Quick Navigation

Report Overview

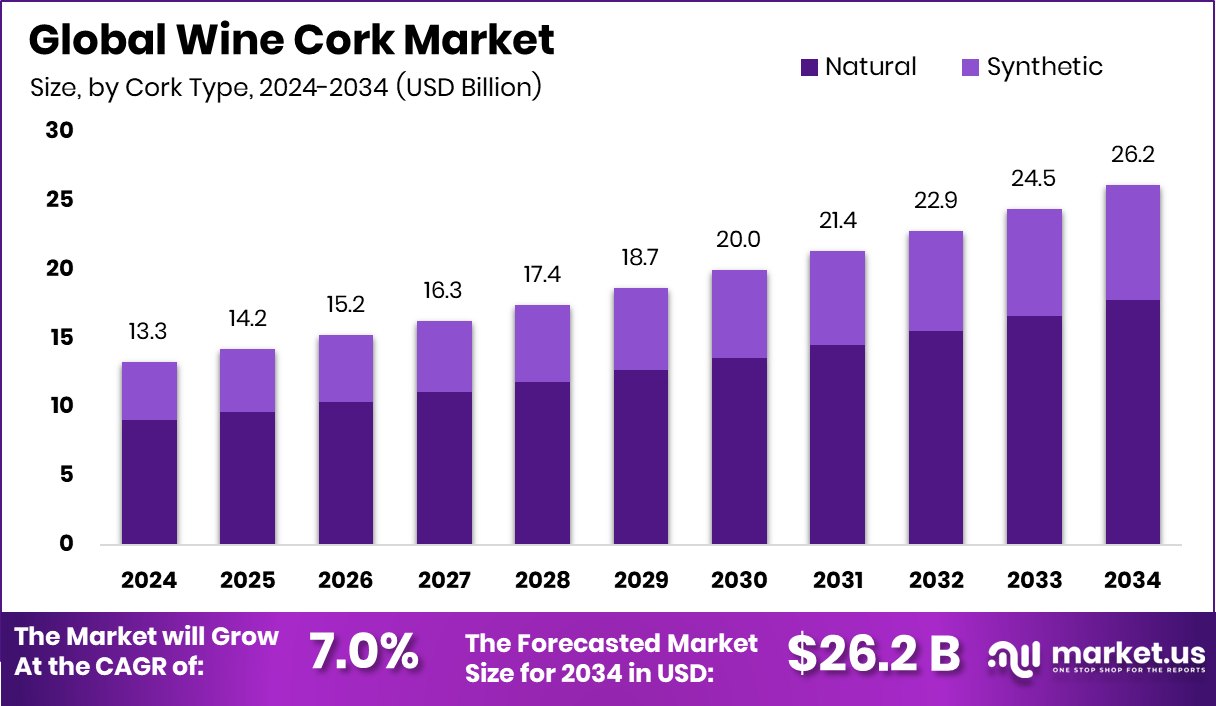

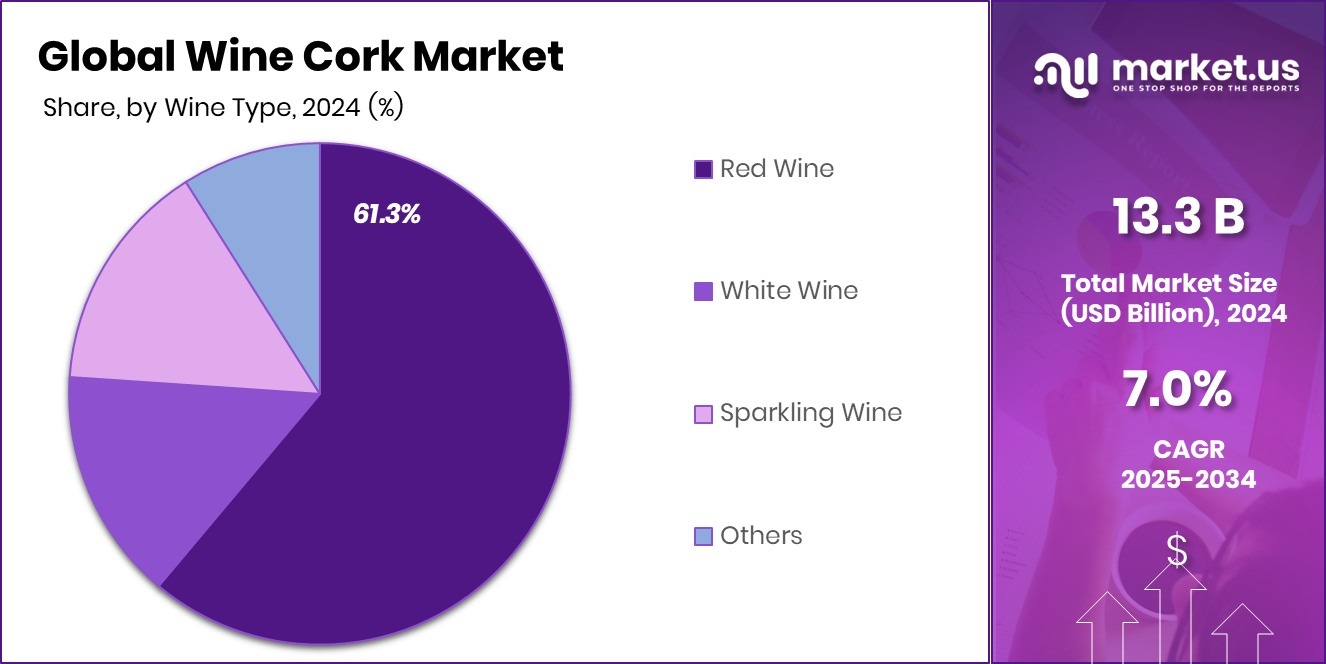

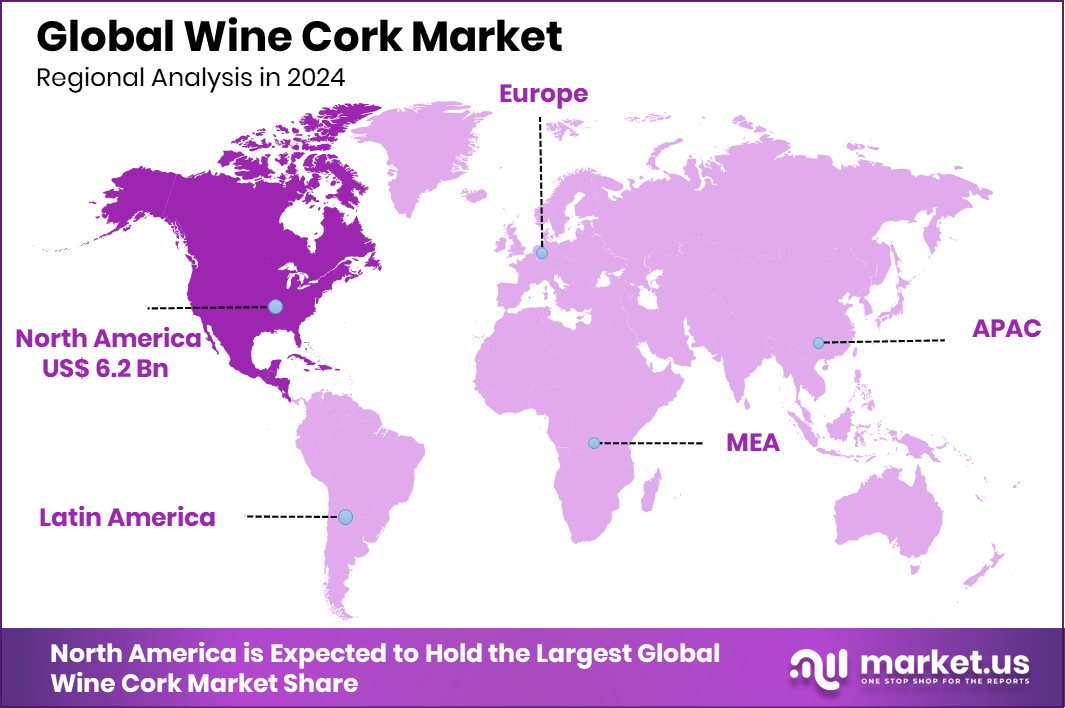

Global Wine Cork Market is expected to be worth around USD 26.2 billion by 2034, up from USD 13.3 billion in 2024, and grow at a CAGR of 7.0% from 2025 to 2034. Wine cork sales in North America reached USD 6.2 Bn, capturing 46.9% share.

A wine cork is a stopper used to seal wine bottles and preserve the liquid inside. Traditionally made from the bark of the cork oak tree, these corks are favored for their elasticity, permeability, and natural origin. While synthetic and screw caps exist, natural cork remains popular for premium wines due to its ability to allow minimal oxygen transfer, which supports aging.

The wine cork market refers to the global industry involved in the production, distribution, and sale of cork stoppers used in wine bottling. It includes both natural and synthetic variants, catering to wineries of all sizes. This market spans multiple regions, especially Europe and South America, where cork oak is cultivated. The market’s size and dynamics depend largely on global wine production volumes, shifting consumer preferences, and packaging innovations.

The wine cork market is growing due to increased global wine consumption and rising premium wine sales. As wineries focus on quality and heritage branding, natural cork’s popularity strengthens. The expansion of vineyards and artisanal wine labels further boosts demand for authentic cork closures. According to an industry report, WineFi raises £1.5M in a Seed round for a fine wine investment platform. Ferovinum secures £17.5M Series A to expand wine and spirits platform.

Demand for wine corks is rising with wine tourism, e-commerce, and growing exports of bottled wine. Consumers associate corked wines with tradition and superior quality. The shift toward sustainable packaging also supports natural cork, given its biodegradable and renewable nature.

Key Takeaways

- Global Wine Cork Market is expected to be worth around USD 26.2 billion by 2034, up from USD 13.3 billion in 2024, and grow at a CAGR of 7.0% from 2025 to 2034.

- In 2024, natural corks held a 69.4% market share due to their premium sealing properties.

- Wood-based corks dominated the market with a 73.7% share, driven by sustainability and traditional preferences.

- Red wine accounted for 61.3% of wine cork usage, reflecting its aging needs and oxygen control.

- In 2024, North America dominated global demand with 46.9%, USD 6.2 Bn.

By Cork Type Analysis

In 2024, natural corks led with a 69.4% share, showing a strong preference.

In 2024, Natural held a dominant market position in the By Cork Type segment of the Wine Cork Market, with a 69.4% share. This strong dominance is primarily driven by increasing consumer and producer preference for sustainable, biodegradable, and traditional wine packaging solutions.

Natural cork, harvested from the bark of cork oak trees, continues to be associated with premium wine quality, heritage, and aging potential, making it the favored choice among both winemakers and high-end consumers. The segment’s performance has been supported by its compatibility with wine preservation, allowing controlled oxygen ingress that enhances the flavor maturation process over time.

Natural cork’s widespread use in the wine industry has also been reinforced by growing environmental awareness. With cork being a renewable and recyclable material, its alignment with eco-conscious trends has significantly contributed to its uptake.

Wine-producing regions with a strong tradition in viticulture, especially across Europe and South America, have continued their reliance on natural cork due to long-standing practices and the value consumers place on authenticity. Additionally, the cork’s ability to reinforce brand identity and elevate product image has made it a strategic packaging choice in the competitive wine market.

By Material Analysis

Wood-based corks dominated the material segment, holding a 73.7% share globally.

In 2024, Wood held a dominant market position in By Material segment of the Wine Cork Market, with a 73.7% share. This dominance reflects the continued industry reliance on natural wooden corks, primarily sourced from cork oak trees, which are preferred for their porous structure, elasticity, and ability to preserve wine quality over time.

Wood-based corks are especially valued in premium wine categories, where aging potential and traditional presentation significantly influence consumer choices. The 73.7% share underscores how wood remains the standard material for sealing wines that are intended to mature in bottles.

The preference for wood as a cork material is also driven by environmental and sustainability factors. Wooden corks are biodegradable, renewable, and recyclable, offering a low carbon footprint compared to synthetic alternatives. Wineries aiming to align with eco-friendly branding and sustainable production practices continue to invest in wood-based closures.

Moreover, the tactile feel and auditory ‘pop’ of a wooden cork remain essential sensory elements in wine consumption experiences, reinforcing authenticity and quality. The segment’s leading market share highlights the trust and tradition associated with wooden corks, ensuring their continued relevance in a competitive and evolving wine packaging landscape.

By Wine Type Analysis

Red wine usage drove demand, accounting for 61.3% of cork applications.

In 2024, Red Wine held a dominant market position in the By Wine Type segment of the Wine Cork Market, with a 61.3% share. This substantial share is primarily attributed to the aging characteristics and storage requirements of red wines, which benefit significantly from cork closures.

Natural corks, often preferred for sealing red wines, allow a controlled amount of oxygen ingress that supports the maturation of complex flavors over time. As red wines are typically cellared longer than white or rosé wines, cork remains the optimal sealing choice, reinforcing the segment’s reliance on traditional closure methods.

The 61.3% dominance also reflects global red wine consumption trends, particularly in markets like Europe, North America, and emerging regions in Asia where premium and vintage wines are gaining popularity. Red wine producers continue to favor corks not just for functionality but for enhancing the perceived quality and presentation of their products.

Moreover, consumers associate cork-sealed red wines with authenticity, heritage, and superior value, further driving demand. The segment’s performance indicates a sustained preference for cork in red wine bottling, maintaining its leadership in the wine cork market as producers prioritize both preservation and brand positioning for their red wine offerings.

Key Market Segments

By Cork Type

- Natural

- Synthetic

By Material

- Wood

- Plastic

- Rubber

- Silicone

- Glass

- Metal

By Wine Type

- Red Wine

- White Wine

- Sparkling Wine

- Others

Driving Factors

Rising Preference for Natural and Eco-Friendly Closures

One of the main driving factors in the wine cork market is the growing preference for natural and eco-friendly packaging. As consumers become more environmentally conscious, there is increased demand for biodegradable and renewable materials, making natural cork a top choice. Unlike plastic or metal closures, cork is harvested sustainably from cork oak trees without harming them.

This aligns well with the sustainability goals of many wineries and appeals to green-minded consumers. Moreover, natural cork enhances wine aging and flavor, offering both functional and ecological advantages. This dual benefit—environmental and performance-based—is boosting cork usage globally, especially for premium wines.

Restraining Factors

Growing Popularity of Synthetic and Screw Cap Closures

A major restraining factor for the wine cork market is the rising popularity of synthetic and screw cap closures. These alternatives are often more affordable, easier to open, and do not pose the risk of “cork taint”—a condition caused by a compound called TCA that can spoil wine. For mass-produced or budget wines, screw caps are especially preferred due to their consistency and low cost.

Additionally, some regions like Australia and New Zealand have widely adopted non-cork closures, challenging traditional cork usage. As winemakers seek cost-effective and convenient sealing solutions, the competition from synthetic materials and metal caps continues to limit the full potential growth of natural cork in certain market segments.

Growth Opportunity

Expanding Wine Industry in Emerging Global Markets

A key growth opportunity for the wine cork market lies in the expanding wine industry across emerging markets such as China, India, Brazil, and South Africa. As wine consumption grows in these countries, both domestic production and imports are increasing. Wineries in these regions are beginning to adopt traditional practices, including the use of natural corks for premium wines.

With rising disposable incomes and changing lifestyles, consumers in these markets are showing more interest in aged and high-quality wines, where cork closures are often preferred. This creates a new demand base for cork manufacturers. As wine culture spreads beyond traditional Western regions, the wine cork market can grow by tapping into these new and fast-developing opportunities.

Latest Trends

Increased Use of Recycled and Biodegradable Corks

A notable trend in the wine cork market is the growing adoption of recycled and biodegradable cork materials. As environmental concerns gain prominence, wineries are increasingly seeking sustainable packaging solutions. Recycled corks, often made from repurposed cork waste, offer an eco-friendly alternative without compromising the quality of wine preservation.

Biodegradable corks, designed to break down naturally over time, further align with the industry’s shift towards sustainability. This trend reflects a broader movement within the wine industry to reduce environmental impact and meet consumer demand for greener products.

Regional Analysis

North America held a 46.9% share in the Wine Cork Market, valued at USD 6.2 Bn.

In 2024, North America held a dominant position in the global Wine Cork Market, accounting for 46.9% of the total share and reaching a value of USD 6.2 billion. This leadership is largely attributed to the region’s strong wine production and consumption base, particularly in the United States, which is among the largest wine-consuming countries globally.

The preference for natural and sustainable cork closures among premium wine brands has significantly contributed to market growth in North America. Europe remains a vital region as well, supported by long-established wine traditions and high-quality cork manufacturing, especially in countries like Portugal and Spain.

In Asia Pacific, the market is gradually expanding with increasing urbanization and growing consumer interest in wine culture, particularly in China and Japan. The Middle East & Africa and Latin America show modest growth, with Latin America benefiting from wine production hubs such as Argentina and Chile. However, their market values remain comparatively lower than those of North America.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, J. C. RIBEIRO continued to maintain its reputation as a specialized player in the wine cork market by focusing on high-quality cork production. The company’s strength lies in its ability to balance tradition with modern processing standards. J. C. RIBEIRO’s corks are known for their premium quality, serving boutique wineries and export-focused wine producers. Their focus on maintaining strict quality control and traceability in sourcing cork wood further reinforces their credibility among wine producers that value consistency and sustainability.

Korkindustrie GmbH & Co. KG, a Germany-based cork manufacturer, strengthened its market presence through its efficient production systems and reliability in supply. The company is well-integrated into the European supply chain, catering especially to wine producers in Central and Eastern Europe. Its long-standing industry relationships and ability to meet both large-volume and specialty cork orders have helped it maintain steady growth.

Lafitte, with its heritage rooted in French winemaking traditions, remains a respected name in the wine cork sector. Known for its natural corks, Lafitte’s stronghold is in supplying premium cork closures to both local and international wine markets. The company continued to benefit in 2024 from increased demand for natural corks and heightened awareness around eco-friendly wine packaging.

Top Key Players in the Market

- A. Silva USA LLC

- Advance Cork International

- Allstates Rubber & Tool Corp

- Amorim Cork S.A

- Bangor Cork

- C. Ribeiro S. A

- DIAM BOUCHAGE SAS

- J. C. RIBEIRO

- Korkindustrie GmbH & Co. KG

- Lafitte

- PORTOCORK AMERICA

- Precisionelite

- Sugherificio Martinese & Figli Srl

- Vinventions

- Waterloo Container Company

Recent Developments

- In March 2025, DIAM Bouchage expanded its “Origine by Diam” range of bio-sourced corks. The range now includes four options: Origine 3, 5, 10, and 30. These corks are designed to meet various aging potentials and oxygen requirements, providing winemakers with sustainable choices tailored to their wines.

- In 2024, Amorim partnered with Rockwell Group, BlueWell, and Southern Glazer’s Wine & Spirits to launch the Cork Collective recycling program in New York. This initiative collects used cork stoppers from hotels and restaurants, repurposing them for community projects and promoting environmental sustainability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 13.3 Billion |

| Forecast Revenue (2034) | USD 26.2 Billion |

| CAGR (2025-2034) | 7.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Cork Type (Natural, Synthetic), By Material (Wood, Plastic, Rubber, Silicone, Glass, Metal), By Wine Type (Red Wine, White Wine, Sparkling Wine, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | A. Silva USA Llc, Advance Cork International, Allstates Rubber & Tool Corp, Amorim Cork S.A, Bangor Cork, C. Ribeiro S. A, DIAM BOUCHAGE SAS, J. C. RIBEIRO, Korkindustrie GmbH & Co. KG, Lafitte, PORTOCORK AMERICA, Precisionelite, Sugherificio Martinese & Figli Srl, Vinventions, Waterloo Container Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |