Global Photoacoustic Imaging Market By Product (Photoacoustic Tomography (PAT) and Photoacoustic Microscopy (PAM)), By Imaging Type (Pre-Clinical and Clinical), By Application (Oncology, Cardiology, Angiology, Histology and Interventional Radiology), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181857

- Number of Pages: 281

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

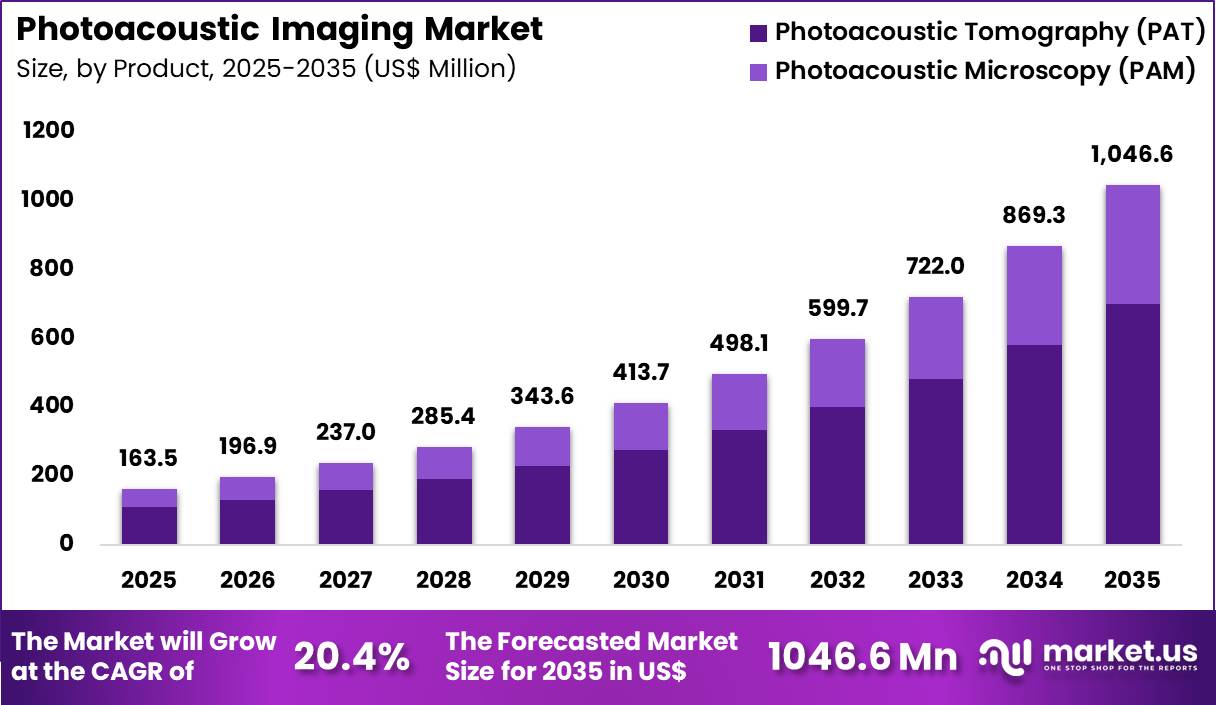

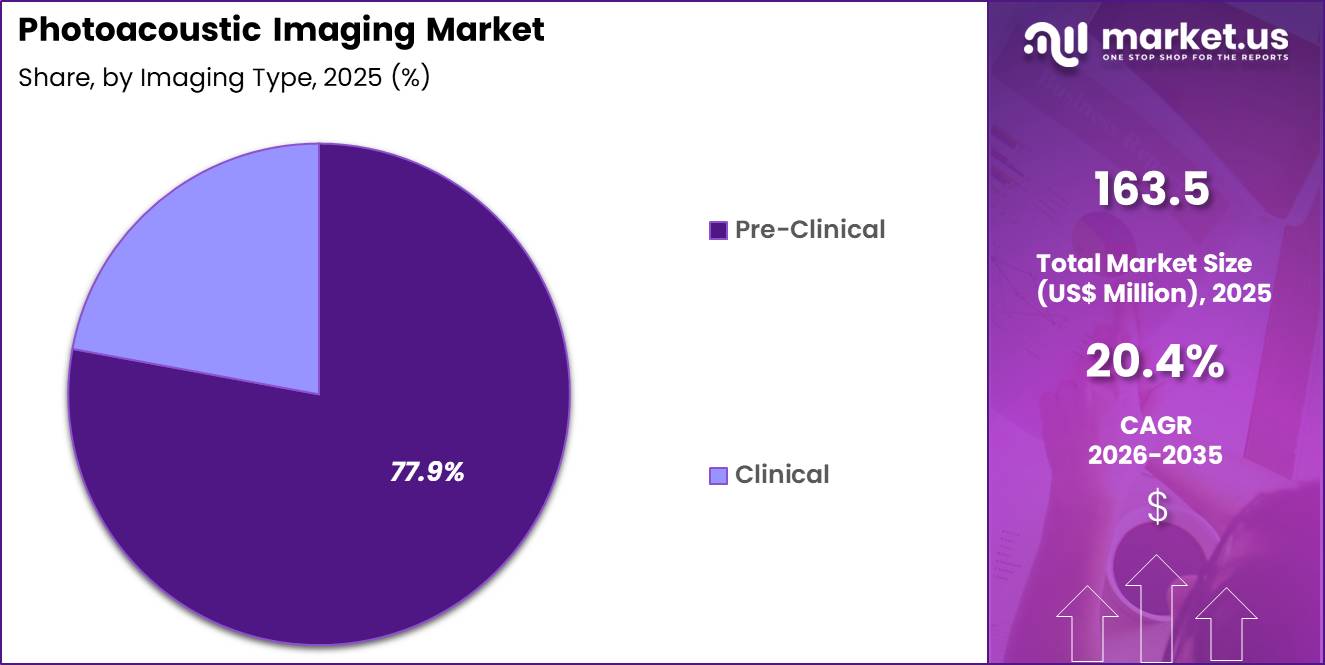

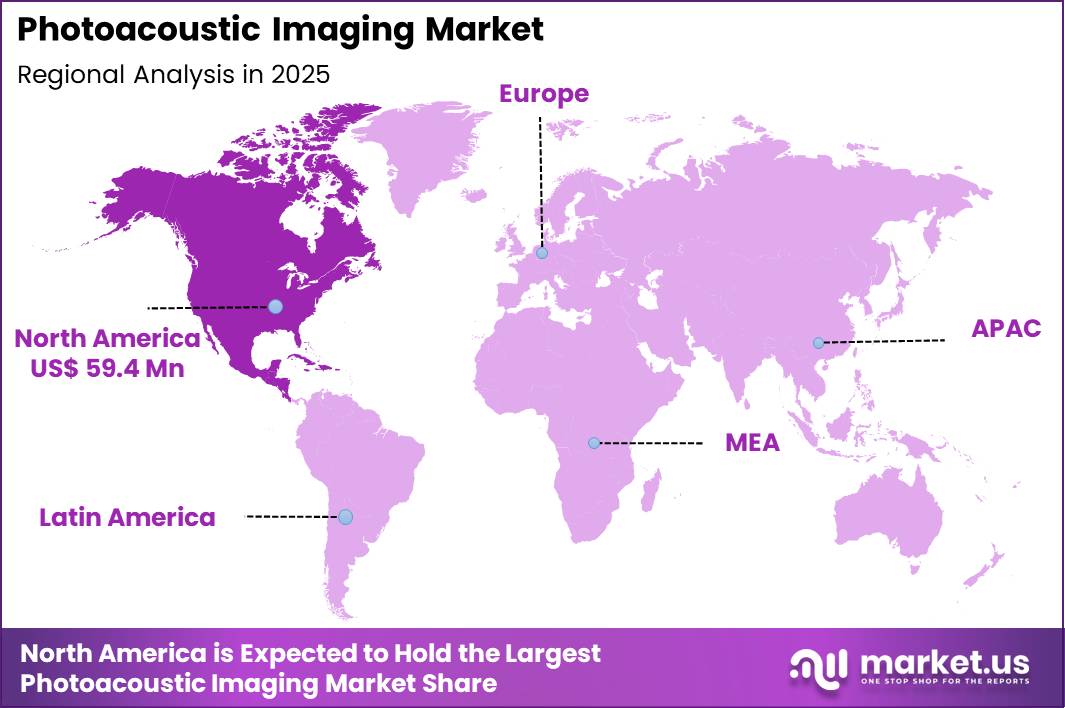

The Global Photoacoustic Imaging Market size is expected to be worth around US$ 1046.6 Million by 2035 from US$ 163.5 Million in 2025, growing at a CAGR of 20.4% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 36.3% share with a revenue of US$ 59.4 Million.

Increasing demand for non-invasive, high-resolution imaging modalities that combine optical contrast with deep tissue penetration propels the photoacoustic imaging market as clinicians and researchers seek tools that reveal functional and molecular information beyond conventional ultrasound or optical techniques.

Radiologists increasingly apply photoacoustic imaging in oncology to visualize tumor vascular networks and oxygenation status, enabling assessment of hypoxia levels that influence treatment response in breast, prostate, and skin cancers. These systems support dermatologic applications by detecting melanoma depth and margins through melanin-specific absorption, guiding excision planning and reducing recurrence risks.

In cardiovascular diagnostics, photoacoustic imaging quantifies plaque composition and neovascularization in carotid arteries, supporting risk stratification for stroke prevention. Researchers utilize the technology in preclinical studies to monitor drug delivery and nanoparticle accumulation in tumor models, providing real-time insights into pharmacokinetics and therapeutic efficacy.

Photoacoustic microscopy further enables high-resolution imaging of microvasculature in small animal models, advancing understanding of angiogenesis and inflammation in arthritis and wound healing research.

Manufacturers pursue opportunities to develop compact, hybrid photoacoustic-ultrasound systems that integrate both modalities for complementary anatomical and functional imaging, expanding clinical applications in point-of-care breast cancer screening and intraoperative tumor margin assessment. These advancements facilitate portable devices suitable for bedside use in neonatal or critical care settings, where non-ionizing imaging of brain oxygenation or peripheral perfusion remains critical.

Opportunities emerge in multispectral photoacoustic imaging that distinguishes chromophores like hemoglobin, melanin, and lipids, enhancing diagnostic specificity in heterogeneous tissues. Companies invest in laser source miniaturization and energy-efficient designs to improve accessibility and reduce operational costs.

In January 2026, researchers from the University of Southern California and the California Institute of Technology published findings on a hybrid imaging approach combining rotational ultrasound tomography with photoacoustic techniques. The system demonstrated the ability to generate high-resolution three-dimensional images of human tissue structures and vascular networks within seconds.

In January 2025, iThera Medical partnered with TRUMPF Photonic Components to incorporate vertical-cavity surface-emitting laser technology into its optoacoustic imaging systems. This transition enables more compact device designs with improved energy efficiency, supporting broader clinical usability.

Recent trends emphasize faster acquisition times, hybrid multimodal integration, and AI-assisted image reconstruction, positioning photoacoustic imaging as a transformative modality for precision diagnostics and therapeutic monitoring in oncology, dermatology, and vascular medicine.

Key Takeaways

- In 2025, the market generated a revenue of US$ 463.5 Million, with a CAGR of 20.4%, and is expected to reach US$ 1046.6 Million by the year 2035.

- The product segment is divided into photoacoustic tomography (PAT) and photoacoustic microscopy (PAM), with photoacoustic tomography (pat)taking the lead with a market share of 66.8%.

- Considering imaging type, the market is divided into pre-clinical and clinical. Among these, pre-clinical held a significant share of 77.9%.

- Furthermore, concerning the application segment, the market is segregated into oncology, cardiology, angiology, histology and interventional radiology. The oncology sector stands out as the dominant player, holding the largest revenue share of 41.3% in the market.

- North America led the market by securing a market share of 36.3%.

Product Analysis

Photoacoustic tomography accounted for 66.8% of growth within product and dominate the photoacoustic imaging market due to its stronger suitability for deeper tissue visualization and broader organ-level imaging. Scientific reviews consistently describe PAT as a hybrid optical-ultrasound modality with strong potential for both preclinical and clinical imaging, especially when researchers need wider field coverage and better penetration than microscopy-oriented systems provide.

PAT is expected to strengthen further because it supports functional and structural assessment of blood-rich tissues, tumor microenvironments, and internal organs with high optical contrast. Research teams also prefer PAT in translational workflows because it aligns more closely with whole-organ and small-animal imaging needs than highly localized microscopy formats.

Continued improvements in detector design, reconstruction algorithms, and multispectral imaging are likely to reinforce PAT leadership across research programs and future clinical translation efforts.

Imaging Type Analysis

Pre-clinical imaging accounted for 77.9% of growth within imaging type and dominate the photoacoustic imaging market because most photoacoustic systems still operate primarily in research environments rather than routine clinical care.

Peer-reviewed reviews describe photoacoustic imaging as highly active in translational and preclinical oncology research, where investigators use it to evaluate tumor oxygenation, vascularity, and therapy response in animal models before broader clinical deployment.

This segment is projected to maintain its lead because research institutions and technology developers continue to use preclinical platforms to validate hardware performance, contrast mechanisms, and disease models before human adoption expands.

Pre-clinical systems are also likely to grow because they offer greater experimental flexibility for multimodal imaging, contrast-agent studies, and longitudinal small-animal monitoring. The dominance of this segment reflects the current stage of technology maturity, where research-driven validation still outweighs routine hospital-scale clinical implementation.

Application Analysis

Oncology accounted for 41.3% of growth within application and dominate the photoacoustic imaging market due to the strong ability of photoacoustic systems to visualize tumor vascularity, oxygen saturation, and other biologic features relevant to cancer detection and monitoring.

Reviews of photoacoustic imaging in oncology highlight its growing value in translational cancer research and its potential to complement existing imaging methods in tumor assessment. This demand is expected to increase further because the global cancer burden remains high.

WHO reported around 20 million new cancer cases in 2022 and projected more than 35 million new cases in 2050, which reflects a 77% increase. Oncology researchers and imaging developers are therefore likely to continue prioritizing photoacoustic tools that improve tumor characterization, treatment monitoring, and functional imaging in preclinical and emerging clinical settings.

Key Market Segments

By Product

- Photoacoustic Tomography (PAT)

- Photoacoustic Microscopy (PAM)

By Imaging Type

- Pre-Clinical

- Clinical

By Application

- Oncology

- Cardiology

- Angiology

- Histology

- Interventional Radiology

Drivers

Rising adoption of photoacoustic imaging in preclinical research is driving the market.

Photoacoustic imaging systems have gained substantial traction in academic and pharmaceutical research institutions for non-invasive visualization of vascular structures and molecular targets in small-animal models. These platforms combine optical excitation with ultrasonic detection to provide high-resolution functional and anatomical information.

The driver aligns with increased funding for translational imaging studies in oncology and cardiovascular disease models. Research facilities report improved sensitivity to hemoglobin oxygenation and contrast agent distribution compared to conventional optical techniques.

The trend supports accelerated evaluation of novel therapeutics through longitudinal monitoring in live subjects. Enhanced depth penetration facilitates studies of deeper tissues without invasive procedures. The expansion corresponds with growing installation of hybrid photoacoustic-ultrasound systems in core imaging facilities.

Sustained demand reflects the modality’s unique ability to bridge preclinical and clinical imaging applications. This factor maintains consistent procurement of dedicated photoacoustic instrumentation and related components. Overall, the momentum in research utilization sustains forward progression in specialized imaging technology adoption.

Restraints

High system acquisition and operational costs are restraining the market.

Commercial photoacoustic imaging platforms require significant capital investment, frequently exceeding several hundred thousand dollars for research-grade systems equipped with tunable lasers and multi-channel ultrasound arrays. Smaller academic departments and biotechnology companies often face budgetary limitations when allocating funds for such specialized instrumentation.

The restraint extends implementation timelines due to lengthy procurement processes and facility preparation requirements. Ongoing expenses include maintenance of high-power lasers and periodic calibration of acoustic detectors. The factor moderates penetration beyond well-funded research centers and large pharmaceutical organizations.

Providers encounter challenges justifying return on investment without dedicated grant support. The dynamic influences preference for collaborative core facilities over individual departmental ownership. This constraint tempers broader market expansion in resource-constrained environments.

The limitation persists in constraining rapid scaling of photoacoustic capabilities across diverse research institutions. Financial barriers continue to affect adoption patterns in emerging application areas.

Opportunities

Development of clinical-grade photoacoustic systems for breast and thyroid imaging is creating growth opportunities.

Manufacturers are advancing compact photoacoustic devices optimized for human breast and thyroid examinations, integrating handheld probes with real-time image reconstruction algorithms. These systems target improved differentiation of benign and malignant lesions through hemoglobin-based contrast. Opportunities arise for adjunctive use alongside conventional ultrasound in outpatient diagnostic workflows.

The framework supports potential reduction in unnecessary biopsies through enhanced lesion characterization. Developers gain capacity to pursue regulatory clearance pathways for specific clinical indications. The development facilitates partnerships with radiology groups for prospective validation studies.

Such progress enables expansion into point-of-care imaging in women’s health and endocrinology clinics. The opportunity fosters differentiation through non-ionizing, contrast-free functional imaging capabilities. Stakeholders anticipate increased clinical acceptance as evidence accumulates on diagnostic performance. This advancement positions participants for transition from preclinical to human diagnostic applications.

Impact of Macroeconomic / Geopolitical Factors

Research institutions and advanced imaging centers continue to explore photoacoustic imaging, yet economic pressure shapes how quickly this technology moves from labs to clinical settings. Rising costs for lasers, sensors, and hybrid imaging systems increase the overall investment required, which can slow adoption in smaller facilities.

Limited access to affordable capital further delays expansion of experimental imaging programs and commercial deployments. Global geopolitical uncertainty affects the supply of precision optical components and semiconductor-based detection systems, creating procurement challenges.

US tariffs on imported lasers, imaging electronics, and specialized components add to equipment costs and reduce pricing flexibility for vendors. These constraints may extend commercialization timelines and limit early-stage installations.

At the same time, developers invest in localized manufacturing and strategic supplier networks to stabilize production. Strong interest in non-invasive, high-resolution imaging for oncology and vascular research continues to support a positive long-term market outlook.

Latest Trends

Increased installations of hybrid photoacoustic-ultrasound systems in academic medical centers is driving the market.

Several leading academic medical centers installed commercial hybrid photoacoustic-ultrasound imaging platforms in 2024-2025 for translational research and early-phase clinical studies. These systems combine photoacoustic functional information with conventional B-mode ultrasound for co-registered anatomical and molecular visualization.

The 2024-2025 installations reflect growing recognition of the modality’s potential in breast cancer staging and sentinel lymph node mapping. Researchers benefit from simultaneous acquisition of structural and hemodynamic data in a single examination. The development aligns with institutional investments in multimodal imaging infrastructure.

Facilities report enhanced capabilities for monitoring treatment response in neoadjuvant therapy protocols. The trend stimulates collaboration between radiology, oncology, and biomedical engineering departments. Early clinical experience demonstrates feasibility in human subjects with acceptable safety profiles.

The increased deployment accelerates data collection for regulatory submissions. Overall, this institutional adoption elevates photoacoustic imaging from experimental to clinically oriented research tool.

Regional Analysis

North America is leading the Photoacoustic Imaging Market

North America accounted for 36.3% of the photoacoustic imaging market in 2025 as research institutions, cancer centers, and biomedical laboratories expanded adoption of hybrid imaging technologies that combine optical and ultrasound techniques for high-resolution tissue visualization.

Universities and medical research facilities across the United States and Canada are increasingly using this technology for oncology research, vascular imaging, and functional tissue analysis due to its ability to provide detailed molecular-level insights.

According to the National Cancer Institute, about 1.96 million new cancer cases were estimated in the United States in 2023, creating strong demand for advanced imaging tools that support early detection and tumor characterization. Research organizations are therefore investing in imaging platforms that improve visualization of tumor vasculature and oxygenation levels.

Pharmaceutical companies are also adopting advanced imaging techniques to support preclinical studies and drug development workflows. Technological advancements in laser systems, transducers, and real-time imaging software have improved image resolution and clinical usability. Academic collaborations and federal funding programs are accelerating innovation in biomedical imaging technologies.

Hospitals and specialty clinics are gradually integrating advanced imaging systems into diagnostic and research settings. These factors collectively supported steady growth of hybrid optical imaging technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as governments and research institutions expand investment in biomedical imaging and precision medicine technologies. Countries such as China, Japan, South Korea, and Singapore are strengthening research infrastructure focused on cancer diagnostics and advanced imaging science.

China’s National Bureau of Statistics reported that research and development spending reached about 3.09 trillion yuan in 2022, supporting continued innovation in biomedical technologies including advanced imaging systems. Universities and research institutes across the region are increasingly adopting hybrid imaging techniques for preclinical research, particularly in oncology and cardiovascular studies.

Hospitals are also expanding access to advanced diagnostic imaging as part of broader healthcare modernization programs. Growing prevalence of chronic diseases and increasing focus on early disease detection are encouraging adoption of high-resolution imaging tools.

Biotechnology companies are collaborating with academic institutions to develop new imaging applications and improve system performance. Governments are supporting innovation through funding programs and technology parks dedicated to life sciences research. These developments are expected to accelerate the adoption of advanced biomedical imaging technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Photoacoustic Imaging Market drive expansion by advancing hybrid imaging systems that combine optical and ultrasound technologies, improving real-time visualization of biological tissues for research and clinical applications. Companies collaborate with academic institutions and biomedical research centers to accelerate adoption in oncology, cardiovascular studies, and preclinical imaging.

They also invest in software analytics, laser-based imaging components, and miniaturized systems that enhance image resolution and portability. FUJIFILM VisualSonics represents a prominent participant in the Photoacoustic Imaging Market and operates as a Canada-based subsidiary of Fujifilm that develops high-frequency ultrasound and photoacoustic imaging systems for preclinical and translational research.

The company focuses on delivering high-resolution imaging platforms that support advanced biomedical research and drug development. Industry competitors continue to introduce innovative imaging technologies, expand research collaborations, and strengthen product portfolios to accelerate the adoption of next-generation imaging solutions.

Top Key Players

- Advantest Corp.

- TomoWave

- Kibero GmbH

- FUJIFILM VisualSonics Inc.

- Seno Medical Instruments

- iThera Medical GmbH

- Aspectus GmbH

- Vibronix Inc.

Recent Developments

- In January 2026, Seno Medical obtained EU MDR CE certification for its Imagio Model 9100 system. The platform combines optoacoustic imaging with integrated AI-based analysis to support real-time differentiation between benign and malignant breast lesions, improving diagnostic confidence during clinical assessments.

- In July 2025, FUJIFILM VisualSonics introduced the Vevo F2 LAZR-X20 imaging system, which integrates a wide ultrasound frequency range with photoacoustic capabilities. The platform is designed for preclinical research applications, enabling non-invasive visualization of tissue components such as lipids and collagen in oncology and neurobiology studies.

- In January 2025, a clinical study involving more than 200 patients demonstrated the use of photoacoustic radiomics to assess Ki-67 expression in breast cancer. The findings highlight the potential of the technology to provide non-invasive molecular insights that could complement or reduce the need for traditional biopsy methods.

Report Scope

Report Features Description Market Value (2025) US$ 163.5 Million Forecast Revenue (2035) US$ 1046.6 Million CAGR (2026-2035) 20.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Photoacoustic Tomography (PAT) and Photoacoustic Microscopy (PAM)), By Imaging Type (Pre-Clinical and Clinical), By Application (Oncology, Cardiology, Angiology, Histology and Interventional Radiology) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Advantest Corp., TomoWave, Kibero GmbH, FUJIFILM VisualSonics Inc., Seno Medical Instruments, iThera Medical GmbH, Aspectus GmbH, Vibronix Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Photoacoustic Imaging MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Photoacoustic Imaging MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Advantest Corp.

- TomoWave

- Kibero GmbH

- FUJIFILM VisualSonics Inc.

- Seno Medical Instruments

- iThera Medical GmbH

- Aspectus GmbH

- Vibronix Inc.

Our Clients

- 181857

- March 2026