Quick Navigation

Report Overview

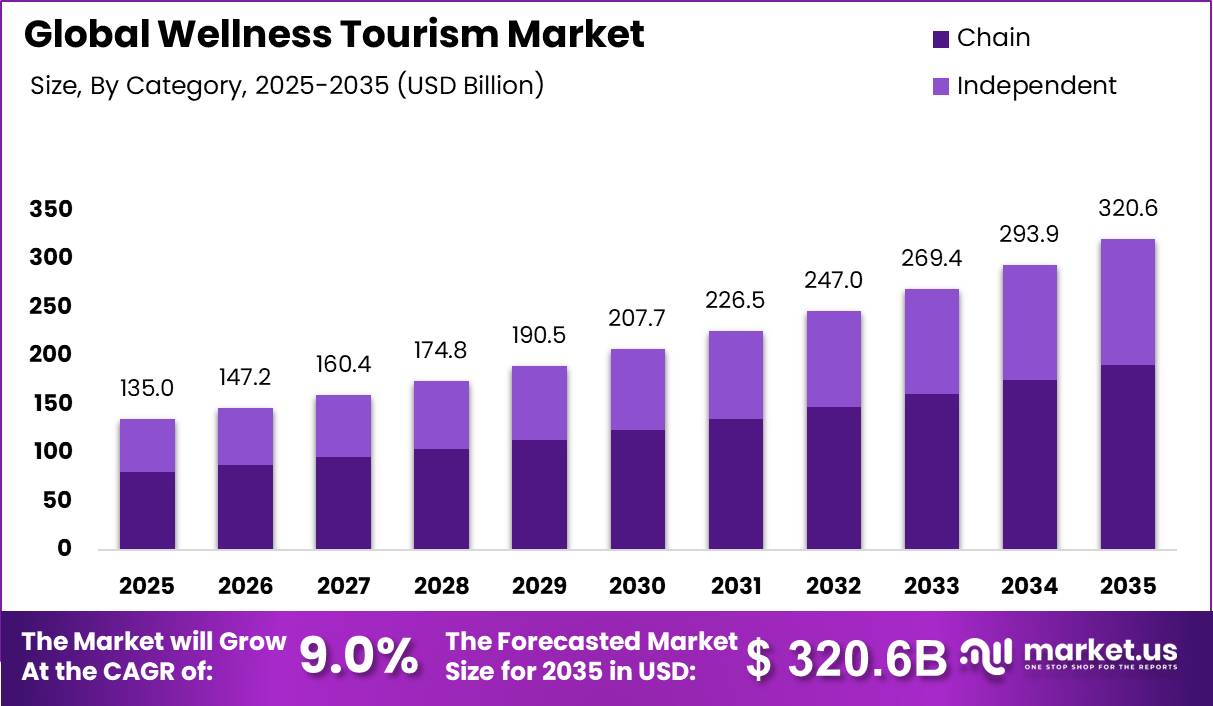

Global Wellness Tourism Market size is expected to be worth around USD 320.6 Billion by 2035 from USD 135.0 Billion in 2025, growing at a CAGR of 9.0% during the forecast period 2026 to 2035. This trajectory reflects a structural shift in how consumers allocate discretionary health spending globally.

The wellness tourism market covers travel experiences where health improvement, disease prevention, and mental and physical recovery are primary motivations rather than incidental benefits. This market spans resort and spa stays, medical wellness retreats, Ayurvedic and traditional medicine programs, corporate burnout recovery travel, and longevity-focused health travel. This means the market serves both individual consumers and institutional buyers such as corporate employers.

Key Takeaways

- Global Wellness Tourism Market was valued at USD 135.0 Billion in 2025.

- The market is forecast to reach USD 320.6 Billion by 2035, growing at a CAGR of 9.0%.

- By Category, Chain hotels dominate with a 59.7% market share in 2025.

- By Type, Resorts and Spa hold the leading position with a 39.6% share.

- By Booking Mode, Online Travel Agencies account for 51.5% of bookings.

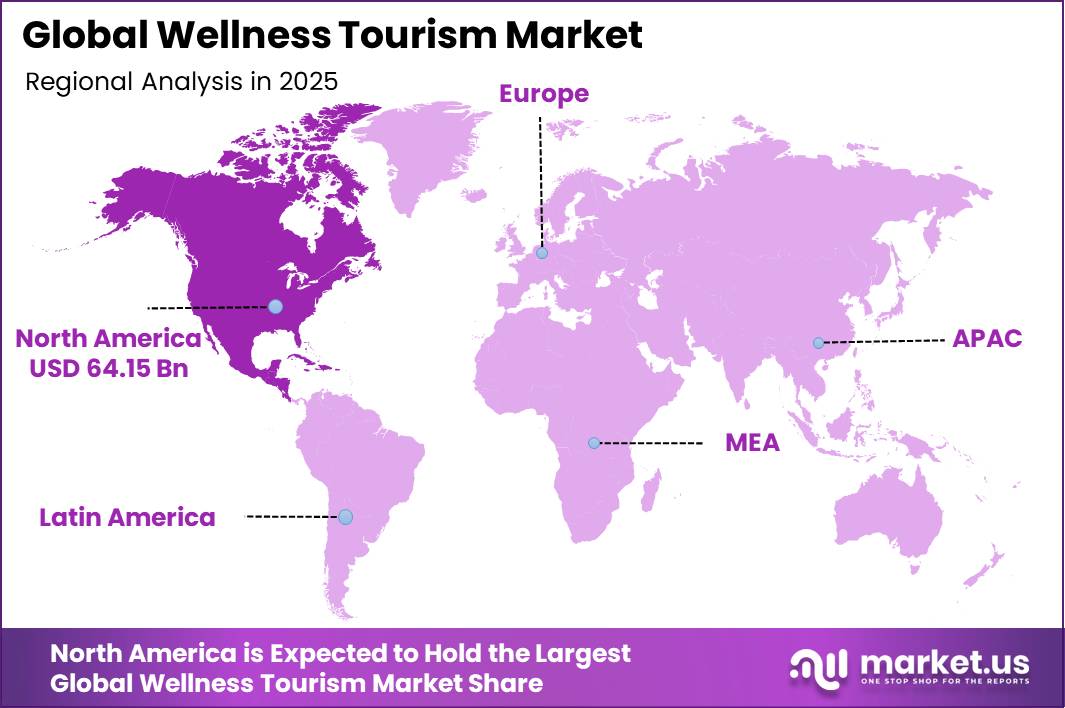

- North America leads all regions with a 47.50% share, valued at USD 64.15 Billion.

According to the Global Wellness Institute, wellness tourism generated approximately $894 billion in global spending in 2024, reflecting a strong post-pandemic recovery in health-motivated travel. This scale confirms that wellness tourism has moved from a niche premium segment into a mainstream consumer spending category with consistent institutional investment.

Data from the Global Wellness Institute shows wellness tourism expenditure climbed from $439 billion in 2012 to $720.4 billion in 2019, while total wellness tourism trips rose from 524.4 million to 936.4 million over the same period. This volume growth signals that wellness travel is broadening beyond high-net-worth consumers into the aspirational middle class, creating addressable demand at multiple price points.

Governments across Southeast Asia and Western Europe have positioned wellness tourism as a strategic export sector. Regulatory frameworks in Thailand, India, and Germany formally recognize wellness and traditional medicine tourism as distinct hospitality categories. This creates structured entry conditions for global operators seeking cross-border scale and government-backed destination partnerships.

Category Analysis

Chain dominates with 59.7% due to standardized service delivery and global loyalty networks.

In 2025, Chain held a dominant market position in the By Category segment of the Wellness Tourism Market, with a 59.7% share. Large chain operators benefit from centralized procurement, brand-level wellness certification, and cross-property loyalty programs that drive repeat bookings. This structural advantage limits independent operators from competing on price and consistency at scale.

Independent wellness properties hold 40.3% of the market by appealing to travelers who prioritize cultural authenticity and specialized treatment protocols unavailable within standardized chain offerings. Independent operators face higher customer acquisition costs but retain greater pricing flexibility for premium niche experiences. In January 2026, Indian Hotels Company Limited completed its acquisition of a 51% stake in Sparsh Infratech, making Atmantan Wellness Resort a subsidiary and signaling that branded consolidation of independent wellness assets is an active strategy.

Type Analysis

Resorts and Spa dominate with 39.6% due to integrated physical and mental recovery programming.

In 2025, Resorts and Spa held a dominant market position in the By Type segment of the Wellness Tourism Market, with a 39.6% share. These properties offer full-immersion wellness environments combining therapeutic treatments, nutrition programming, and fitness facilities under one roof. Operators in this sub-segment command the highest per-night yields in the entire wellness hospitality stack.

Business Hotels capture 25% of the wellness tourism market by embedding wellness amenities into corporate travel infrastructure, targeting executives who require stress management and recovery services alongside conference facilities. This dual positioning allows business hotel operators to generate wellness revenue without building standalone retreat infrastructure. As a result, corporate travel managers are increasingly evaluating wellness provisions as a baseline procurement criterion.

Airport Hotels hold a 17% share by serving transit travelers seeking short-duration recovery between long-haul flights, a segment that prioritizes sleep, hydration, and decompression over extended therapy programs. This sub-segment benefits from guaranteed foot traffic and predictable demand patterns tied to flight schedules rather than seasonal tourism cycles.

Booking Mode Analysis

Online Travel Agencies dominate with 51.5% due to price comparison access and digital booking convenience.

In 2025, Online Travel Agencies held a dominant market position in the By Booking Mode segment of the Wellness Tourism Market, with a 51.5% share. OTA dominance gives platform operators significant pricing leverage over wellness properties, particularly independent resorts with limited direct marketing budgets. This means wellness operators who fail to build direct booking channels face long-term margin compression as OTA commission rates rise.

Direct Booking channels serve high-intent travelers who have already selected a specific property and seek personalized pre-arrival wellness consultation. Direct bookings allow operators to capture full revenue without commission deductions and to collect first-party guest health data that improves treatment personalization. This creates a strong commercial case for operators to invest in CRM infrastructure and direct digital marketing capabilities.

Travel Agents retain a meaningful role in the luxury wellness segment by curating multi-property itineraries combining medical screenings, retreat programs, and post-treatment recovery stays across multiple destinations. High-net-worth clients booking longevity and regenerative health programs continue to rely on specialist agents for vetting clinical credentials and managing complex cross-border logistics.

Key Market Segments

By Category

- Chain

- Independent

By Type

- Resorts and Spa

- Business Hotels

- Airport Hotels

- Holiday Hotels

- Others

By Booking Mode

- Direct Booking

- Travel Agents

- Online Travel Agencies

Drivers

Healthy ageing travel demand is a long-term growth driver as the global population aged 60 and above is projected to grow from 1.0 billion in 2020 to 1.4 billion by 2030, reaching 2.1 billion by 2050. The 80+ age group is expected to triple to 426 million people. Older travelers typically stay four to seven nights, generating higher per-visit yield than traditional leisure travelers. Destinations combining accessibility, medical support, and preventive wellbeing services are well positioned to capture this expanding demographic.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border travel normalization | +2.4% | Europe core, Middle East, Americas, APAC corridors | Short term (≤ 2 years) |

| Premium wellness spend expansion | +2.1% | North America core, EU, GCC, Southeast Asia | Medium term (2-4 years) |

| Healthy ageing travel demand | +1.8% | Japan, EU, North America, affluent APAC | Long term (≥ 4 years) |

| Asia-Pacific destination recovery | +1.6% | Thailand, Indonesia, Japan, Korea, India | Thailand, Indonesia, Japan, Korea, India |

| Preventive health consumer shift | +1.5% | North America, EU, urban APAC, GCC | Medium term (2-4 years) |

| Higher-yield destination repositioning | +1.3% | Southern Europe, GCC, SEA, Latin America | Medium term (2-4 years) |

Restraints

Climate-exposed destination risk is constraining wellness tourism growth because many leading destinations occupy climate-sensitive coastal, tropical, desert, and island regions. European climate assessments released in 2026 show travelers are shifting away from peak-summer Mediterranean destinations toward cooler locations and off-season travel. In 2025, parts of Spain recorded temperatures near 45.8°C, prompting heat-related restrictions on outdoor hospitality activities. These conditions directly reduce the commercial viability of outdoor wellness offerings including yoga, nature immersion, and recovery programs.

Operators face higher expenditures on cooling technologies, water conservation systems, and climate-adaptation infrastructure as weather extremes increase in frequency. Increasing heatwaves and droughts raise operational complexity and insurance costs simultaneously. This means operators in Mediterranean, island, and high-temperature markets must absorb rising capital costs while managing shrinking peak operating windows, making new investment decisions in these zones structurally riskier.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Travel cost inflation | -2.1% | Europe, North America, long-haul corridors | Medium term (2-4 years) |

| Climate-exposed destination risk | -1.8% | Mediterranean, GCC, South Asia, islands | Long term (≥ 4 years) |

| Wellness-medical regulatory limits | -1.6% | EU, U.S., GCC, advanced APAC | Long term (≥ 4 years) |

| Asset-heavy development economics | -1.4% | Resort markets globally, urban premium hubs | Medium term (2-4 years) |

| Geopolitical route disruption | -1.3% | Middle East, Eastern Europe, Asia corridors | Short term (≤ 2 years) |

| Aging-infrastructure service ceiling | -1.1% | Legacy spa towns, island resorts, Europe | Medium term (2-4 years) |

Challenges

Climate-driven destination stress is a significant long-term challenge as rising temperatures and environmental pressures alter travel patterns and destination attractiveness across coastal, island, and high-temperature wellness markets. Wellness resorts in these zones face growing risks from extreme weather events that reduce outdoor programming viability and shift seasonal demand. Adapting to these conditions requires investments in cooling systems, shaded facilities, and climate-resilient infrastructure.

Operating and capital costs for climate adaptation may increase by 5% to 15% over a decade for affected operators. Tourism-related carbon emissions are projected to increase by 25% by 2030 under a business-as-usual scenario, intensifying regulatory and reputational pressure on operators to decarbonize. These twin cost and compliance pressures are reshaping destination planning and shifting long-term investment toward more climate-resilient wellness locations.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Specialized wellness labour gaps | -1.9% | North America, EU, GCC, resort APAC | Long term (≥ 4 years) |

| Persistent tourism inflation | -1.7% | Europe, North America, key leisure hubs | Medium term (2-4 years) |

| Climate-driven destination stress | -1.6% | Mediterranean, island resorts, South Asia | Long term (≥ 4 years) |

| Volatile geopolitical and safety risk | -1.4% | Middle East, Eastern Europe, select APAC | Medium term (2-4 years) |

| Fragmented health regulatory alignment | -1.3% | EU regulatory hubs, North America, GCC | Long term (≥ 4 years) |

| Capacity and infrastructure bottlenecks | -1.1% | High-demand coastal and heritage hubs | Medium term (2-4 years) |

Opportunities

Employer-funded wellness retreats represent a near-term revenue opportunity as companies invest in structured wellbeing, resilience, and burnout-reduction programs for employees. These retreats are positioned as measurable workforce engagement and retention initiatives rather than discretionary perks. Typical programs span two to four days, combining wellness experiences with coaching, team-building, and professional development activities.

Corporate wellness retreat contracts are commonly valued at $800 to $2,500 per employee, creating a scalable B2B revenue stream for operators. Direct employer partnerships reduce customer acquisition costs by 30% to 50% compared with consumer-focused marketing models. Additional services such as executive coaching, health diagnostics, and family participation options can increase total contract value by 15% to 25%, improving per-booking profitability for operators who invest in corporate sales infrastructure.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Longevity clinic travel | +2.6% | North America core, GCC, EU, Thailand, Singapore | Medium term (2-4 years) |

| Employer-funded wellness retreats | +1.9% | U.S., Western Europe, Singapore, Australia | Short term (≤ 2 years) |

| Secondary-city medical wellness hubs | +2.1% | India, SEA, Eastern Europe, LATAM, MENA | Medium term (2-4 years) |

| Subscription-led recovery travel | +1.5% | North America, EU, Japan, Korea | Medium term (2-4 years) |

| Senior preventive travel programs | +2.3% | Japan, EU, North America, affluent APAC | Long term (≥ 4 years) |

| Wellness real estate integration | +1.8% | GCC, Southern Europe, U.S., Southeast Asia | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Wellness Tourism Market with a Market Share of 47.50%, Valued at USD 64.15 Billion

North America holds the largest share of the global wellness tourism market at 47.50%, equivalent to USD 64.15 Billion in 2025. The region benefits from high per-capita health spending, established corporate wellness purchasing infrastructure, and a dense network of medically accredited resort properties. Consumer willingness to pay premium rates for preventive health travel reinforces North America’s structural lead over all other regions.

Europe represents the second-largest wellness tourism region, anchored by established spa town destinations in Germany, Austria, and Central Europe alongside Mediterranean resort markets in Spain, Italy, and France. European climate assessments released in 2026 show that travelers are shifting away from peak-summer Mediterranean destinations toward cooler locations and off-season travel, reshaping seasonal demand patterns across the region. This means European operators must diversify their programming calendars to maintain occupancy year-round.

Asia Pacific is a structurally important growth region for wellness tourism, driven by Thailand, India, Japan, South Korea, and Indonesia. Traditional medicine systems including Ayurveda and Traditional Chinese Medicine provide Asia Pacific destinations with differentiated treatment offerings unavailable in Western resort markets. This creates pricing power at the premium end and positions the region as a preferred long-haul destination for medically curious travelers from North America and Europe.

Latin America serves a growing domestic wellness travel base alongside international visitors seeking cost-competitive retreat experiences relative to North American and European equivalents. Brazil and Mexico lead regional wellness hospitality development, with eco-resort and thermal spa formats drawing increasing international attention. By contrast, infrastructure gaps and currency volatility in smaller Latin American markets constrain the pace of new wellness property development.

The Middle East and Africa region is investing heavily in wellness tourism infrastructure as part of broader economic diversification agendas. GCC states, particularly Saudi Arabia and the UAE, are integrating wellness and longevity programming into new resort developments to attract high-net-worth international visitors. South Africa contributes a nature-based wellness offering centered on safari retreat formats that command strong premiums from global travelers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

The Indian Hotels Company Limited formalized its entry into integrated wellness hospitality in November 2025 by acquiring a 51% stake in Sparsh Infratech Private Limited, owner of Atmantan Wellness Resort. This acquisition gives IHCL a clinically credentialed wellness asset to position against international luxury chains. The WHO-reported 25% rise in global anxiety and depression during COVID-19 strengthens the commercial case for IHCL’s wellness pivot.

Marriott International, Inc. operates across the wellness hospitality spectrum through its portfolio of luxury, upper-upscale, and select-service brands, each integrating wellness amenities at varying price points. This multi-tier positioning allows Marriott to capture wellness demand across corporate, leisure, and high-net-worth consumer segments simultaneously. Global life expectancy of approximately 73 years, per World Bank estimates, supports long-term demand for the preventive health programming Marriott increasingly features across its spa and wellness offerings.

Key Players

- Accor

- Belmond Management Limited

- Four Seasons Hotel Limited

- InterContinental Hotel Group

- Mandarin Oriental Hotel Group Limited

- Marriott International, Inc.

- Rosewood Hotel Group

- The Indian Hotel Company Limited

- Radisson Hotel Group

- Aman Resorts

Recent Developments

- 2025 – Accor announced multiple luxury hotel openings including wellness-integrated Fairmont properties such as Fairmont Tokyo and Fairmont Udaipur, both featuring full spa, wellness, and holistic health facilities as part of their core property design.

- 2025 – Accor published its official “2025 Wellness Trends” framework, highlighting the increased integration of science-based wellness, spa innovation, and nature-focused retreat design across its global hospitality brands.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 135.0 Billion |

| Forecast Revenue (2035) | USD 320.6 Billion |

| CAGR (2026-2035) | 9.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Category (Chain, Independent); By Type (Resorts and Spa, Business Hotels, Airport Hotels, Holiday Hotels, Others); By Booking Mode (Direct Booking, Travel Agents, Online Travel Agencies) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Accor, Belmond Management Limited, Four Seasons Hotel Limited, InterContinental Hotel Group, Mandarin Oriental Hotel Group Limited, Marriott International, Inc., Rosewood Hotel Group, The Indian Hotel Company Limited, Radisson Hotel Group, Aman Resorts |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

In 2022, the global Wellness Tourism market accounted for USD 822.3 billion and is expected to grow to around USD 1922.2 billion in 2032.