025, supported by the growing adoption of advanced diagnostic imaging technologies for cancer detection, cardiovascular assessment, and minimally invasive clinical procedures. The increasing patient volume, rising healthcare expenditure, and expanding integration of precision imaging systems in hospital settings are key factors contributing to segment growth.

Diagnostic Imaging Centers are witnessing substantial demand due to the increasing preference for specialized imaging services and improved accessibility to advanced diagnostic technologies. Research and Academic Institutes represent a prominent segment, driven by extensive investments in biomedical imaging research, preclinical studies, and innovation in molecular imaging techniques.

Pharmaceutical and Biotechnology Companies are increasingly utilizing photoacoustic tomography for drug development, therapeutic monitoring, and translational research applications. The Others segment includes contract research organizations and specialty healthcare facilities, which are gradually adopting photoacoustic imaging systems to enhance diagnostic capabilities and support emerging clinical applications across multiple therapeutic areas.

Key Market Segments

By Component

- Imaging Systems

- Software

- Accessories and Consumables

- Services

By Application

- Oncology

- Cardiology

- Neurology

- Dermatology

- Ophthalmology

- Others

By End User

- Hospitals and Clinics

- Diagnostic Imaging Centers

- Research and Academic Institutes

- Pharmaceutical and Biotechnology Companies

- Others

Driving Factors

The increasing prevalence of cancer and cardiovascular disorders is a major driver for the Photoacoustic Tomography (PAT) market. Healthcare systems are focusing on early-stage diagnosis and non-invasive imaging technologies to improve patient outcomes and reduce treatment costs.

PAT combines optical imaging and ultrasound imaging, enabling high-resolution visualization of tissues without exposing patients to ionizing radiation. This capability is supporting its adoption in oncology, vascular imaging, and functional brain imaging applications.

In addition, the World Health Organization (WHO) estimates that cardiovascular diseases account for approximately 17.9 million deaths annually worldwide. The growing burden of chronic diseases is increasing the demand for advanced imaging technologies capable of providing functional and molecular-level information. Furthermore, the U.S. FDA has increased research activities related to photoacoustic imaging standards and medical imaging technologies, supporting clinical commercialization and regulatory advancement of PAT systems.

Trending Factors

A major trend observed in the Photoacoustic Tomography market is the integration of artificial intelligence (AI), machine learning, and hybrid imaging technologies with photoacoustic systems. Healthcare providers and research institutes are increasingly adopting multimodal imaging platforms that combine PAT with ultrasound, MRI, or fluorescence imaging to improve diagnostic precision and real-time visualization.

The integration of AI algorithms is enhancing image reconstruction, tissue characterization, and automated disease detection capabilities. According to the National Institute of Biomedical Imaging and Bioengineering (NIBIB), current government-supported research programs are emphasizing AI-enabled image enhancement, real-time imaging systems, advanced signal processing, and image-guided surgery applications in photoacoustic technologies.

In addition, the number of AI-enabled medical imaging devices approved by the FDA has continued to rise significantly, reflecting increasing regulatory support for intelligent imaging systems. The adoption of non-ionizing imaging technologies is also increasing because of rising concerns regarding repeated radiation exposure associated with CT imaging.

Furthermore, hybrid photoacoustic-ultrasound systems are gaining clinical interest in breast imaging and vascular diagnostics due to their capability to simultaneously provide anatomical and functional information with improved imaging depth and contrast resolution.

Restraining Factors

High equipment costs and limited clinical standardization remain key restraints affecting the growth of the Photoacoustic Tomography market. PAT systems require advanced laser technologies, high-frequency ultrasound detectors, specialized software platforms, and sophisticated image reconstruction algorithms, significantly increasing overall system costs.

The installation and maintenance expenses associated with these systems are restricting adoption, particularly in small hospitals and healthcare facilities across developing economies. In addition, reimbursement policies for photoacoustic imaging procedures remain limited in several countries because the technology is still in the early commercialization phase. According to the U.S. Food and Drug Administration (FDA), there is still a lack of standardized performance testing methods for emerging photoacoustic imaging systems.

The absence of universal imaging protocols and regulatory harmonization creates challenges for manufacturers during clinical validation and approval processes. Furthermore, healthcare providers continue to rely heavily on established imaging modalities such as MRI, CT, and PET imaging due to their wider availability and clinical familiarity. Training requirements for operating photoacoustic systems and interpreting imaging data also limit rapid clinical adoption. These factors collectively slow the penetration of PAT systems into mainstream diagnostic workflows despite ongoing technological advancements.

Opportunity

The expansion of precision medicine, image-guided surgery, and emerging healthcare infrastructure presents substantial opportunities for the Photoacoustic Tomography market. Governments and healthcare institutions are increasingly investing in advanced diagnostic technologies capable of improving disease monitoring and personalized treatment planning.

PAT technology offers significant opportunities in oncology, dermatology, neurology, and cardiovascular imaging because it enables functional and molecular imaging with high contrast and real-time capabilities. According to the National Institute of Biomedical Imaging and Bioengineering (NIBIB), ongoing federally funded research programs are supporting developments in photoacoustic tomography, endoscopic imaging, intravascular imaging, and image-guided therapeutic monitoring.

Additionally, the increasing use of minimally invasive surgeries is creating demand for intraoperative imaging systems that can precisely identify tumors and vascular structures during surgical procedures. The approval of advanced imaging systems such as the FDA-cleared Imagio Breast Imaging System highlights the growing clinical potential of photoacoustic technologies in breast cancer diagnostics.

Emerging economies across Asia-Pacific and Latin America are also increasing healthcare expenditures and investing in advanced imaging infrastructure. These developments are expected to create long-term commercial opportunities for manufacturers focused on portable, AI-integrated, and cost-efficient photoacoustic tomography systems.

Regional Analysis

In 2025, North America dominated the global Photoacoustic Tomography market, accounting for over 42.5% of the total market share and generating revenue of approximately US$ 48.3 million. The regional market growth is primarily supported by the strong presence of advanced healthcare infrastructure, increasing adoption of non-invasive imaging technologies, and significant investments in biomedical research activities.

The United States remains the key contributor within the region due to rising demand for early disease diagnosis, particularly in oncology, cardiovascular disorders, and neurological imaging applications. Furthermore, the growing integration of artificial intelligence and advanced imaging software into diagnostic systems has accelerated the adoption of photoacoustic tomography technologies across hospitals and research institutions.

The presence of major market players, continuous technological advancements, and favorable government funding for medical imaging research are further strengthening regional market expansion. Academic collaborations and clinical trials associated with precision medicine and molecular imaging are also contributing to the increasing utilization of photoacoustic tomography systems in North America.

In addition, rising healthcare expenditure and growing awareness regarding early-stage disease detection continue to create favorable market conditions. Canada is also witnessing steady growth due to increasing research activities and expanding healthcare modernization initiatives across the country.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The competitive landscape of the Photoacoustic Tomography market is characterized by the presence of established medical imaging companies and emerging technology innovators focused on advancing non-invasive diagnostic solutions. Key players are actively investing in research and development activities to enhance imaging accuracy, portability, and real-time visualization capabilities.

Strategic collaborations with research institutes, hospitals, and biotechnology firms are further supporting technological advancements and commercialization efforts. Companies are also emphasizing product launches and regulatory approvals to strengthen their market position across oncology, cardiology, and preclinical imaging applications. Increasing integration of artificial intelligence and hybrid imaging technologies is enabling manufacturers to improve diagnostic efficiency and expand clinical adoption.

In addition, growing investments in precision medicine and early disease detection are encouraging market participants to develop advanced photoacoustic imaging platforms with higher resolution and deeper tissue penetration. The market remains moderately consolidated, with leading players competing on the basis of innovation, product performance, pricing strategies, and global distribution networks to expand their customer base and revenue share.

Market Key Players

- FUJIFILM VisualSonics Inc.

- iThera Medical GmbH

- Seno Medical Instruments Inc.

- Endra Life Sciences Inc.

- TomoWave Laboratories Inc.

- Advantest Corporation

- Kibero GmbH

- Illumisonics Inc.

- Microphotoacoustics Inc.

- PhotoSound Technologies Inc.

- PreXion Corporation

- Art Photonics GmbH

- OPOTEK LLC

- EKSPLA

- Vibronix Inc.

- Others

Recent Developments

- June 2025 – FUJIFILM VisualSonics Inc. introduced the Vevo F2 LAZR-X20 Photoacoustic Imaging Platform, a next-generation preclinical ultrasound and photoacoustic imaging system designed for advanced tissue characterization and multi-modal imaging applications. The platform expanded the company’s capabilities in oncology, cardiovascular, neurobiology, and molecular imaging research.

- March 2025 – ENDRA Life Sciences Inc. announced an enhanced commercialization strategy for its Thermo-Acoustic Enhanced UltraSound (TAEUS®) platform, with a stronger focus on metabolic disease management and liver health monitoring associated with GLP-1 therapies. The strategic repositioning was aimed at addressing the growing demand for non-invasive liver diagnostics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 113.7 Million |

| Forecast Revenue (2035) | US$ 537.2 Million |

| CAGR (2026-2035) | CAGR of 16.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Imaging Systems, Software, Accessories and Consumables, Services) By Application (Oncology, Cardiology, Neurology, Dermatology, Ophthalmology, Others) By End User (Hospitals and Clinics, Diagnostic Imaging Centers, Research and Academic Institutes, Pharmaceutical and Biotechnology Companies, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | FUJIFILM VisualSonics Inc., iThera Medical GmbH, Seno Medical Instruments Inc., Endra Life Sciences Inc., TomoWave Laboratories Inc., Advantest Corporation, Kibero GmbH, Illumisonics Inc., Microphotoacoustics Inc., PhotoSound Technologies Inc., PreXion Corporation, Art Photonics GmbH, OPOTEK LLC, EKSPLA, Vibronix Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |