Quick Navigation

Report Overview

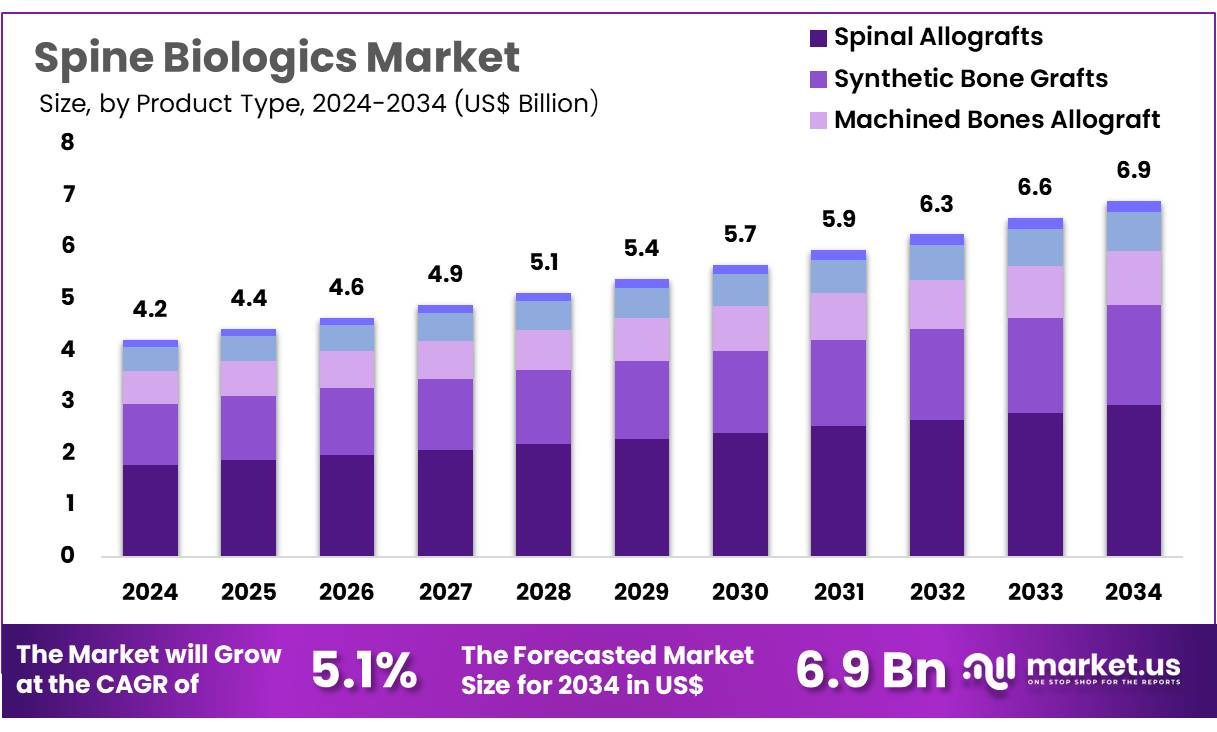

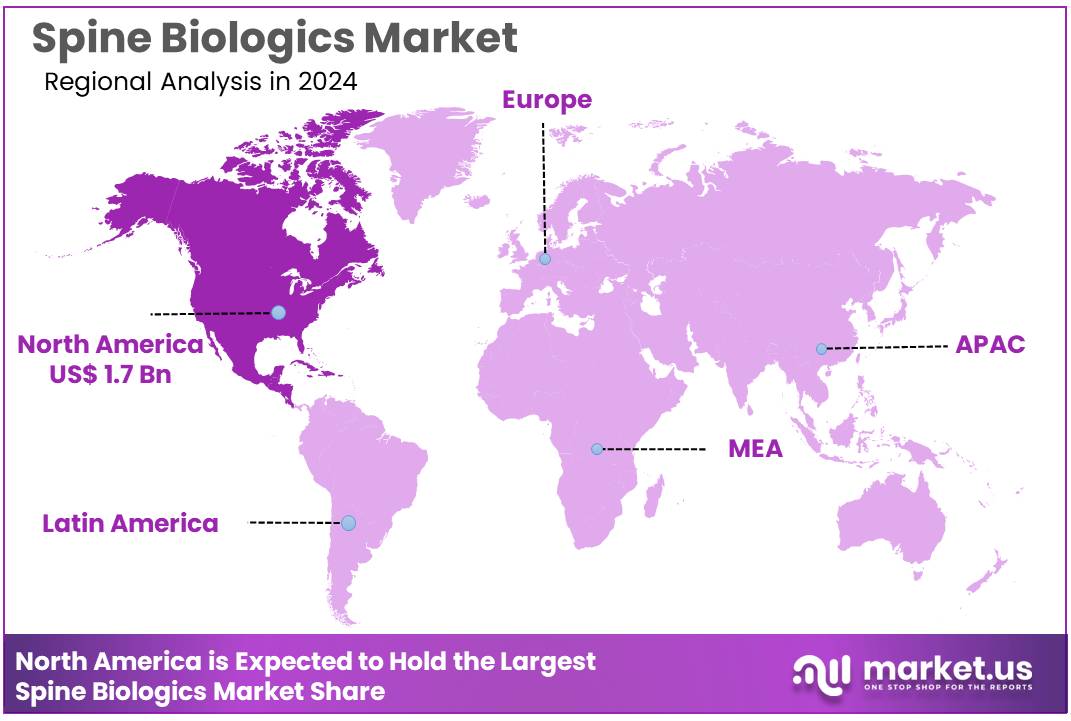

Global Spine Biologics Market size is expected to be worth around US$ 6.9 billion by 2034 from US$ 4.2 billion in 2024, growing at a CAGR of 5.1% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 39.8% share and holds US$ 1.7 Billion market value for the year.

Growing demand for effective treatments in spine surgery is driving the expansion of the spine biologics market. Spine biologics, which include products such as bone grafts, growth factors, and stem cell therapies, are widely used in spinal fusion and regeneration procedures to promote healing and restore function. These biologics play a critical role in addressing complex spinal disorders, including degenerative diseases, trauma, and spinal deformities.

As the global population ages, the incidence of spinal disorders rises, creating significant opportunities for advanced biologic therapies. In July 2022, AlloSource introduced AlloFuse microfibers, demineralized bone allografts designed for orthopedic procedures such as foot, ankle, and spine surgeries. These microfibers are made entirely from demineralized cortical bone, providing a pure and effective solution for bone grafting.

The market also benefits from the increasing focus on regenerative medicine, where biologics are used to stimulate tissue repair and reduce the need for traditional surgical interventions. The National Spinal Cord Injury Statistical Center (NSCISC) projected that the US population would reach approximately 335 million in 2023, with an estimated 18,000 new cases of traumatic spinal cord injury occurring annually.

These trends create a growing demand for biologics that can help address the challenges of spinal injury and degeneration. Recent innovations in biologic therapies, such as stem cell-based treatments and advanced biomaterials, present new opportunities for market growth, providing safer, more effective solutions for spinal conditions.

Key Takeaways

- Spine Biologics Market size is expected to be worth around US$ 6.9 billion by 2034 from US$ 4.2 billion in 2024

- The product type segment is divided into synthetic bone grafts, spinal allografts, machined bones allograft, demineralized bone matrix, and others, with spinal allografts taking the lead in 2024 with a market share of 42.5%.

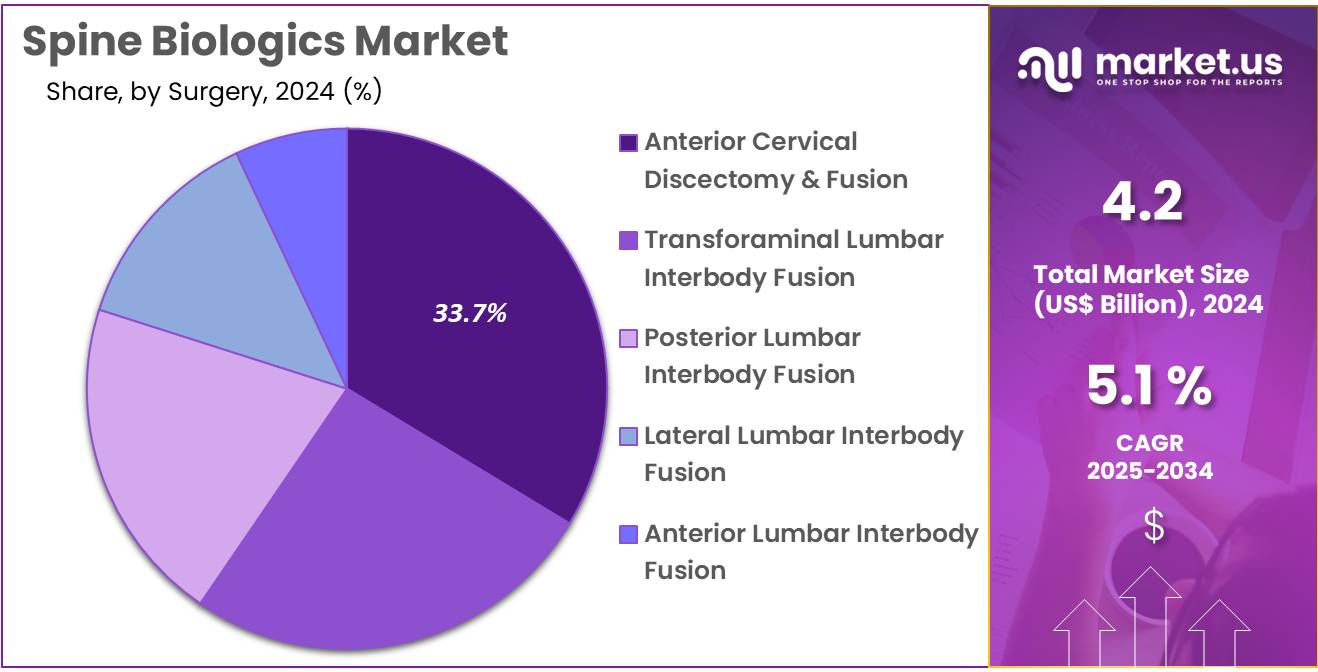

- Considering surgery, the market is divided into transforaminal lumbar interbody fusion, posterior lumbar interbody fusion, lateral lumbar interbody fusion, anterior lumbar interbody fusion, and anterior cervical discectomy & fusion. Among these, anterior cervical discectomy & fusion held a significant share of 33.7%.

- Furthermore, concerning the end-use segment, the market is segregated into hospitals and ambulatory surgical centers. The anterior cervical discectomy & fusion sector stands out as the dominant player, holding the largest revenue share of 61.2% in the Spine Biologics market.

- North America led the market by securing a market share of 39.8% in 2024.

Product Type Analysis

The spinal allografts segment led in 2023, claiming a market share of 42.5% owing to the increasing demand for effective solutions in spinal fusion surgeries. Spinal allografts, including demineralized bone matrix and machined bone allografts, are expected to see rising adoption due to their ability to promote bone healing while reducing the risk of complications compared to autografts.

The growing preference for minimally invasive procedures and the rising incidence of spinal degenerative diseases are anticipated to further support this segment’s expansion. Additionally, advancements in tissue processing and allograft preservation techniques are expected to enhance the efficacy and safety of spinal allografts, making them a preferred choice for spine surgeons.

As the healthcare industry focuses on improving patient outcomes and reducing recovery times, spinal allografts are likely to continue to grow in popularity, particularly in complex spinal surgeries.

Surgery Analysis

The anterior cervical discectomy & fusion held a significant share of 33.7% due to the increasing number of patients undergoing spinal surgeries to address degenerative disc diseases and cervical spine disorders. ACDF is anticipated to remain one of the most widely performed surgeries, with its ability to restore stability and alleviate pain in patients with cervical spine issues.

The growing aging population, which is more susceptible to cervical disc degeneration, is likely to drive the demand for ACDF procedures. Furthermore, advancements in surgical techniques and the integration of biologics to enhance bone fusion and reduce recovery times are expected to increase the popularity of ACDF surgeries. As the need for spinal fusion procedures continues to rise, the ACDF segment is projected to see continued growth, driven by improvements in surgical outcomes and post-operative care.

End-use Analysis

The anterior cervical discectomy & fusion segment had a tremendous growth rate, with a revenue share of 61.2% owing to as more hospitals and ambulatory surgical centers (ASCs) adopt these procedures to treat cervical spine issues. The increasing prevalence of cervical spine disorders, particularly in the aging population, is expected to drive the demand for ACDF surgeries in both hospital and outpatient settings.

ASCs are anticipated to see significant growth in the number of ACDF surgeries due to their ability to provide cost-effective, minimally invasive options with shorter recovery times compared to traditional hospital settings. As healthcare facilities aim to optimize patient throughput and reduce treatment costs, the demand for ACDF surgeries in ASCs is projected to increase.

Hospitals are also expected to continue investing in advanced surgical technologies and biologics to improve patient outcomes, further contributing to the growth of this segment in the spine biologics market.

Key Market Segments

By Product Type

- Synthetic Bone Grafts

- Spinal Allografts

- Machined Bones Allograft

- Demineralized Bone Matrix

- Others

By Surgery

- Transforaminal Lumbar Interbody Fusion

- Posterior Lumbar Interbody Fusion

- Lateral Lumbar Interbody Fusion

- Anterior Lumbar Interbody Fusion

- Anterior Cervical Discectomy & Fusion

By End-use

- Hospitals and

- Ambulatory Surgical Centers

Drivers

Growing prevalence of spinal injury is driving the spine biologics market

Growing prevalence of spinal injuries significantly drives the spine biologics market by escalating the demand for advanced therapeutic solutions. The National Spinal Cord Injury Statistical Center (NSCISC) projected the US population to reach approximately 335 million in 2023. Based on current data, an estimated 18,000 new cases of traumatic spinal cord injury (tSCI) occur annually in the United States, equating to 54 cases per million individuals.

This rising incidence underscores the urgent need for effective biologic treatments that can promote spinal cord repair and improve patient outcomes. Spine biologics, including stem cell therapies, growth factors, and biomaterials, offer promising avenues for enhancing nerve regeneration and functional recovery. As healthcare providers seek innovative solutions to address the complexities of spinal injuries, the adoption of spine biologics is expected to increase.

Additionally, advancements in biotechnology and regenerative medicine drive the development of more sophisticated and targeted biologic therapies. Increased awareness and better diagnostic tools enable earlier intervention, further boosting the demand for spine biologics. Government initiatives and funding dedicated to spinal injury research also support market growth by facilitating the translation of scientific discoveries into clinical applications.

Furthermore, the integration of personalized medicine approaches with spine biologics allows for tailored treatments that cater to individual patient needs, enhancing therapeutic efficacy. As the global burden of spinal injuries continues to rise, the spine biologics market is projected to expand, fueled by continuous innovations and a growing emphasis on improving quality of life for affected individuals.

Restraints

High complexity of technology is restraining the spine biologics market

A significant restraint in the spine biologics market is the high complexity of the underlying technology, which poses challenges for widespread adoption and effective implementation. Developing advanced biologic therapies for spinal injuries requires sophisticated laboratory techniques and specialized expertise, making it difficult for many healthcare institutions to integrate these solutions into their treatment protocols.

The intricate processes involved in manufacturing and administering spine biologics demand rigorous quality control and adherence to stringent regulatory standards, increasing operational costs and time. Additionally, the customization of biologic treatments to cater to individual patient needs adds another layer of complexity, necessitating personalized approaches that can be resource-intensive. Smaller research facilities and healthcare providers may struggle to afford the necessary investments in technology and training, limiting their ability to participate in the market.

Furthermore, the rapid pace of technological advancements means that existing biologic therapies can quickly become outdated, requiring continuous investment in research and development to stay competitive. The complexity of ensuring consistent and reproducible results across different clinical settings also hampers the scalability of spine biologics. As a result, the high technological complexity acts as a barrier to entry, restricting market growth and limiting the accessibility of advanced spine biologic treatments to a broader population.

Opportunities

Rising innovation is creating opportunities for the spine biologics market

Rising innovation creates substantial opportunities for the spine biologics market by driving the development of more effective and versatile therapeutic solutions. In August 2024, Stryker introduced the Pangea Plating System, which obtained FDA approval in 2023. This advanced system provides a versatile and comprehensive plating portfolio with variable-angle options designed to accommodate diverse patient needs. Innovations like the Pangea Plating System enhance the efficacy of spinal surgeries by offering customizable solutions that improve patient outcomes and reduce recovery times.

Additionally, advancements in stem cell research and gene therapy are enabling the creation of more targeted biologic treatments that can effectively address spinal cord injuries and promote regeneration. The integration of biomaterials and nanotechnology into spine biologics allows for the development of scaffolds and delivery systems that enhance the stability and functionality of implanted therapies.

Collaborative efforts between biotechnology firms, research institutions, and medical device companies accelerate the innovation cycle, leading to the commercialization of cutting-edge spine biologic products.

Furthermore, the adoption of digital technologies and data analytics facilitates the optimization of treatment protocols and the personalization of therapies, increasing their effectiveness and patient satisfaction. Increased investment in research and development by key industry players supports the continuous introduction of novel biologic solutions, expanding the market’s potential.

As innovation drives the creation of more sophisticated and reliable spine biologics, the market is anticipated to experience significant growth, meeting the evolving needs of patients and healthcare providers alike. This surge in innovative therapies not only enhances the treatment landscape for spinal injuries but also positions the spine biologics market for sustained expansion and increased adoption globally.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors influence the spine biologics market in several ways. On the positive side, rising healthcare investments, particularly in emerging markets, drive demand for advanced biologics in spinal treatments. The growing prevalence of spinal disorders, coupled with the aging population, increases the need for effective therapeutic solutions.

However, economic slowdowns can limit healthcare spending, reducing the adoption of high-cost biologic treatments. Geopolitical issues, such as trade restrictions or supply chain disruptions, may impact the availability of key materials used in biologics manufacturing, raising costs.

Additionally, regulatory challenges across different regions can hinder market access and complicate product approval processes. Despite these challenges, the ongoing advancements in research and development, along with increasing adoption of minimally invasive treatments, are expected to support long-term growth in the spine biologics market.

Latest Trends

Integration of AI Driving the Spine Biologics Market

Increasing integration of artificial intelligence (AI) is driving growth in the spine biologics market. High advancements in AI technology are expected to enhance treatment outcomes and streamline the development of biologic therapies for spinal conditions. AI applications, such as improved imaging, diagnostics, and personalized treatment plans, are projected to optimize patient care and predict surgical outcomes.

In September 2024, Medtronic plc unveiled multiple advancements across software, hardware, and imaging to enhance its AiBLE ecosystem, integrating navigation, data, AI, imaging, robotics, software, and implants to improve predictability and outcomes in spine and cranial surgical procedures. As AI continues to advance, its role in developing precision biologics and improving clinical practices in spinal care is likely to increase, boosting market growth.

Regional Analysis

North America is leading the Spine Biologics Market

North America dominated the market with the highest revenue share of 39.8% owing to the increasing prevalence of spinal disorders, advancements in biologic treatments, and the growing demand for minimally invasive surgical options. The rise in aging populations and lifestyle-related conditions, such as obesity and osteoporosis, has led to an increase in spinal surgeries, further driving demand for innovative spine biologics.

In January 2024, the US Food and Drug Administration (FDA) granted Breakthrough Device Designation to Renovos Biologics for its flagship product, RENOVITE Bone Morphogenic Protein 2. This recognition highlights the region’s strong focus on advancing spinal treatments, particularly biologics that support bone regeneration and enhance healing after spinal surgeries.

The ongoing development of advanced biologic therapies, including stem cell-based treatments and bone morphogenic proteins, has contributed to the market’s expansion by providing more effective, less invasive treatment alternatives. Furthermore, increased healthcare investments and collaborations between biotech companies and medical device firms have enhanced the availability of cutting-edge solutions for spine surgery, contributing to the steady growth of the spine biologics market in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rising healthcare investments, a growing population, and an increasing prevalence of spinal disorders. The demand for advanced biologic treatments, particularly for conditions like degenerative disc disease and spinal stenosis, is anticipated to rise as healthcare systems in countries like China, India, and Japan improve.

The region’s expanding aging population and urbanization are likely to contribute to higher incidences of spinal disorders, leading to greater demand for spinal biologics in surgeries and rehabilitation. Additionally, advancements in biotechnology and regenerative medicine in countries such as South Korea and Australia are expected to drive innovation in the field.

With increasing awareness of the benefits of biologic treatments, such as quicker recovery times and reduced risk of complications, the market for spine biologics in Asia Pacific is projected to grow rapidly. The development of local manufacturing capabilities and government initiatives to improve healthcare access are likely to further propel the market’s growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the spine biologics market focus on strategies like developing advanced biomaterials and tissue engineering solutions to improve treatment outcomes for spinal disorders. Companies enhance their product portfolios by introducing innovative bone graft substitutes, synthetic implants, and biologics for fusion and non-fusion procedures.

Collaborations with orthopedic surgeons and healthcare institutions drive product optimization and adoption in clinical settings. Geographic expansion into regions with increasing demand for minimally invasive surgeries helps capture new customer bases. Investments in research and development strengthen their ability to address evolving patient and healthcare needs.

Medtronic plc is a leading company in this market, offering a wide range of biologic solutions such as Infuse Bone Graft for spinal fusion procedures. The company focuses on innovation, combining advanced materials with extensive clinical research to deliver effective solutions. Medtronic’s strong global presence and commitment to improving patient outcomes solidify its leadership position in the spinal care industry.

Top Key Players

- Zimmer Biomet

- Stryker

- PUR Biologics

- Orthofix Medical

- Orthofix

- Medtronic

- Kuros Biosciences

- Cerapedics

- Biocomposites

Recent Developments

- In October 2023, Orthofix Medical, a prominent global leader in spine and orthopedics, announced the 510(k) clearance and commercial rollout of OsteoCove, an innovative bioactive synthetic graft designed for advanced orthopedic applications.

- In July 2023, Cerapedics, a commercial-stage orthopedics company dedicated to improving bone repair therapies, secured FDA approval for two of its products intended for cervical spinal fusion. Its next-generation product is currently under review for use in lumbar spinal fusion.

- In April 2023, PUR Biologics, a subsidiary of HippoFi, Inc., introduced PURcore, a moldable synthetic material designed for spine surgery. This advanced product incorporates an interconnected micropore structure that facilitates the rapid colonization of patient cells and growth factors, promoting efficient bone healing and regeneration.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 4.2 billion |

| Forecast Revenue (2034) | US$ 6.9 billion |

| CAGR (2025-2034) | 5.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Synthetic Bone Grafts, Spinal Allografts, Machined Bones Allograft, Demineralized Bone Matrix, and Others), By Surgery (Transforaminal Lumbar Interbody Fusion, Posterior Lumbar Interbody Fusion, Lateral Lumbar Interbody Fusion, Anterior Lumbar Interbody Fusion, and Anterior Cervical Discectomy & Fusion), By End-use (Hospitals and Ambulatory Surgical Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zimmer Biomet, Stryker, PUR Biologics, Orthofix Medical, Orthofix, Medtronic, Kuros Biosciences, Cerapedics, and Biocomposites. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |