Quick Navigation

- Report Overview

- Key Takeaways

- Business Environment Analysis

- Product Type Analysis

- Power Output Analysis

- Vehicle Type Analysis

- Charging Standard Analysis

- End-User Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Emerging Trends

- Regional Analysis

- Competitive Landscape

- Recent Developments

- Report Scope

Report Overview

The Global Hypercharger Market size is expected to be worth around USD 350.5 Billion by 2034, from USD 13.4 Billion in 2024, growing at a CAGR of 38.6% during the forecast period from 2025 to 2034.

A hypercharger is a high-power charging station designed to rapidly charge electric vehicles. It significantly exceeds the power output of standard EV chargers, often delivering up to 350 kW, which can provide substantial charge in just minutes.

The hypercharger market encompasses the production, distribution, and installation of high-speed charging stations for electric vehicles. This market serves automotive manufacturers, EV owners, and infrastructure providers aiming to reduce EV charging times and enhance charging convenience.

The Hypercharger market is rapidly growing, driven by the need for faster and more efficient electric vehicle (EV) charging solutions. These chargers, capable of delivering high-speed energy, are critical to supporting EV adoption globally. Key markets like China, Europe, and the U.S. are witnessing significant investments and technological advancements, spurring market growth.

Technological innovations, such as Zeekr’s 10-80% battery charge in under 11 minutes, are reducing EV charging times. Additionally, government funding, like the $7.5 billion U.S. investment, supports infrastructure development. Increasing demand for electric vehicles globally, with 3.2 million new registrations in Europe (2023), highlights the opportunity for hypercharger solutions.

The demand for hyperchargers is fueled by rising EV ownership and the need for shorter charging durations. For instance, Germany’s 18% EV sales growth signifies market potential. Collaborative projects, such as the XPeng-Volkswagen initiative, emphasize the opportunities for creating extensive charging networks in urban areas.

Governments play a critical role in market growth. The U.S. aims for 500,000 chargers by 2030, with 24,800 projects underway. Similarly, Europe’s supportive policies and China’s large-scale investments foster growth. Regulations also ensure safety and efficiency, promoting broader adoption.

Key Takeaways

- The Hypercharger Market was valued at USD 13.4 billion in 2024 and is expected to reach USD 350.5 billion by 2034, with a CAGR of 38.6%.

- In 2024, Ultra-Fast Chargers dominated the product type segment with 42.7%, driven by their ability to significantly reduce charging times.

- In 2024, 100–200 kW led the power output segment with 39.8%, owing to its balance of fast charging and widespread compatibility.

- In 2024, Passenger Vehicles accounted for 47.3% of the vehicle type segment, reflecting the increasing adoption of EVs in urban areas.

- In 2024, the CCS (Combined Charging System) dominated the charging standard segment with 38.6%, attributed to its interoperability and wide acceptance.

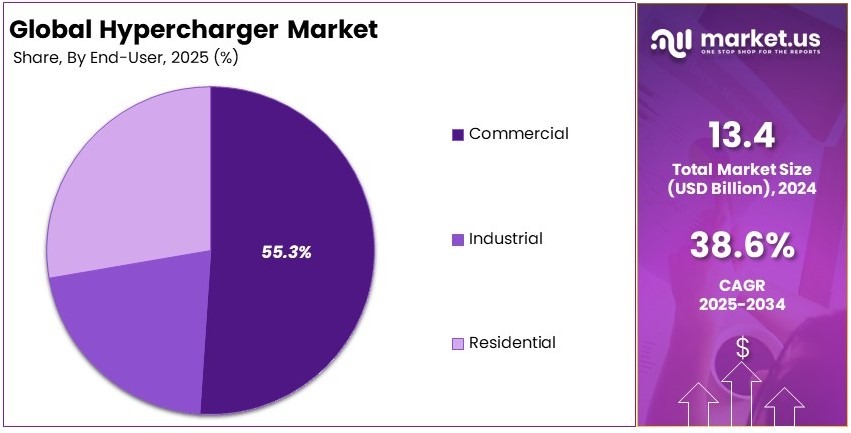

- In 2024, the Commercial end-user segment led with 55.3%, driven by rising investments in charging stations and public infrastructure.

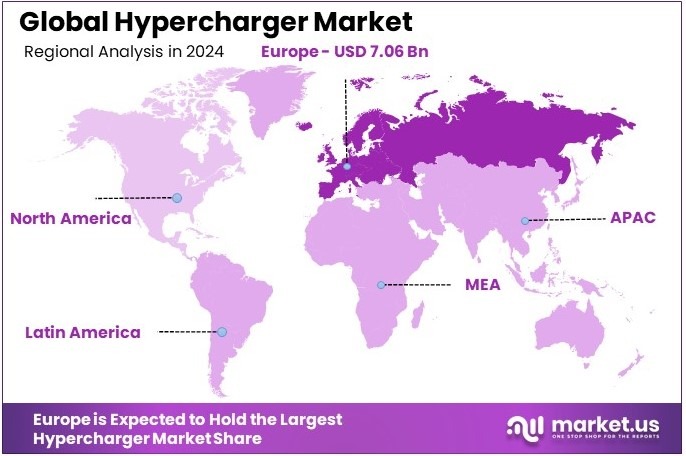

- In 2024, Europe dominated the market with 52.7% and generated revenues of USD 7.06 billion, driven by strong EV policies and infrastructure advancements.

Business Environment Analysis

The hypercharger market shows low saturation in developed regions, with substantial growth potential in emerging markets. As the International Energy Agency notes, global electric vehicle (EV) sales reached 14% of new car sales in 2022, highlighting the need for advanced charging solutions to support rising EV adoption.

Target demographics include urban EV owners and fleet management operators who prioritize fast, reliable charging options. For instance, hyperchargers cater to consumers with limited home charging access, offering a solution for densely populated areas and long-distance travelers. This growing customer base presents significant opportunities for market expansion.

Product differentiation is essential to stay competitive. Hyperchargers that offer ultra-fast charging, integrated payment systems, and smart grid connectivity stand out. Additionally, features like vehicle-to-grid capabilities attract environmentally conscious consumers and fleet managers looking for efficient energy management solutions.

Investment opportunities are significant, particularly in infrastructure development. According to the European Investment Bank, funding for EV charging stations is expected to exceed €2 billion by 2025. Emerging markets in Asia and South America also offer untapped potential due to their rapid urbanization and EV adoption rates.

Adjacent markets like renewable energy and battery storage systems align closely with hyperchargers. Solar-powered charging stations and integrated energy storage solutions boost sustainability efforts. This synergy promotes adoption in regions focusing on clean energy, creating additional revenue streams for businesses in the EV ecosystem.

Product Type Analysis

Ultra-Fast Chargers dominate with 42.7% due to their rapid charging capabilities and increasing adoption in urban areas.

The Hypercharger market is segmented by product type into DC Fast Chargers, Ultra-Fast Chargers, and Wireless Hyperchargers. Ultra-Fast Chargers, capturing 42.7% of the market, stand out due to their ability to significantly reduce charging time, making them highly attractive for commercial use in cities with high electric vehicle throughput.

This segment benefits from technological advancements that enable the handling of higher power outputs, thus supporting the rapid growth of electric vehicle infrastructures.

DC Fast Chargers, holding a market share of 31.2%, are essential for mid-range electric vehicles and are commonly found in public charging stations and malls. They offer a balance between speed and accessibility, making them a practical choice for many users.

Wireless Hyperchargers, with a 26.1% share, represent the future of charging technology with their convenience and innovative contactless charging features. Although they currently hold a smaller segment of the market, their integration into everyday environments like coffee shops and offices is anticipated to increase.

Power Output Analysis

100–200 kW leads with 39.8% due to its compatibility with a wide range of vehicles and balance in efficiency and speed.

In the Hypercharger market, power output is a crucial differentiator, segmented into Up to 100 kW, 100–200 kW, and Above 200 kW. The 100–200 kW segment dominates the market with 39.8%, favored for its versatility in accommodating a broad spectrum of electric vehicles from sedans to light commercial vehicles without compromising much on charging time.

This range represents a sweet spot, providing a rapid charge while still being relatively economical in terms of energy consumption and infrastructure demands.

The Up to 100 kW segment accounts for 30.3% of the market, primarily serving older models and compact vehicles.

It is prevalent in residential areas where slower, overnight charging is feasible. The Above 200 kW segment, which captures 29.9%, caters to cutting-edge electric vehicles and high-demand commercial applications, offering ultra-fast charging speeds necessary for high-usage fleets and luxury electric vehicles.

Vehicle Type Analysis

Passenger Vehicles dominate with 47.3% due to the rising consumer adoption of electric cars.

Vehicle type segmentation in the Hypercharger market includes Passenger Vehicles, Commercial Vehicles, Electric Buses, and Two-Wheelers. The Passenger Vehicles segment leads with 47.3% market share, driven by the increasing consumer shift towards electric vehicles for personal use.

The growth in this segment is supported by the expanding global push for sustainable transportation and government incentives for electric vehicle buyers.

Commercial Vehicles have a 26.7% share, influenced by businesses updating their fleets to electric models for cost efficiency and regulatory reasons. Electric Buses represent 15.6% of the market, vital for urban public transport systems transitioning to greener alternatives. Two-Wheelers, which hold 10.4% of the market, are increasingly popular in densely populated cities due to their low cost and minimal space requirements.

Charging Standard Analysis

CCS (Combined Charging System) leads with 38.6% due to its widespread adoption in North America and Europe.

Charging standards are integral to the Hypercharger market, with CCS (Combined Charging System), CHAdeMO, Tesla Supercharger, and GB/T as the main types.

The CCS standard is the most prevalent, holding 38.6% of the market, favored for its compatibility with a majority of the latest electric vehicles produced by American and European manufacturers. This standard supports both AC and DC charging, making it versatile for various applications.

CHAdeMO accounts for 30.1% of the market, popular in Japan and among older electric vehicle models that require DC fast charging. Tesla Supercharger, capturing 18.4%, is exclusive to Tesla vehicles, offering high-speed charging capabilities. The GB/T standard holds 12.9% of the market, primarily used in China, pivotal in the largest electric vehicle market globally.

End-User Analysis

Commercial dominates with 55.3% due to the expansion of public electric vehicle infrastructure.

The end-user segments in the Hypercharger market are categorized into Residential, Commercial, and Industrial. Commercial uses lead with a 55.3% share, driven by the global expansion of electric vehicle charging stations and parking spaces.

They are designed to accommodate an increasing number of electric vehicles in public and semi-public areas. This segment’s growth is bolstered by both government policies and private investments in electric vehicle infrastructure.

Residential use accounts for 24.8% of the market, reflecting the growth in home charging setups as more consumers purchase electric vehicles. Industrial applications, with a 19.9% market share, are crucial for logistic companies and industries transitioning to electric options to reduce carbon emissions and fuel costs, aligning with broader sustainability goals.

Key Market Segments

By Product Type

- DC Fast Chargers

- Ultra-Fast Chargers

- Wireless Hyperchargers

By Power Output

- Up to 100 kW

- 100–200 kW

- Above 200 kW

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Electric Buses

- Two-Wheelers

By Charging Standard

- CCS (Combined Charging System)

- CHAdeMO

- Tesla Supercharger

- GB/T

By End-User

- Residential

- Commercial

- Charging Stations

- Parking Spaces

- Industrial

Driving Factors

Rising Market Demand Drives Market Growth

The growth of the Hypercharger Market is fueled by several key drivers. Rising adoption of electric vehicles has increased the need for fast charging solutions, as seen with Tesla expanding its Supercharger network. Expansion of charging infrastructure supports this trend and meets growing consumer demand, much like ChargePoint extending services in urban areas.

Government incentives encourage investments in charging facilities, similar to subsidies provided by the European Union. Growing environmental awareness pushes consumers and businesses to seek sustainable energy solutions, as seen with companies like Siemens investing in green charging stations.

In addition, these factors create a positive market atmosphere. The emphasis on reducing charging times makes Ultra-Fast Charging Technologies particularly attractive.

Integrating renewable energy sources like solar and wind helps lower costs and adds to sustainability. Public-private partnerships further support network growth by sharing resources and expertise. Charging-as-a-service models offer flexibility and reduce upfront costs.

Restraining Factors

High Costs and Standardization Issues Restraints Market Growth

The Hypercharger Market faces several restraints that hinder its progress. High initial investment and installation costs present a major barrier, as seen with startups struggling to secure funding for new stations.

Lack of standardization in charging technologies causes uncertainty, much like earlier mobile phone charging wars that confused consumers. This lack of uniformity affects consumer trust and slows adoption.

Limited availability of charging stations in rural areas limits market reach; for example, parts of the Midwest still lack coverage. Dependence on electric grid capacity further complicates expansion efforts, similar to challenges faced by renewable energy projects. These factors create a challenging environment for new entrants.

Investors may hesitate due to financial risks and unclear returns. As a result, scaling infrastructure becomes slower. Manufacturers must navigate complex regulatory landscapes that add to costs. Communities in remote regions may struggle to attract infrastructure investments.

Growth Opportunities

Innovative Solutions Provides Opportunites

The Hypercharger Market offers numerous growth opportunities that stakeholders can capitalize on. The development of ultra-fast charging technologies reduces consumer wait times, as seen with companies like ABB introducing 350 kW chargers.

Integration of renewable energy solutions into charging stations creates cost savings and environmental benefits, similar to how SunPower powers stations with solar panels. Growth in public-private partnerships provides new funding avenues, such as collaborations between governments and companies like Shell.

Increasing adoption of charging-as-a-service business models opens up recurring revenue streams, exemplified by EVgo’s subscription plans. These opportunities encourage investment and innovation. For example, a company might partner with a local government to build a solar-powered hypercharger station, which not only lowers energy costs but also appeals to eco-conscious consumers.

Another firm could launch a subscription-based service offering unlimited fast charging. These strategies align with modern consumer trends. The combination of technology, finance, and service design enhances market appeal. Companies can differentiate themselves by focusing on user convenience and sustainability.

Emerging Trends

Smart Integration Is Latest Trending Factor

The Hypercharger Market is trending toward smart integration and user-focused innovations. The growing popularity of smart charging stations with real-time monitoring marks a shift in consumer expectations, similar to how Blink’s smart chargers operate.

Integration with mobile apps for user convenience simplifies transactions and scheduling, as seen with platforms like PlugShare. Increasing demand for public charging networks in high-traffic locations underlines the need for accessibility, much like the expansion of Tesla Superchargers on busy highways.

Adoption of contactless payment systems enhances user experience and speeds up service, following examples such as Apple Pay integration at ChargePoint stations. These trends reflect a digital transformation in charging solutions.

For instance, a driver can monitor charge status through an app and receive notifications when charging is complete. This real-time data improves efficiency and planning. Digital wallets and contactless systems reduce wait times and address safety concerns. Public-private partnerships and smart city initiatives further encourage the adoption of these technologies, creating a seamless and efficient charging ecosystem.

Regional Analysis

Europe Dominates with 52.7% Market Share

Europe leads the Hypercharger Market with a 52.7% share, amounting to USD 7.06 billion. This dominance is largely driven by aggressive environmental policies, substantial investments in EV infrastructure, and high consumer demand for electric vehicles.

The region benefits from government incentives that support EV adoption, partnerships between governments and private sectors to expand charging networks, and a growing awareness of sustainability issues. Additionally, Europe’s strong automotive industry plays a crucial role in integrating hypercharging technologies with new vehicle models.

The influence of Europe in the global Hypercharger Market is expected to remain strong. The ongoing push towards carbon neutrality and the expansion of electric mobility solutions across the continent are likely to keep Europe at the forefront of hypercharger technology adoption, potentially increasing its market share.

Regional Mentions:

- North America: North America holds a significant position in the Hypercharger Market, driven by technological advancements and regulatory support for sustainable transportation. The region’s commitment to reducing carbon emissions and increasing EV sales fuels its market growth.

- Asia Pacific: Asia Pacific is rapidly advancing in the Hypercharger Market, supported by large-scale EV adoption in countries like China and Japan. Government initiatives and expanding manufacturing capabilities are key factors boosting the market in this region.

- Middle East & Africa: The Middle East and Africa are progressively engaging in the Hypercharger Market with investments in sustainable transportation and smart city initiatives. The region’s focus on diversifying from oil dependency to renewable technologies is enhancing its market presence.

- Latin America: Latin America is slowly adopting hypercharging solutions amidst growing environmental awareness and urbanization. Efforts to modernize transportation infrastructure and increase EV imports are catalyzing the market’s development in this region.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the competitive landscape of the Hypercharger Market, four key players stand out due to their significant market presence and influential roles in shaping industry trends: ABB Ltd., Siemens AG, Tesla, Inc., and Schneider Electric SE.

ABB Ltd. is renowned for its robust offerings in the electric vehicle charging sector, including fast charging solutions that cater to a wide range of automotive applications. ABB’s hyperchargers are noted for their high efficiency and reliability, making them a preferred choice in public and private charging settings across various geographies.

Siemens AG brings its extensive expertise in electrical engineering to the hypercharger market, providing advanced technology solutions that enhance the charging infrastructure. Siemens focuses on integrating renewable energy sources with its charging technology, promoting sustainability in its offerings and supporting the transition to greener transportation options.

Tesla, Inc. has revolutionized the electric vehicle market and its approach to hypercharging infrastructure is no exception. Tesla’s Superchargers are among the fastest in the world, capable of delivering significant charge in minutes. Tesla continues to expand its network globally, ensuring that Tesla vehicle owners have exclusive access to one of the most powerful charging solutions available.

Schneider Electric SE specializes in energy management and automation solutions, and its entry into the hypercharger market complements its broader environmental sustainability goals. Schneider Electric offers innovative charging solutions that emphasize energy efficiency and smart connectivity, aligning with the needs of modern electric vehicles and consumer expectations for rapid charging.

Together, these companies not only lead in technology and innovation but also in deploying new solutions that address the growing demand for efficient and fast charging infrastructure. Their collective efforts are crucial in driving forward the global adoption of electric vehicles, thereby supporting the reduction of carbon emissions and enhancing the overall sustainability of transportation.

Major Companies in the Market

- ABB Ltd.

- Siemens AG

- Tesla, Inc.

- Schneider Electric SE

- ChargePoint Holdings, Inc.

- EVBox Group

- Delta Electronics, Inc.

- Alfen N.V.

- Blink Charging Co.

- Tritium DCFC Limited

- Fastned B.V.

- Electrify America LLC

- Ionity GmbH

Recent Developments

- XPeng and Volkswagen’s Collaboration in China: On January 2025, XPeng announced a partnership with Volkswagen China to establish a super-fast charging network across China. The plan includes deploying 20,000 charging units in 420 cities, accessible to both brands’ vehicle owners. This collaboration combines expertise in high-power liquid-cooled charging technology.

- UK’s Investment in EV Charging Infrastructure: As of January 2025, the UK government approved over £500 million in EV charging projects in 18 months. Key projects include a £100 million network in Wales and a £68 million initiative in West Sussex, expanding public plug points to 73,000 by the end of 2024.

- EVgo’s $1.25 Billion Loan for Charging Expansion: On December 2024, EVgo secured a $1.25 billion loan from the U.S. Department of Energy to install 7,500 EV chargers at 1,100 stations nationwide. The project focuses on 350kW fast chargers and aligns with federal goals to promote EV adoption.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 13.4 Billion |

| Forecast Revenue (2034) | USD 350.5 Billion |

| CAGR (2025-2034) | 38.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (DC Fast Chargers, Ultra-Fast Chargers, Wireless Hyperchargers), By Power Output (Up to 100 kW, 100–200 kW, Above 200 kW), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Buses, Two-Wheelers), By Charging Standard (CCS, CHAdeMO, Tesla Supercharger, GB/T), By End-User (Residential, Commercial – Charging Stations, Parking Spaces, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABB Ltd., Siemens AG, Tesla, Inc., Schneider Electric SE, ChargePoint Holdings, Inc., EVBox Group, Delta Electronics, Inc., Alfen N.V., Blink Charging Co., Tritium DCFC Limited, Fastned B.V., Electrify America LLC, Ionity GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |