Quick Navigation

Report Overview

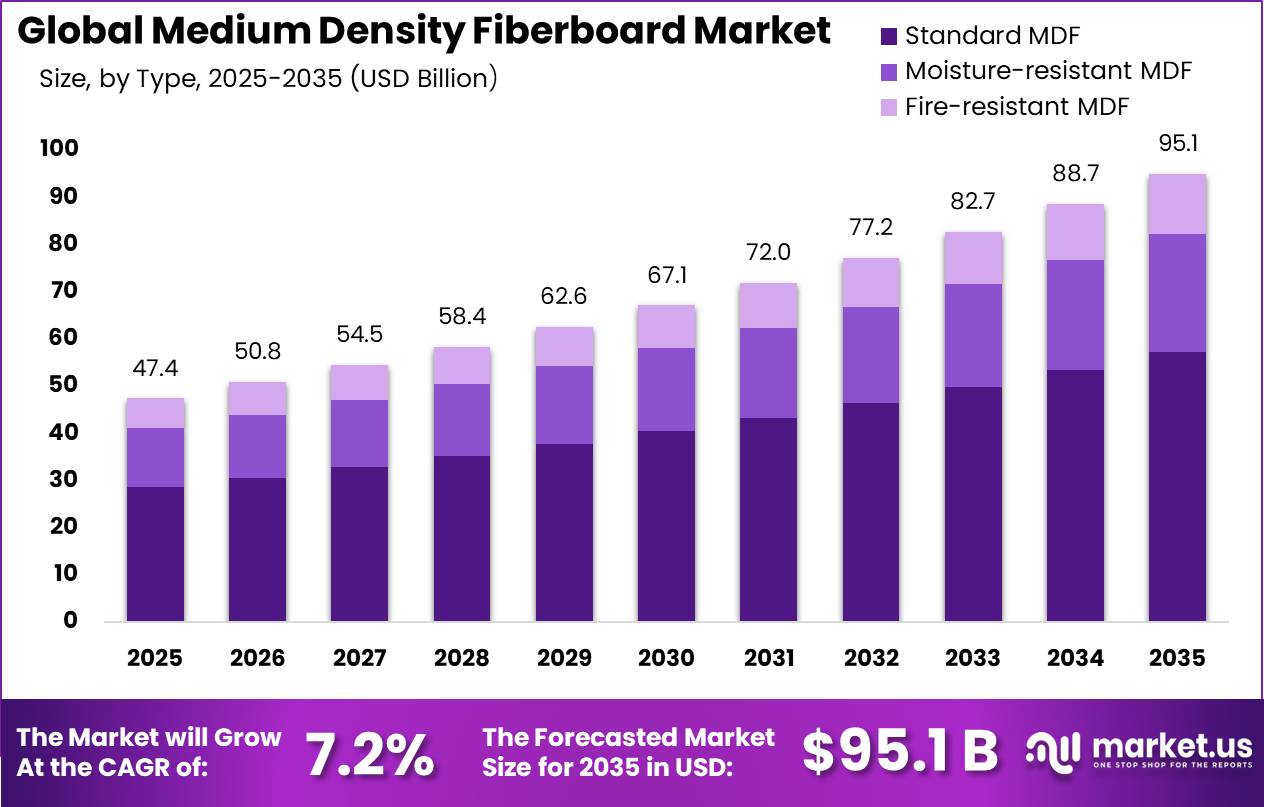

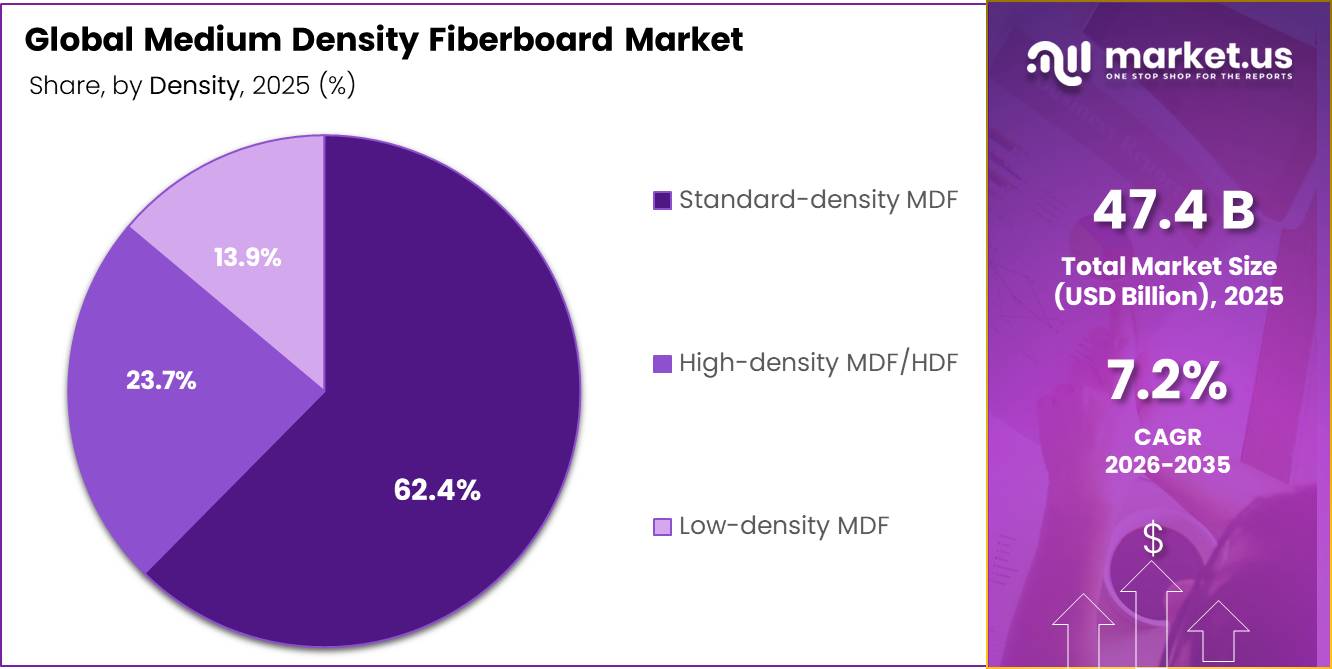

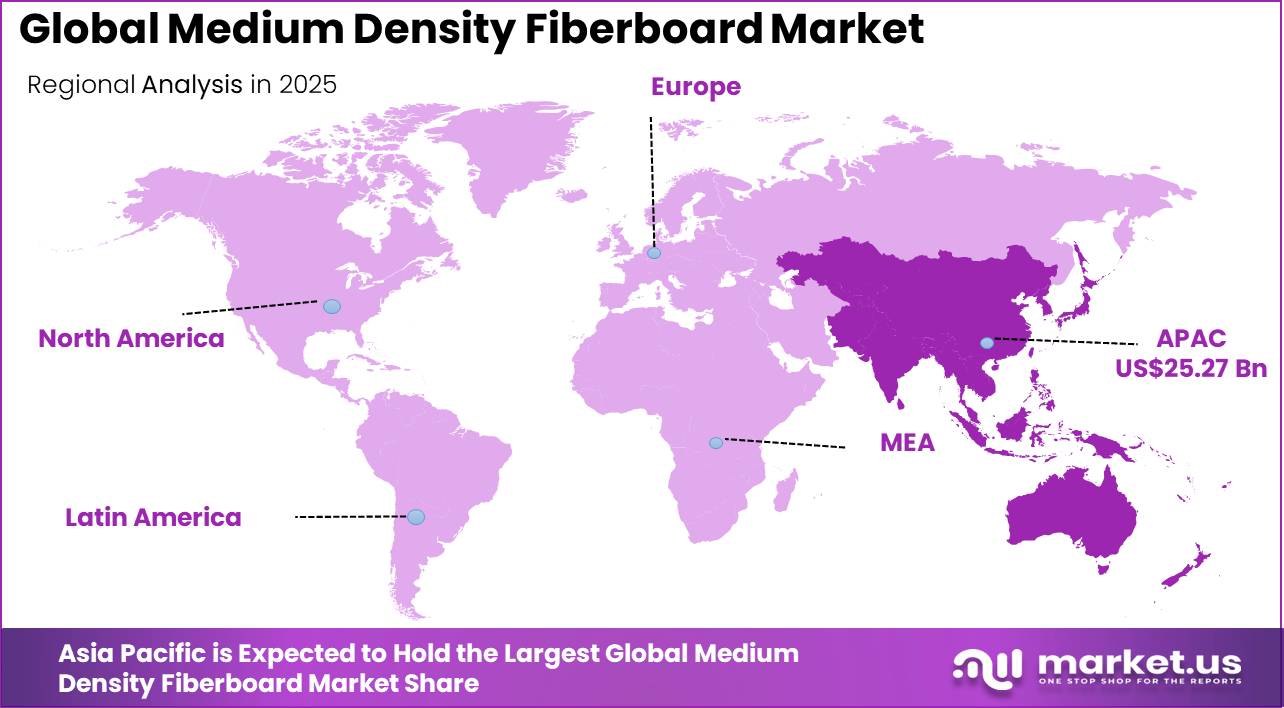

The Global Medium Density Fiberboard Market was valued at US$ 47.4 billion in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 7.2%, reaching about US$ 95.1 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 53.3% share, holding USD 25.26 billion in revenue.

The Medium Density Fiberboard market is driving due to rapid urbanization, rising disposable income levels, and growing preference for value-for-money engineered wood products used in furniture, construction, and interior decorating applications. MDF production entails milling down hardwoods and softwoods to create fibers, adding wax and resin adhesives, and pressing them together in panels using intense heat and pressure in order to achieve uniform dimension and smoothness at reduced costs compared to solid wood, thus rendering MDF more favored for mass production.

The worldwide construction industry accounts for 36% of global energy consumption and up to 40% of greenhouse gas emissions in relation to energy generation. As such, the industry acts as one of the largest consumers of MDF; hence, the adoption of stringent environmental regulation laws has become critical. Formaldehyde emissions have been regulated in accordance with U.S. EPA TSCA Title VI, limiting emissions to no more than 0.09 ppm, whereas the CARB Phase 2 formaldehyde standard limits emissions to 0.05 ppm.

Key Takeaways

- The Global Medium Density Fiberboard Market was valued at US$47.4 billion in 2025.

- The Global Medium Density Fiberboard Market is projected to grow at a CAGR of 7.2% and is estimated to reach US$95.1 billion by 2035.

- On the basis of Product/Type, Standard MDF dominated the market, constituting 60.3% of the total market share.

- Based on the Density/Grade, the Standard – density MDF dominated the Global Medium Density Fiberwood market, with a substantial market share of around 62.4%.

- Based on the Application, Furniture and Cabinetry led the market, comprising 42.8% of the total market.

- Among the end-uses, Residential held a major share in the Global Medium Density Fiberwood market, with 58.7% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the Global Medium Density Fiberwood market, accounting for 53.3% of the total global consumption.

Product Analysis

Standard MDF represents the dominant Segment in the Market

Standard MDF was the choice, taking up 60.3% of the market around the world. The reason Standard MDF is so popular is that it is very easy to work with and it does not cost a lot. You can cut Standard MDF, shape it, and finish it without any problems, which makes it perfect for making a lot of things at once.

The Moisture Resistant MDF segment is an important area for growth, making up 26.3% of the market in 2025. The hotel and commercial real estate industries are growing fast in the Asia-Pacific region, which means there is a demand for Moisture Resistant MDF because it lasts a long time and does not need to be replaced often, which saves money in the long run.

Density Analysis

Standard-density MDF is a significant density

Standard-Density MDF was the choice for many people, and it had 62.4% of the global market. This is because Standard-Density MDF is very good at being strong and easy to work with, which makes it perfect for making furniture, fixing up the inside of buildings, and building cabinets.

High-Density MDF, which is also called HDF, was used by 23.7% of the market in 2025. It is the type of MDF that is growing in popularity the fastest. This is happening because more and more people want to use High-Density MDF for flooring, and it needs to be very hard, able to withstand impacts, and keep its shape.

Application Analysis

The Furniture and Cabinetry accounts for the largest share of medium density fiberboard applications

Furniture and Cabinetry dominated the global MDF with 42.8%. The strength of the Furniture and Cabinetry market can be attributed to the size of the furniture market; as urbanization increases, there would be more migration to metropolitan areas, and by 2030, 68% of the population would live in cities, according to UN estimates.

The segment of Flooring and Panels is seeing rapid expansion, capturing 17.2% of the market share in 2025. Demand for the MDF floor is boosted by this demand. Asia Pacific represents a significant share in the flooring market as it generates 56.4% of the revenue.

End Use Analysis

Medium Density Fiberboard Are Mostly Utilized in the Residential

The Residential segment had the largest share of the global MDF market, taking up 58.7%. The Residential segment has this share because the global residential construction sector is getting bigger and bigger. As a result, the Residential segment is using MDF to make furniture, cabinets, floors, and other things for homes.

The United Nations says that by 2030, 68% of people will live in cities, which means the Residential segment will keep getting bigger and using MDF. The Commercial segment is also important. It had 24.6% of the market in 2025. The Commercial segment is the part of the market that is expected to grow the most. More offices, stores and hotels are being built, which means there is a need for MDF to make walls, furniture and decorations.

Key Market Segments

By Type

- Standard MDF

- Moisture resistant MDF

- Fire resistant MDF

By Density

- Standard‑density MDF

- High‑density MDF/HDF

- Low‑density MDF

By Applications

- Furniture and cabinetry

- Flooring and panels

- Doors, moldings, and millwork

- Interior décor and wall panels

- Packaging and others

By End Use

- Residential

- Commercial

- Institutional/industrial

Market Dynamics

Drivers

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-Led Furniture & Interior Demand | +2.4% | Asia Pacific (India, China, Southeast Asia), Middle East | Short term (≤ 2 years) |

| MDF Cost Competitiveness vs. Solid Hardwood | +1.5% | Global, especially Emerging Markets | Short term (≤ 2 years) |

| Residential Construction & Modular Housing Programs | +1.2% | India (PMAY), Southeast Asia, GCC | Short term (≤ 2 years) |

| Low-Emission Resin Technology Adoption | +0.9% | Europe, North America, Japan | Medium term (2–4 years) |

| E-Commerce & D2C Furniture Channel Expansion | +0.8% | India, China, USA, Brazil | Short term (≤ 2 years) |

| BIS QCO & Import Substitution Driving Domestic Capacity | +0.4% | India | Short term (≤ 2 years) |

Urbanization-Led Furniture & Interior Demand

Asia Pacific’s structural urbanization cycle, with India adding an estimated 35–40 million urban residents annually and China sustaining Tier-3 city development programs, is the single most potent demand vector for MDF today. Furniture accounts for approximately 51% of global MDF volume consumption, and within that, the residential end-use segment alone commands over 60% of demand.

India’s furniture market grew +11% in USD terms in 2024, one of the fastest paces in Asia Pacific, and CSIL forecasts sustained +6% real growth in both 2025 and 2026, directly translating into accelerated panel procurement cycles for domestic MDF producers. At the unit-economics level, MDF production costs run approximately USD 220/m³ versus USD 450–650/m³ for seasoned hardwood, a cost differential that is structurally widening as deforestation controls tighten and FSC-certified timber supply remains constrained, pulling specifiers toward engineered wood panels.

Restraints

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH Formaldehyde Emission Compliance Barrier | -1.6% | Europe, Export Markets Supplying EU | Short term (≤ 2 years) |

| Chinese Overcapacity & Low-Price Export Pressure | -1.2% | Global (South & Southeast Asia, Africa, LatAm) | Short term (≤ 2 years) |

| Urea-Formaldehyde Resin Price Volatility | -0.9% | Global | Short term (≤ 2 years) |

| High Capital Intensity of New Mill Establishment | -0.7% | Emerging Markets — India, Africa, Southeast Asia | Medium term (2–4 years) |

| Elevated Interest Rates Compressing Construction CapEx | -0.5% | North America, Europe | Short term (≤ 2 years) |

EU REACH Formaldehyde Emission Compliance Barrier

Commission Regulation (EU) 2023/1464, amending Annex XVII of REACH, mandates that from 6 August 2026, all furniture and wood-based articles placed on the EU market must not exceed a formaldehyde emission ceiling of 0.062 mg/m³, a threshold materially stricter than the current US EPA/CARB Phase 2 limit of 0.11 ppm for standard MDF.

Producers manufacturing to pre-2026 E1 class specifications (0.124 mg/m³) face a mandatory reformulation cycle: transitioning to low-emission UF resins or MDI-based binders raises per-unit adhesive costs by an estimated 8–15%, while chamber-method compliance testing under Appendix 14 adds qualification lead times of up to 28 days per batch.

The margin impact is asymmetric: large integrated producers absorbing reformulation CapEx across higher volumes dilute the unit cost increase to roughly 3–5%, while smaller mills face effective margin compression of 10–18% on EU-directed product lines, widening the competitive gap and accelerating capacity consolidation in the short term.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Wood Fiber Feedstock Scarcity | -1.3% | Global, Acute in South Asia & Sub-Saharan Africa | Long term (≥ 4 years) |

| Particleboard & Plywood Substitution Pressure | -0.8% | Global | Medium term (2–4 years) |

| Logistics & Freight Cost Volatility | -0.6% | Global, Especially Asia-to-Europe Trade Lanes | Medium term (2–4 years) |

| Skilled Technical Workforce Deficit | -0.5% | India, Southeast Asia, Africa | Long term (≥ 4 years) |

| Energy Cost & Grid Reliability Constraints | -0.4% | India, South & Southeast Asia, Eastern Europe | Medium term (2–4 years) |

Wood Fiber Feedstock Scarcity

MDF production is structurally dependent on a continuous supply of wood residues, agro-fiber, and plantation timber chips feedstock streams that are simultaneously being competed for by biomass energy, pulp & paper, and pellet export industries, creating a multi-sector supply squeeze that no single player can resolve unilaterally.

For a mid-sized MDF plant of 30,000–50,000 m³/year capacity, raw material and wood chip procurement already constitutes approximately 45–55% of total operating cost; even a 10–12% rise in fiber input prices consistent with the cost inflation seen in the 2023–2025 window driven by competition from the biomass sector compresses operating EBITDA margins toward the 8–10% band, as confirmed by Indian industry margin profiles for FY27.

Long-term mitigation requires corporate-level responses including backward integration into captive plantation programs (typically requiring 5,000–10,000 acres minimum per mill to achieve meaningful fiber self-sufficiency), multi-year offtake agreements with sawmills and paper mills for residual fiber streams, and R&D investment in agro-fiber MDF (bagasse, rice husk, bamboo) to diversify feedstock bases, none of which deliver operational relief in under 36–48 months.

Opportunities

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Specialty MDF (Fire Retardant, Moisture Resistant) | +1.8% | Middle East, Europe, North America, India | Medium term (2–4 years) |

| Green Building & Sustainable Construction Certification | +1.3% | Global, Led by Europe, GCC, India | Medium term (2–4 years) |

| Agro-Fiber & Recycled Content MDF Innovation | +1.0% | South Asia, Southeast Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Export Penetration via India’s Furniture PLI & QCO Tailwind | +0.9% | India (export to USA, EU, GCC) | Medium term (2–4 years) |

| M&A Roll-Up of Fragmented Domestic Mills | +0.6% | India, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

Specialty MDF (Fire Retardant, Moisture Resistant)

The specialty MDF sub-segment encompassing fire retardant (FR-MDF) and moisture-resistant (MR-MDF) grades represents largely untapped white space within the broader engineered wood panels market, currently commanding a sizable but disproportionately underserved share of total addressable demand, particularly in hospitality, healthcare, transit infrastructure, and modular commercial fit-out projects where building codes mandate fire-performance certification.

Unlike standard commodity MDF which is increasingly exposed to margin compression from Chinese overcapacity specialty grades carry realized price premiums of 25–40% per m³ over standard panels, driven by the cost of inorganic flame-retardant additive packages (typically 8–12% of panel weight), proprietary manufacturing process modifications, and third-party certification costs (EN 13501, UL 94, IS 15380) that create durable competitive moats for qualified producers.

This opportunity is currently underexploited because most mid-scale mills lack the dedicated press configurations, additive dosing systems, and certification infrastructure to serve FR and MR grade specifications; estimated capital investment of ₹3–5 crore per production line upgrade and because specifier awareness among architects and interior contractors in emerging markets remains nascent.

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Medium Density Fiberboard Manufacturing

The global MDF market in 2025 is dealing with a lot of problems because of what’s happening in the world. Two things are causing these problems. The Russia-Ukraine conflict and the trade issues between the U.S. and China. These two things are affecting how raw materials are supplied how prices are determined and how trade is happening in regions. The war between Russia and Ukraine has changed the way timber is supplied around the world.

Since Russia invaded Ukraine, the UK and Europe have stopped importing wood products from Russia and Belarus. This has led to a market where timber is being relabelled as coming from other countries like those in the Baltic states. The cost of making MDF, particleboard and plywood in Russia is going to go up by more than 15%, which will reduce the profit margins of companies that are part of the supply chain. Research says that the market for wood-based panels in Russia and Ukraine will not go back to what it was before the invasion, and other countries will take over the market share that was lost.

At the time the U.S. is changing the way it trades with other countries, which is affecting how MDF is bought in North America. In March 2025 the U.S. increased the taxes on softwood lumber from 14.5% to 34.5% which means that the total taxes are now almost 40%. This is increasing the costs for MDF manufacturers that rely on fiber from North America.

The U.S. also put a 25% tax on kitchen cabinets and upholstered wooden furniture in October 2025 which is disrupting the demand for MDF. Because of these problems companies are looking for ways to get their supplies and they are turning to countries in Southeast Asia, Scandinavia and Latin America to reduce their dependence, on trade with countries that have sanctions or high taxes.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Medium Density Fiberboard Market

Asia Pacific emerged as the leading region in terms of global MDF market share in 2025, holding an impressive 53.3%, owing to the excellent urbanization trends prevalent there. As per UN ESCAP (2025), over 2.2 billion people live in urban areas in the Asia-Pacific region, and it is expected that this will rise by a further 50% by 2050.

Europe was second in global MDF market share in 2025, capturing 19.2%. Being the most regulation-led market in terms of growth, sustainability is a critical area. The European Environment Agency indicates that in 2023, the European Union’s building sector emitted around 33% of total energy-related emissions. As such, ensuring that buildings are constructed using low-emission technologies is a crucial policy objective. Under the revised Energy Performance of Buildings Directive (EPBD), enacted in 2024, a strategy for decarbonizing the European building stock by 2050 is being pursued.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global MDF market has big players. These players have a lot of production capacity. Are present in many places. ARAUCO is leading the market. They are present in North America and Latin America. They control their production process from forestry to finished panels. This helps them keep costs low and manage their supply chain well. ARAUCO’s approach allows them to stay ahead.

In Europe, EGGER Group and Kronospan Limited are the players. They focus on making products with low emissions. Their manufacturing meets E0 and E1 standards. They source materials with FSC certification. This approach makes them suppliers for buyers who care about sustainability.

In the Asia-Pacific region, Daiken Corporation and Kastamonu Entegre are doing well. They have increased their production capacity. Adopted new resin technology. This helps them meet the growing demand for MDF in their region and for exports. MDF demand keeps growing.

In India, Greenpanel and Centuryply are becoming more important. This is because of the growing construction activity and demand for furniture in residential projects. The Indian market is growing fast. All MDF manufacturers are focusing on developing products without formaldehyde, making acquisitions, and getting sustainability certifications.

Major Players in the Industry

- ARAUCO

- Centuryply

- Daiken Corporation

- Dare Panel Group Co., Ltd.

- Dongwha Malaysia Holdings Sdn. Bhd.

- Duratex

- EGGER Group

- Fantoni Spa

- Georgia-Pacific

- Greenpanel

- Kastamonu Entegre

- Kronospan Limited

- M. Kaindl KG

- Nag Hamady Fiber Board Co.

- Norbord Inc.

- Roseburg Forest Products

- Rushil Décor

- Swiss Krono Group

- Uniboard

- Unilin

- VRG Dongwha

- West Fraser Timber Co. Ltd.

- Weyerhaeuser

Key Development

- In May 2025, Homanit, a German company that makes medium- and high-density fiberboards, said it will invest $250 million to build its first factory in the United States. The factory will be in Alcolu, South Carolina. It should be up and running by 2028. This is a move for Homanit, a major European MDF maker, to enter the North American market.

- In October 2024, Unilin said they will invest twenty million euros to start recycling MDF on a large scale. This is a step for the MDF industry to use circular economy principles. The MDF industry is doing this because they have to deal with a lot of rules, and people are getting upset about waste from panels in Europe.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 47.4 Bn |

| Forecast Revenue (2035) | US$ 95.1 Bn |

| CAGR (2026-2035) | 7.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Standard MDF, Moisture Resistant MDF, Fire Resistant MDF), By Density (Standard-density MDF, High Density MDF, Low Density MDF), By Application (Cabinet, Flooring, Furniture, Molding, Door, and Millwork, Packaging System, Others), By End-use (Residential, Commercial, Institutional) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ARAUCO, Centuryply, Daiken Corporation, Dare Panel Group Co. Ltd., Dongwha Malaysia Holdings Sdn. Bhd., Duratex, EGGER Group, Fantoni Spa, Georgia-Pacific, Greenpanel, Kastamonu Entegre, Kronospan Limited, M. Kaindl KG, Nag Hamady Fiber Board Co., Norbord Inc., Roseburg Forest Products, Rushil Décor, Swiss Krono Group, Uniboard, Unilin, VRG Dongwha, West Fraser Timber Co. Ltd., Weyerhaeuser. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |