Quick Navigation

Report Overview

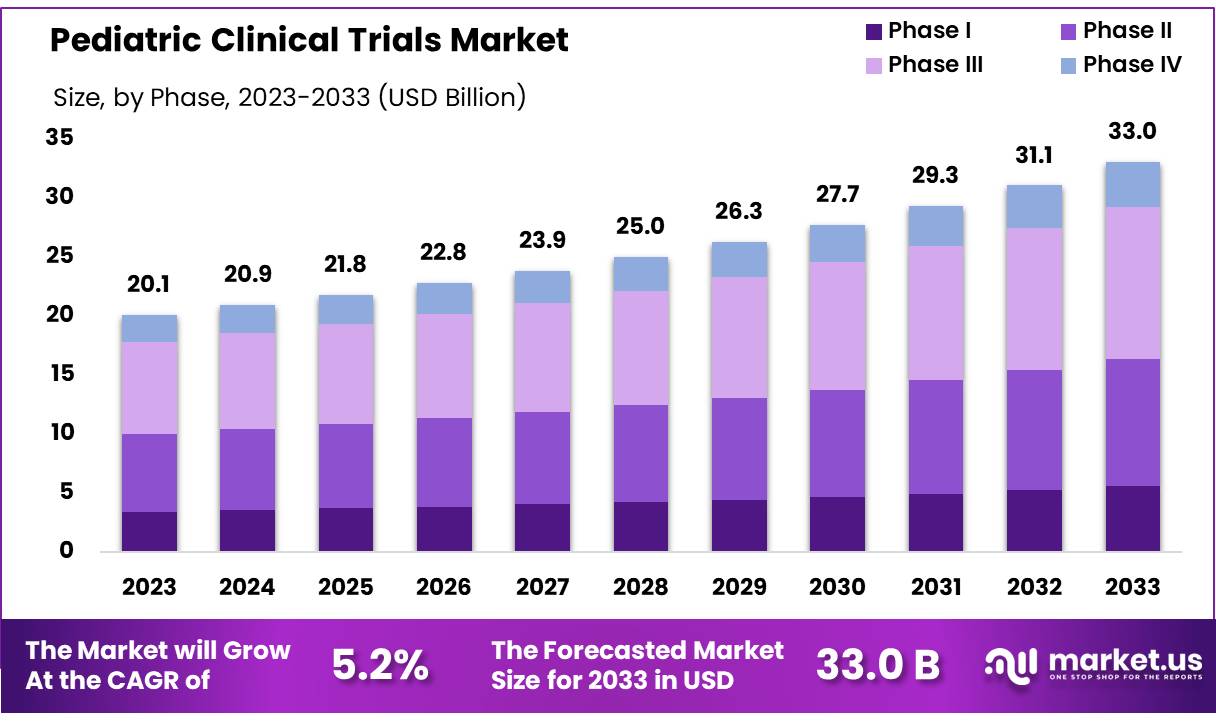

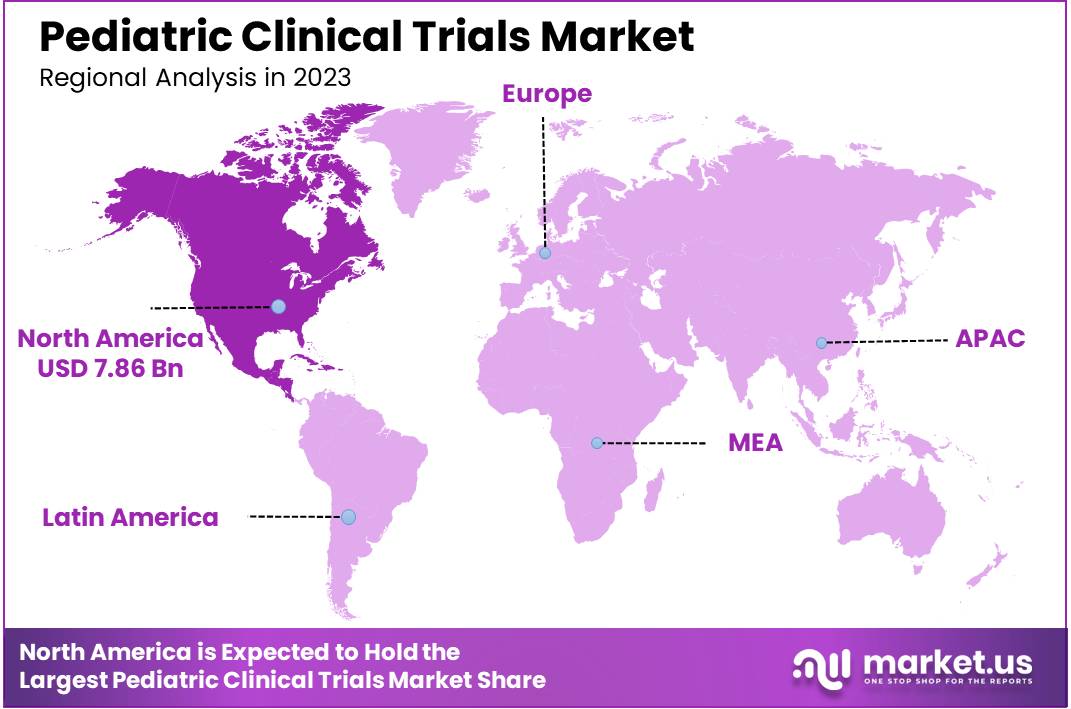

Global Pediatric Clinical Trials Market size is expected to be worth around US$ 33.0 Billion by 2033 from US$ 20.1 Billion in 2023, growing at a CAGR of 5.0% during the forecast period from 2024 to 2033. In 2023, North America led the market, achieving over 39.10% share with a revenue of US$ 7.89 Billion.

The global pediatric clinical trials market is a critical segment of medical research focused on developing safe and effective treatments tailored to children’s unique physiological and developmental needs. In 2023, the market was valued at US$ 20.10 billion, with an anticipated CAGR of 5.2% over the next decade, driven by rising awareness of pediatric-specific treatments, increasing prevalence of chronic and rare pediatric diseases, and advancements in personalized medicine.

- In 2023, approximately 25% of children and adolescents in the United States are impacted by chronic disease.

- As reported by UNICEF in November 2023, pneumonia remains the leading cause of death among children, responsible for over 700,000 fatalities annually in children under the age of five.

- Globally, more than 1,400 cases of pneumonia occur per 100,000 children each year, equating to one case for every 71 children. South Asia records the highest incidence, with 2,500 cases per 100,000 children, followed by West and Central Africa, where the rate is 1,620 cases per 100,000 children.

Regulatory mandates like the FDA’s Pediatric Research Equity Act (PREA) and the EMA’s Pediatric Investigation Plans (PIP) have been instrumental in driving research efforts. The market faces challenges such as ethical concerns, limited recruitment due to smaller patient pools, and the high cost and duration of pediatric studies. Despite these hurdles, innovations in trial design, such as adaptive trials and the integration of digital technologies like remote monitoring, are enhancing the efficiency of pediatric clinical research.

Key Takeaways

- The Pediatric Clinical Trials market generated a revenue of US$ 20.10 Billion and is predicted to reach US$ 33.04 Billion, with a CAGR of 5.2%.

- Based on the Phase, the Phase III segment generated the most revenue for the market with a market share of 38.9%.

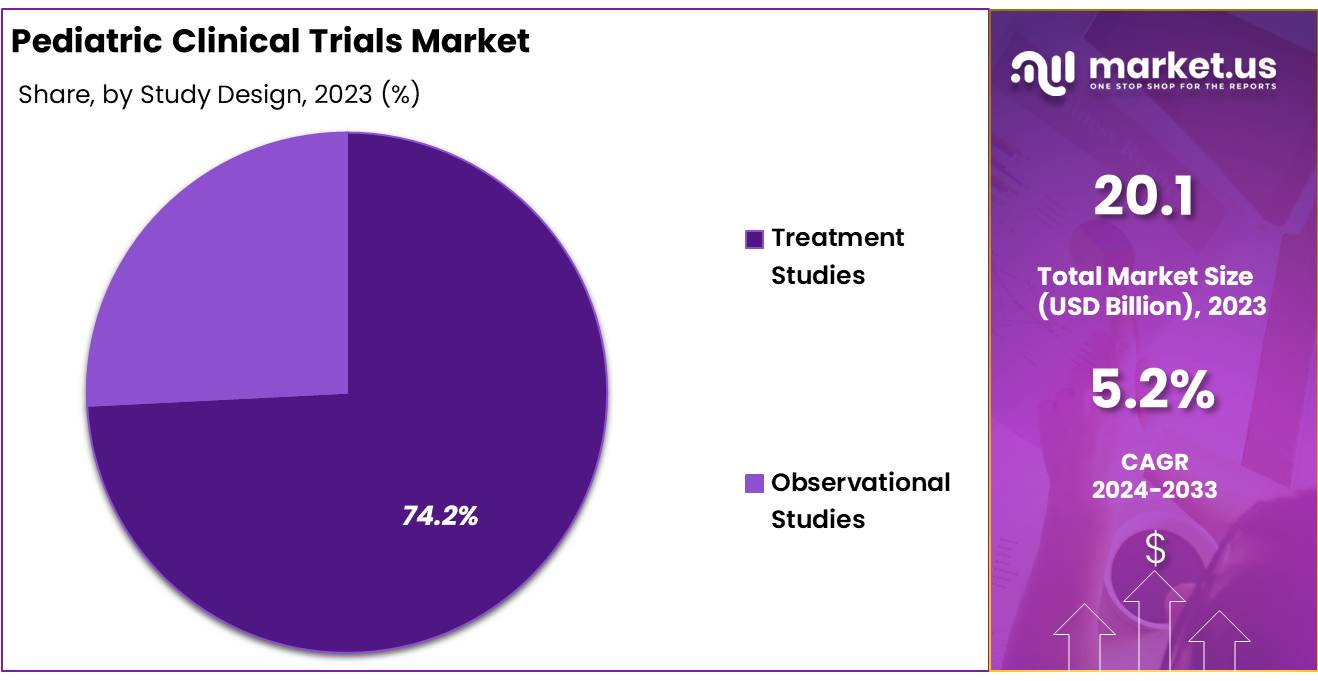

- Based on the study design, the Treatment Studies segment generated the most revenue for the market with a market share of 74.2%.

- By indication, the Infectious Diseases segment contributed the most to the market and secured a market share of 25.2%.

- In terms of sponsor, the industry led the market in 2023, with a market share of 52.7%.

- Region-wise, North America remained the lead contributor to the market, by claiming the highest market share, amounting to 39.10%.

Phase Analysis

In 2023, the Phase III segment dominated the pediatric clinical trials market, capturing 38.9% of the total revenue share. These trials are essential for evaluating therapies on large pediatric populations, ensuring reliable data on dosing, side effects, and efficacy. The increasing focus on targeted therapies for pediatric diseases has driven the growth of Phase III trials, as pharmaceutical companies aim to validate treatments on broader scales for safer and more effective pediatric care.

Looking ahead, the Phase I segment is forecasted to grow at the fastest rate from 2024 to 2033. Early-stage trials are gaining traction for their role in assessing safety, tolerability, and pharmacokinetics in children. Innovations in trial designs, such as adaptive trials, combined with technological advancements, are streamlining the execution of Phase I studies, making them more efficient and widely adopted.

Study Design Analysis

In 2023, the treatment studies segment emerged as the largest contributor to the market. These studies focus on evaluating the safety and effectiveness of therapies designed for pediatric patients, addressing the growing need for specialized treatments for various childhood conditions. Regulatory agencies are actively supporting pediatric-focused research, further fueling the growth of this segment by incentivizing the development of safer, more effective therapies.

From 2024 to 2033, observational studies are anticipated to grow significantly due to their cost-effectiveness and efficiency. These studies typically require fewer resources compared to traditional interventional trials, allowing broader participant inclusion and quicker completion. Additionally, their low-risk approach makes them an ethical and preferred choice for pediatric research, yielding valuable data to inform clinical and regulatory decisions.

Indication Analysis

In 2024, the oncology segment held a leading market share due to the rising prevalence of cancer among children and the demand for more effective treatments. According to a May 2024 report by the American Cancer Society, approximately 9,620 children under the age of 15 in the U.S. are projected to be diagnosed with cancer, with 1,040 fatalities expected. These alarming statistics have prompted pharmaceutical companies to focus on developing targeted therapies tailored to the unique needs of pediatric patients.

The infectious diseases segment is expected to grow rapidly from 2024 to 2033, driven by the increasing prevalence of infectious diseases among children. The urgent need for vaccines and effective treatments for conditions such as respiratory infections, gastrointestinal illnesses, and emerging pathogens has highlighted the importance of pediatric clinical trials in addressing these global health challenges.

Sponsor Analysis

In 2023, the sponsor industry accounted for 52.7% of the global pediatric clinical trials market. Sponsors, including pharmaceutical and biotechnology companies, play a vital role in funding and managing clinical research. These organizations focus on advancing pediatric-specific therapies by investing in trials to evaluate the safety and efficacy of new treatments. Regulatory incentives, such as exclusivity extensions, along with growing demand for targeted pediatric therapies, further bolster this segment’s prominence.

Sponsors are leveraging innovative trial designs, advanced technologies, and partnerships with academic and clinical research institutions to streamline research processes. This approach ensures regulatory compliance while accelerating the development of new treatments, reinforcing the sponsor industry’s dominant position in the market.

Key Market Segments

By Phase

- Phase I

- Phase II

- Phase III

- Phase IV

By Study Design

- Treatment Studies

- Observational Studies

By Indication

- Infectious Diseases

- Oncology

- Autoimmune/inflammation

- Respiratory Disorders

- Mental Health Disorders

- Others

By Sponsor

- Industry

- Government Organizations

- Non-Government Organizations

- Associations

- Others

Drivers

Increasing Prevalence of Pediatric Diseases

The increasing prevalence of pediatric diseases, including cancer, infectious diseases, and respiratory disorders, is driving a greater need for targeted treatments and clinical trials designed specifically for children.

Pediatric cancer, for example, is the second leading cause of death among children globally, with an estimated 400,000 new cases diagnosed each year according to the World Health Organization (WHO). Additionally, respiratory conditions like asthma affect approximately 235 million people worldwide, with children making up a significant portion of this population.

Infectious diseases, particularly those caused by viral infections, continue to be a major health concern for children. The Centers for Disease Control and Prevention (CDC) reports that respiratory infections, such as pneumonia, are among the top causes of death in children under five years old. Moreover, as the pediatric population grows, the need for age-appropriate clinical trials has become more urgent.

Despite the rising incidence of these conditions, children have historically been underrepresented in clinical trials, making it challenging to develop pediatric-specific treatments. According to the National Institutes of Health (NIH), less than 20% of clinical trials include pediatric patients, highlighting the need for more focused research and development in pediatric healthcare. This underscores the importance of enhancing clinical trials and creating treatments tailored to the unique needs of children to address this growing healthcare challenge.

Restrains

High Costs and Longer Durations

Pediatric clinical trials are generally more expensive and time-consuming compared to adult trials due to several factors. One key challenge is the complexity of dosing, as children’s bodies metabolize drugs differently than adults, requiring careful adjustments to ensure both efficacy and safety. This often leads to additional studies and longer trial periods to determine appropriate dosages for different pediatric age groups.

Furthermore, the safety monitoring process is more intricate in pediatric trials, as adverse effects in children can differ significantly from those in adults. The need for specialized pediatric expertise, including pediatricians, clinical pharmacologists, and ethical oversight, adds to the cost and duration of these trials.

In addition, the smaller patient pool for pediatric studies can make recruitment more challenging, lengthening the time required to meet enrollment targets. These factors contribute to the higher costs and extended timelines, making pediatric clinical trials more resource-intensive than adult-focused research.

Opportunities

Targeted Therapies for Rare Pediatric Diseases

The growing focus on developing targeted therapies for rare pediatric diseases presents significant opportunities for companies to innovate and lead in niche therapeutic areas. Rare pediatric conditions, such as genetic disorders, rare cancers, and congenital diseases, often lack effective treatments, creating an urgent need for specialized therapies. As awareness of these unmet needs increases, pharmaceutical and biotechnology companies are dedicating more resources to developing personalized treatments tailored specifically to these conditions.

Targeted therapies, including gene therapies and precision medicines, offer the potential to address the root causes of these rare diseases, offering more effective solutions compared to traditional treatments. As a result, companies that invest in these therapies can position themselves as leaders in the rare pediatric disease market.

Additionally, regulatory incentives such as orphan drug status, fast-tracking approval processes, and extended exclusivity rights further encourage the development of such therapies. This trend not only fills a critical gap in pediatric healthcare but also opens up new revenue streams for companies in a rapidly growing market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a significant impact on the pediatric clinical trials market, influencing both the costs and execution of clinical research. Economic downturns can lead to reduced funding for research, limiting the resources available for pediatric trials, which are already more expensive due to their complexity. Additionally, inflation can drive up costs for materials, labor, and patient recruitment, further straining trial budgets.

Geopolitical factors, such as regulatory changes, trade restrictions, and political instability, can disrupt clinical trial operations across borders, affecting global collaboration and the recruitment of diverse patient populations. For example, regulatory hurdles or delays in different countries may slow down trial timelines, especially when multinational trials are involved.

On the other hand, geopolitical stability and supportive policies in regions like North America and Europe can enhance the growth of pediatric clinical trials by fostering innovation, ensuring regulatory alignment, and facilitating smoother operations. These factors, therefore, shape the market’s dynamics and growth potential.

Latest Trends

The pediatric clinical trials market is evolving with key trends shaping its growth and efficiency. Technological advancements, such as digital health tools, telemedicine, and remote monitoring, are transforming how trials are conducted by improving data collection and patient engagement. Regulatory bodies are increasingly advocating for the inclusion of pediatric populations in clinical research, offering incentives and frameworks that encourage the development of child-specific therapies.

There is also a growing focus on rare pediatric diseases, driven by the need for targeted and innovative therapies, which has opened new opportunities in niche therapeutic areas. Geographically, regions like Asia-Pacific are emerging as hubs for pediatric clinical trials due to their improved research infrastructure, lower costs, and diverse patient pools, making recruitment more feasible.

Additionally, partnerships between pharmaceutical companies, academic institutions, and research organizations are enhancing collaboration, further accelerating the pace of trials. These trends collectively indicate a dynamic future for the market.

Regional Analysis

North America Dominates the Global Pediatric Clinical Trials Market

In 2023, North America led the global pediatric clinical trials market, capturing a 39.10% revenue share. This growth is primarily attributed to the presence of established market players and the increasing number of clinical trials conducted in the region.

Additionally, North America’s robust healthcare infrastructure, featuring advanced research facilities and a well-developed network of hospitals and clinics, supports efficient trial processes and facilitates the recruitment of pediatric participants.

The U.S. market, in particular, is expected to thrive due to significant investments in research and development by both government bodies and private organizations, fostering innovation in pediatric therapies.

Furthermore, growing government support for pediatric clinical trials has encouraged numerous pharmaceutical companies to expand their investments in the country. This combination of factors underscores North America’s dominance in the pediatric clinical trials market and highlights its strong foundation for continued growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The pediatric clinical trials market is characterized by a competitive landscape dominated by both established pharmaceutical companies and emerging biotechnology firms. Key players, including Pfizer, Inc., Johnson & Johnson, Novartis AG, and GlaxoSmithKline plc, hold significant market shares due to their extensive experience in drug development and strong global presence. These companies are investing heavily in research and development to advance pediatric-specific therapies and maintain their market positions.

Additionally, collaborations between pharmaceutical companies, research institutions, and government organizations are becoming more prominent, driving innovation and expanding access to pediatric clinical trials. The market is also witnessing a rise in niche players focusing on rare pediatric diseases, offering targeted therapies and addressing unmet needs.

With North America leading the global market share, regions like Asia-Pacific are emerging as competitive hubs, driven by lower trial costs and diverse patient populations. This dynamic competition continues to shape the market’s growth trajectory.

Top Key Players

- ICON plc

- Syneos Health

- Medpace

- Thermo Fisher Scientific Inc.

- Premier Research

- Laboratory Corporation of America

- QPS Holdings.

- Pfizer Inc.

- The Emmes Company, LLC

- IQVIA Inc.

Recent Developments

- In July 2024, Labcorp announced a collaboration with Naples Comprehensive Healthcare (NCH) in Southwest Florida. This partnership aims to integrate the expertise, technologies, and key capabilities of both organizations to enhance access to laboratory services and improve the delivery of high-quality care.

- In March 2024, Pfizer Inc. received marketing authorization from the European Commission (EC) for PREVENAR 20®, its 20-valent pneumococcal conjugate vaccine. Approved for active immunization in the European Union, the vaccine targets invasive disease, pneumonia, and acute otitis media caused by Streptococcus pneumoniae in infants, children, and adolescents aged 6 weeks to under 18 years.

- In December 2023, Pfizer Inc. and Valneva SE completed participant recruitment for the Phase 3 trial of VLA15, their Lyme disease vaccine candidate. The trial, which includes both adult and pediatric participants, builds on positive Phase 1 and 2 results and focuses on evaluating the efficacy, safety, lot consistency, and immunogenicity of VLA15..

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 20.10 Billion |

| Forecast Revenue (2033) | US$ 33.04 Billion |

| CAGR (2024-2033) | 5.2 |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Phase -Phase I, Phase II, Phase III and Phase IV, By Study Design -Treatment Studies and Observational Studies, By Indication – Infectious Diseases, Oncology, Autoimmune/inflammation, Respiratory Disorders, Mental Health Disorders and Others, By Sponsor- Industry, Government Organizations, Non-Government Organizations, Associations and Others. |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ICON plc, Syneos Health, Medpace, Thermo Fisher Scientific Inc., Premier Research, Laboratory Corporation of America, QPS Holdings., Pfizer Inc., The Emmes Company, LLC and IQVIA Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |