Quick Navigation

Report Overview

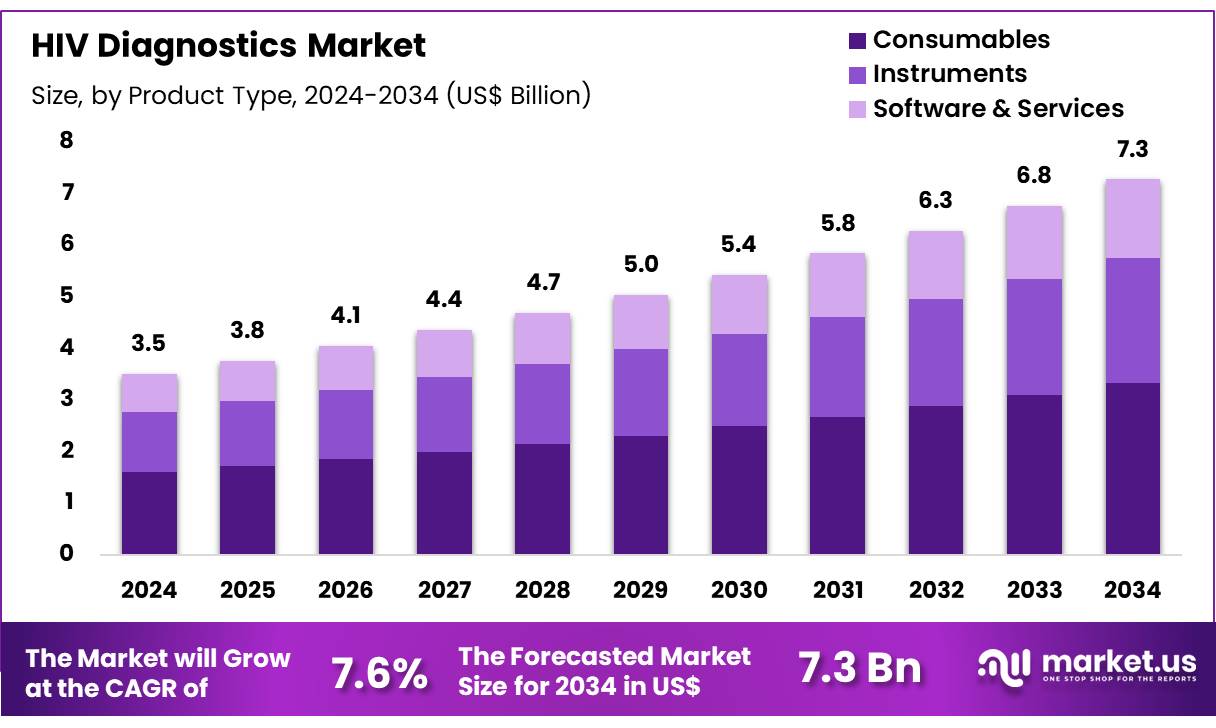

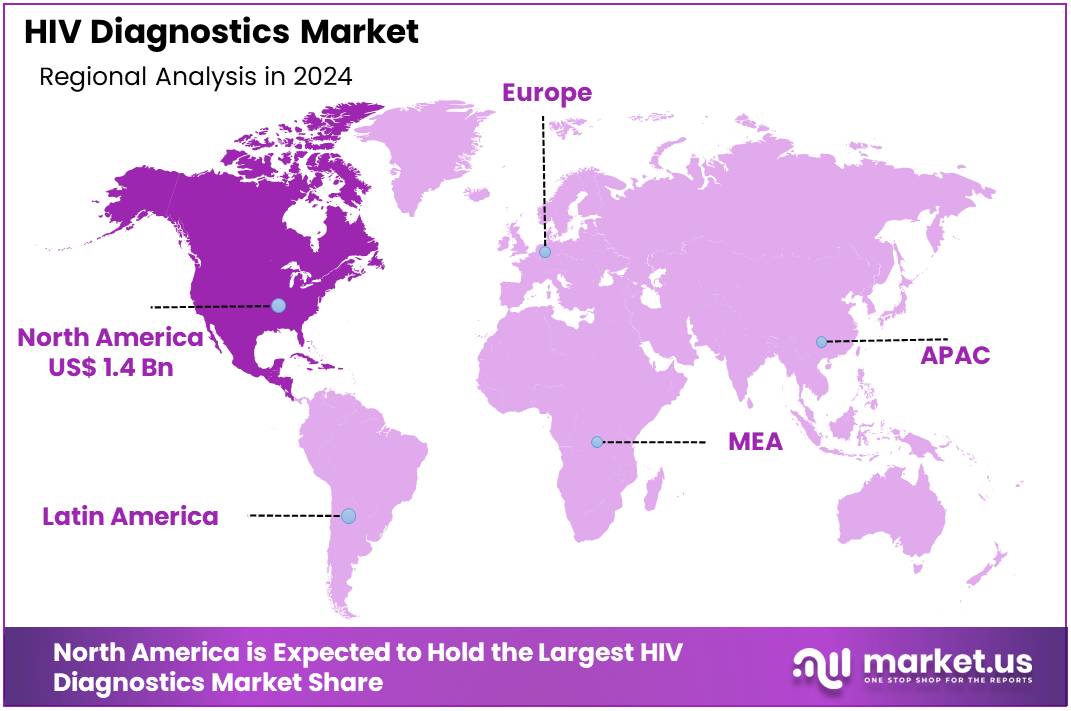

Global HIV Diagnostics Market size is expected to be worth around US$ 7.3 billion by 2034 from US$ 3.5 billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.6% share with a revenue of US$ 1.4 Billion.

Growing awareness of the importance of early HIV detection and the rising focus on preventive healthcare are driving the expansion of the HIV diagnostics market. HIV diagnostics play a critical role in the early identification of the virus, enabling timely interventions and improving patient outcomes. The market is seeing significant demand for innovative diagnostic tools, including rapid tests, nucleic acid tests (NAT), and self-testing kits, which provide quick and accurate results.

The increasing availability of home-based HIV testing solutions has empowered individuals to take control of their health, making early diagnosis more accessible. In May 2022, Amref Health Africa-Tanzania introduced the ‘Afya Kamilifu’ project in the Mara Region, which facilitated the distribution of HIV self-test kits across health centers, promoting early detection and prevention.

The growing trend of self-testing, supported by organizations like the Centers for Disease Control and Prevention (CDC), has opened up new opportunities for market growth. Additionally, advancements in point-of-care (POC) testing technologies and molecular diagnostics have significantly improved the speed, accuracy, and convenience of HIV testing, further driving adoption.

Increasing government and NGO initiatives to improve HIV testing coverage and reduce the stigma associated with HIV testing continue to create opportunities for expanding market reach. As treatment regimens become more effective and accessible, the demand for HIV diagnostics that support early detection and continuous monitoring will continue to drive market growth.

Key Takeaways

- In 2024, the market for HIV diagnostics generated a revenue of US$ 5 billion, with a CAGR of 7.6%, and is expected to reach US$ 7.3 billion by the year 2034.

- The product type segment is divided into instruments, consumables, and software & services, with consumables taking the lead in 2024 with a market share of 45.8%.

- Considering test type, the market is divided into viral load tests, antibody tests, CD4 tests, early infant diagnosis, and viral identification. Among these, antibody tests held a significant share of 38.6%.

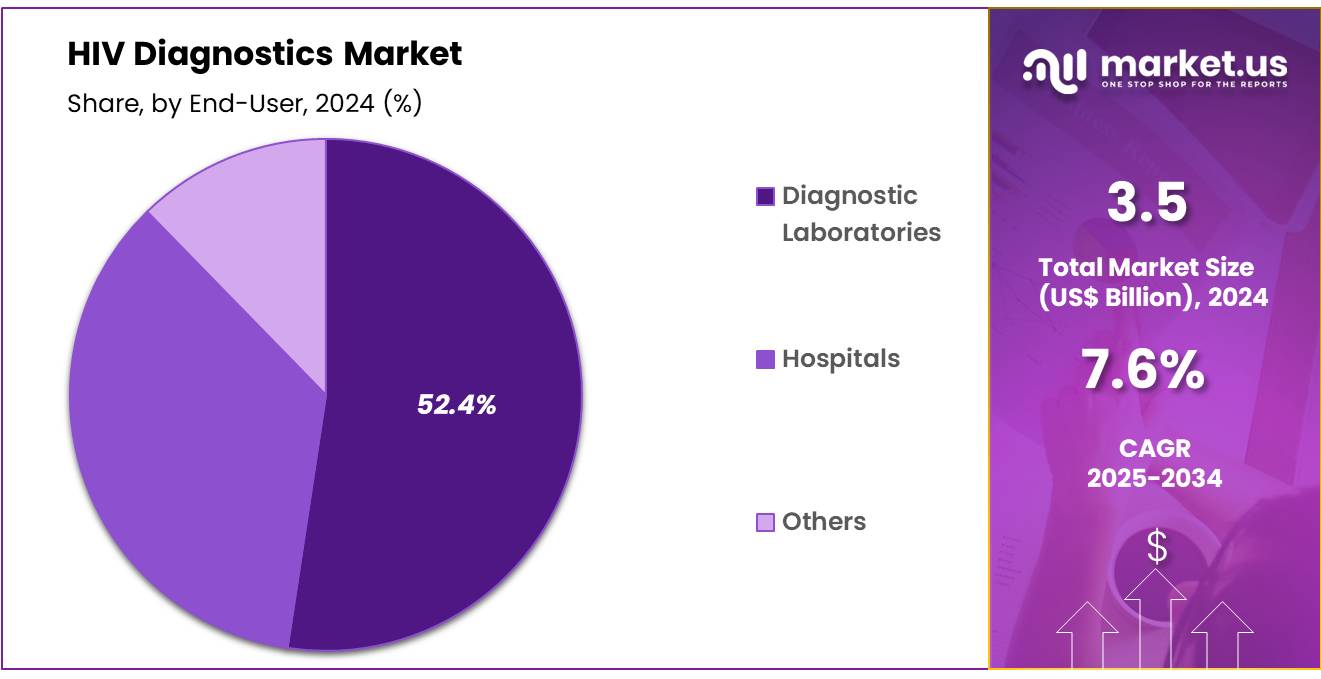

- Furthermore, concerning the end-user segment, the market is segregated into diagnostic laboratories, hospitals, and others. The diagnostic laboratories sector stands out as the dominant player, holding the largest revenue share of 52.4% in the HIV diagnostics market.

- North America led the market by securing a market share of 39.6% in 2024.

Product Type Analysis

The consumables segment led in 2024, claiming a market share of 45.8% owing to the increasing demand for accurate, reliable, and efficient diagnostic tools. Consumables such as test kits, reagents, and sample collection materials are anticipated to experience higher adoption as the need for rapid HIV testing rises. The growing number of HIV screening programs, especially in low- and middle-income countries, is likely to drive demand for consumables due to their essential role in the diagnostic process.

Furthermore, advancements in consumables, such as improvements in sensitivity, stability, and ease of use, are projected to make HIV diagnostics more accessible, contributing to the growth of this segment. The rising awareness of the importance of early detection and regular monitoring of HIV is expected to further accelerate market growth, making consumables a key driver in the HIV diagnostics market.

Test Type Analysis

The antibody tests held a significant share of 38.6% due to their widespread use in diagnosing HIV infections and monitoring treatment progress. Antibody tests, which detect the presence of HIV-specific antibodies in blood or oral fluid, are expected to remain a cornerstone of HIV diagnostics due to their high sensitivity, affordability, and ease of use. The growing focus on early diagnosis and the increasing implementation of routine HIV screening in various healthcare settings, such as hospitals, clinics, and mobile testing units, are projected to drive the demand for antibody tests.

Additionally, the rising availability of point-of-care antibody tests, which provide rapid results, is likely to contribute to the growth of this segment. As global efforts to combat HIV continue, the demand for reliable and accessible diagnostic tools, particularly antibody tests, is expected to increase, further driving market expansion.

End-user Analysis

The diagnostic laboratories segment had a tremendous growth rate, with a revenue share of 52.4% owing to the increasing demand for accurate and timely HIV testing. Diagnostic laboratories play a central role in diagnosing HIV infections, performing confirmatory tests, and monitoring patients’ viral loads and immune function. As the incidence of HIV increases in various regions, and as healthcare systems focus on early diagnosis and treatment, diagnostic laboratories are likely to see rising demand for HIV testing services.

The growing adoption of advanced diagnostic technologies, such as PCR-based viral load tests and integrated testing platforms, is expected to further accelerate the demand for diagnostic services. Additionally, as the need for specialized HIV monitoring in clinical settings grows, diagnostic laboratories will continue to be essential in providing comprehensive HIV diagnostic and monitoring solutions, contributing to the overall growth of this segment in the HIV diagnostics market.

Key Market Segments

Product Type

- Instruments

- Consumables

- Software & Services

Test Type

- Viral Load Tests

- Antibody Tests

- CD4 Tests

- Early Infant Diagnosis

- Viral Identification

End-user

- Diagnostic Laboratories

- Hospitals

- Others

Drivers

Growing Prevalence of HIV Driving the HIV Diagnostics Market

Growing prevalence of HIV is anticipated to drive the HIV diagnostics market significantly. According to the World Health Organization, by the end of 2021, approximately 38.4 million individuals globally were living with HIV, with two-thirds of these cases concentrated in the African region. This disproportionate burden emphasizes the urgent need for accessible and reliable diagnostic tools in high-prevalence areas. Healthcare providers increasingly prioritize early and accurate HIV testing to reduce transmission rates and initiate timely treatment.

Advances in diagnostic technologies, such as point-of-care tests and rapid diagnostic kits, enhance detection capabilities, especially in resource-constrained settings. Public health campaigns emphasizing the importance of routine testing drive adoption among at-risk populations. Governments and non-profit organizations expand funding for HIV diagnostic programs to support underserved regions. Collaborations between diagnostic manufacturers and healthcare providers ensure broader access to innovative solutions.

Expanding research into fourth-generation assays and molecular diagnostics enhances test sensitivity and specificity. Integration of HIV diagnostics into antenatal care programs improves maternal and child health outcomes. These trends highlight the critical role of advanced diagnostic tools in addressing the global HIV burden effectively.

Restraints

High Costs Are Restraining the HIV Diagnostics Market

High costs associated with HIV diagnostics are restraining the market. Advanced testing technologies, such as nucleic acid tests and fourth-generation assays, require significant investment, making them expensive for widespread adoption in low-income regions. Laboratories face additional expenses for maintaining equipment and procuring reagents and consumables. Limited healthcare budgets in resource-constrained settings restrict the availability of comprehensive diagnostic services.

Inconsistent insurance coverage for advanced testing discourages individuals from seeking regular screenings. The high cost of training personnel to operate sophisticated diagnostic tools further increases operational expenses for healthcare providers. Inadequate reimbursement policies for HIV diagnostics in certain regions limit market penetration. Addressing these challenges requires the development of cost-effective diagnostic solutions and increased funding support to improve access to testing in underserved areas.

Opportunities

Increasing Blood Donations as an Opportunity for the HIV Diagnostics Market

Increasing blood donations present a significant opportunity for the HIV diagnostics market. The World Health Organization reported in June 2023 that approximately 118.5 million blood donations are collected globally each year. High-income countries account for 40% of these donations, while low-income regions contribute only 16%, reflecting disparities in healthcare infrastructure. Rising demand for safe blood transfusion practices drives the adoption of HIV testing as part of mandatory screening protocols. Blood banks and transfusion centers increasingly integrate advanced diagnostics to ensure donor blood safety.

Public health initiatives emphasizing voluntary blood donation enhance the availability of samples for testing and improve detection rates. Governments and healthcare organizations invest in upgrading diagnostic facilities to support large-scale screening efforts. Innovations in rapid diagnostic kits and point-of-care testing improve testing efficiency in blood donation centers. Expanding awareness about the importance of HIV screening in transfusion safety strengthens market growth. These trends position rising blood donations as a critical factor in advancing HIV diagnostics globally.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the HIV diagnostics market. On the positive side, increased global healthcare investments and growing awareness of HIV prevention and treatment drive demand for innovative diagnostic solutions. The rise in international aid for healthcare initiatives, particularly in low- and middle-income countries, enhances access to HIV testing technologies.

However, economic recessions can lead to budget cuts, potentially limiting the expansion of HIV testing programs, particularly in underfunded regions. Geopolitical issues, such as political instability and trade restrictions, may disrupt the supply chain for diagnostic tools and reagents, raising costs and impacting availability.

Additionally, differing regulatory frameworks across countries can complicate market access and slow product approval. Despite these challenges, the increasing global focus on universal health coverage and HIV prevention initiatives ensures a continued demand for advanced diagnostic tools, supporting long-term growth in the market.

Latest Trends

Introduction of Novel Testing Kits Driving the HIV Diagnostics Market

Rising introduction of novel testing kits is significantly driving the HIV diagnostics market. High advancements in testing technologies, such as rapid and point-of-care diagnostic kits, are expected to increase accessibility and convenience for users, particularly in remote or resource-limited areas. The growing need for early detection and timely intervention in HIV treatment is likely to further expand market demand.

In February 2023, Mylab Discovery Solutions, an Indian-based laboratory, introduced rapid testing kits for the early detection of sexually transmitted infections, including HCV, HIV, and Syphilis. This launch aims to enhance accessibility and speed in STI diagnosis, supporting early intervention and treatment. As novel testing kits continue to be developed, the HIV diagnostics market is expected to experience significant growth, improving health outcomes and ensuring broader global access to diagnostic services.

Regional Analysis

North America is leading the HIV Diagnostics Market

North America dominated the market with the highest revenue share of 39.6% owing to advancements in diagnostic technologies, increased awareness about early detection, and ongoing efforts to reduce transmission rates. The growing focus on HIV prevention, coupled with the continued push for routine testing in high-risk populations, has bolstered demand for reliable and accessible diagnostic tools.

The introduction of rapid, point-of-care HIV tests, which offer quick and accurate results, has contributed significantly to the market’s expansion. Additionally, partnerships like Roche’s collaboration with The Global Fund, through its Global Access Program, have enhanced HIV diagnosis in resource-limited settings by addressing critical infrastructure challenges.

This partnership has aimed to strengthen healthcare systems, build local capacity for diagnostic testing, and improve healthcare waste management, all of which support the broader efforts to control the HIV epidemic. The increased availability of these diagnostic solutions, coupled with expanded access to healthcare, has played a key role in the continued growth of the HIV diagnostics market in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rising prevalence of HIV, increasing healthcare access, and advancements in diagnostic technologies. Countries like India, China, and Thailand, which are heavily impacted by the HIV epidemic, are anticipated to see increased demand for HIV diagnostic solutions. As reported by The Indian Express in August 2022, approximately 24.01 lakh individuals in India are living with HIV, highlighting the significant public health challenge posed by the disease in the country.

The government’s focus on expanding access to HIV testing and treatment, along with rising awareness campaigns about early detection, is likely to drive market growth. The increasing availability of rapid diagnostic tests and the implementation of HIV screening programs in high-risk populations will further boost the demand for HIV diagnostics. As healthcare infrastructure continues to improve and public awareness increases, the market for HIV diagnostics in Asia Pacific is expected to expand, contributing to better HIV management and prevention in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the HIV diagnostics market focus on developing rapid and highly sensitive tests to enable early detection and timely treatment initiation. Companies invest in R&D to innovate point-of-care solutions and molecular diagnostics, improving accessibility in resource-limited settings. Collaborations with healthcare organizations and governments help expand awareness and testing programs globally.

Geographic expansion into regions with high disease prevalence and increasing healthcare investments drives market penetration. Many players also emphasize affordability and compliance with international guidelines to ensure widespread adoption and reliability.

Abbott Laboratories is a leading company in this market, offering advanced HIV diagnostic solutions such as the ARCHITECT and Alinity platforms. The company focuses on combining cutting-edge technology with ease of use to deliver precise and reliable results. Abbott’s global presence and commitment to improving public health solidify its leadership in the diagnostics sector.

Top Key Players

- Abbott

- Aurobindo Pharma Ltd

- BD

- Bristol-Myers Squibb Company

- INVEX Health

- Janssen Global Services, LLC

- VIIV Healthcare

Recent Developments

- In June 2023, INVEX Health announced the development of an innovative Oral Fluid-Based HIV Self-Test, which is currently undergoing validation in India. Additionally, the company expanded its therapeutic portfolio by acquiring global licensing rights for a patented product targeting Psoriasis, demonstrating its commitment to advancing healthcare solutions.

- In August 2022, Aurobindo Pharma Ltd launched a triple-combination HIV medication specifically formulated for children living with HIV/AIDS in low- and middle-income countries. This initiative aims to improve access to life-saving treatments for pediatric HIV patients in underserved regions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.5 billion |

| Forecast Revenue (2034) | US$ 7.3 billion |

| CAGR (2025-2034) | 7.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Instruments, Consumables, and Software & Services), Test Type (Viral Load Tests, Antibody Tests, CD4 Tests, Early Infant Diagnosis, and Viral Identification), End-user (Diagnostic Laboratories, Hospitals, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Abbott, Aurobindo Pharma Ltd, BD, Bristol-Myers Squibb Company, INVEX Health, Janssen Global Services, LLC, VIIV Healthcare. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |