Quick Navigation

Report Overview

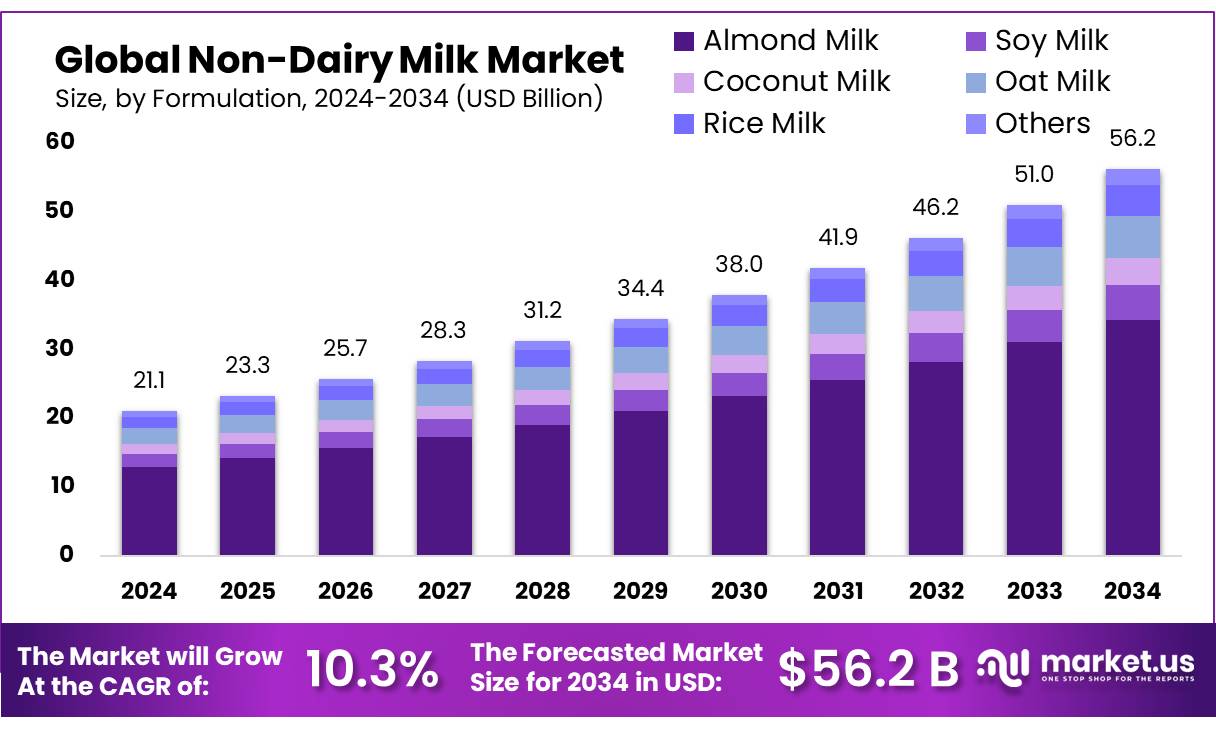

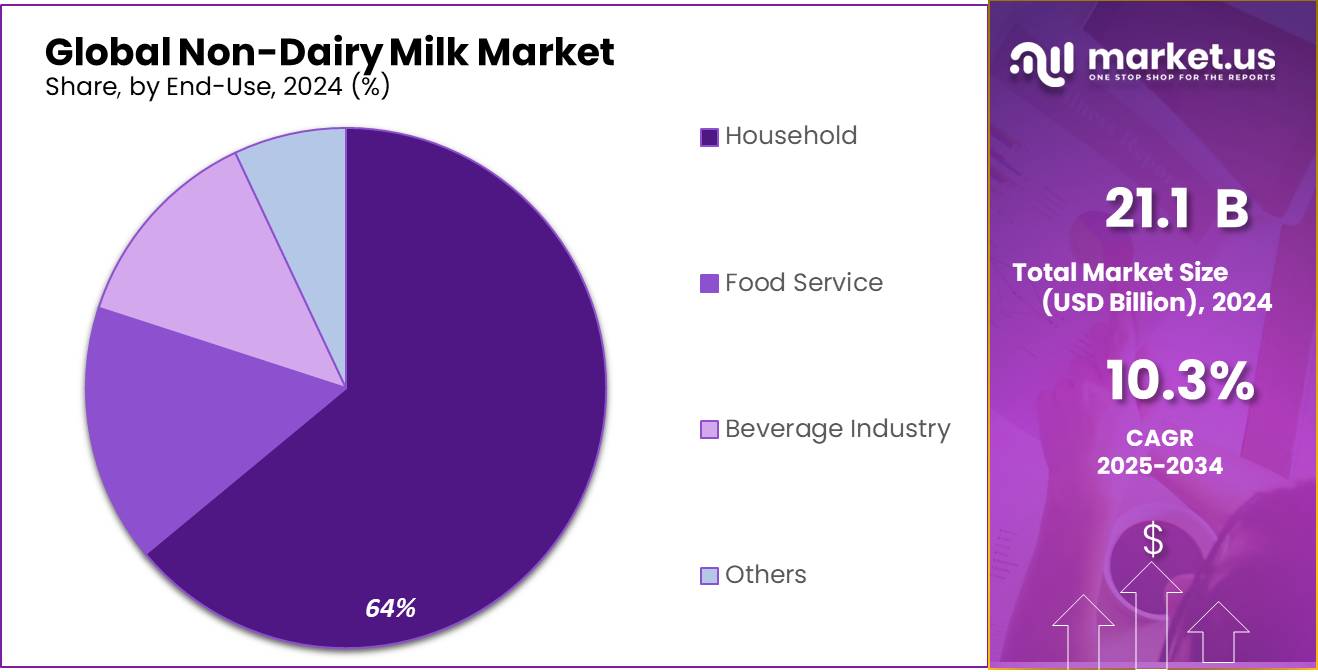

The Global Non-Dairy Milk Market size is expected to be worth around USD 56.2 Bn by 2034, from USD 21.1 Bn in 2024, growing at a CAGR of 10.3% during the forecast period from 2025 to 2034.

The non-dairy milk industry has experienced remarkable growth over the past decade, driven by evolving consumer preferences, health consciousness, and environmental concerns. Non-dairy milks, derived from plant sources such as almonds, soy, oats, and coconuts, offer alternatives to traditional dairy products, catering to those with lactose intolerance, vegan lifestyles, or dietary preferences. This shift has led to a dynamic market landscape with significant economic implications.

Several key drivers are Health Consciousness: A growing awareness of lactose intolerance and milk allergies has led consumers to seek alternatives. Notably, over 60% of the global population is affected by some level of milk allergy. Additionally, plant-based milks are often perceived as healthier options due to lower saturated fat content and the absence of cholesterol.

Product Innovation and Variety has seen a diversification of non-dairy milk options, including almond, soy, oat, and coconut milks, each catering to different taste preferences and nutritional needs. Oat milk, for instance, has gained significant traction, with sales in the U.S. reaching $213 million in 2020, making it the second most consumed plant milk after almond milk .

Geographic Expansion is increasing availability in emerging markets presents significant growth potential. As of 2025, China is projected to generate $10.28 billion in revenue from milk substitutes, highlighting the importance of this market.

Government initiatives and corporate policies are also influencing the industry’s trajectory. For instance, Starbucks announced in November 2024 that it would eliminate the extra charge for plant-based milks in its U.S. and Canada stores, aiming to promote sustainable choices among consumers . Such moves by major corporations not only make plant-based options more accessible but also signal a broader acceptance and normalization of non-dairy alternatives.

Key Takeaways

- The global non-dairy milk market is expected to grow from USD 21.1 billion in 2024 to USD 56.2 billion by 2034, at a CAGR of 10.3%.

- Almond milk dominates the market with a 61.10% share in 2024, driven by health benefits, low-calorie content, and growing consumer preference for dairy-free beverages.

- Carton packaging leads the market with a 72.20% share in 2024, favored for its sustainability, durability, and convenience in preserving non-dairy milk products.

- Household consumption accounts for 64.20% of the market in 2024, as plant-based milk becomes a staple in homes due to health awareness and dietary preferences.

- Supermarkets dominate distribution with a 48.20% share in 2024, offering a broad selection of non-dairy milk options, ensuring accessibility and convenience for consumers.

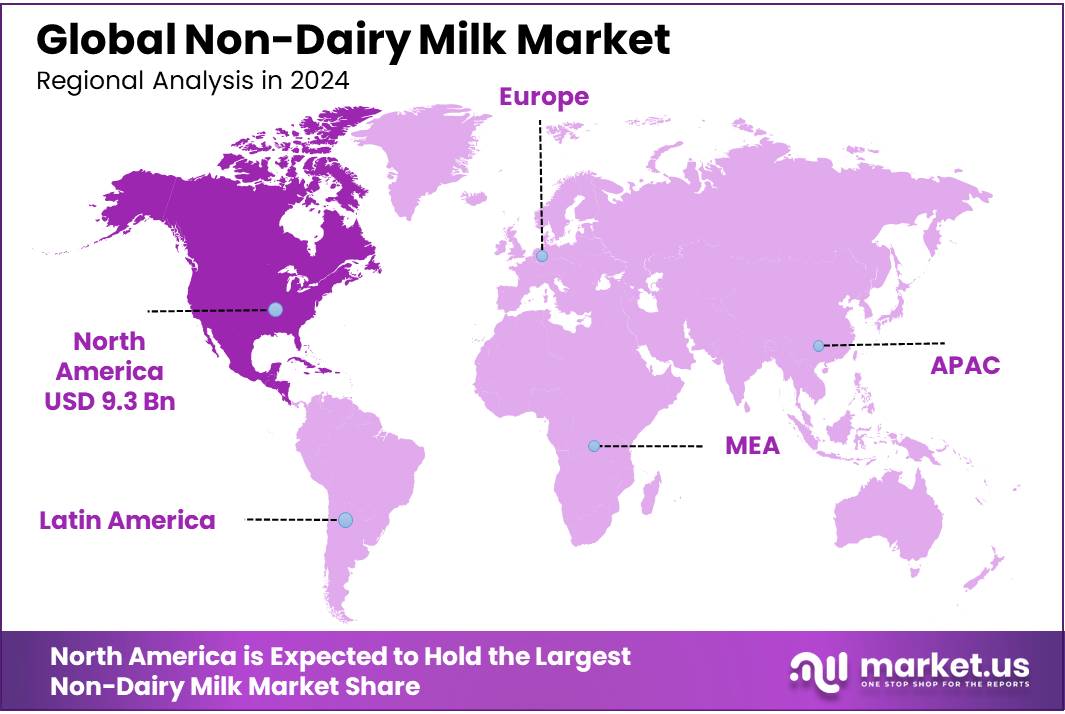

- North American non-dairy milk market is a dominant force in the global landscape, commanding a significant 44.10% market share, valued at approximately $9.3 billion.

By Formulation

Almond Milk Leads the Market with 61.10% Share in 2024

In 2024, Almond Milk held a dominant market position, capturing more than a 61.10% share of the non-dairy milk market. This remarkable performance can be attributed to the growing preference for plant-based alternatives among health-conscious consumers and those with lactose intolerance or dairy allergies. Almond milk’s smooth texture, mild flavor, and versatility in both cooking and beverages have contributed to its widespread appeal.

Over the years, the segment has witnessed steady growth, and in 2025, it is expected that almond milk will maintain its leadership, continuing to cater to a large consumer base seeking dairy-free options. The increasing availability of almond milk in various retail outlets, alongside its recognition as a low-calorie and nutrient-rich beverage, is likely to sustain its market dominance in the coming years.

By Packaging Type

Carton Packaging Dominates with 72.20% Share in 2024

In 2024, Carton packaging held a dominant market position, capturing more than a 72.20% share of the non-dairy milk market. This type of packaging has gained significant traction due to its convenience, durability, and ability to preserve the quality of the product for a longer period. Cartons are lightweight, easy to store, and widely accepted by consumers, making them the preferred choice for non-dairy milk brands.

As sustainability continues to be a growing concern, carton packaging, which is often recyclable, aligns well with consumer preferences for environmentally friendly solutions. By 2025, the carton segment is expected to retain its leading position as it remains the most popular and reliable packaging option in the market.

By End-Use

Household End-Use Dominates the Non-Dairy Milk Market with 64.20% Share in 2024

In 2024, Household consumption held a dominant market position, capturing more than a 64.20% share of the non-dairy milk market. The growing awareness of plant-based diets and the increasing demand for dairy-free alternatives have made non-dairy milk a staple in households worldwide. Consumers are increasingly opting for healthier, lactose-free, and environmentally friendly options, making household use the largest segment in the market.

This trend is further fueled by the convenience of non-dairy milk, which can easily replace traditional dairy milk in everyday use, from beverages to cooking. In 2025, the household segment is expected to maintain its strong position, driven by rising health-consciousness and the ongoing shift towards plant-based diets.

By Distribution Channel

Supermarkets Lead the Non-Dairy Milk Market with 48.20% Share in 2024

In 2024, Supermarkets held a dominant market position, capturing more than a 48.20% share of the non-dairy milk market. The convenience and accessibility of supermarkets have made them the go-to distribution channel for consumers seeking non-dairy milk options. With a wide variety of brands and packaging options available, supermarkets provide a one-stop shop for consumers looking to purchase non-dairy milk.

The steady increase in demand for plant-based beverages has driven supermarkets to expand their product offerings, making non-dairy milk readily available to a broad customer base. In 2025, supermarkets are expected to continue holding a significant market share as consumer preferences for convenience and variety remain strong.

Key Market Segments

By Formulation

- Almond Milk

- Original

- Unsweetened

- Sweetened

- Flavored

- Others

- Soy Milk

- Original

- Unsweetened

- Sweetened

- Flavored

- Others

- Coconut Milk

- Original

- Unsweetened

- Sweetened

- Flavored

- Others

- Oat Milk

- Original

- Unsweetened

- Sweetened

- Flavored

- Others

- Rice Milk

- Original

- Unsweetened

- Sweetened

- Flavored

- Others

- Others

By Packaging Type

- Carton

- Bottle

- Pouch

By End-Use

- Household

- Food Service

- Beverage Industry

- Others

By Distribution Channel

- Supermarkets

- Online Retail

- Health Food Stores

- Convenience Stores

- Others

Drivers

Growing Health Consciousness and Increasing Demand for Plant-Based Diets

One of the key driving factors behind the rapid growth of the non-dairy milk market is the increasing awareness of health and wellness among consumers. With rising concerns about lactose intolerance, allergies, and the overall health risks associated with dairy consumption, many individuals are turning to plant-based alternatives like almond, oat, and soy milk. In 2024, the demand for non-dairy milk in the United States alone increased significantly, with plant-based milk sales reaching over $2.5 billion, according to the Plant Based Foods Association. This shift in consumer behavior reflects a broader trend toward healthier lifestyles and more sustainable food choices.

The surge in plant-based milk consumption is also influenced by the growing popularity of veganism and vegetarianism, with more people adopting these diets for health, ethical, and environmental reasons. The rising trend is supported by numerous studies, including one from the Good Food Institute, which reports that the plant-based dairy sector grew by 20% from 2020 to 2021. These statistics underscore the changing attitudes toward dairy, with a clear preference for plant-based alternatives among consumers.

Government initiatives also play a significant role in promoting plant-based diets. For example, the European Union and the United States have seen the introduction of policies that encourage sustainable food systems and plant-based consumption. The U.S. Department of Agriculture (USDA) has advocated for a shift toward more plant-based options in its dietary guidelines, which in turn supports the growth of non-dairy milk options in the marketplace.

Restraints

High Cost of Non-Dairy Milk Products

One of the major restraining factors for the growth of the non-dairy milk market is the relatively high cost of plant-based milk compared to traditional dairy milk. While non-dairy milk offers a variety of benefits such as being lactose-free, vegan, and suitable for individuals with certain allergies, the price often makes it less accessible for many consumers. According to a report by the U.S. Department of Agriculture (USDA), plant-based milk can be up to three times more expensive than regular cow’s milk, depending on the type and brand. For instance, a gallon of almond milk typically costs around $3.99, while a gallon of dairy milk can be found for as low as $1.99.

This price gap is primarily due to the more expensive ingredients used in plant-based milk production, such as almonds, oats, and soy, which are often sourced from specialized farms. Additionally, the processing and packaging of non-dairy milk products add to the overall cost, making it harder for these products to compete on price with traditional dairy milk. For many budget-conscious consumers, this price difference remains a barrier to adopting plant-based milk options.

In response to this challenge, some governments have started introducing initiatives aimed at reducing the cost of plant-based alternatives. For example, the European Union has been providing subsidies to plant-based food producers to encourage sustainable agricultural practices and lower production costs. However, despite these efforts, the high cost of non-dairy milk remains a significant hurdle to widespread adoption, especially in lower-income regions or countries where dairy is the more affordable option.

Opportunity

Rising Consumer Demand for Plant-Based Alternatives

One major growth opportunity for the non-dairy milk sector is the increasing demand driven by changing consumer preferences, particularly among health-conscious individuals and those seeking more sustainable dietary choices. As people shift away from dairy for various reasons—such as lactose intolerance, veganism, and environmental concerns—the popularity of plant-based milk alternatives is rapidly rising. Non-dairy milk is perceived as a healthier option, with lower levels of saturated fats and more nutrients like fiber and antioxidants.

According to a report by the Plant-Based Foods Association (PBFA), U.S. retail sales of plant-based foods reached a value of $7.4 billion in 2023, which was an 11% increase from the previous year. Within this sector, plant-based milk alone grew by 9% in 2023, reaching $2.9 billion in sales. Almond milk remains the market leader, but oat and soy milk are catching up fast due to their perceived health benefits and versatility.

Governments and industries have recognized this shift and are providing various incentives to support the growth of the plant-based market. In Europe, for example, the European Union’s “Farm to Fork” strategy aims to make food systems fair, healthy, and environmentally-friendly. This includes supporting plant-based food production through research funding and eco-friendly farming initiatives.

Not only is there a demand for dairy alternatives, but consumers are also showing a preference for clean-label, non-GMO, and organic products. As a result, manufacturers in the non-dairy milk sector are responding by investing in innovation and product development to cater to these needs. Brands that successfully combine taste, health benefits, and sustainability will continue to thrive.

Trends

Rise in Plant-Based Milk Innovations and Government Support

One of the latest major trends in the non-dairy milk market is the significant rise in the innovation of plant-based milk products. This trend is being driven by increasing consumer demand for sustainable and health-conscious alternatives to dairy. Plant-based milks such as almond, oat, soy, and coconut milk are becoming increasingly popular, not just among vegans and those with dairy intolerances, but also with the wider health-aware consumer base.

Recent data indicate that oat milk sales, for example, have seen a remarkable surge. According to industry leaders and food organizations, oat milk sales in the United States grew by 131% in the past year alone. This growth outpaces that of other plant-based milks, reflecting a broader shift in consumer preferences towards options perceived as being more environmentally sustainable and healthier.

In response to this trend, food manufacturers are not just increasing the variety of available non-dairy milk products but are also investing in new technologies to improve taste and texture, making these alternatives more appealing to a broad audience. Innovations such as enhanced flavor infusion, improved nutritional profiles (like increased calcium and vitamin D fortification), and better emulsification techniques that mimic the creamy texture of dairy milk are key focus areas.

Government initiatives are also playing a crucial role in supporting the non-dairy milk market. Several governments worldwide have started to promote plant-based diets as part of their sustainability and health initiatives. For instance, the Canadian government has invested millions into the plant-based food sector, recognizing its potential to reduce carbon footprints and improve national health standards.

Moreover, public health campaigns are increasingly including recommendations for plant-based diets, which indirectly support the growth of the non-dairy milk market. These initiatives often highlight the lower cholesterol and saturated fat levels in plant-based milks compared to traditional dairy.

Regional Analysis

The North American non-dairy milk market is a dominant force in the global landscape, commanding a significant 44.10% market share, valued at approximately $9.3 billion. This region’s prominence is driven by a robust consumer shift towards plant-based diets, heightened awareness of lactose intolerance, and increasing concerns over animal welfare and environmental sustainability.

In the United States and Canada, consumer preferences are rapidly evolving, with a noticeable tilt towards almond, oat, and soy milks. Oat milk, in particular, has witnessed exponential growth, aligning with global trends. Market statistics reveal that sales of oat milk in North America surged by over 130% in the last year, outpacing other alternatives due to its environmental and health benefits. This surge is supported by both the influx of new consumers entering the plant-based market and existing consumers diversifying their non-dairy preferences.

Furthermore, the market is buoyed by governmental support, such as the U.S. Department of Agriculture’s (USDA) programs promoting plant-based food options through various health initiatives. Canadian government investments into the plant-based sector, including funding for research and development, also underscore the regional commitment to fostering sustainable food options.

Innovation remains a cornerstone of North America’s market strategy, with companies continually exploring new formulations to improve taste and texture, thereby enhancing consumer acceptance. These innovations are critical in catering to a demographic increasingly seeking variety and quality in plant-based products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Almond Breeze, a brand by Blue Diamond Growers, stands out in the non-dairy milk market for its extensive range of almond milk products. Known for its creamy texture and mild flavor, Almond Breeze caters to a health-conscious audience with options that are low in calories and rich in vitamins. Their innovation in flavored and barista blends has broadened their appeal among both direct consumers and coffee shop chains, reinforcing their market presence as leaders in almond-based non-dairy alternatives.

Traditionally known for their ice cream, Ben & Jerry’s has made significant strides in the non-dairy market with their line of vegan ice cream made from almond milk and sunflower butter. Their commitment to social justice and sustainable practices resonates well with the younger demographic. Ben & Jerry’s continues to innovate by introducing new flavors and limited editions, thereby maintaining strong brand loyalty and recognition in the non-dairy segment.

A global giant in the food industry, Danone has diversified its portfolio to include a variety of non-dairy products under brands like Silk and So Delicious. These products range from almond, soy, oat, and coconut milks, catering to a wide array of tastes and dietary needs. Danone focuses on sustainability and health, leveraging its extensive distribution network to dominate the non-dairy sector while continuously innovating in product development and marketing strategies.

Elmhurst 1925 has transformed from a traditional dairy brand to a plant-based milk innovator, offering a unique line of nut and grain milks that are minimally processed. Their products are known for being made with simple ingredients and without artificial additives, appealing to consumers looking for clean, whole-food options. Elmhurst’s focus on water conservation and eco-friendly packaging further strengthens its appeal to environmentally conscious consumers.

Top Key Players

- Almond Breeze

- Ben & Jerry’s

- Danone

- Elmhurst 1925

- General Mills

- Happy Cow Limited

- Malk

- Oatly

- Pacific Foods

- Ripple Foods

- Silk

- So Delicious

- Trader Joe’s

Recent Developments

In 2024 Almond Breeze , the almond milk market, where Almond Breeze is a key player, is valued at about $6.0 billion, reflecting its strong market position and consumer preference for almond milk.

As of 2024 Ben & Jerry’s, the brand has innovated by launching a new line of oat-based non-dairy ice cream, catering to the growing consumer demand for vegan and lactose-intolerant options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 21.1 Bn |

| Forecast Revenue (2034) | USD 56.2 Bn |

| CAGR (2025-2034) | 10.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Formulation (Almond Milk, Soy Milk, Coconut Milk, Oat Milk, Rice Milk, Others), By Packaging Type (Carton, Bottle, Pouch), By End-Use (Household, Food Service, Beverage Industry, Others), By Distribution Channel (Supermarkets, Online Retail, Health Food Stores, Convenience Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Almond Breeze, Ben & Jerry’s, Danone, Elmhurst 1925, General Mills, Happy Cow Limited, Malk, Oatly, Pacific Foods, Ripple Foods, Silk, So Delicious, Trader Joe’s |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |