Quick Navigation

Report Overview

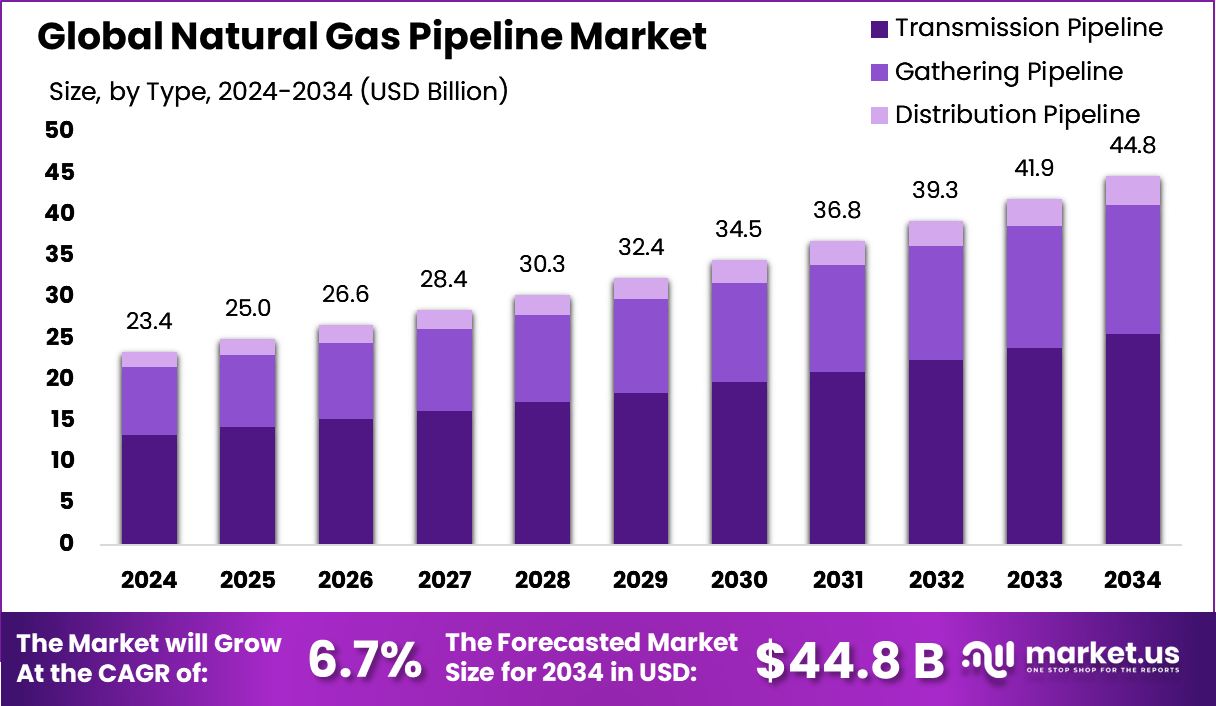

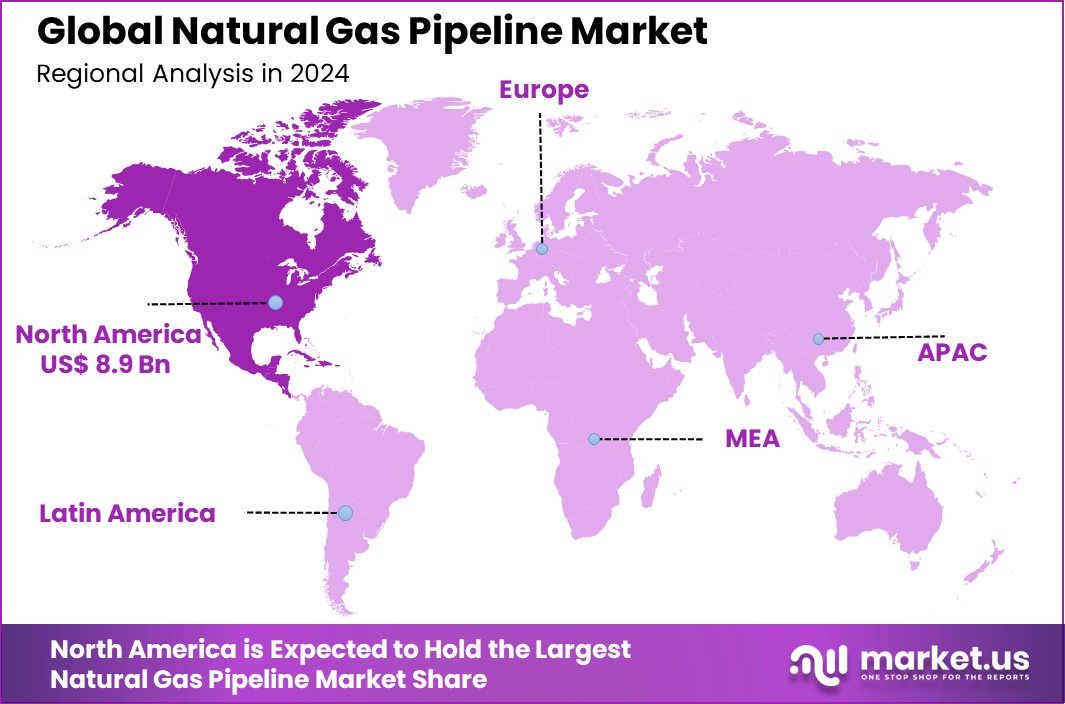

Global Natural Gas Pipeline Market is expected to be worth around USD 44.8 billion by 2034, up from USD 23.4 billion in 2024, and grow at a CAGR of 6.7% from 2025 to 2034. Holding a 38.20% share, North America’s Natural Gas Pipeline Market was valued at USD 8.9 billion in 2024.

A natural gas pipeline is a vast network of interconnected pipes designed to transport natural gas from production sites to end-users, including industrial plants, power stations, and residential areas. These pipelines vary in size and function, including transmission pipelines that move gas across long distances at high pressures and distribution pipelines that deliver it to consumers at lower pressures. The infrastructure ensures a steady supply of natural gas, supporting economic growth, energy security, and industrial expansion.

The natural gas pipeline market encompasses the construction, maintenance, and expansion of pipeline networks that transport natural gas. Driven by rising energy demand and infrastructure modernization, the market includes public and private investments in new pipeline projects, retrofits, and upgrades. Governments and energy companies worldwide invest heavily in pipeline expansions to enhance distribution efficiency, reduce transmission losses, and meet growing urban and industrial needs.

Investment in natural gas pipeline infrastructure is accelerating due to government funding and regulatory incentives. In FY 2022, around $196 million was allocated for NGDISM grants, a trend expected to continue in subsequent years. Pipeline projects are further bolstered by policies promoting clean energy alternatives to coal, reducing carbon footprints, and increasing natural gas adoption. Modernization efforts also include the replacement of aging pipelines with high-efficiency materials, enhancing safety and performance.

Increasing industrial and commercial demand for natural gas is pushing pipeline expansions. Many industries are shifting to natural gas due to its cost-effectiveness and lower emissions. In states like Pennsylvania, grants of up to $1.5 million or 50% of project costs are available to extend distribution lines to industrial zones, stimulating market growth. Additionally, rising electricity consumption is fueling natural gas-fired power plants, reinforcing pipeline infrastructure needs.

Advancements in pipeline technology and automation are unlocking new opportunities. Companies are investing in leak detection, smart metering, and AI-driven monitoring systems to enhance pipeline efficiency. Expansion in emerging markets, particularly in Asia and Latin America, presents further potential as urbanization increases energy demand. Government-backed funding and incentives continue to attract investments, ensuring steady growth in natural gas infrastructure.

Key Takeaways

- Global Natural Gas Pipeline Market is expected to be worth around USD 44.8 billion by 2034, up from USD 23.4 billion in 2024, and grow at a CAGR of 6.7% from 2025 to 2034.

- The transmission pipeline segment dominates the natural gas pipeline market with a 57.10% share.

- Pipelines with diameters above 24 inches hold a significant 43.30% of the market.

- Compressor stations, vital for maintaining gas flow, represent 59.30% of the application market segment.

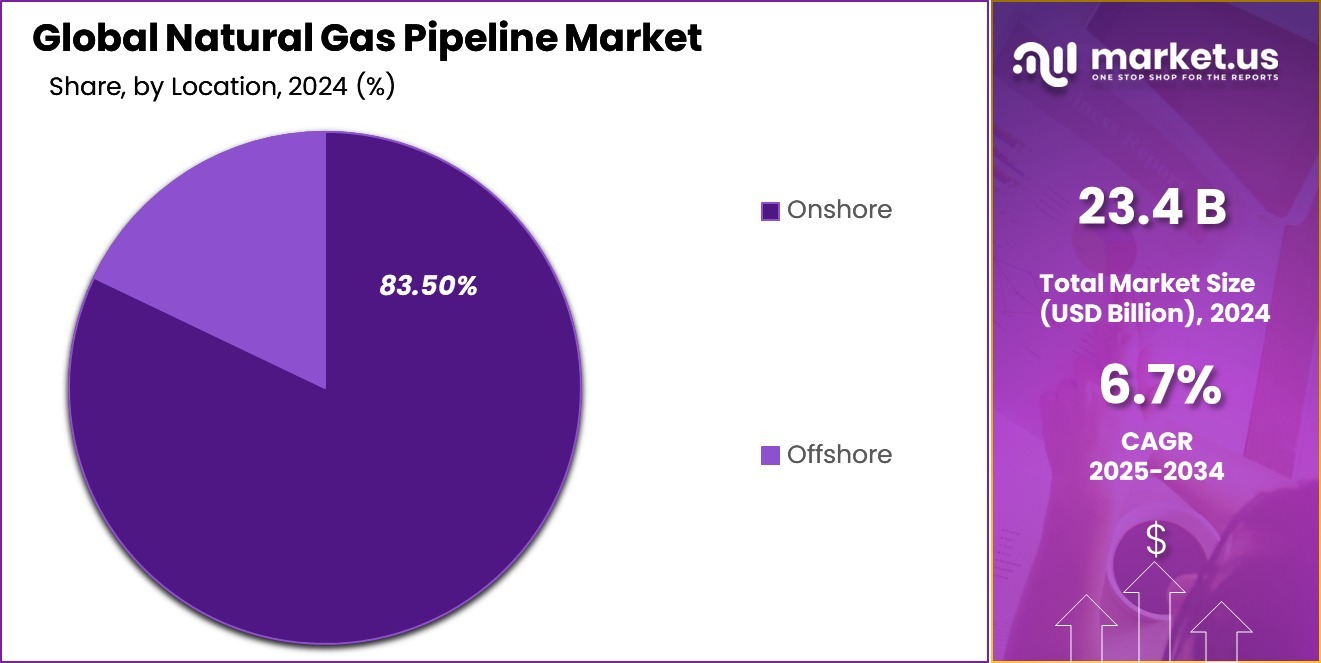

- The onshore segment overwhelmingly leads, comprising 83.50% of natural gas pipeline installations.

- The North American Natural Gas Pipeline Market reached USD 8.9 billion in 2024, accounting for 38.20% market share.

By Type Analysis

Transmission pipelines dominate, holding 57.10% of the natural gas pipeline market.

In 2024, the Transmission Pipeline segment held a dominant position in the “By Type” category of the Natural Gas Pipeline Market, commanding a 57.10% share. This segment’s substantial market share reflects its critical role in the long-distance transport of natural gas from production sites to local distribution companies and large industrial users. Transmission pipelines are the backbone of the natural gas supply chain, characterized by their large diameter pipes, which are essential for moving vast quantities of natural gas across extensive distances.

The dominance of this segment is further underscored by increasing investments in pipeline infrastructure to support the growing demand for energy, particularly in regions experiencing rapid industrial growth and urbanization. The strategic expansion of transmission pipelines is also driven by the need to replace older and less efficient pipelines with more technologically advanced and environmentally safe options. This renewal and expansion are crucial in maintaining the reliability and efficiency of the energy supply chain, thereby ensuring uninterrupted service to end-users.

Moreover, the expansion of the transmission pipeline infrastructure is closely aligned with national energy security strategies, which prioritize the establishment of a robust and dependable energy delivery system to cater to domestic needs and support economic growth. This segment’s growth is expected to continue as more regions invest in enhancing their energy infrastructure to meet future demand efficiently and sustainably.

By Diameter Analysis

Above 24-inch diameter pipelines account for 43.30% of the market share.

In 2024, the Above 24 Inches segment held a dominant market position in the By Diameter category of the Natural Gas Pipeline Market, capturing a 43.30% share. This segment’s substantial share is primarily attributed to the rising demand for large-capacity pipelines that can efficiently transport high volumes of natural gas over long distances. As global energy consumption increases, infrastructure developers are investing heavily in high-diameter pipelines to optimize transmission efficiency and reduce operational costs.

The preference for above 24 Inches pipelines is driven by their ability to handle greater pressure and volume, making them the preferred choice for cross-border and inter-regional natural gas transportation. These pipelines are essential in major energy-exporting nations and regions with high energy demands, where expanding natural gas infrastructure remains a priority. Governments and private sector players are focusing on constructing larger pipelines to accommodate growing gas production and consumption needs.

Additionally, advancements in pipeline materials and construction technologies have enhanced the durability and safety of large-diameter pipelines, further strengthening their market position. As energy security concerns rise and countries seek to improve energy distribution networks, the Above 24 Inches segment is expected to witness sustained investment and growth, reinforcing its dominance in the market.

By Application Analysis

Compressor stations lead applications with a 59.30% share in the market.

In 2024, the Compressor Station segment held a dominant market position in the By Application category of the Natural Gas Pipeline Market, securing a 59.30% share. This segment’s leadership is primarily driven by the critical role compressor stations play in maintaining the pressure and flow of natural gas across extensive pipeline networks. As natural gas travels long distances, it experiences pressure loss due to friction and distance. Compressor stations are strategically installed at intervals to boost pressure, ensuring efficient and uninterrupted gas transportation.

The increasing demand for natural gas across industrial, commercial, and residential sectors has necessitated the expansion of compressor stations to support the growing pipeline infrastructure. Rising cross-border and intercontinental gas trade has further accelerated the need for high-capacity compressor stations, particularly along major transmission pipelines. Governments and private energy firms are investing in upgrading existing stations and developing new ones to enhance efficiency and meet environmental regulations.

Moreover, advancements in compressor technologies, including energy-efficient and low-emission systems, are further supporting the growth of this segment. As global energy consumption continues to rise and pipeline networks expand to meet demand, the Compressor Station segment is expected to maintain its dominance in the market, reinforcing its crucial role in natural gas transportation.

By Location Analysis

Onshore locations significantly lead, comprising 83.50% of the natural gas pipeline market.

In 2024, the Onshore segment held a dominant market position in the by-location category of the Natural Gas Pipeline Market, securing an 83.50% share. This significant market presence is primarily driven by the extensive development of land-based pipeline networks for the efficient transportation of natural gas from production fields to processing plants, storage facilities, and end users. Onshore pipelines remain the preferred infrastructure due to their lower installation costs, easier maintenance, and accessibility compared to offshore alternatives.

The expansion of natural gas production in key regions, particularly in North America, Asia-Pacific, and the Middle East, has fueled the demand for onshore pipelines to support growing energy needs. The increasing adoption of natural gas as a cleaner alternative to coal and oil has further accelerated pipeline installations in industrial and urban areas. Additionally, government initiatives focused on enhancing energy security and reducing carbon emissions have led to significant investments in upgrading and expanding existing onshore pipeline networks.

Moreover, advancements in pipeline monitoring and leak-detection technologies have improved the operational efficiency and safety of onshore infrastructure, reinforcing its dominance. As demand for natural gas continues to rise across industries, the Onshore segment is expected to maintain its stronghold, driven by continuous infrastructure development and regulatory support.

Key Market Segments

By Type

- Transmission Pipeline

- Gathering Pipeline

- Distribution Pipeline

By Diameter

- Below 16 Inches

- 16 to 24 Inches

- Above 24 Inches

By Application

- Compressor Station

- Metering Station

- Others

By Location

- Onshore

- Offshore

Driving Factors

Rising Global Energy Demand Driving Pipeline Expansion

The increasing energy demand worldwide is a major force driving the natural gas pipeline market. As economies grow, industries expand, and urbanization accelerates, the need for a reliable and efficient energy supply is rising.

Natural gas has become a preferred energy source due to its lower carbon emissions compared to coal and oil, making it an essential part of the global energy transition. Many countries are investing in pipeline infrastructure to ensure stable energy distribution, reduce dependence on imports, and meet domestic energy needs.

Additionally, industrial sectors such as power generation, manufacturing, and chemicals are relying more on natural gas, further boosting pipeline expansion. As energy consumption continues to increase, the natural gas pipeline market is expected to grow steadily.

Restraining Factors

High Installation Costs Limiting Pipeline Expansion

The high cost of building natural gas pipelines is a major challenge for market growth. Constructing a pipeline requires significant investment in materials, labor, and advanced technology to ensure safety and efficiency.

Additionally, regulatory approvals, land acquisition, and environmental compliance add to the overall expenses, making the process lengthy and costly. Many regions, especially developing economies, struggle to fund large-scale pipeline projects due to budget constraints and financial risks.

Maintenance costs also remain high, as pipelines require regular monitoring and upgrades to prevent leaks and operational failures. These financial challenges often delay projects or lead to cancellations, limiting market expansion. Unless cost-effective solutions are implemented, the high investment needed will continue to restrain pipeline development worldwide.

Growth Opportunity

Pipeline Expansion in Emerging Markets Boosting Growth

Emerging markets present a significant growth opportunity for the natural gas pipeline industry. Countries in Asia, Africa, and Latin America are rapidly expanding their energy infrastructure to meet rising demand from industries and households.

Many of these nations are shifting from coal and oil to cleaner energy sources like natural gas, creating a strong need for new pipeline networks. Governments and private investors are funding large-scale pipeline projects to improve energy access, support economic growth, and enhance energy security.

Additionally, international partnerships and foreign investments are driving the development of cross-border pipelines, further expanding market potential. As these regions continue to industrialize and urbanize, the demand for natural gas pipelines will increase, opening up major growth opportunities.

Latest Trends

Smart Pipeline Technologies Enhancing Safety and Efficiency

The natural gas pipeline industry is witnessing a growing trend in the adoption of smart technologies to improve safety, efficiency, and monitoring capabilities. Advanced sensors, real-time data analytics, and automated control systems are being integrated into pipeline networks to detect leaks, monitor pressure, and predict maintenance needs.

These smart technologies help reduce operational risks, minimize downtime, and enhance overall pipeline performance. Additionally, artificial intelligence (AI) and the Internet of Things (IoT) are being used to analyze vast amounts of data, enabling quicker decision-making and improved pipeline management.

As regulatory bodies emphasize stricter safety and environmental compliance, companies are investing in digital solutions to modernize their infrastructure. This trend is expected to shape the future of the natural gas pipeline market.

Regional Analysis

In 2024, North America led the Natural Gas Pipeline Market, capturing 38.20% market share, valued at USD 8.9 billion.

In 2024, North America dominated the Natural Gas Pipeline Market, securing a 38.20% market share, valued at USD 8.9 billion. The region’s stronghold is driven by extensive pipeline infrastructure, increasing natural gas production, and significant investments in pipeline expansion projects across the United States and Canada. The ongoing development of cross-border pipelines, along with rising LNG exports, further fuels market growth.

In Europe, the market is shaped by energy diversification strategies, reducing dependency on Russian gas and increasing pipeline connectivity between countries. Governments are prioritizing pipeline upgrades and new projects to enhance energy security. Asia Pacific is witnessing rapid growth due to increasing natural gas demand in China and India, coupled with large-scale infrastructure investments.

Countries in the region are actively expanding domestic and cross-border pipelines to meet industrial and residential energy needs. The Middle East & Africa market is driven by major gas-producing nations such as Qatar, Iran, and Saudi Arabia, focusing on pipeline network expansion for both domestic consumption and exports.

Meanwhile, Latin America sees moderate growth, supported by pipeline developments in Brazil and Argentina, aimed at enhancing regional gas distribution. With continued investments, North America is expected to maintain its dominance, while Asia Pacific emerges as a high-growth region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Antero Midstream Corporation remains a key player in the natural gas pipeline market, benefiting from its strong foothold in the Appalachian Basin. The company continues to expand its midstream infrastructure to support Antero Resources’ production, ensuring stable revenue generation. Its focus on water infrastructure and compression services further strengthens its market position.

Bechtel Corporation plays a crucial role as a leading engineering and construction firm specializing in large-scale natural gas pipeline projects. The company’s expertise in designing high-capacity pipelines and LNG export terminals positions it as a strategic partner in global energy expansion. Bechtel’s involvement in pipeline modernization and energy transition projects keeps it at the forefront of industry developments.

Berkshire Hathaway Energy, through its subsidiary BHE Pipeline Group, holds a dominant presence in the U.S. pipeline infrastructure market. The company’s extensive assets and financial strength enable it to invest in modernizing existing pipelines while expanding its network. Regulatory compliance and sustainability efforts remain key focus areas for long-term growth.

Boardwalk Pipeline Partners LP continues to expand its footprint in the U.S. Gulf Coast region, benefiting from rising LNG exports. The company’s investment in storage and transportation infrastructure enhances its role as a reliable midstream provider, ensuring a stable supply to industrial and commercial users.

Cheniere Energy Inc. strengthens its market influence through LNG pipeline development, supporting its export terminals. With increasing global LNG demand, Cheniere’s pipeline investments ensure efficient gas supply to its liquefaction facilities, reinforcing its leadership in the gas value chain.

Top Key Players in the Market

- Antero Midstream Corporation

- Bechtel Corporation

- Berkshire Hathaway Energy

- Boardwalk Pipeline Partners LP

- Cheniere Energy Inc.

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Continental Industries

- Enbridge Inc.

- Energy Transfer LP

- EnLink Midstream Partners LP

- Enterprise Products Partners LP

- ExxonMobil

- Gastite

- Kinder Morgan Inc.

Recent Developments

- In December 2024, Boardwalk Pipelines made a final investment decision on the Kosciusko Junction pipeline project, which will transport 1.16 Bcf/d of natural gas. The project is supported by a 20-year agreement and aims to meet growing demand in the Southeast.

- In July 2024, Bechtel signed a fixed-price engineering, procurement, and construction (EPC) contract with Sempra Infrastructure for the Port Arthur LNG Phase 2 project. This project is crucial for expanding LNG export capabilities in the U.S.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 23.4 Billion |

| Forecast Revenue (2034) | USD 44.8 Billion |

| CAGR (2025-2034) | 6.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Transmission Pipeline, Gathering Pipeline, Distribution Pipeline), By Diameter (Below 16 Inches, 16 to 24 Inches, Above 24 Inches), By Application (Compressor Station, Metering Station, Others), By Location (Onshore, Offshore) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Antero Midstream Corporation, Bechtel Corporation, Berkshire Hathaway Energy, Boardwalk Pipeline Partners LP, Cheniere Energy Inc., Chevron Corporation, China Petroleum & Chemical Corporation, Continental Industries, Enbridge Inc., Energy Transfer LP, EnLink Midstream Partners LP, Enterprise Products Partners LP, ExxonMobil, Gastite, Kinder Morgan Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |