Quick Navigation

Report Overview

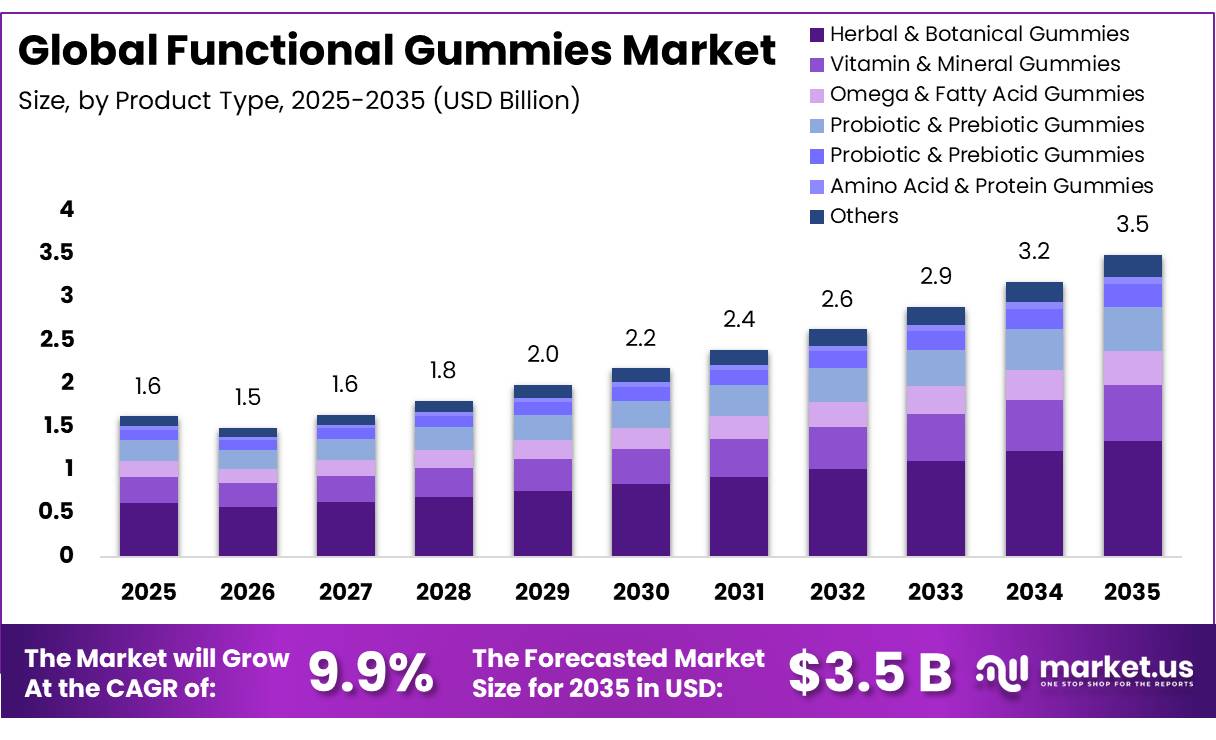

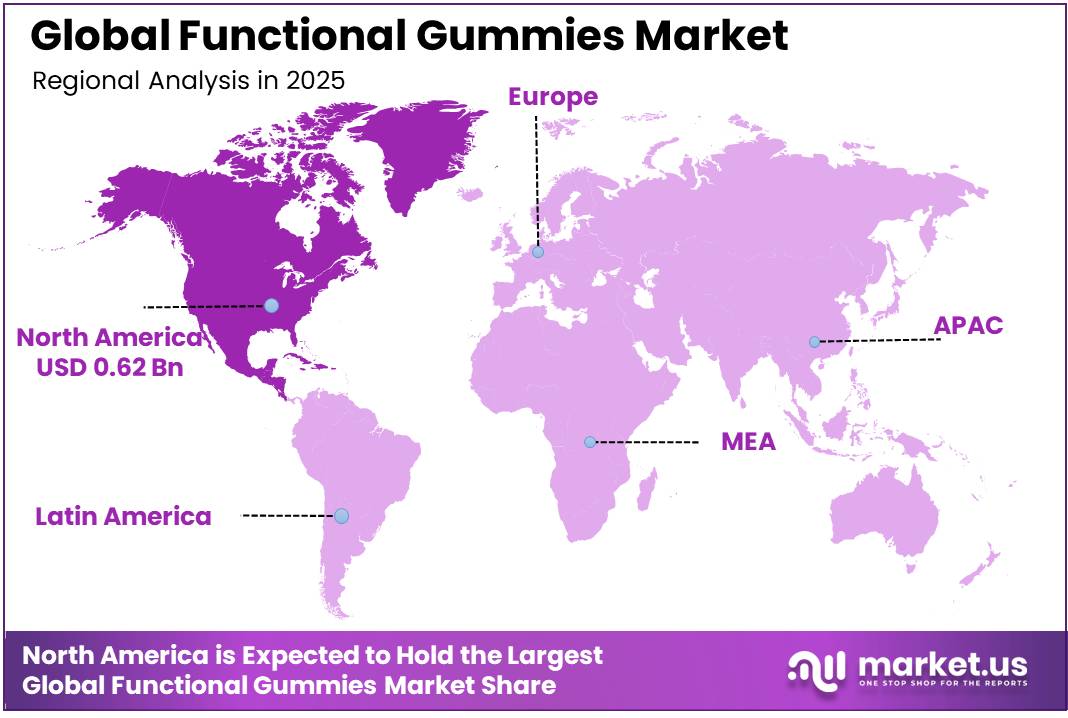

In 2025, the Global Functional Gummies Market was valued at USD 1.6 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.9%, reaching about USD 3.5 billion by 2035. In 2025, North America led the market, achieving over 38.2% share with a revenue of USD 0.62 billion.

The functional gummies industry has evolved from a niche dietary supplement category into a significant segment of the global health and wellness market. Functional gummies are chewable products formulated with vitamins, minerals, probiotics, botanicals, omega fatty acids, and other bioactive ingredients intended to support immunity, digestive health, cognitive performance, sleep, and overall well-being.

- The Council for Responsible Nutrition (CRN) reported that 74% to 75% of U.S. ad`ults used dietary supplements in 2023, reflecting strong consumer acceptance of nutrition-based wellness products.

Key Takeaways

- The Global Functional Gummies Market was valued at US$1.6 billion in 2025.

- The market is projected to grow at a CAGR of 9.9% and is estimated to reach US$3.5 billion by 2035.

- Herbal & Botanical Gummies dominated the product type segment, accounting for 38.4% share in 2025.

- Digestive Health led the functionality segment with a 30.2% share, also registering the fastest growth.

- Gelatin-based gummies dominated the ingredient source segment with a 74.3% share, while Plant-based is set to be the fastest-growing segment.

- Berry led the flavor segment with a 28.9% share and is also projected to be the fastest-growing flavor.

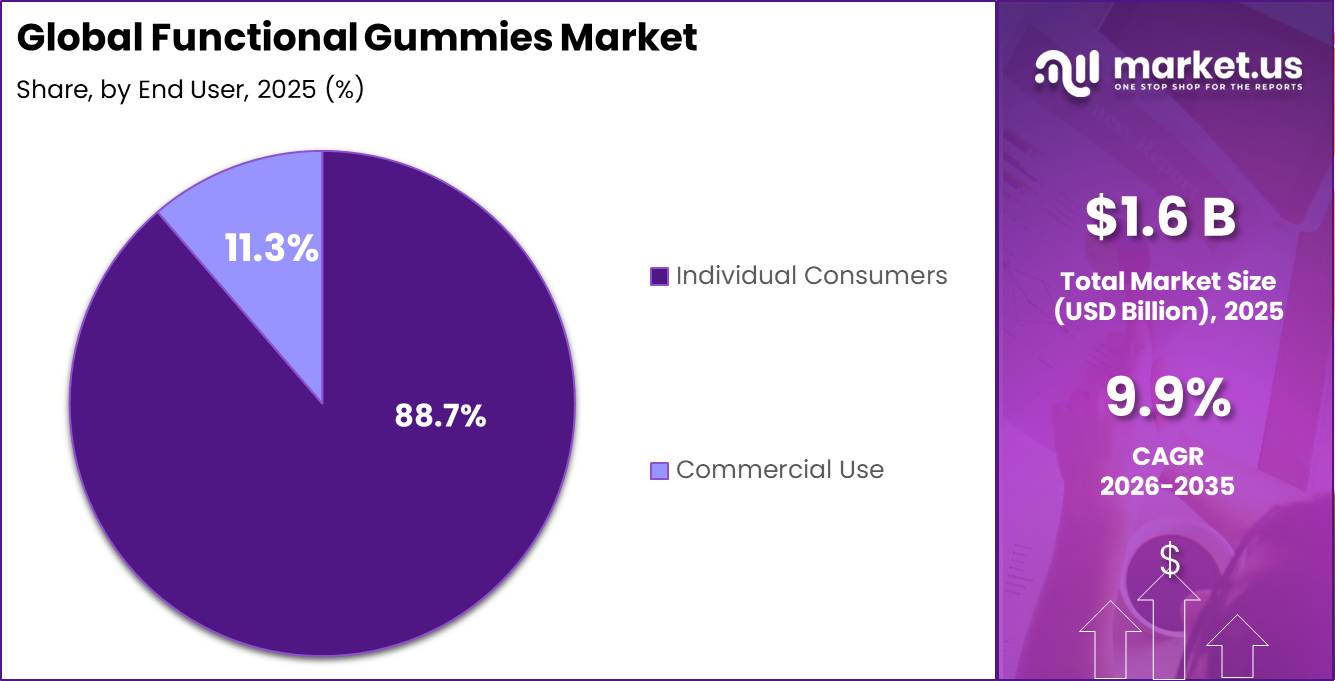

- Individual Consumers accounted for the largest share at 88.7% in the end-user segment and are also the fastest-growing segment.

- North America led the regional landscape with a 38.2% share in 2025, while Asia Pacific is projected to be the fastest-growing region.

Gummies have become one of the most preferred delivery formats due to ease of consumption and improved compliance among adults and children. Manufacturers are therefore investing in innovative formulations containing vitamins, probiotics, and plant-based ingredients to meet evolving consumer health demands.

Future growth opportunities are expected to emerge from clean-label formulations, sugar-reduced products, vegan gummies, and science-backed functional ingredients. Regulatory authorities continue to strengthen nutrition and health policies that support informed consumer choices.

For example, the European Commission’s Farm to Fork Strategy promotes healthier and more sustainable food systems, encouraging innovation in nutrition-focused products. Advances in ingredient encapsulation, probiotic stability, and personalized nutrition technologies are expected to further enhance product effectiveness and consumer adoption. As wellness-focused consumption patterns continue to expand globally, functional gummies are expected to remain an important delivery format within the broader nutraceutical and functional food industry.

Functional Gummies Market Segmentation

Product Type Analysis

Herbal & Botanical Gummies dominate the market due to growing preference for plant-based wellness solutions

In 2025, Herbal & Botanical Gummies held a dominant market position, capturing more than a 38.4% share of the functional gummies market. The segment’s leadership was supported by increasing consumer interest in natural health products made from botanical extracts and herbal ingredients. Products containing elderberry, turmeric, ashwagandha, ginger, chamomile, and other plant-based compounds gained strong acceptance among consumers seeking daily wellness support through convenient formats.

- In September 2025, the American Botanical Council reported that U.S. retail sales of herbal dietary supplements reached a record US$13.231 billion in 2024, increasing 4%, or approximately US$680 million, from the previous year.

Probiotic & Prebiotic Gummies is the fastest growing segment in the functional gummies market. Growth of this category has been fueled by rising consumer awareness regarding gut health and its connection to overall wellness. The growing popularity of preventive healthcare and daily wellness routines has encouraged wider adoption of digestive health supplements, helping this segment expand rapidly across multiple consumer groups. As interest in microbiome health continues to increase, Probiotic & Prebiotic Gummies are expected to witness sustained momentum in the coming years.

Functionality Analysis

Digestive Health dominates the market as consumers prioritize everyday gut wellness

In 2025, Digestive Health held a dominant market position, capturing more than a 30.2% share of the functional gummies market. The segment maintained its leadership as consumers increasingly focused on maintaining healthy digestion as part of their daily wellness routines. Functional gummies formulated with fiber, digestive enzymes, probiotics, and prebiotics gained strong popularity due to their convenience and pleasant taste. Many consumers viewed digestive health as a foundation for overall well-being, driving regular consumption of products designed to support gut balance and digestive comfort.

- In March 2025, the International Food Information Council found that 37% of U.S. consumers were seeking digestive or gut-health benefits from foods, beverages, or nutrients, up 7 percentage points from 2022.

Immunity Support is the fastest growing segment in the functional gummies market. During 2025 and moving into 2026, consumers increasingly adopted products that help support immune function as part of proactive health management. Gummies containing vitamins, minerals, botanical extracts, and other wellness-focused ingredients attracted strong interest due to their convenience and enjoyable consumption experience. The segment benefited from rising awareness of preventive healthcare, with consumers seeking simple ways to incorporate immune-supporting nutrients into their daily routines.

Ingredient Source Analysis

Gelatin-based gummies dominate the market due to proven texture and formulation advantages.

In 2025, Gelatin-based held a dominant market position, capturing more than a 74.3% share of the functional gummies market. The segment continued to lead because gelatin remains one of the most widely used ingredients for producing gummies with a soft texture, elasticity, and extended shelf stability. Manufacturers favored gelatin-based formulations due to their compatibility with a wide range of functional ingredients, including vitamins, minerals, probiotics, and botanical extracts. The ingredient also supports efficient large-scale production, making it a preferred choice across the dietary supplement industry.

- In June 2025, the UK National Diet and Nutrition Survey reported that 2% of participants identified as vegetarian, fewer than 5% identified as vegan, and another 4% followed a mainly vegetarian or vegan diet while occasionally consuming meat.

Plant-based is the fastest growing segment in the functional gummies market. During 2025 and into 2026, demand increased as more consumers sought vegan, vegetarian, and animal-free supplement options. Manufacturers expanded the use of plant-derived ingredients such as pectin, agar, and starch-based alternatives to meet changing dietary preferences. The segment gained momentum among consumers looking for clean-label products and those seeking alternatives that align with sustainability-focused lifestyles.

Flavor Analysis

Berry flavor dominates the market due to its broad consumer appeal and familiar taste

In 2025, Berry held a dominant market position, capturing more than a 28.9% share of the functional gummies market. The segment maintained its leading position because berry flavors are widely recognized and preferred across different age groups. Flavors such as strawberry, blueberry, raspberry, and mixed berries have long been associated with gummies, making them a popular choice among consumers seeking both taste and functionality. During 2025, the popularity of berry-flavored gummies remained strong as consumers increasingly looked for enjoyable supplement formats that could be easily incorporated into everyday routines.

- In September 2025, the USDA reported that U.S. cultivated blueberry production reached a record 5 million pounds in 2024, valued at US$1.15 billion. Around 55% was directed to the fresh market. Wild blueberry production totalled another 90.8 million pounds, with almost the entire crop used in processing, providing supply for juices, concentrates, extracts, and flavor formulations.

Apple is the fastest growing segment in the functional gummies market. Throughout 2025 and into 2026, apple-flavored gummies gained increasing attention from consumers looking for lighter and more refreshing flavor options. The flavor has attracted both younger and adult consumers due to its familiar taste and versatility across different wellness applications. Manufacturers have expanded their product offerings by introducing green apple, red apple, and blended fruit variations to create more distinctive flavor experiences.

End User Analysis

Individual Consumers dominate the market due to strong demand for daily wellness supplements.

In 2025, Individual Consumers held a dominant market position, capturing 88.7% share of the functional gummies market. The segment led the market as functional gummies became an increasingly popular part of personal health and wellness routines. Consumers across different age groups preferred gummies because they are convenient, easy to consume, and available in a variety of flavors and health-focused formulations. Products targeting immunity, digestive health, sleep support, energy, and general nutrition witnessed strong demand from individuals seeking simple ways to maintain their well-being.

Commercial Use is the fastest growing segment in the functional gummies market. Throughout 2025 and into 2026, businesses increasingly incorporated functional gummies into wellness, nutrition, and health-related programs. The segment has gained momentum across sectors such as fitness centers, healthcare facilities, corporate wellness initiatives, hospitality services, and specialty nutrition providers. Organizations are showing greater interest in convenient nutritional products that can support consumer engagement and wellness-focused experiences.

Key Market Segments

By Product Type

- Herbal & Botanical Gummies

- Vitamin & Mineral Gummies

- Omega & Fatty Acid Gummies

- Probiotic & Prebiotic Gummies

- Collagen Gummies

- Amino Acid & Protein Gummies

- Others

By Functionality

- Digestive Health

- Immunity Support

- Heart Health

- Bone & Joint Health

- Cognitive Health & Focus

- Stress Relief & Mental Wellness

- Children’s Nutrition

- Others

By Ingredient Source

- Plant-based

- Gelatin-based

- Marine-based

By Flavor

- Berry

- Citrus

- Tropical

- Apple

- Grape

- Mixed Fruit

- Others

By End User

- Individual Consumers

- Commercial Use

Driver Analysis

Preventive wellness demand linked to obesity and nutrient gaps

The strongest structural demand driver is the migration of consumers from episodic treatment to everyday preventive nutrition, which directly favors gummies because they convert compliance from a “pill-taking” task into a food-like routine.

In the U.S., CDC reports adult obesity prevalence at 41.9%, representing more than 100 million adults with obesity and more than 22 million with severe obesity, while NIH’s Office of Dietary Supplements states adults 19–70 need 15 mcg (600 IU) of vitamin D daily and adults 71+ need 20 mcg (800 IU), creating a large addressable pool for nutrient-delivery formats built around daily use cases such as immunity, bone health, sleep, and metabolic support.

The CAGR lift is estimated at about +2.1 percentage points because the driver is broad-based, recurring, and linked to high-prevalence public-health conditions rather than short-lived wellness fads.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive wellness demand linked to obesity and nutrient gaps | +2.1% | North America core, EU urban, APAC upper-income corridors | Medium term (2-4 years) |

| E-commerce scale-up and repeat-purchase convenience for supplements | +1.7% | North America core, EU, APAC corridors, South America spill-over | Short term (≤ 2 years) |

| Sugar-control reformulation and better-for-you positioning | +1.3% | North America core, EU core, developed APAC | Short term (≤ 2 years) |

| Regulatory tightening on cGMP, label claims, and dosage compliance | +1.0% | North America core, EU core | Medium term (2-4 years) |

| Nutrient personalization around vitamin D, immunity, and daily adherence | +1.5% | North America core, Europe mature markets, APAC metro demand nodes | Medium term (2-4 years) |

| Institutional nutrition rules accelerating low-sugar format innovation | +0.8% | United States core with formulation spill-over to Canada and EU | Long term (≥ 4 years) |

Restraint Analysis

Pectin and hydrocolloid sourcing

Pectin-based gummies face a narrower formulation window than many soft-chew formats because pectin performance is sensitive to source quality, solids balance, pH, and cooking conditions, while imported pectic substances remain exposed to customs classification and external supply concentration under HS 1302.20, making the category vulnerable to lead-time elongation and vendor qualification bottlenecks.

In operating terms, a 2-4 week delay in pectin availability can idle specialized vegan gummy lines, raise safety-stock requirements by 20-35 percent, and push working-capital absorption higher just as brands are also carrying more packaging and active-ingredient inventory to reduce stockout risk; if substitution trials are required, commercial launch delays can easily run 6-10 weeks because texture, active stability, and sensory output must all be revalidated.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| cGMP enforcement risk | -1.4% | North America core | Short term (≤ 2 years) |

| Claims and label tightening | -1.1% | North America core, EU | Short term (≤ 2 years) |

| Sugar and syrup cost volatility | -0.9% | North America core, EU, APAC corridors | Medium term (2-4 years) |

| Pectin and hydrocolloid sourcing | -0.7% | EU, North America core, APAC export hubs | Medium term (2-4 years) |

| Novel ingredient authorization delays | -1.3% | EU, UK spillover, selective APAC premium channels | Medium term (2-4 years) |

| Tariff and import-cost exposure | -0.6% | North America import channels | Long term (≥ 4 years) |

Opportunity Analysis

Public health co‑branded gummies

Public health co‑branded gummies represent a white‑space where manufacturers collaborate directly with national and regional health authorities on behavior‑change campaigns (vitamin D sufficiency, iron in women, basic micronutrient adequacy), using gummies as the preferred vehicle for hard‑to‑reach or low‑adherence populations, rather than relying solely on retail‑driven supplement uptake.

Statistics from Australia’s Bureau of Statistics show that one in three people (33.6%) used dietary supplements in 2023, up from 28.5% in 2011–12, and vitamin/mineral supplements are the most common type, yet 65–70% of the population remain non‑daily users, implying a large pool of partially or non‑engaged individuals.

Structuring co‑branded products around simple, government‑endorsed health messages and distribution through schools, community clinics and employer programs could tap into an incremental TAM wherein 5–10% of non‑daily supplement users adopt low‑ticket gummy regimens at annual spend of USD 10–30 per capita, creating a multi‑billion dollar revenue layer with marketing costs 25–40% lower than traditional consumer campaigns due to subsidized or shared outreach.

Because these formats would be designed around measurable public health objectives rather than current discretionary wellness drivers, manufacturers could negotiate volume‑based contracts that stabilize capacity utilization, reduce waste and lift EBITDA margins by 2–3 percentage points, translating to roughly +2.3 points of CAGR upside if scaled in North America, the EU and APAC urban centers over the next 2–3 years as governments increasingly seek palatable interventions to improve micronutrient status.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Clinical-grade metabolic gummies | +2.8% | North America, EU, Japan | Medium term (2-4 years) |

| Public health co-branded gummies | +2.3% | North America, EU, APAC urban | Short term (≤ 2 years) |

| Regulated pediatric and women’s health gummies | +2.0% | North America, EU, Australia | Medium term (2-4 years) |

| EFSA/FOSHU-aligned novel ingredient gummies | +1.9% | EU, Japan | Long term (≥ 4 years) |

| Low-sugar, high-fiber clinical nutrition gummies | +1.7% | North America, EU, APAC | Medium term (2-4 years) |

| Digital adherence and DTC subscription gummies | +1.5% | North America core, EU | Short–medium term (≤ 4 years) |

Challenges Analysis

Ingredient and NDI/novel approvals lag

The functional gummies segment depends heavily on rapid incorporation of new botanical extracts, probiotics, nootropics and specialised micronutrients, yet the regulatory treatment of “new dietary ingredients” in the US, “novel foods” and new supplement substances in the EU, and new nutraceutical ingredients under India’s Section 22 and Nutra Regulations creates a chronic lag between scientific discovery, formulation work and legally marketable gummy products.

In the US, any dietary ingredient not marketed before October 15, 1994 generally requires a New Dietary Ingredient notification filed at least 75 days before introduction, with substantive safety evidence around dose, conditions of use and history of consumption; in the EU, candidate substances can spend 12–24 months in assessment pipelines before gaining approval, while in India a component not listed in the relevant schedules must secure Food Safety and Standards Authority of India clearance, adding further months of dossier preparation and review.

For a global functional gummy launch containing two or three such newer actives, staggered approval timing can create 18–30 month gaps between first‑market and last‑market entry, resulting in opportunity costs where brands may lose 20–30% of peak‑year revenue in stricter jurisdictions simply because they cannot synchronise launches, while also bearing parallel formulation costs for interim region‑specific variants that omit the pending ingredients.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Multi-regime nutra compliance load | -1.2% | North America, EU regulatory hubs, India, East Asia | Medium term (2–4 years) |

| Sugar, HFSS and UPF policy pressure | -1.0% | North America, EU, India, GCC, Latin America | Long term (≥ 4 years) |

| Ingredient and NDI/novel approvals lag | -0.9% | US, EU, India, China, ASEAN | Medium term (2–4 years) |

| cGMP, quality and contamination risk | -0.8% | Global manufacturing clusters | Medium term (2–4 years) |

| Logistics, cold chain and packaging stress | -0.7% | APAC logistics corridors, EU–US lanes, Emerging markets | Short term (≤ 2 years) |

| Scientific substantiation and claim risk | -0.6% | North America core, EU, India urban | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Global Supply Chain Disruptions and Ingredient Costs Influence Functional Gummies Market.

The ongoing geopolitical tensions and military conflicts in regions such as Eastern Europe and the Middle East have created challenges for the functional gummies market during 2025 and 2026. While functional gummies are not directly linked to defense-related industries, the sector depends heavily on global supply chains for ingredients, packaging materials, manufacturing inputs, and international transportation. As a result, disruptions caused by war have indirectly affected production and distribution activities.

Many functional gummy manufacturers source vitamins, botanical extracts, sweeteners, gelatin, pectin, and specialty ingredients from multiple countries. Increased shipping costs, longer transit times, and periodic disruptions in trade routes have raised procurement expenses for manufacturers. Energy price fluctuations associated with geopolitical instability have also increased production and logistics costs, particularly for companies operating large manufacturing facilities.

On the demand side, consumer interest in health, immunity, and preventive wellness products has remained resilient. In some regions, concerns about personal well-being have even supported demand for nutritional supplements and functional gummies. Although geopolitical conflicts have created cost pressures and operational challenges, the industry continues to adapt through supply chain adjustments, product innovation, and broader sourcing strategies, helping sustain overall market stability.

Regional Analysis

North America Leads Functional Gummies Market with Strong Consumer Adoption

North America emerged as the dominant region in the Functional Gummies market, accounting for 38.2% of the global market share and generating approximately USD 0.62 billion in revenue in 2025. The region’s leadership is supported by a highly developed dietary supplement industry, strong consumer awareness regarding preventive healthcare, and widespread adoption of convenient nutrition products. Functional gummies have gained significant popularity among adults seeking daily support for immunity, digestive health, sleep, energy, and overall wellness.

The United States remains the largest contributor within the region due to high supplement usage rates. The presence of established supplement manufacturers, extensive retail networks, and growing demand for personalized nutrition solutions continues to strengthen regional market performance. Product innovation, including sugar-reduced, vegan, and clean-label gummies, has further accelerated consumer acceptance across North America.

Asia-Pacific is witnessing steady expansion due to increasing urbanization, changing lifestyles, and growing awareness of wellness-focused products. Rising disposable incomes and expanding access to dietary supplements through retail and e-commerce channels are contributing to market development across several countries in the region.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Functional Gummies market exhibits a moderately fragmented structure, with several global dietary supplement manufacturers, nutraceutical companies, and specialty wellness brands competing across multiple product categories. No single company controls a dominant share of the global market, as consumer demand is spread across immunity, digestive health, sleep support, energy, beauty, and personalized nutrition gummies. The market is characterized by continuous product innovation, strong brand positioning, and expanding online distribution channels.

These companies continue to strengthen their market presence through new product launches, expansion of plant-based gummy portfolios, and investments in science-backed formulations. Many manufacturers are also focusing on sugar-reduced, vegan, and personalized nutrition products to attract health-conscious consumers. Alongside these major players, numerous regional and niche brands operate in specific health categories, further contributing to market fragmentation.

The Major Players in The Industry

- ABH Natures

- Better Nutritionals

- Bettera Wellness

- Cava Pharma

- Herbaland

- Hero Nutritionals

- Makers Nutrition

- Nutra Solutions

- Procaps

- Santa Cruz Nutritionals

- Seven Seas Ltd

- SMP Nutra

- Superior Supplement Manufacturing

- The Bountiful Company

- Vitakem Nutraceutical

Key Development

- In July 2025, Cava Pharma continued to focus on nutraceutical gummies from Canada, offering kids’ gummies, adult gummies, and non-gummy supplements. The company emphasized 100% natural flavours and child-friendly formats, supporting demand for easy-to-consume functional nutrition products.

- In March 2025, Better Nutritionals continued to support the functional gummies sector through its high-end contract manufacturing facility in Gardena, California. The company focused on gummy and chocolate supplement production, serving brands that require customized formulations, quality certifications, and scalable production support.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.6 Bn |

| Forecast Revenue (2035) | USD 3.5 Bn |

| CAGR (2026-2035) | 9.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Herbal & Botanical Gummies, Vitamin & Mineral Gummies, Omega & Fatty Acid Gummies, Probiotic & Prebiotic Gummies, Collagen Gummies, Amino Acid & Protein Gummies, and Others), By Functionality (Digestive Health, Immunity Support, Heart Health, Bone & Joint Health, Cognitive Health & Focus, Stress Relief & Mental Wellness, Children’s Nutrition, and Others), By Ingredient Source (Plant-based, Gelatin-based, and Marine-based), By Flavor (Berry, Citrus, Tropical, Apple, Grape, Mixed Fruit, and Others), By End User (Individual Consumers and Commercial Use) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ABH Natures, Better Nutritionals, Bettera Wellness, Cava Pharma, Herbaland, Hero Nutritionals, Makers Nutrition, Nutra Solutions, Procaps, Santa Cruz Nutritionals, Seven Seas Ltd, SMP Nutra, Superior Supplement Manufacturing, The Bountiful Company, Vitakem Nutraceutical |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |