Quick Navigation

Report Overview

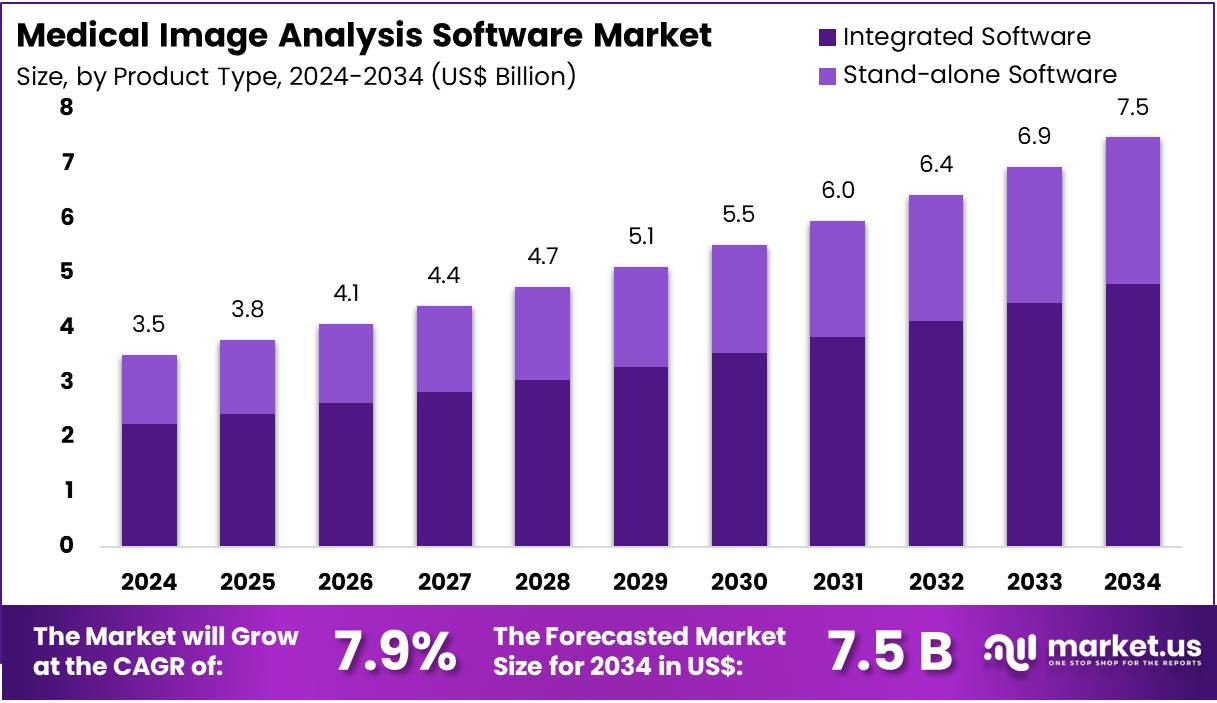

The Global Medical Image Analysis Software Market size is expected to be worth around US$ 7.5 Billion by 2034, from US$ 3.5 Billion in 2024, growing at a CAGR of 7.9% during the forecast period from 2025 to 2034.

Increasing demand for advanced diagnostic tools and the growing need for improved healthcare efficiency are driving the medical image analysis software market. Healthcare providers increasingly rely on these software solutions to enhance diagnostic accuracy, reduce human error, and streamline medical imaging workflows.

The integration of artificial intelligence (AI) and machine learning (ML) technologies has become a key trend, enabling software to process complex images faster and more accurately. These advancements support a broad range of applications, including radiology, oncology, and cardiology, where precise image interpretation is crucial for effective treatment planning.

In September 2022, King Abdullah Medical City (KAMC) in Mecca, Saudi Arabia, upgraded its radiology and imaging infrastructure by adopting Agfa HealthCare’s Enterprise Imaging platform. This transition not only improved workflow efficiency but also optimized the accessibility of medical data across the facility, showcasing the shift toward digital solutions in healthcare. As medical imaging continues to evolve, the market is projected to expand, with rising opportunities in AI-driven software and enhanced imaging capabilities for faster, more accurate diagnostics.

Key Takeaways

- In 2024, the market for medical image analysis software generated a revenue of US$ 3.5 billion, with a CAGR of 7.9%, and is expected to reach US$ 7.5 billion by the year 2034.

- The product type segment is divided into integrated software and stand-alone software, with integrated software taking the lead in 2024 with a market share of 64.3%.

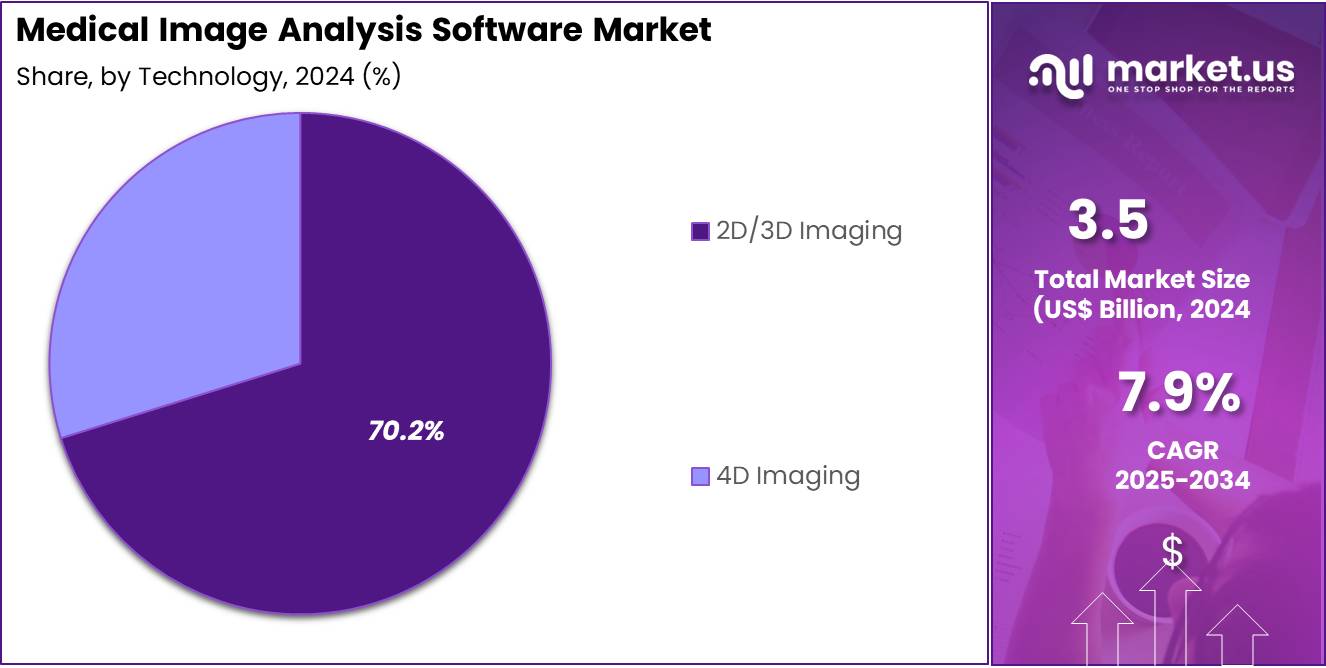

- Considering technology, the market is divided into 2D/3D imaging and 4D imaging. Among these, 2D/3D imaging held a significant share of 70.2%.

- Furthermore, concerning the application segment, the market is segregated into orthopedic, dental, neurology, cardiology, oncology, and others. The cardiology sector stands out as the dominant player, holding the largest revenue share of 42.4% in the medical image analysis software market.

- The modality segment is segregated into tomography, ultrasound imaging, radiographic imaging, combined modalities, and mammography, with the tomography segment leading the market, holding a revenue share of 43.5%.

- Considering end-user, the market is divided into hospitals, diagnostic centers, ASCs, and others. Among these, hospitals held a significant share of 56.8%.

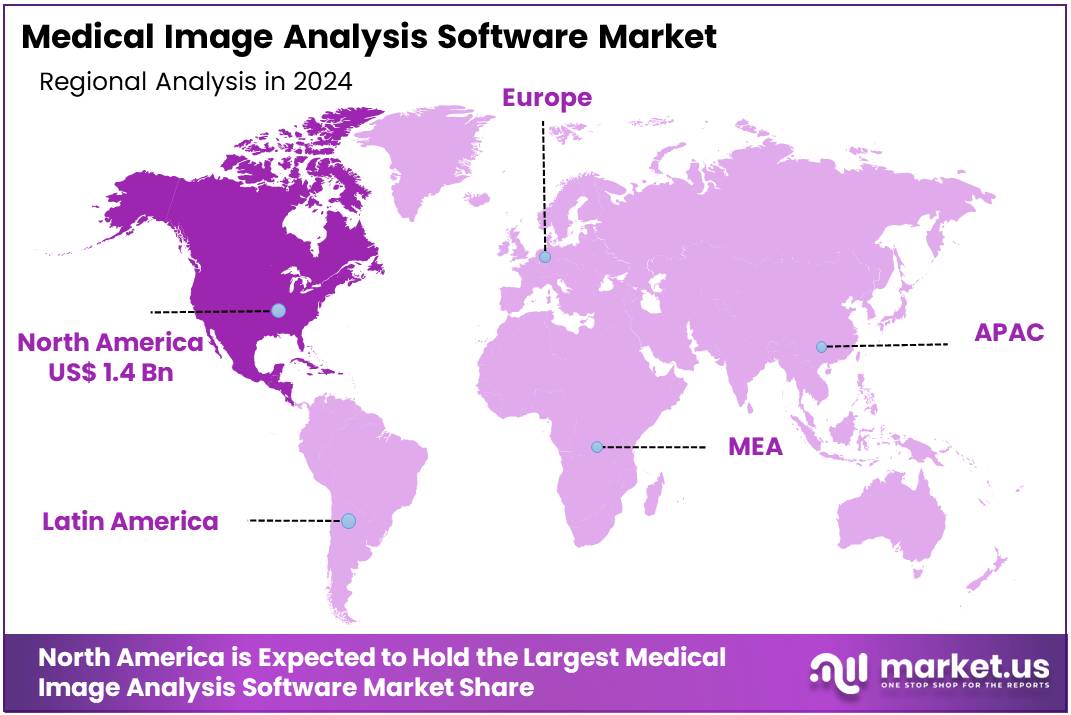

- North America led the market by securing a market share of 38.7% in 2024.

Product Type Analysis

The integrated software segment led in 2023, claiming a market share of 64.3% owing to the increasing demand for seamless integration of image analysis tools into broader healthcare IT systems. Integrated software solutions provide greater interoperability between medical devices, electronic health records (EHR), and other hospital management systems, enabling a more efficient workflow.

The growing focus on improving diagnostic accuracy and operational efficiency is likely to drive the adoption of integrated solutions. Additionally, advancements in artificial intelligence (AI) and machine learning (ML) that enhance image analysis capabilities are anticipated to further contribute to the growth of this segment. As healthcare providers aim to streamline operations and enhance patient care, the demand for integrated medical image analysis software is projected to increase.

Technology Analysis

The 2D/3D imaging held a significant share of 70.2% due to the rising demand for detailed and accurate imaging in diagnostic procedures. 2D/3D imaging provides clear visualization of anatomical structures, making it essential in the diagnosis and treatment planning for various conditions such as cancers, heart diseases, and musculoskeletal disorders. The increasing use of 3D imaging in surgeries and diagnostics is expected to drive the segment’s expansion.

As technology improves, 2D/3D imaging software becomes more accessible and cost-effective, making it a preferred choice in clinical settings. Furthermore, the growing trend of minimally invasive procedures, which rely on detailed imaging, is anticipated to boost the adoption of 2D/3D medical image analysis software.

Application Analysis

The cardiology segment had a tremendous growth rate, with a revenue share of 42.4% owing to the increasing prevalence of cardiovascular diseases (CVD) worldwide. As CVDs remain one of the leading causes of morbidity and mortality, the demand for advanced diagnostic tools to assess heart health is projected to rise. Medical image analysis software plays a crucial role in cardiology by enhancing the accuracy of imaging techniques such as echocardiography, CT scans, and MRIs for heart disease diagnosis.

The increasing adoption of non-invasive diagnostic techniques and the growing focus on personalized healthcare are likely to further drive the demand for medical image analysis in cardiology. Additionally, advancements in software that allow for better 3D modeling and real-time data processing are expected to contribute to the segment’s growth.

Modality Analysis

The tomography segment grew at a substantial rate, generating a revenue portion of 43.5% as tomography techniques, such as CT and PET scans, continue to play a critical role in diagnostic imaging. Tomography allows for detailed cross-sectional imaging of the body, which is essential for detecting a wide range of diseases, including cancer, neurological disorders, and cardiovascular diseases.

As the need for early diagnosis and precise treatment planning grows, the demand for tomography software that enhances the visualization and interpretation of these images is projected to rise. Moreover, technological advancements, such as high-resolution imaging and improved reconstruction algorithms, are anticipated to drive the adoption of tomography-based medical image analysis solutions.

End-user Analysis

The hospitals held a significant share of 56.8% as hospitals remain the primary location for a wide range of diagnostic and treatment procedures. Hospitals are projected to drive the demand for medical image analysis software as they increasingly adopt advanced imaging techniques to enhance diagnostic accuracy and improve patient outcomes. The rising prevalence of chronic diseases, such as cancer and cardiovascular diseases, is likely to increase the need for sophisticated imaging tools in hospitals.

Furthermore, the growing focus on improving operational efficiency and patient care through integrated IT systems is expected to further contribute to the demand for medical image analysis software in hospital settings. As hospitals continue to invest in advanced diagnostic technologies, this segment is projected to see continued growth.

Key Market Segments

By Product Type

- Integrated Software

- Stand-alone Software

By Technology

- 2D/3D Imaging

- 4D Imaging

By Application

- Orthopedic

- Dental

- Neurology

- Cardiology

- Oncology

- Others

By Modality

- Tomography

- Computed Tomography

- Magnetic Resonance Imaging

- Positron Emission Tomography

- Single-Photon Emission Tomography

- Ultrasound Imaging

- Radiographic Imaging

- Combined Modalities

- PET/MR

- SPECT/CT

- PET/MR

- Mammography

By End-user

- Hospitals

- Diagnostic Centers

- ASCs

- Others

Drivers

Increasing Adoption of AI and Machine Learning is Driving the Market

The integration of artificial intelligence (AI) and machine learning (ML) into medical image analysis software is a key driver of market growth. These technologies enhance diagnostic accuracy, streamline workflows, and reduce human error, making them indispensable in modern healthcare. According to the US Food and Drug Administration (FDA), the agency approved 75 AI/ML-based medical devices in 2023, a 25% increase from 2022, with a significant portion focused on imaging applications.

Companies like NVIDIA and GE Healthcare have invested heavily in AI-driven imaging solutions, with NVIDIA reporting a 30% year-over-year growth in its healthcare segment revenue in 2023. The National Institutes of Health (NIH) also allocated US$1.8 billion to AI research in 2023, underscoring the importance of these technologies in advancing medical imaging.

Hospitals and diagnostic centers are increasingly adopting AI-powered tools to handle the growing volume of imaging data, which is expected to reach 2.5 billion studies annually by 2024, as per the Radiological Society of North America (RSNA). This trend is driving demand for advanced software solutions, positioning AI and ML as critical enablers of market expansion.

Restraints

High Implementation Costs are Restraining the Market

Despite its potential, the high cost of implementing medical image analysis software remains a significant restraint. The initial investment required for advanced systems, including hardware upgrades and staff training, can be prohibitive for smaller healthcare providers. According to the American Hospital Association (AHA), the average cost of deploying AI-based imaging solutions in 2023 ranged from US$500,000 to US$1 million per facility, depending on the scale.

Additionally, maintenance and software licensing fees add to the financial burden, with annual costs estimated at US$100,000 to US$200,000 per institution. The World Health Organization (WHO) reported in 2023 that 40% of low- and middle-income countries struggle to afford advanced imaging technologies, limiting market penetration in these regions.

Even in developed markets, budget constraints and reimbursement challenges hinder widespread adoption. For instance, Medicare reimbursement rates for AI-assisted imaging procedures increased by only 2% in 2023, failing to keep pace with rising costs. These financial barriers slow down the adoption of cutting-edge solutions, particularly among smaller clinics and rural healthcare facilities.

Opportunities

Integration of Advanced Imaging Modalities is Creating Growth Opportunities

Integrating advanced imaging modalities, such as MRI, CT scans, and ultrasound, with medical image analysis software presents significant growth opportunities in the healthcare sector. These integrations enhance diagnostic capabilities, allowing for more accurate and comprehensive assessments of patient conditions. These advancements have led to a notable increase in both the volume and complexity of medical imaging, thereby increasing the demand for sophisticated analysis software.

By incorporating advanced imaging modalities, healthcare providers can offer more precise diagnostics, leading to better patient outcomes and driving the adoption of integrated software solutions. This trend not only supports the expansion of the market but also underscores the importance of continuous innovation in medical imaging technologies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the medical image analysis software market, creating both challenges and opportunities. Rising healthcare expenditures, particularly in developed regions like North America and Europe, positively impact market growth. For instance, US healthcare spending reached US$4.5 trillion in 2023, a 5% increase from 2022, according to the Centers for Medicare & Medicaid Services (CMS).

However, inflation and supply chain disruptions have increased the cost of software development and deployment, posing challenges for vendors. Geopolitical tensions, such as the US-China trade conflict, have disrupted the supply of critical components, delaying product launches. On the positive side, government initiatives like the European Union’s US$820 billion recovery fund, which allocated US$55 billion to digital health in 2023, support market expansion.

Emerging markets in Asia and Africa also present growth opportunities, driven by increasing healthcare investments and infrastructure development. Despite these challenges, the market remains resilient, with technological advancements and strategic collaborations driving long-term growth.

Trends

Shift Toward Cloud-Based Solutions is a Recent Trend

A notable trend in the medical image analysis software market is the shift toward cloud-based solutions, driven by the need for scalability, accessibility, and cost efficiency. Cloud platforms allow healthcare providers to store, analyze, and share imaging data securely, facilitating collaboration among specialists. According to Microsoft’s 2023 Healthcare Trends Report, 60% of healthcare organizations adopted cloud-based imaging solutions by 2023, up from 40% in 2022.

Amazon Web Services (AWS) reported a 50% increase in healthcare-related cloud service usage in 2023, with imaging applications being a major contributor. The US Department of Health and Human Services (HHS) also emphasized the importance of cloud technology in its 2023 Health IT Strategic Plan, allocating US$150 million to support cloud adoption in healthcare.

This trend is further supported by advancements in data security and compliance with regulations like HIPAA and GDPR, which ensure patient data protection. As a result, cloud-based solutions are becoming the preferred choice for healthcare providers, driving innovation and market growth.

Regional Analysis

North America is leading the Medical Image Analysis Software Market

North America dominated the market with the highest revenue share of 38.7% owing to advancements in AI and machine learning, increased adoption of digital health technologies, and rising demand for precision medicine. According to the US Food and Drug Administration (FDA), the number of AI-based medical imaging devices approved in 2023 reached 171, marking a 30% increase from 2022. This growth reflects the rapid integration of AI into healthcare.

Hospitals and diagnostic centers are increasingly adopting these tools to enhance diagnostic accuracy and operational efficiency. For example, the Centers for Medicare & Medicaid Services (CMS) reported a 15% rise in reimbursements for AI-assisted imaging procedures in 2023, encouraging healthcare providers to invest in advanced software solutions.

Moreover, the growing prevalence of chronic diseases, such as cancer and cardiovascular conditions, has driven demand for early and accurate diagnoses. In 2023, the American Cancer Society estimated 1.9 million new cancer cases in the US, underscoring the need for advanced imaging technologies. Government initiatives, including the National Institutes of Health (NIH)’s US$6.5 billion investment in AI and imaging research in 2023, have further accelerated market growth.

Additionally, partnerships between tech giants like Google Health and healthcare providers have played a crucial role, with Google Health’s AI imaging tools being deployed in over 100 US hospitals by early 2024. These factors collectively highlight the strong expansion of the medical image analysis software market in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing healthcare digitization, rising investments in AI, and expanding access to advanced diagnostic tools. In 2023, the Indian government allocated US$ 1.3 billion to its Digital Health Mission, which aims to integrate AI-based imaging solutions into public healthcare systems.

Similarly, China’s National Health Commission reported a US$ 25.2 billion investment in AI healthcare technologies in 2023, with a particular focus on imaging and diagnostics. Additionally, partnerships between global tech firms and local healthcare providers are expected to foster innovation. For instance, Siemens Healthineers collaborated with Apollo Hospitals in India to deploy AI-powered imaging solutions across 70 facilities in 2023.

The growing adoption of telemedicine and remote diagnostics, particularly in rural areas, is likely to further increase demand. By 2024, the Asia Pacific region is projected to see a 20% annual growth in the adoption of advanced imaging tools, supported by favorable government policies and technological advancements.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the medical image analysis software market implement various strategies to drive growth, including technological advancements, strategic partnerships, and mergers and acquisitions. Companies focus on enhancing software capabilities with artificial intelligence (AI) and machine learning to improve diagnostic accuracy and efficiency. They also invest in expanding their product portfolios to cater to diverse medical specialties.

Many leading firms are collaborating with healthcare institutions and academic research centers to foster innovation and stay competitive. Additionally, global expansion and a strong focus on emerging markets further enhance their market presence. One of the key players in the market is Siemens Healthineers, a global leader in healthcare technology.

The company provides a broad range of medical imaging and diagnostic solutions, leveraging cutting-edge software to support healthcare professionals. Siemens Healthineers integrates AI into its imaging solutions to streamline workflows and enhance patient care. Their focus on precision medicine and improving clinical outcomes makes them a prominent player in the medical imaging space.

Top Key Players in the Medical Image Analysis Software Market

- Siemens Healthineers AG

- MIM Software, Inc

- ESAOTE SPA

- Deep Rui Medical

- Canon Medical Systems

- Bruker

- Agfa-Gevaert Group

Recent Developments

- In January 2023, Bruker Corporation expanded its capabilities in bioimaging and data analytics through the acquisition of ACQUIFER Imaging GmbH. This strategic move enhances Bruker’s expertise in high-content screening and large-scale data management solutions for advanced imaging applications.

- In January 2023, Canon Medical Systems USA Inc. formed a collaboration with ScImage, Inc., a company specializing in cloud-based enterprise imaging and PACS solutions. This partnership aims to streamline medical image management and improve interoperability across healthcare systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.5 billion |

| Forecast Revenue (2034) | US$ 7.5 billion |

| CAGR (2025-2034) | 7.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Integrated Software and Stand-alone Software), By Technology (2D/3D Imaging and 4D Imaging), By Application (Orthopedic, Dental, Neurology, Cardiology, Oncology, and Others), By Modality (Tomography (Computed Tomography, Magnetic Resonance Imaging, Positron Emission Tomography, and Single-Photon Emission Tomography), Ultrasound Imaging, Radiographic Imaging, Combined Modalities (PET/MR, SPECT/CT, and PET/MR), and Mammography), By End-user (Hospitals, Diagnostic Centers, ASCs, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens Healthineers AG, MIM Software, Inc, ESAOTE SPA, Deep Rui Medical, Canon Medical Systems, Bruker, and Agfa-Gevaert Group. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |