Quick Navigation

Report Overview

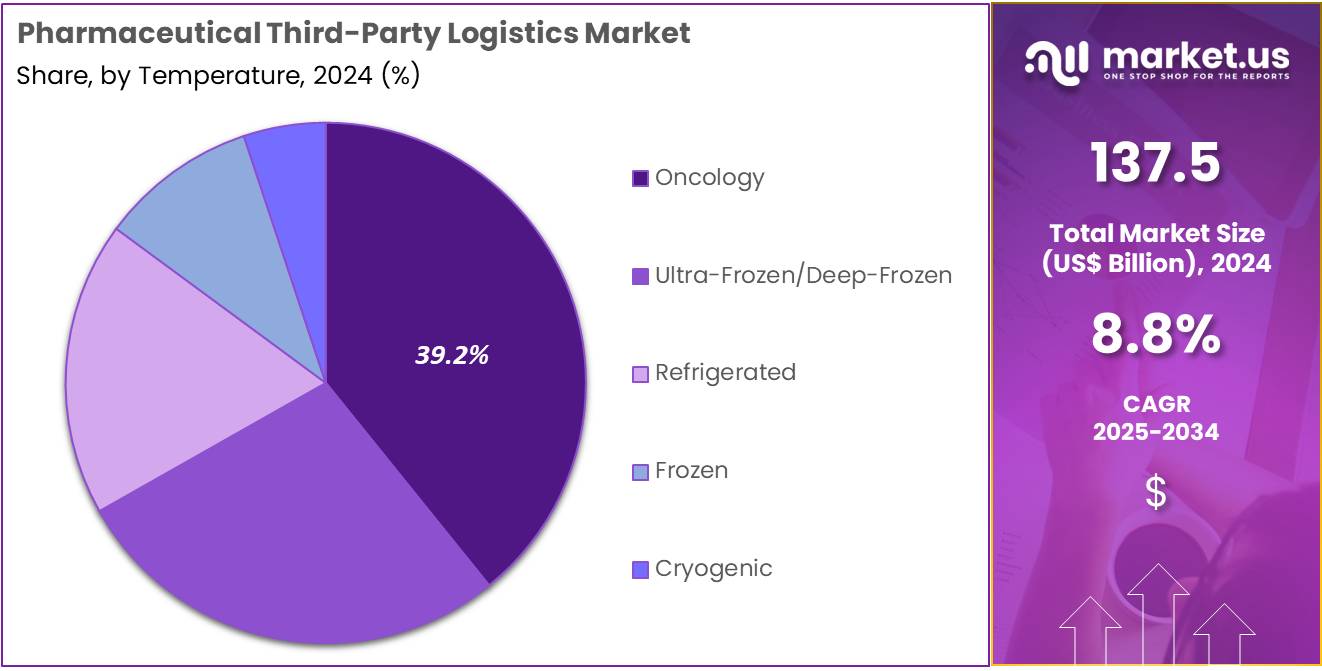

The Pharmaceutical Third-Party Logistics Market size is expected to be worth around US$ 319.6 billion by 2034 from US$ 137.5 billion in 2024, growing at a CAGR of 8.8% during the forecast period 2025 to 2034.

Increasing demand for efficient supply chain solutions and the rising complexity of pharmaceutical distribution are driving the growth of the pharmaceutical third-party logistics (3PL) market. Pharmaceutical companies rely on 3PL providers to manage the storage, transportation, and distribution of drugs and medical products, ensuring timely delivery and compliance with regulatory standards.

The growing emphasis on patient safety, temperature-sensitive products, and the need for track-and-trace capabilities create a significant need for specialized logistics services. Pharmaceutical 3PL providers offer various services, including warehousing, inventory management, cold chain logistics, and last-mile delivery, enabling companies to focus on core competencies while reducing costs. In January 2021, XPO Logistics Inc. completed the acqu`isition of a significant portion of Kuehne + Nagel’s contract logistics operations in the United Kingdom and Ireland.

This move aligns with XPO’s strategy to strengthen its 3PL services in key markets, signaling the ongoing consolidation within the pharmaceutical logistics sector. Recent trends show increased adoption of technology solutions such as cloud-based platforms, real-time tracking systems, and automated warehouses, which improve efficiency and transparency.

The rise in e-commerce and online pharmaceutical sales further presents opportunities for 3PL providers to enhance last-mile delivery capabilities. As the pharmaceutical industry grows and evolves, the pharmaceutical 3PL market is expected to experience continued expansion driven by technological innovation, regulatory compliance, and a focus on cost-effective logistics solutions.

Key Takeaways

- In 2024, the market for pharmaceutical third-party logistics generated a revenue of US$ 137.5 billion, with a CAGR of 8.8%, and is expected to reach US$ 319.6 billion by the year 2033.

- The product type segment is divided into branded, vaccine, generic, biosimilar, and others, with branded taking the lead in 2024 with a market share of 42.3%.

- Considering application, the market is divided into oncology, neurology, infectious diseases, diabetes, cardiovascular diseases, and others. Among these, ambient held a significant share of 36.8%.

- Concerning the temperature segment, the oncology sector stands out as the dominant player, holding the largest revenue share of 39.2% in the pharmaceutical third-party logistics market.

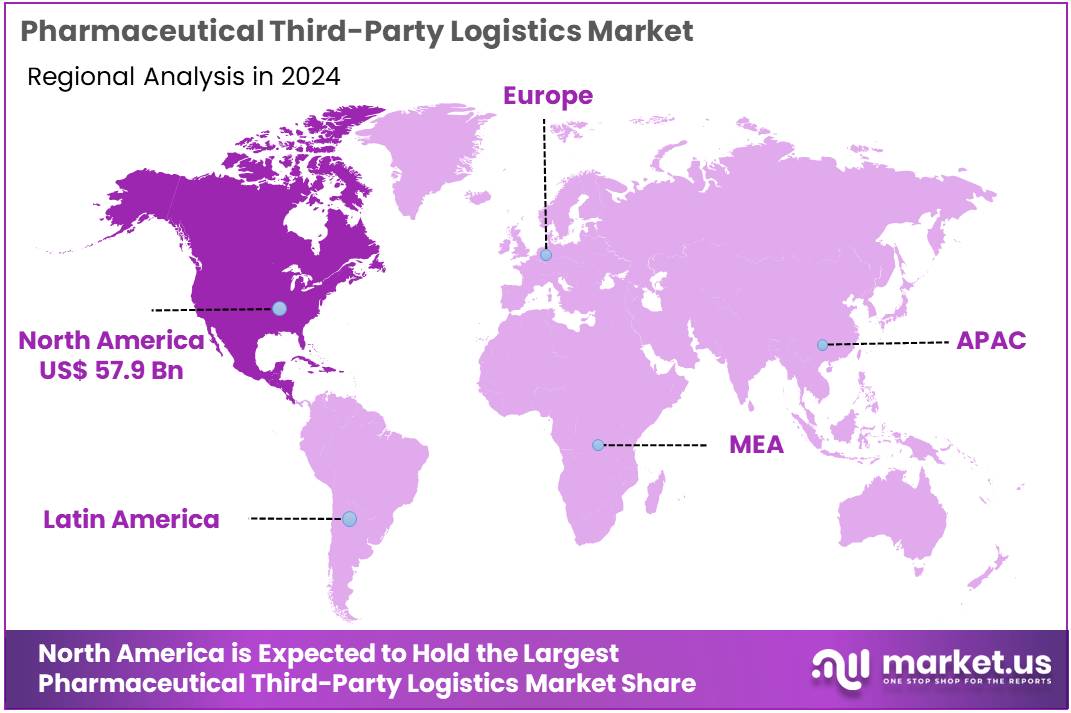

- North America led the market by securing a market share of 42.1% in 2024.

Product Type Analysis

The branded segment led in 2024, claiming a market share of 42.3% owing to as pharmaceutical companies increasingly focus on providing high-quality, branded drugs that stand out in a competitive market. The growth of this segment is expected to be driven by the expanding demand for branded drugs that offer distinct therapeutic benefits, with premium pricing that supports specialized logistics needs.

Additionally, branded drugs require specific storage, handling, and distribution procedures, creating opportunities for third-party logistics providers to offer tailored services. As the pharmaceutical industry continues to innovate and introduce new branded therapies, especially in areas like oncology and immunotherapy, the demand for efficient, reliable logistics solutions is anticipated to rise, contributing to the market’s expansion.

Application Analysis

The ambient held a significant share of 36.8% due to the increasing demand for drugs that do not require temperature-controlled conditions for storage and transportation. Many pharmaceutical products, including those used in oncology, neurology, and infectious diseases, can be safely stored at ambient temperatures, making them ideal candidates for logistics operations that are less costly and more efficient.

The growth of this segment is projected to be fueled by the rising number of generic and over-the-counter drugs entering the market, which do not have the stringent storage requirements that more sensitive medications demand. Additionally, improvements in supply chain technologies and the growing trend of e-commerce and direct-to-patient deliveries are likely to further propel the ambient segment’s expansion.

Temperature Analysis

The oncology segment had a tremendous growth rate, with a revenue share of 39.2% owing to the increasing prevalence of cancer and the growing need for specialized temperature-controlled logistics solutions. Oncology drugs, including biologics and chemotherapy treatments, often require refrigerated or frozen storage to maintain their potency and efficacy.

With the rise in targeted therapies and immunotherapies, many of these drugs need specific handling and transport conditions, which has driven the demand for refrigerated and ultra-frozen logistics solutions. Additionally, as the global cancer treatment market expands and new therapies are introduced, the need for specialized logistics providers who can handle temperature-sensitive products is expected to continue growing, further driving the segment’s growth in the pharmaceutical logistics industry.

Key Market Segments

By Product Type

- Branded

- Vaccine

- Generic

- Biosimilar

- Others

By Application

- Oncology

- Neurology

- Infectious Diseases

- Diabetes

- Cardiovascular Diseases

- Others

By Temperature

- Ultra-frozen/Deep-Frozen

- Refrigerated

- Frozen

- Cryogenic

- Ambient

Drivers

Growing Investment in Healthcare Driving the Pharmaceutical Third-Party Logistics Market

Growing investment in healthcare significantly drives the pharmaceutical third-party logistics market. In February 2022, DHL Supply Chain committed a US$ 400 million investment to expand its Life Sciences and Healthcare division. This initiative added 3 million square feet of pharmaceutical and medical device distribution space, including six new U.S. facilities to address rising demand.

Such investments enhance the capacity of third-party logistics providers to manage complex supply chains efficiently. Healthcare companies increasingly rely on 3PL partners for specialized services like cold chain logistics, ensuring the safe and timely delivery of temperature-sensitive pharmaceuticals. These partnerships streamline operations and reduce costs, enabling pharmaceutical companies to focus on core activities like research and development.

The rise in global healthcare spending, particularly in emerging markets, further fuels demand for robust logistics networks. Technological advancements in tracking and automation optimize supply chain visibility and efficiency. These trends underline the critical role of healthcare investments in shaping the future of pharmaceutical logistics.

Restraints

High Operational Costs Are Restraining the Pharmaceutical Third-Party Logistics Market

High operational costs are restraining the pharmaceutical third-party logistics market. Maintaining temperature-sensitive supply chains, particularly for biologics and vaccines, requires advanced infrastructure and equipment. Specialized vehicles, cold storage facilities, and monitoring systems add significant expenses to logistics operations. Rising fuel prices and labor costs further compound these challenges, increasing the overall cost of transportation and storage.

Compliance with stringent regulatory standards, especially in regions with varying guidelines, adds to operational complexities and costs. Smaller logistics providers often struggle to invest in the required technology and infrastructure, limiting their market share. Unexpected disruptions in the supply chain, such as natural disasters or geopolitical tensions, can escalate operational expenses further. Addressing these cost barriers requires innovative solutions, such as collaborative logistics models and investments in energy-efficient technologies.

Opportunities

Increasing Importance of Cold Chain Logistics

Increasing importance of cold chain logistics offers a substantial opportunity for the pharmaceutical third-party logistics market. A global survey conducted in July 2021 revealed that over 62% of respondents identified cold chain logistics as a critical driver of business growth for 3PL providers. Rising demand for temperature-sensitive products like biologics, vaccines, and specialty drugs underscores the need for advanced cold chain solutions.

Third-party logistics providers invest in cutting-edge refrigeration technologies and real-time tracking systems to ensure product safety and regulatory compliance. The COVID-19 pandemic highlighted the vital role of cold chain logistics in delivering vaccines globally, driving further investment in this area. Emerging markets, with expanding pharmaceutical industries, represent significant growth opportunities for cold chain services.

Partnerships between pharmaceutical companies and logistics providers foster innovation and efficiency in managing complex supply chains. These developments position cold chain logistics as a cornerstone for future growth in the pharmaceutical 3PL sector.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a considerable influence on the pharmaceutical third-party logistics market. On the positive side, global healthcare spending has increased, driving the demand for efficient supply chain solutions, especially in the pharmaceutical sector. Expanding markets in emerging economies fuel growth by increasing the need for reliable logistics networks to handle pharmaceutical distribution.

However, economic slowdowns or trade barriers can disrupt the flow of goods, impacting logistics providers’ efficiency and costs. Geopolitical instability, such as regulatory changes, customs policies, or political unrest, can further complicate cross-border transportation and delay deliveries. Rising fuel costs, environmental regulations, and labor shortages also pose challenges to the logistics industry.

Despite these obstacles, the increasing focus on temperature-controlled logistics, the growth of e-commerce, and the rising demand for healthcare products contribute to a positive market outlook. As a result, the pharmaceutical third-party logistics market is set to continue expanding, driven by both global healthcare growth and innovation in supply chain management.

Trends

Rise in Acquisitions and Mergers Driving the Pharmaceutical Third-Party Logistics Market

Rising acquisitions and mergers are a significant trend in the pharmaceutical third-party logistics market. High demand for integrated supply chain solutions, combined with the growing need for global logistics networks, is expected to push companies to consolidate and expand their operations. Mergers enable logistics providers to enhance their geographical reach, streamline operations, and offer more comprehensive solutions to clients.

The trend is anticipated to increase the efficiency and speed of pharmaceutical deliveries while reducing costs. In September 2024, DSV revealed plans to acquire DB Schenker from Deutsche Bahn for US$ 14.74 billion. This acquisition is designed to expand DSV’s global footprint, strengthen its operational capabilities, and enhance value for its customers, employees, and investors. As acquisitions and mergers continue to rise, the pharmaceutical third-party logistics market is likely to experience increased consolidation, enhanced service offerings, and more efficient global operations, benefiting the entire pharmaceutical supply chain.

Regional Analysis

North America is leading the Pharmaceutical third-party logistics Market

North America dominated the market with the highest revenue share of 42.1% owing to rising demand for streamlined distribution and operational efficiency. The extended collaboration between Yaral Pharma, a generics subsidiary of IBSA, and EVERSANA in May 2023 highlighted the region’s emphasis on optimizing supply chains. EVERSANA’s logistics support allowed Yaral Pharma to enhance market access for its pain management and endocrinology products, catering to growing healthcare needs.

The increasing complexity of pharmaceutical supply chains, coupled with the need for temperature-controlled transportation for biologics and specialty drugs, boosted the reliance on third-party logistics providers. Advancements in digital technologies, including real-time tracking and automated inventory management, further improved operational efficiency.

The expanding pharmaceutical sector, fueled by rising demand for prescription medications and generics, also contributed to the market’s growth. Favorable regulatory frameworks and the presence of established logistics players provided a robust infrastructure for seamless drug distribution. Additionally, the increasing prevalence of chronic diseases and patient-centric delivery models reinforced the demand for reliable and scalable third-party logistics services.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to expanding healthcare infrastructure and increasing pharmaceutical production. FedEx’s announcement in February 2024 of its Life Science Center in India exemplifies the region’s growing focus on catering to healthcare logistics and storage needs, particularly for clinical trials.

Rising demand for cold chain logistics, fueled by the increasing production of biologics and vaccines, is projected to drive growth. Expanding pharmaceutical exports from countries like India and China are likely to boost the need for efficient international logistics solutions. Government initiatives aimed at improving drug accessibility and affordability are anticipated to encourage collaborations between pharmaceutical manufacturers and logistics providers.

Technological advancements, including AI-driven supply chain optimization and real-time shipment monitoring, are expected to enhance service quality. Growing investment in healthcare infrastructure, coupled with rising chronic disease prevalence, is likely to increase reliance on third-party logistics services. Medical tourism, especially in countries offering cost-effective treatments, is estimated to further stimulate demand for specialized pharmaceutical distribution services across Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the pharmaceutical third-party logistics market focus on expanding their cold chain capabilities to ensure the safe transportation of temperature-sensitive drugs, including biologics and vaccines. Companies invest in advanced tracking and monitoring technologies to provide real-time visibility and improve supply chain efficiency.

Strategic partnerships with pharmaceutical manufacturers and healthcare providers help broaden their service offerings and enhance market penetration. Geographic expansion into emerging markets with rising healthcare demands supports further growth. Many players also emphasize sustainability by adopting eco-friendly packaging and fuel-efficient transport solutions.

DHL Supply Chain is a leading company in this market, offering comprehensive third-party logistics services tailored to the pharmaceutical sector. The company combines advanced logistics technology with a global network to ensure the reliable delivery of medical products. DHL’s commitment to innovation and customer-centric solutions makes it a trusted partner in the healthcare logistics industry.

Top Key Players in the Pharmaceutical third-party logistics Market

- McKesson Corporation

- Kuehne+Nagel

- FedEx Express

- EVERSANA

- DB SCHENKER

- CEVA Logistics

- Cencora Corporation

- Cardinal Health

Recent Developments

- In September 2024, CEVA Logistics announced it would assume CMA CGM’s freight management operations. This strategic move allows CEVA to boost its logistics services while enabling CMA CGM to concentrate on its shipping activities, fostering growth and operational efficiency for both organizations.

- In August 2023, FedEx Express revealed its partnership with the Gyeongsangbuk-do provincial government in South Korea. The collaboration focuses on assisting small and medium-sized enterprises (SMEs) in expanding into industries like biopharmaceuticals, semiconductors, automotive manufacturing, and wireless communication devices.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 137.5 billion |

| Forecast Revenue (2034) | US$ 319.6 billion |

| CAGR (2025-2034) | 8.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Branded, Vaccine, Generic, Biosimilar, and Others), By Application (Oncology, Neurology, Infectious Diseases, Diabetes, Cardiovascular Diseases, and Others), By Temperature (Ultra-frozen/Deep-Frozen, Refrigerated, Frozen, Cryogenic, and Ambient) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | McKesson Corporation, Kuehne+Nagel, FedEx Express, EVERSANA, DB SCHENKER, CEVA Logistics, Cencora Corporation, and Cardinal Health. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |